Gold prices tick higher on fresh U.S. tariff threats, Fed rate cut hopes

Introduction & Market Context

LCI Industries (NYSE:LCII) presented its second quarter 2025 earnings results on August 5, 2025, highlighting revenue growth despite a challenging recreational vehicle market environment. The company’s stock was trading down 1.37% in premarket at $94.62, suggesting investors may have concerns about margin pressure and tariff impacts despite the revenue growth.

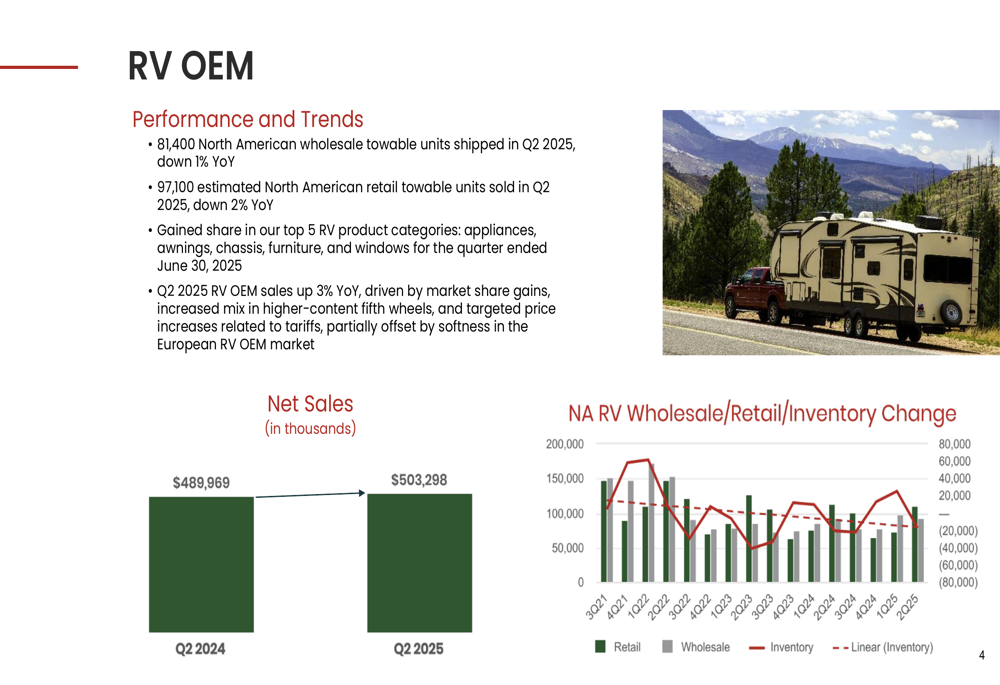

The company continues to navigate a relatively flat RV market, with North American wholesale towable units down 1% year-over-year and retail units down 2%. However, LCI’s strategic diversification into adjacent markets and focus on innovation has enabled it to outperform the broader market.

