IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

LENZ Therapeutics (NASDAQ:LENZ) recently presented its corporate strategy and product pipeline, highlighting the company’s focus on addressing presbyopia, an age-related vision condition affecting approximately 128 million Americans. The presentation, dated May 2025, comes as the company approaches a critical FDA decision date for its lead product candidate, LNZ100, a novel aceclidine-based eye drop formulation.

The company’s stock closed at $28.18 on May 27, 2025, up 1.86% for the day, and has shown significant growth over the past year with a 54% return despite recent volatility. LENZ currently trades well above its 52-week low of $14.42, though below its high of $38.93.

Executive Summary

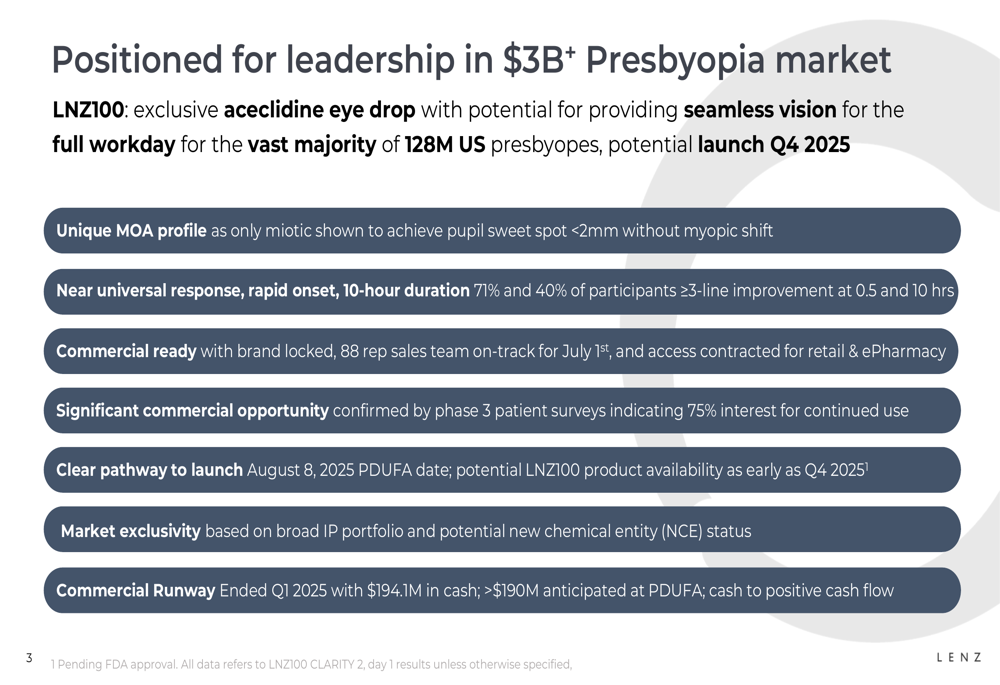

LENZ Therapeutics is positioning LNZ100 (1.75% aceclidine) as a potential first-in-class treatment for presbyopia, with a PDUFA target date of August 8, 2025, and anticipated commercial launch in Q4 2025. The company maintains a strong cash position of $194.1 million as of Q1 2025, which management believes will sustain operations through to positive cash flow.

As shown in the following summary slide, the company is targeting a substantial market opportunity with a comprehensive commercial strategy:

The presentation emphasized LNZ100’s unique mechanism of action that creates a "pupil sweet spot" of less than 2mm without causing myopic shift, which differentiates it from competing approaches. Clinical data demonstrated that 71% of patients achieved a 3-line or greater improvement in near vision at the primary endpoint of 3 hours post-administration.

