Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Leggett & Platt Incorporated (NYSE:LEG) released its second quarter 2025 presentation on July 31, showing improved margins despite continued sales pressure. The diversified manufacturer reported Q2 sales of $1.1 billion, down 6% year-over-year, while adjusted earnings per share increased slightly to $0.30. Despite exceeding revenue expectations, LEG shares fell 9.48% following the earnings release, closing at $9.55, as investors remained concerned about ongoing volume declines.

The company’s presentation highlighted progress on its restructuring initiatives and debt reduction efforts, while maintaining its full-year guidance. Management noted that demand remains pressured due to economic uncertainty, though the benefits from restructuring are beginning to materialize in improved margins.

Quarterly Performance Highlights

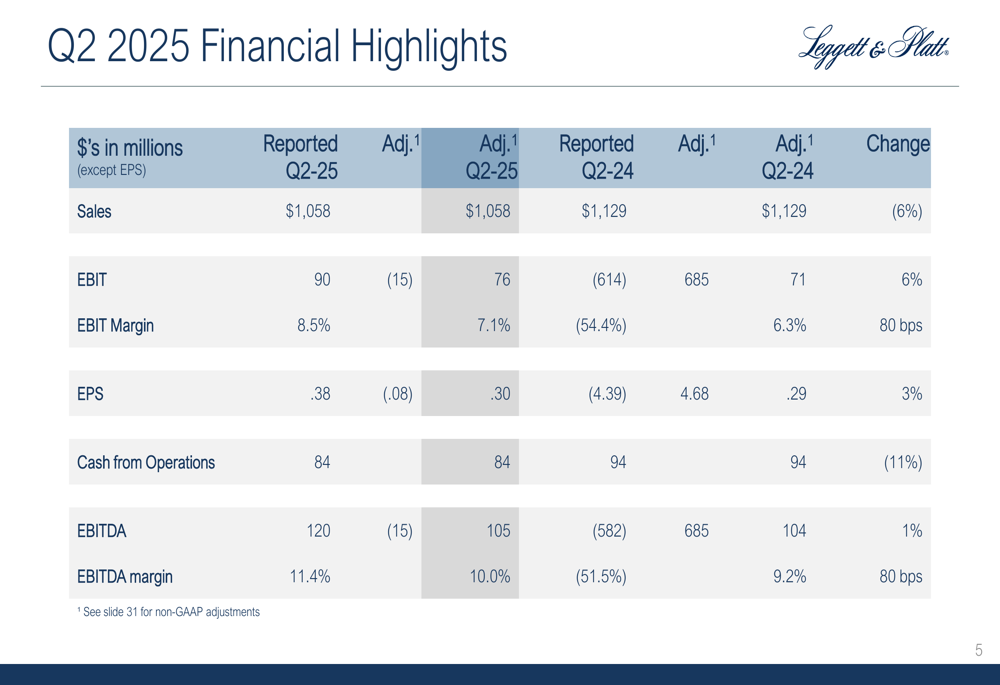

Leggett & Platt’s Q2 2025 results showed a mixed performance with sales declining but profitability metrics improving. The company reported Q2 sales of $1.058 billion, down 6% from $1.129 billion in Q2 2024. Volume decreased by 7%, partially offset by a 1% benefit from raw material-related pricing and currency impacts.

Despite lower sales, adjusted EBIT increased to $76 million, up $4 million or 6% from Q2 2024, while adjusted EBIT margin improved 80 basis points to 7.1%. Adjusted EPS rose slightly to $0.30, compared to $0.29 in the same period last year.

As shown in the following comprehensive financial highlights table:

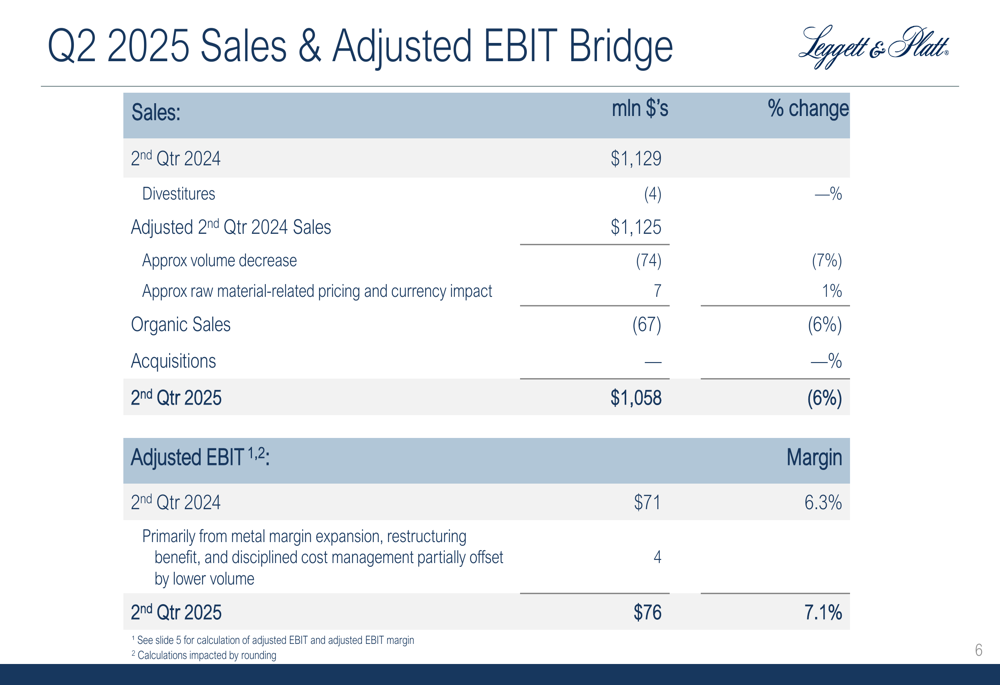

The company’s Q2 2025 EBIT bridge reveals that metal margin expansion, restructuring benefits, and disciplined cost management helped offset the negative impact of lower volume:

Cash flow from operations totaled $84 million in Q2 2025, down $10 million or 11% compared to the same period last year. The company maintained its full-year cash flow guidance of $275-$325 million.

Debt Reduction Progress

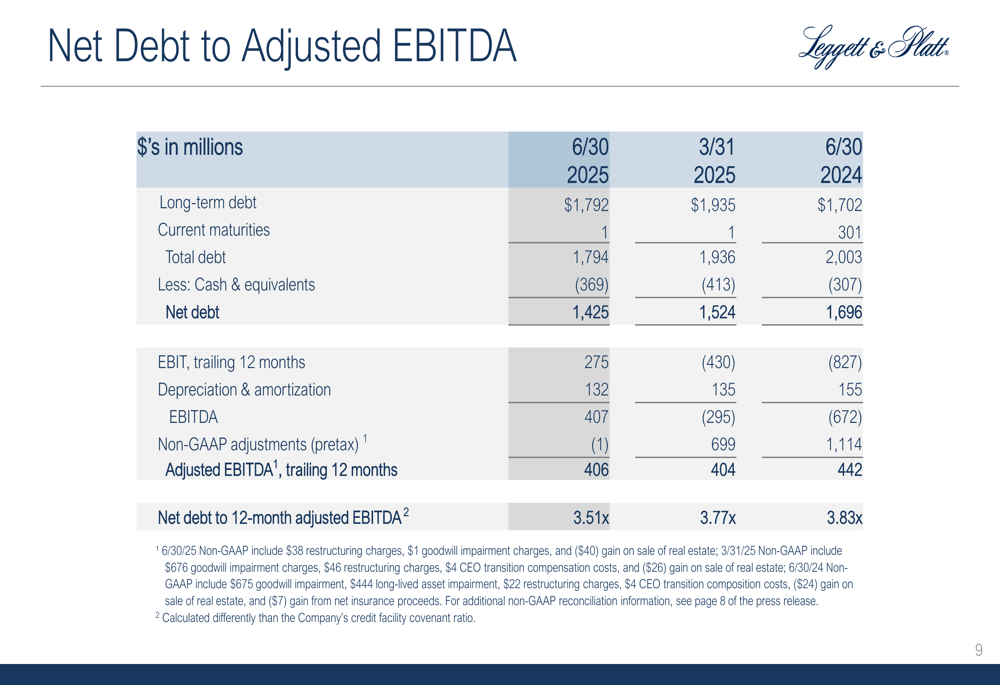

Leggett & Platt made significant progress in strengthening its balance sheet during the quarter. Total (EPA:TTEF) debt decreased to $1.794 billion as of June 30, 2025, down from $2.003 billion a year earlier. Net debt (total debt less cash and equivalents) declined to $1.425 billion from $1.696 billion in the prior year.