Quarterly Performance Highlights

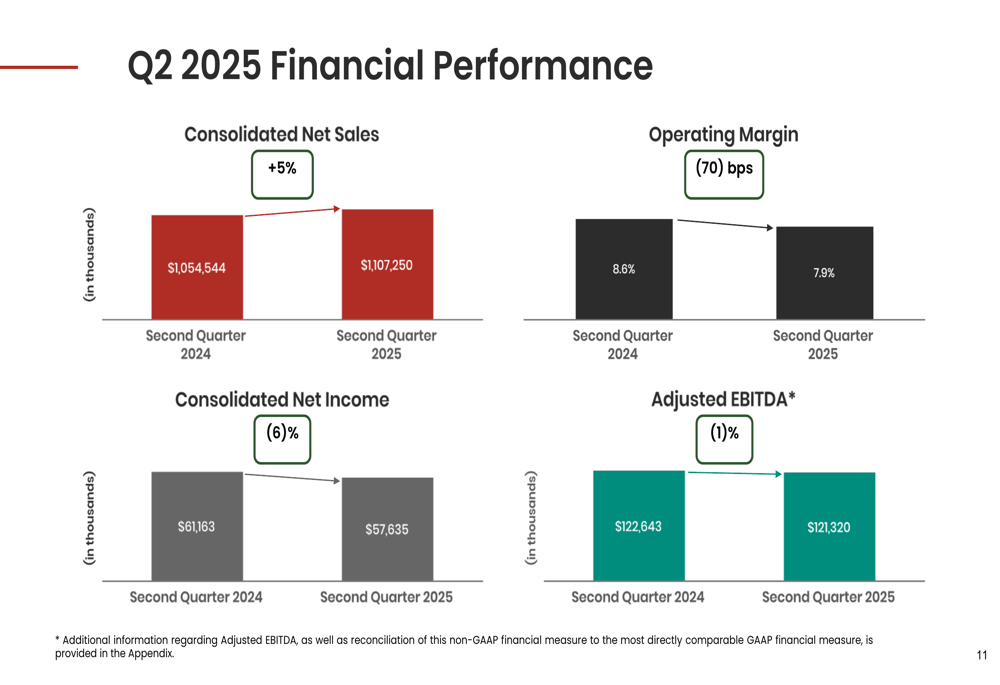

LCI Industries reported net sales of $1.1 billion for Q2 2025, representing a 5% increase year-over-year. However, net income declined 6% to $58 million ($2.29 per diluted share), while adjusted net income reached $60 million ($2.39 per adjusted diluted share).

As shown in the following financial performance chart, operating margin contracted by 70 basis points year-over-year to 7.9%, though it improved sequentially from 7.8% in Q1 2025:

The company’s RV OEM segment, which remains its largest business, saw sales increase 3% year-over-year to $503.3 million despite the slight decline in wholesale shipments. This growth indicates market share gains and increased content per unit. The Adjacent Industries segment delivered even stronger growth of 10% year-over-year, primarily driven by recent acquisitions.

The following chart illustrates LCI’s RV OEM performance relative to the broader market:

LCI’s aftermarket segment also showed positive momentum with sales up 4% year-over-year to $267.7 million, though margins contracted by 200 basis points. The company attributes this growth to meeting heightened repair and replacement demand while expanding its portfolio in diversified markets.

Strategic Initiatives

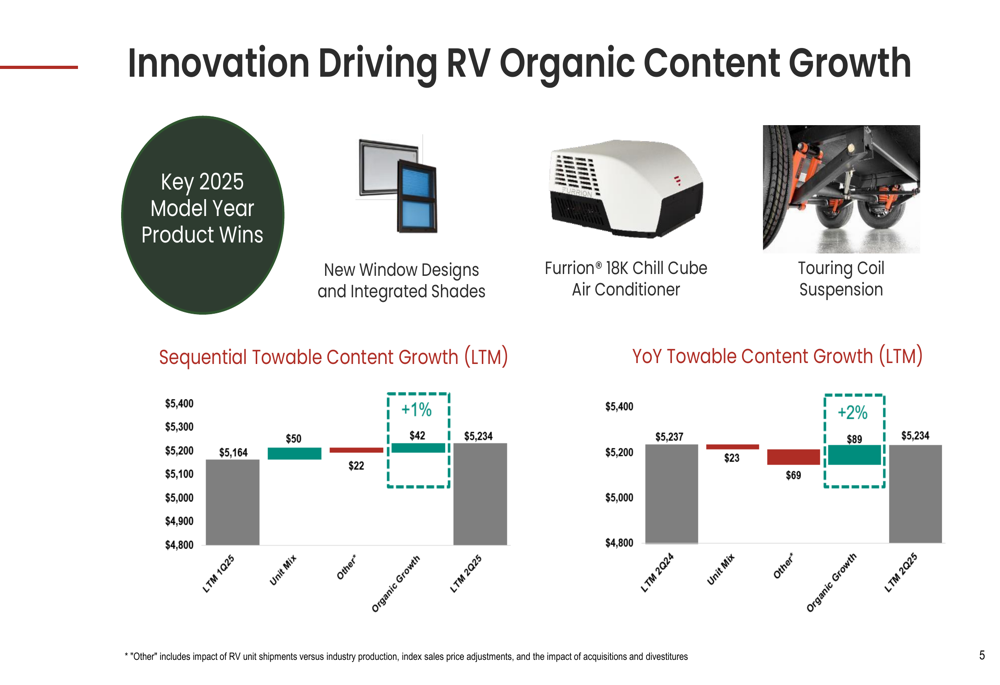

Innovation remains a key driver of LCI’s growth strategy, particularly in increasing content per RV. The company highlighted several 2025 model year product wins, including new window designs with integrated shades, the Furrion 18K Chill Cube air conditioner, and touring coil suspension systems.