Product Profile and Clinical Data

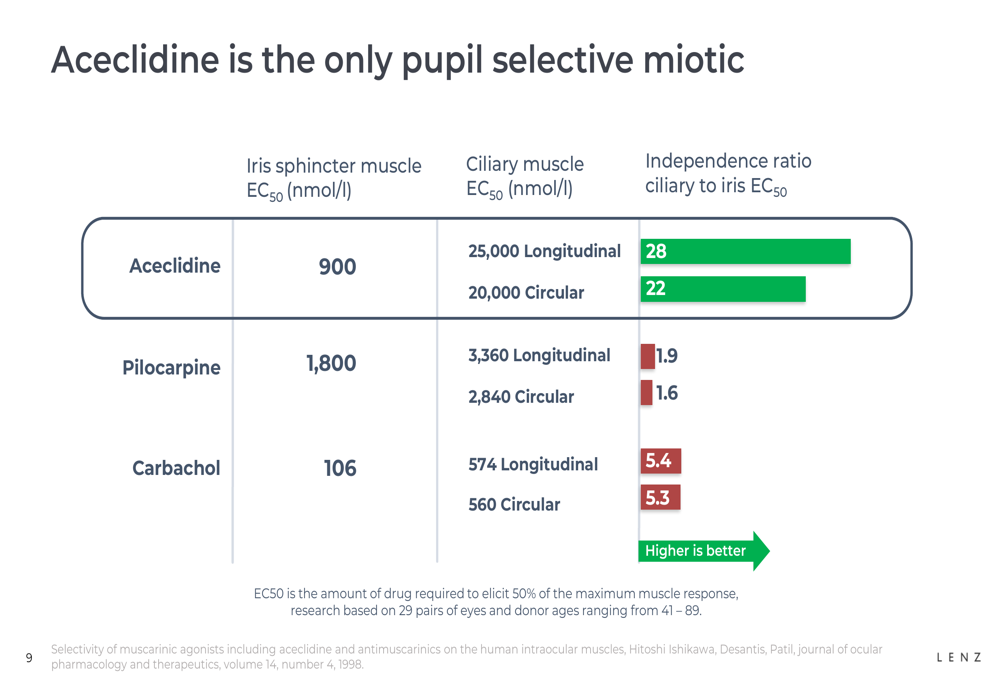

LNZ100 is a preservative-free eye drop containing 1.75% aceclidine, which the company describes as the first and only "pupil selective miotic" for presbyopia treatment. The product’s mechanism of action focuses on creating a pinhole pupil effect without the myopic shift that can compromise distance vision.

The following slide illustrates aceclidine’s selective action on iris muscles compared to other miotics:

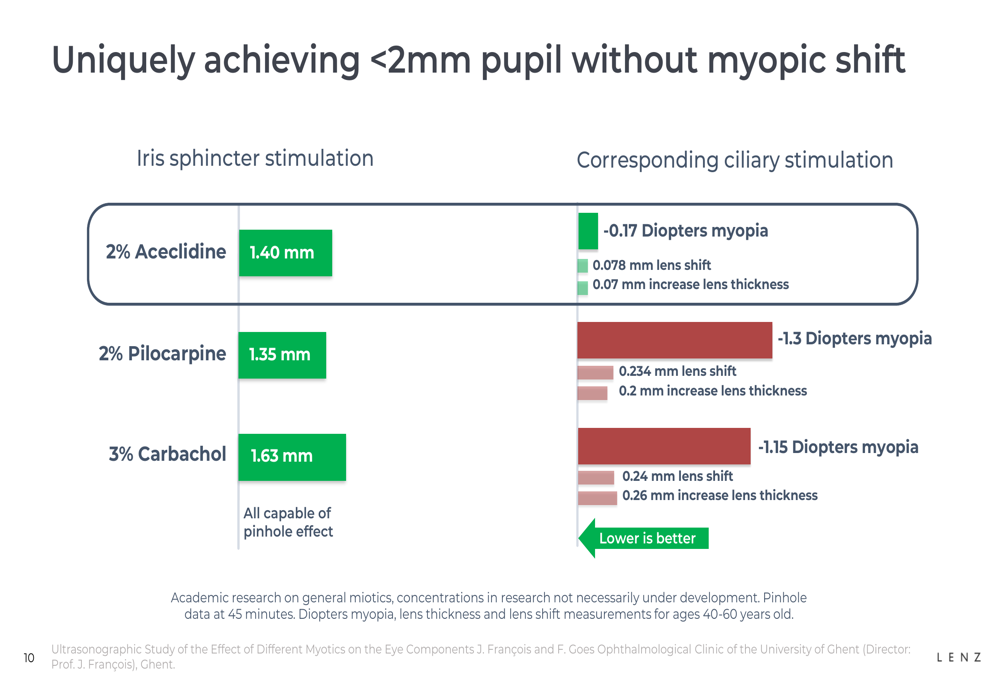

This selectivity translates to clinical advantages, as shown in the comparison of pupil effects versus myopic shift:

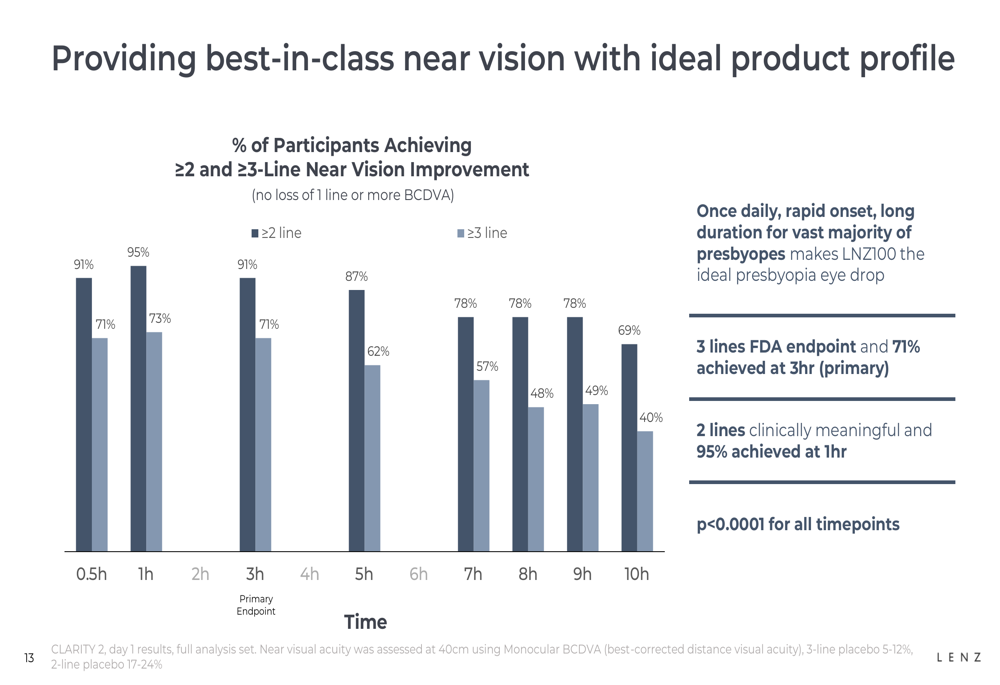

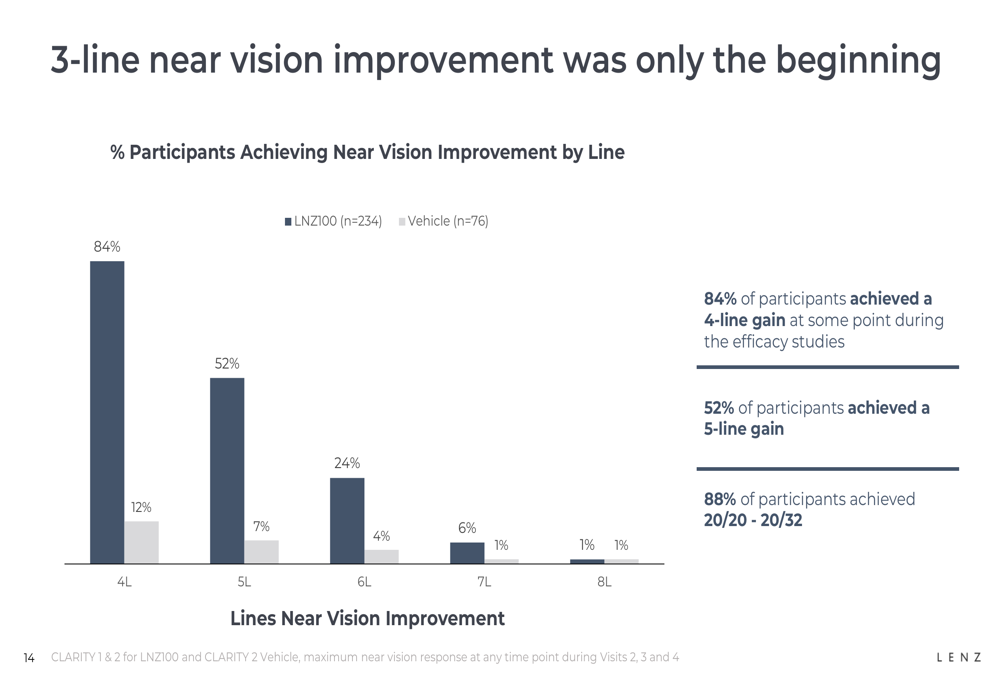

The CLARITY Phase 3 clinical program included three studies with over 600 participants aged 45-75 years. Results demonstrated robust efficacy with rapid onset and sustained duration of action:

The clinical benefits extended beyond the primary endpoint, with many patients achieving even greater vision improvement:

Safety data from the trials showed that LNZ100 was well-tolerated, with the vast majority of adverse events reported as mild. The most common side effects included instillation site irritation (20.1%), visual impairment (13.2%), and hyperemia (9.0%), all of which were classified as mild in severity.

Commercial Strategy and Market Opportunity (SO:FTCE11B)