The company’s net debt to adjusted EBITDA ratio improved to 3.51x, compared to 3.77x at the end of Q1 2025 and 3.83x a year ago, demonstrating continued progress toward deleveraging.

The following chart illustrates the company’s debt reduction and EBITDA performance:

Working capital management also showed improvement, with working capital excluding cash and current debt/lease liabilities at 14.7% of annualized sales as of June 30, 2025, down from 15.0% at the end of Q1 2025.

Restructuring Initiatives

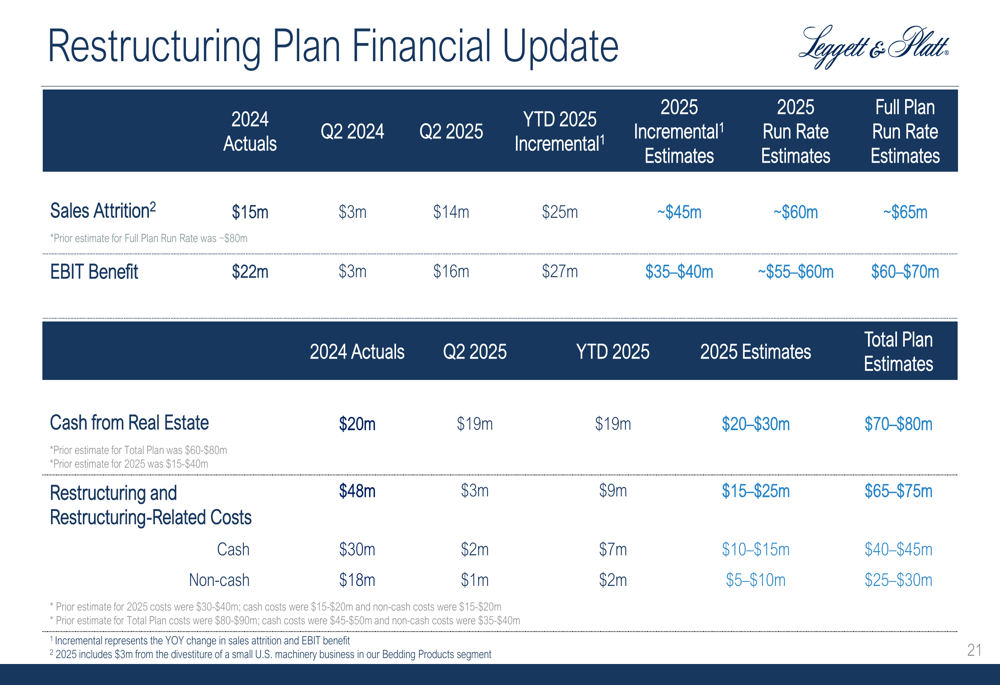

Leggett & Platt’s restructuring program continued to deliver benefits in Q2 2025. The company reported $16 million in EBIT benefits from restructuring during the quarter, compared to just $3 million in Q2 2024. Year-to-date incremental EBIT benefits reached $27 million, with full-year 2025 incremental benefits expected to be $35-$40 million.

The company has made significant progress on its restructuring initiatives across all segments. In Bedding Products, LEG divested a small U.S. machinery business, sold two properties, and largely completed its Specialty Foam consolidation. In Furniture, Flooring & Textile Products, the company launched Phase 2 of its Flooring Products restructuring, while in Specialized Products, it continued to make progress on manufacturing efficiency improvements.

The comprehensive financial update on the restructuring plan shows strong progress toward targets:

Restructuring and restructuring-related costs for 2025 are now expected to be $15-$25 million, lower than initially projected, with $9 million incurred year-to-date.