The following chart demonstrates how these innovations are driving organic content growth in the RV segment:

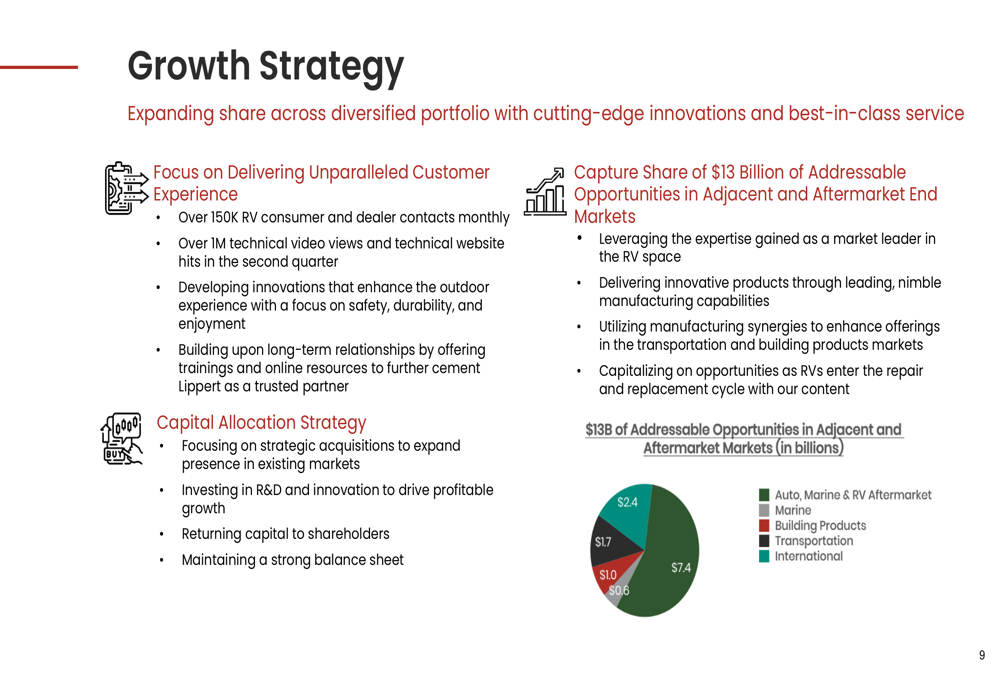

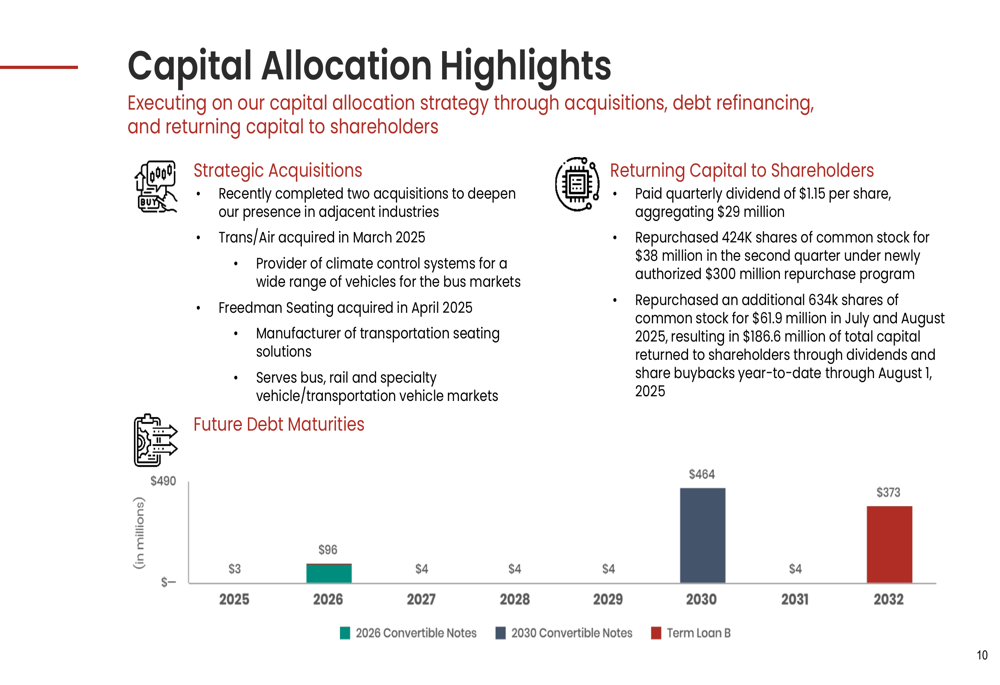

Beyond the RV market, LCI continues to pursue a diversification strategy targeting adjacent markets with an estimated $13 billion of addressable opportunities. The company’s capital allocation strategy balances strategic acquisitions, debt management, and shareholder returns.

The breakdown of these market opportunities is illustrated in the following chart:

In line with this strategy, LCI completed two strategic acquisitions in early 2025: Trans/Air in March and Freedman Seating in April. These acquisitions strengthen the company’s position in the transportation segment, which grew to $79 million in quarterly sales, up from $54 million in Q2 2024.