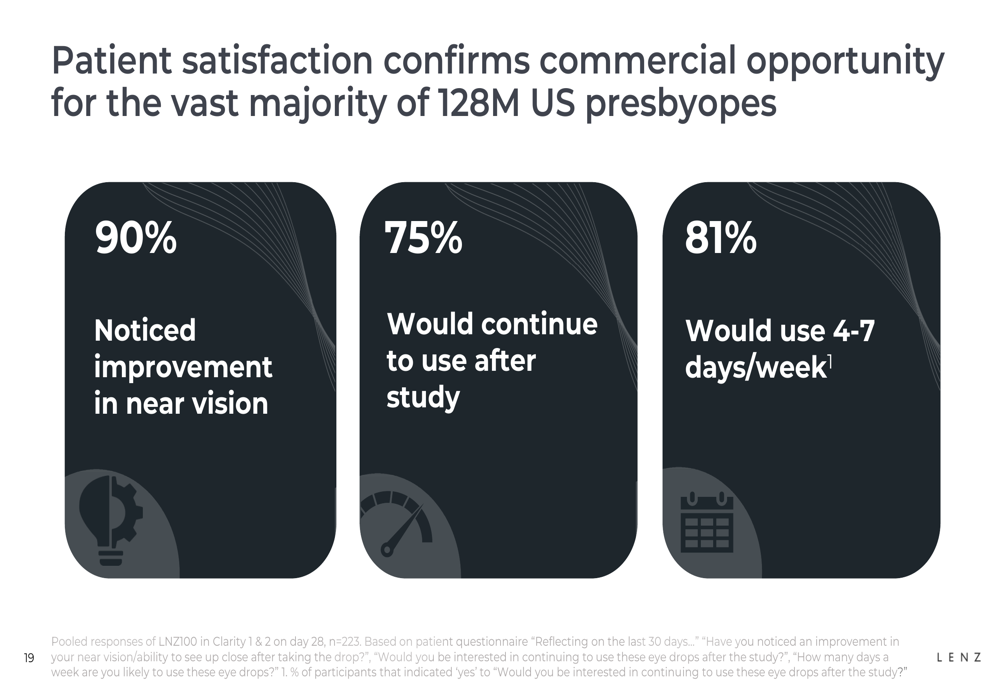

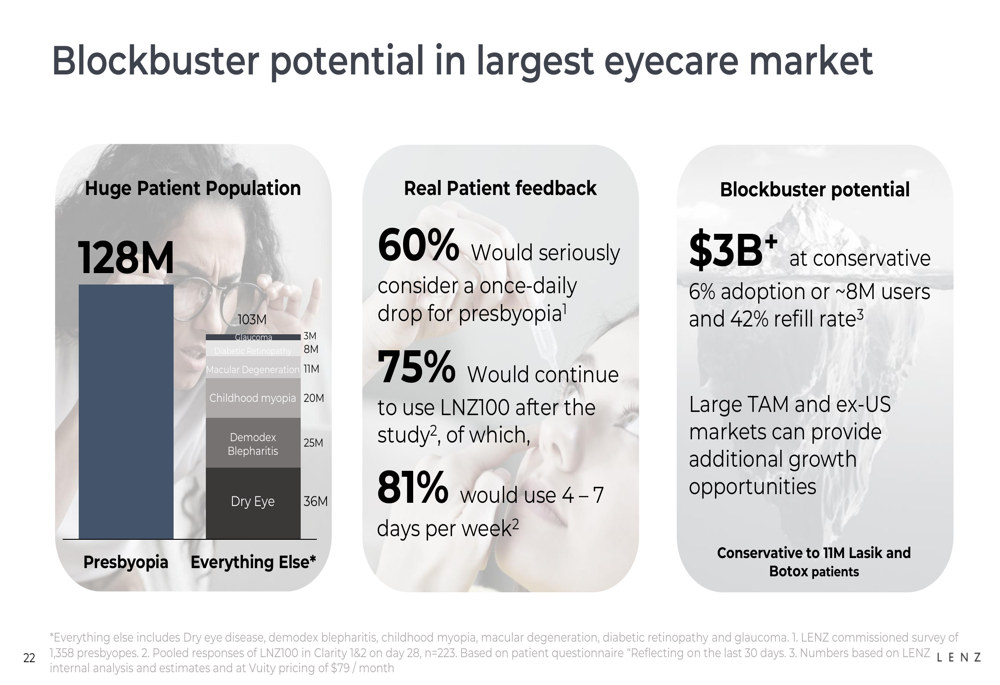

LENZ Therapeutics is targeting what it estimates as a $3+ billion market opportunity in the United States alone. The company’s market research indicates strong interest among both patients and eye care professionals:

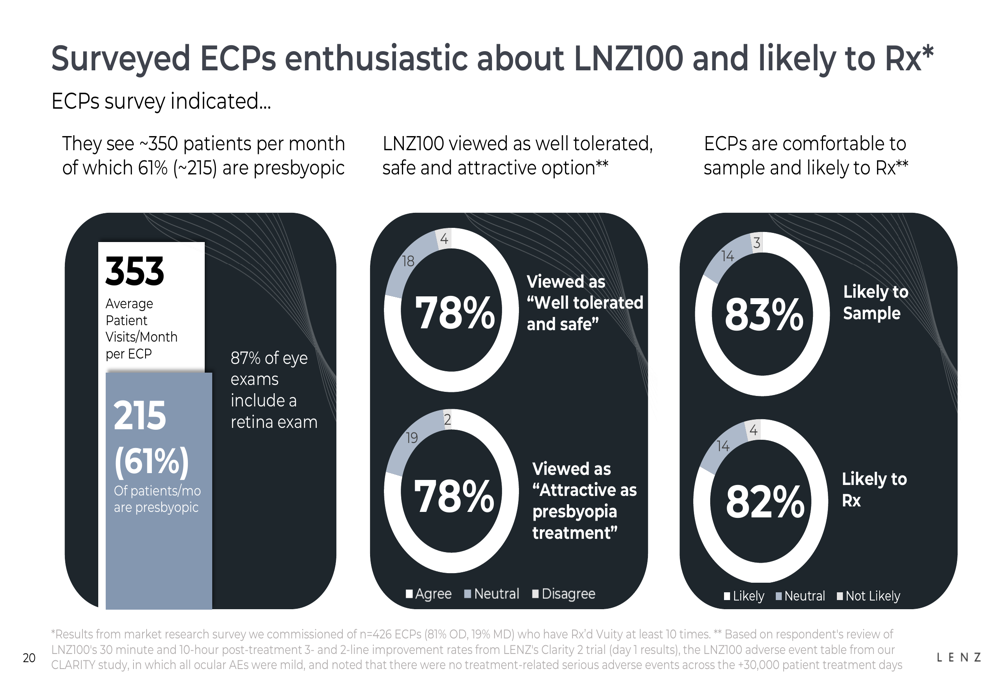

This patient satisfaction is complemented by enthusiasm from eye care professionals, who would be the primary prescribers:

The company’s commercial strategy focuses on three key pillars: encouraging doctor recommendations, building consumer brand awareness, and creating a seamless patient journey. LENZ has already begun implementing this strategy with an unbranded awareness campaign featuring over 50 key opinion leaders.