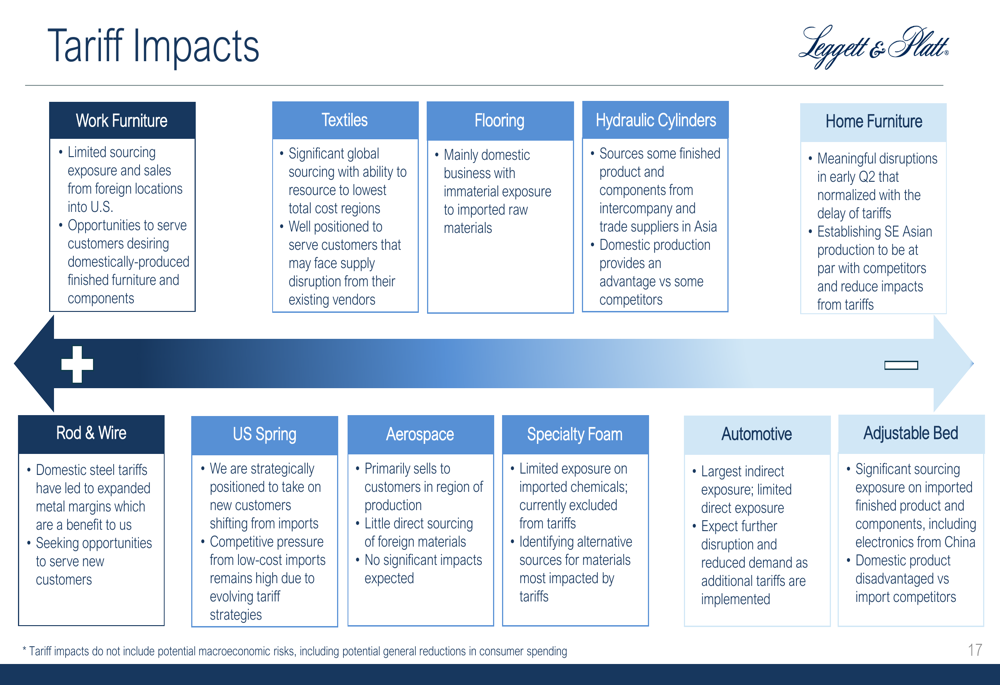

Tariff Impacts and Mitigation

Leggett & Platt provided a detailed overview of tariff impacts across its business segments, highlighting both challenges and opportunities. The company’s exposure varies significantly by segment, with some businesses well-positioned to benefit from shifts toward domestic production, while others face headwinds.

The following chart details the tariff impacts by business segment:

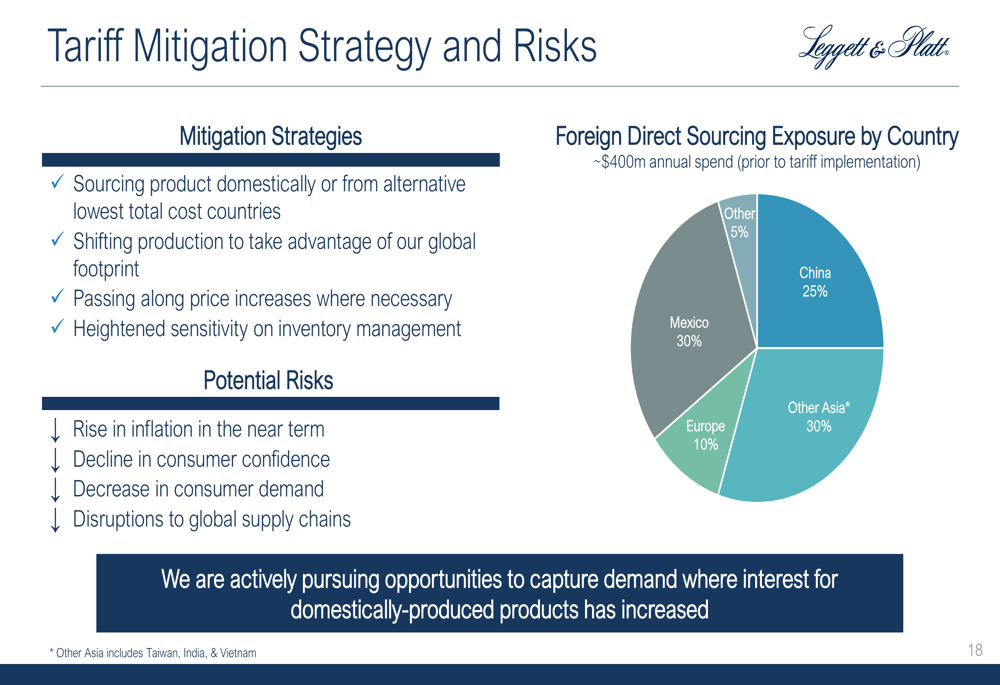

To mitigate tariff risks, Leggett & Platt is implementing several strategies, including sourcing products domestically or from alternative lowest total cost countries, shifting production to leverage its global footprint, passing along price increases where necessary, and maintaining heightened sensitivity on inventory management.