The company also maintained its commitment to shareholder returns, paying a quarterly dividend of $1.15 per share (totaling $29 million) and repurchasing 424,000 shares of common stock for $38 million during the quarter.

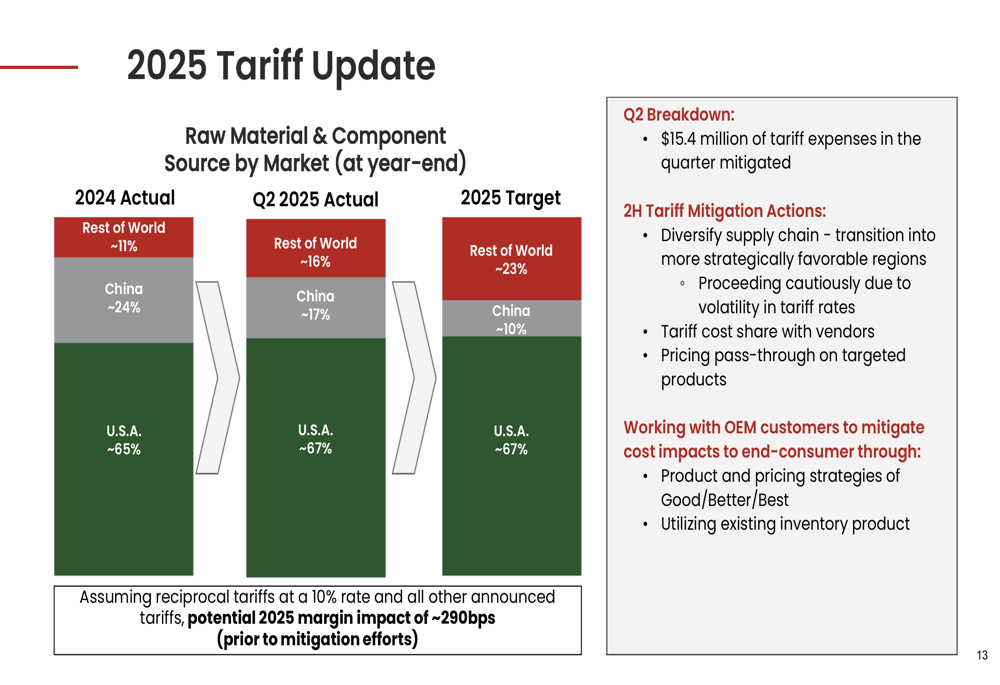

Tariff Impact and Mitigation

A significant focus of LCI’s presentation was its strategy to mitigate the impact of tariffs. The company reported $15.4 million in tariff expenses during Q2 that were successfully mitigated. However, assuming reciprocal tariffs at a 10% rate and all other announced tariffs, LCI faces a potential 2025 margin impact of approximately 290 basis points before mitigation efforts.