The market potential is substantial, as illustrated in the following slide:

Financial Position and Outlook

LENZ reported a cash position of $194.1 million as of Q1 2025, with a net cash burn of $15 million during the quarter. Operating expenses increased to $16.9 million, up 11% from Q4 2024, while SG&A expenses nearly doubled year-over-year to $11.3 million, reflecting the company’s preparations for commercial launch.

The company’s net loss per share improved significantly to $0.53 in Q1 2025, compared to $3.53 in the same period of 2024. Management expects the current cash position to support operations through to positive cash flow, with commercial infrastructure buildout progressing as planned. The company has 88 sales representatives on track to be onboarded by July 1st, 2025.

Analyst consensus remains bullish, with a "Strong Buy" rating and price targets ranging from $36 to $60, suggesting significant upside potential from current levels.

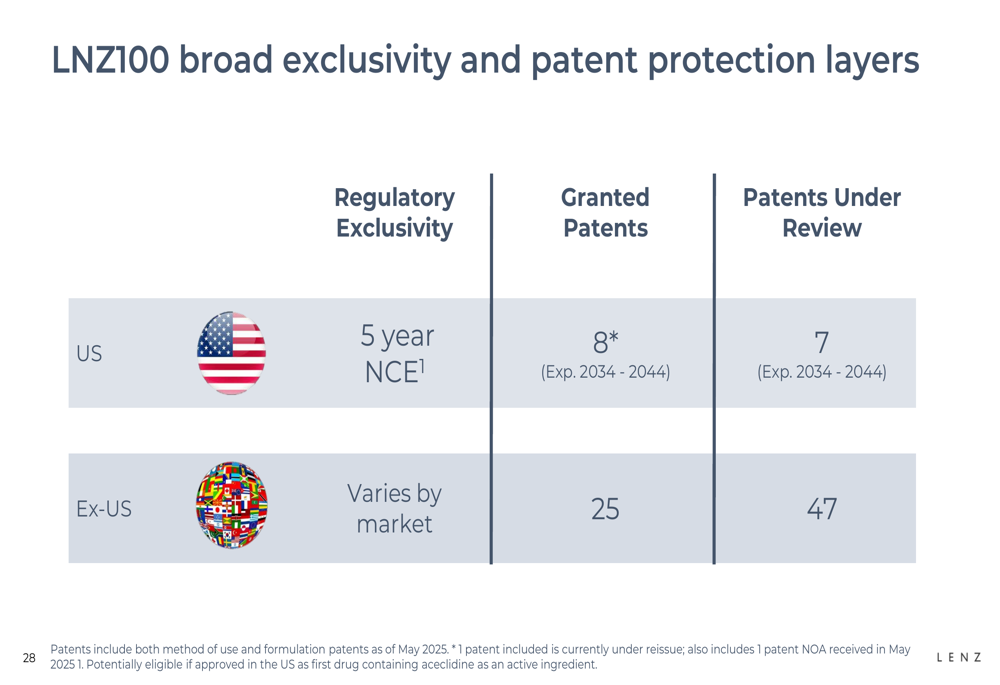

Competitive Advantages and IP Protection

LENZ highlighted several competitive advantages for LNZ100, including its unique mechanism of action, strong clinical profile, and robust intellectual property protection:

The company has secured "Made in USA" designation for LNZ100, which insulates it from potential tariff risks. U.S. Customs and Border Protection confirmed in November 2024 that the USA is the country of origin for the product, and in April 2025 confirmed that LNZ100 will be "duty free."

CEO Abe Schimmelpennik expressed confidence in the company’s position, stating, "We’ve never been more confident in our abilities to deliver once daily, well-tolerated and rapidly acting treatments." Chief Commercial Officer Sean Olson emphasized the product’s uniqueness, noting, "We see this as a category of one."

As LENZ approaches its August PDUFA date, the company appears well-positioned with strong clinical data, a clear commercialization strategy, and sufficient financial resources to support the anticipated Q4 2025 launch of LNZ100.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.