The company’s foreign direct sourcing exposure is diversified across regions, with 30% from Mexico, 25% from China, 30% from other Asian countries (including Taiwan, India, and Vietnam), 10% from Europe, and 5% from other regions.

Forward-Looking Statements

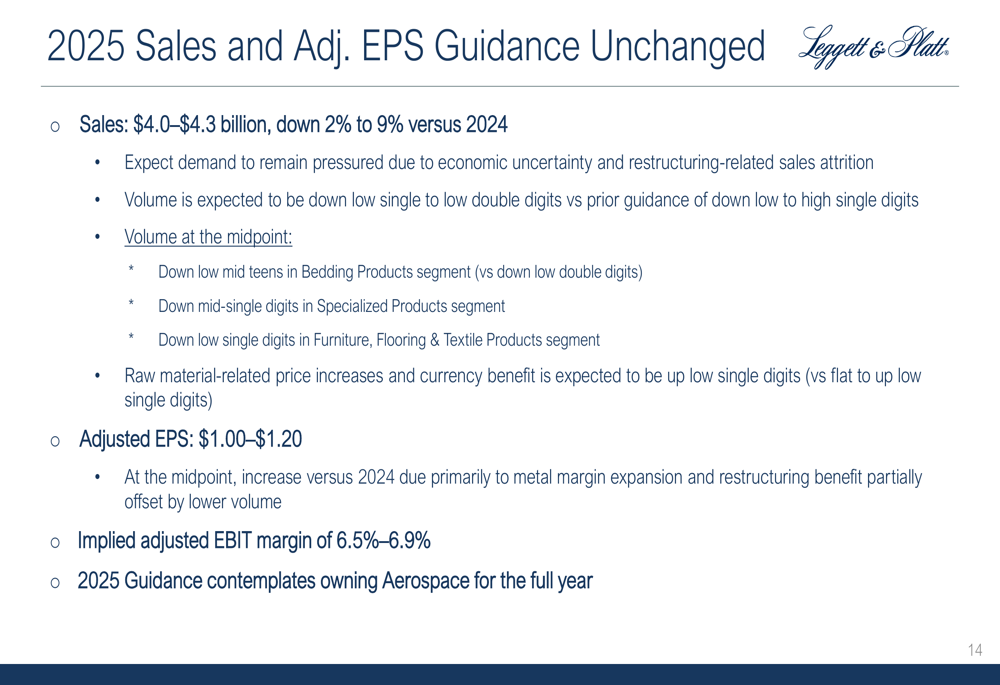

Leggett & Platt maintained its 2025 guidance, projecting sales of $4.0-$4.3 billion (down 2% to 9% versus 2024) and adjusted EPS of $1.00-$1.20. The company expects volume to be down low single to low double digits, a slightly more pessimistic outlook than its previous guidance of down low to high single digits.

By segment, volume at the midpoint of guidance is expected to be down low mid-teens in Bedding Products (versus previous guidance of down low double digits), down mid-single digits in Specialized Products, and down low single digits in Furniture, Flooring & Textile Products.

The company anticipates an implied adjusted EBIT margin of 6.5%-6.9% for the full year, with benefits from metal margin expansion and restructuring partially offsetting the impact of lower volume.

Additional guidance includes depreciation and amortization of approximately $125 million (down from previous guidance of $135 million), net interest expense of approximately $70 million, a tax rate of approximately 26% (up from 25%), and capital expenditures of $80-90 million (down from approximately $100 million).

Despite the challenging sales environment, CEO Karl Glassman expressed confidence in the company’s position, stating, "When the consumer reengages, I am extremely confident this company is in a position of strength." He also highlighted the company’s improved efficiency and financial soundness, saying, "We are more efficient, more agile and more financially sound."

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.