The company is actively working to address these challenges through three primary strategies: diversifying its supply chain, sharing tariff costs with vendors, and implementing targeted price increases. The following chart shows LCI’s progress in reducing its reliance on Chinese suppliers:

As shown in the chart, LCI has reduced its sourcing from China from 24% at the end of 2024 to 17% by Q2 2025, with a target of further reduction to 10% by the end of 2025. Meanwhile, sourcing from the U.S. has increased from 65% to 67%, with sourcing from other international markets growing from 11% to 16% (targeting 23% by year-end).

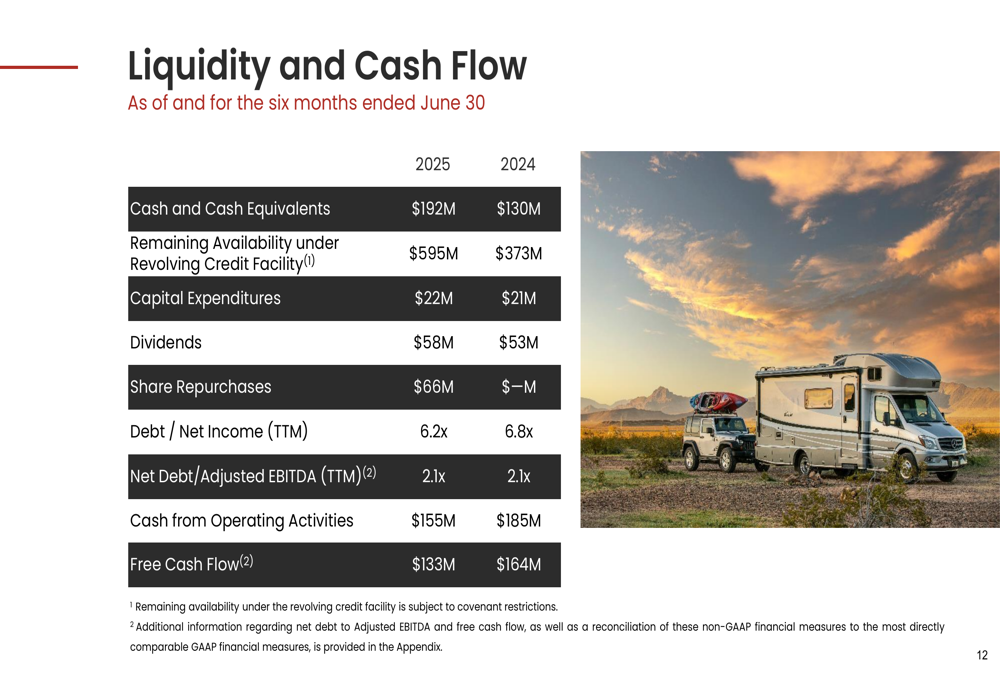

Liquidity and Financial Position

Despite margin pressures and ongoing investments in acquisitions and shareholder returns, LCI maintains a strong liquidity position with $192 million in cash and cash equivalents as of June 30, 2025, up from $130 million a year earlier. The company also has $595 million available under its revolving credit facility, compared to $373 million in the prior year.

The following chart details LCI’s liquidity and cash flow metrics:

Free cash flow for the first six months of 2025 was $133 million, down from $164 million in the same period of 2024. The company’s leverage ratio (net debt to adjusted EBITDA) remained stable at 2.1x, while debt to net income improved to 6.2x from 6.8x a year earlier.

Forward-Looking Statements

Looking ahead, LCI expects the North American RV industry to ship between 320,000 and 350,000 wholesale units in 2025. The company reported that consolidated July 2025 sales were up 5% year-over-year, suggesting a continuation of Q2’s growth trajectory.

In the marine segment, LCI anticipates continued slowness for the remainder of 2025 due to ongoing challenges with inflation and interest rates. However, the company remains optimistic about expansion opportunities in transportation, building products, and utility trailer markets.

On the cost front, LCI stated it is on track to deliver an 85 basis point margin improvement in 2025 through various cost reduction initiatives, which would help offset some of the tariff-related pressures.

The company’s focus on innovation, diversification, and operational efficiency positions it to navigate the current market challenges while pursuing long-term growth opportunities across its expanding portfolio of businesses.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.