Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

Lerøy Seafood Group ASA (OB:LSG) presented its Q2 2025 results on August 20, 2025, highlighting the company’s performance across its integrated value chain during a period of challenging market conditions. CEO Henning Beltestad and CFO Sjur Malm led the presentation, emphasizing the company’s strategic focus on biological improvements and operational efficiency.

The quarter was characterized by significantly lower spot prices for salmon and trout compared to the previous year, creating headwinds for the farming segment. However, the company’s diversified business model and investments in advanced farming technologies helped mitigate these challenges.

Quarterly Performance Highlights

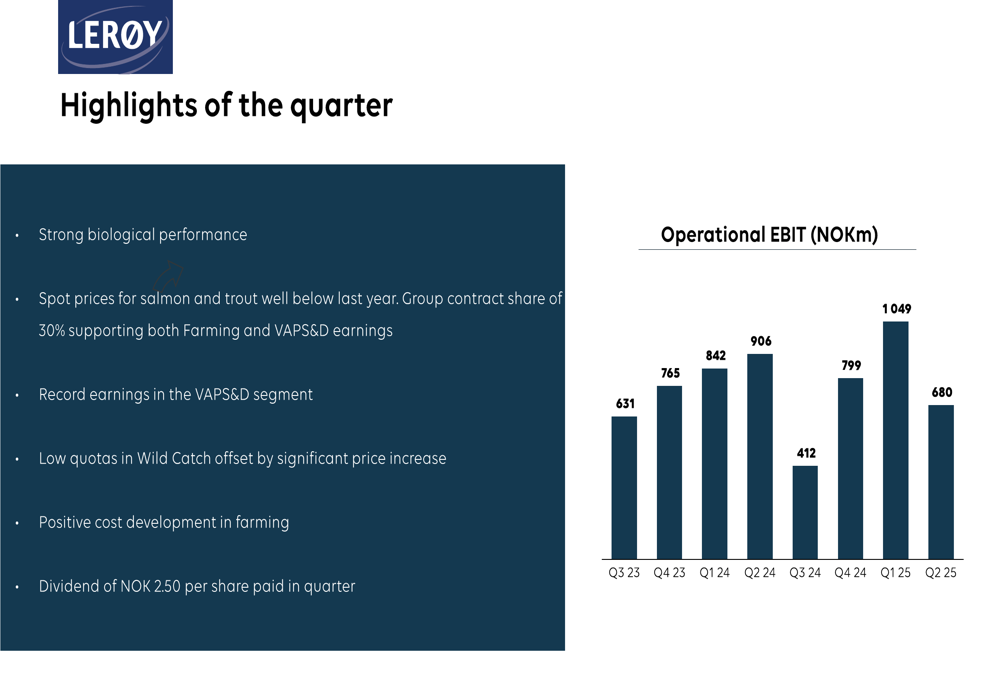

Lerøy reported an operational EBIT of NOK 680 million for Q2 2025, down from NOK 1,049 million in Q1 2025. This decline primarily reflects the impact of lower salmon prices, partially offset by strong biological performance and record earnings in the Value Added Products, Sales & Distribution (VAPS&D) segment.

As shown in the following chart of quarterly operational EBIT:

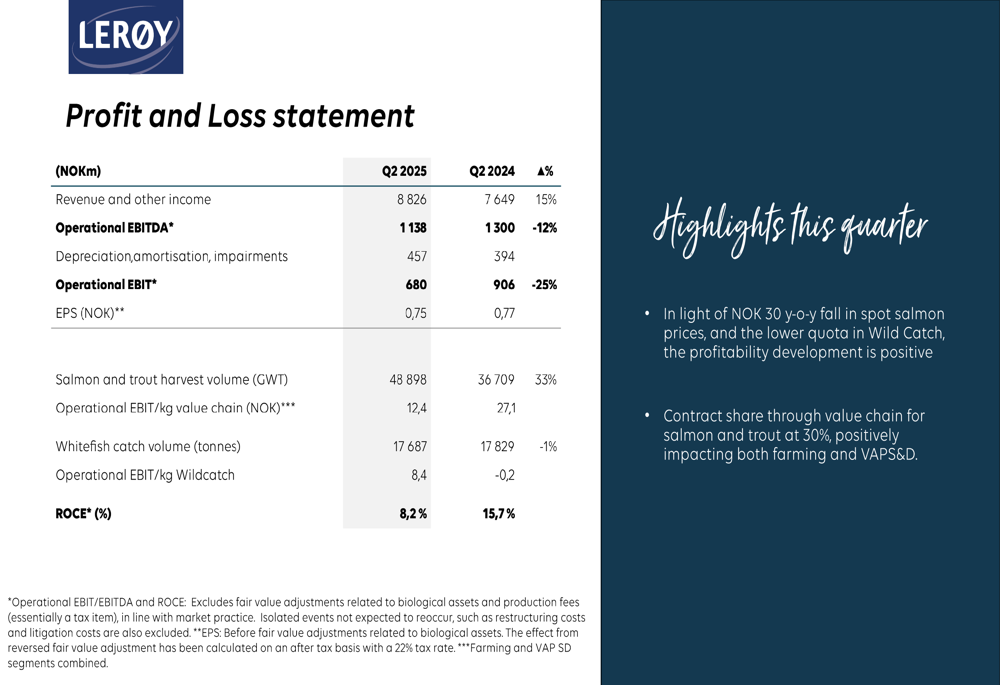

Total (EPA:TTEF) revenue for Q2 2025 reached NOK 8,826 million, with earnings per share at NOK 0.75. The company maintained its harvest volume guidance at 195,000 GWT for 2025, demonstrating confidence in its operational capabilities despite market challenges. Return on capital employed (ROCE) stood at 8.2% for the quarter.

The company’s financial summary reveals the impact of lower salmon prices and reduced wild catch quotas on overall profitability:

Segment Performance Analysis

Farming Segment

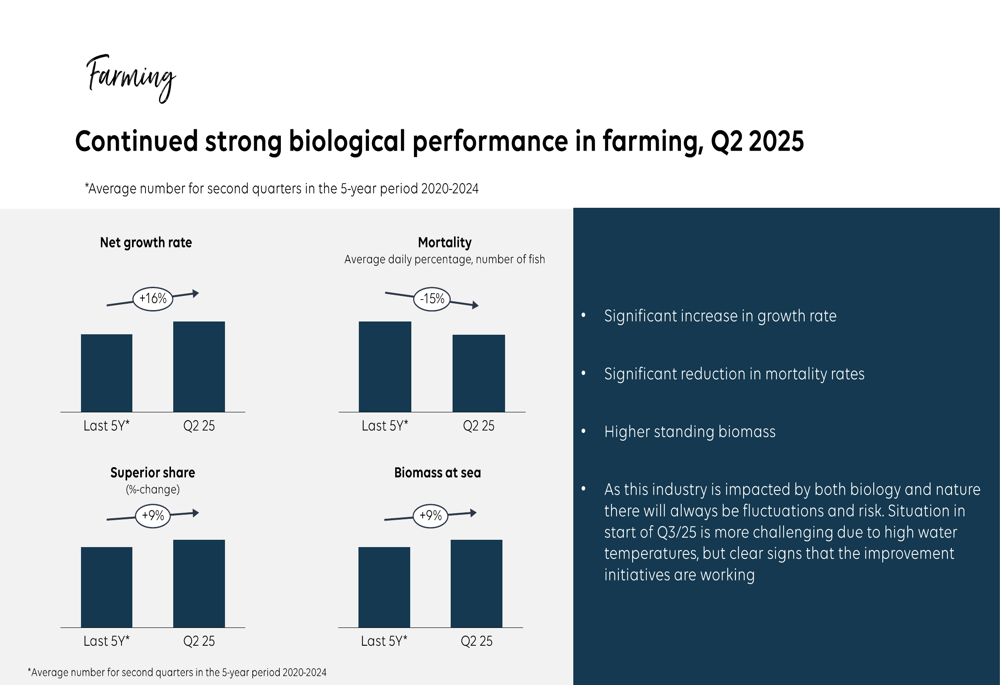

The farming segment faced challenges from lower salmon prices, with benchmark prices approximately NOK 30/kg lower in Q2 2025 compared to Q2 2024. Despite this, Lerøy achieved its highest net production in sea for a second quarter, with high survival rates, improved superior share, and higher average harvest weights.

The company’s biological improvements were particularly notable:

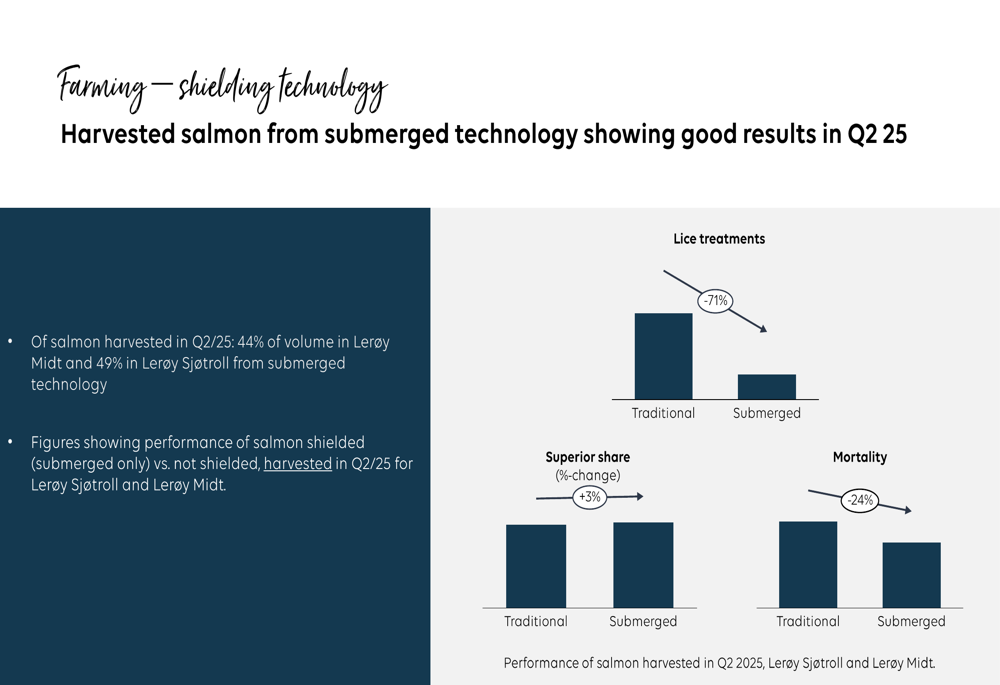

A key driver of these improvements has been Lerøy’s investment in shielding technology, particularly submerged farming. The results speak for themselves:

The company harvested 48,898 GWT of salmon and trout during Q2 2025, with an operational EBIT/kg of NOK 5.2. While biological performance was strong during the quarter, the company noted that the start of Q3 has been more challenging due to high seawater temperatures.

Wild Catch Segment

The Wild Catch segment faced challenges from reduced quotas, particularly for cod. However, this was partially offset by significant price increases for key species. Total catch volume for Q2 2025 was 17,687 tonnes, with the company noting that remaining quotas for 2025 include 4,100 tonnes of cod, 11,900 tonnes of saithe, and 1,100 tonnes of haddock.

VAPS&D Segment

The Value Added Products, Sales & Distribution segment was a bright spot in Lerøy’s Q2 results, achieving record earnings. The segment has shown consistent improvement, with a 18% increase in operational EBIT between Q2 2024 and Q2 2025 on a rolling 12-month basis.

Lerøy’s extensive sales and processing operations, spanning 17 countries with sales to more than 80 markets, continue to provide a competitive advantage and help mitigate volatility in other segments.

Financial Position and Investments

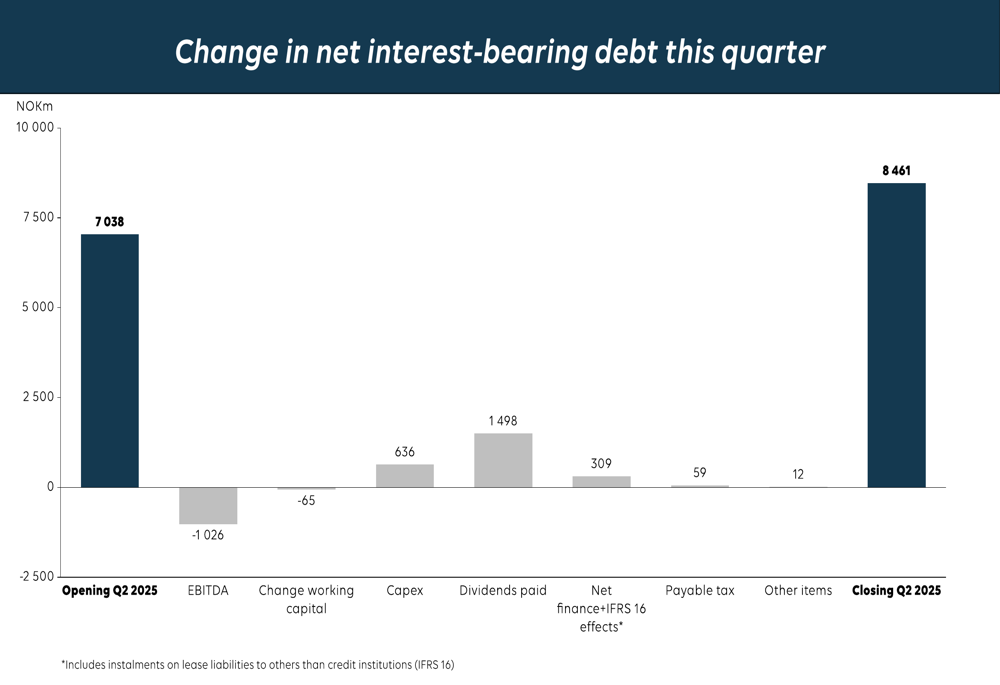

Lerøy maintained a strong balance sheet with an equity ratio of 49% and a BBB+ credit rating. Net interest-bearing debt increased to NOK 8,461 million by the end of Q2 2025, partly due to dividend payments of NOK 1,498 million during the quarter.

The following chart illustrates the changes in net interest-bearing debt:

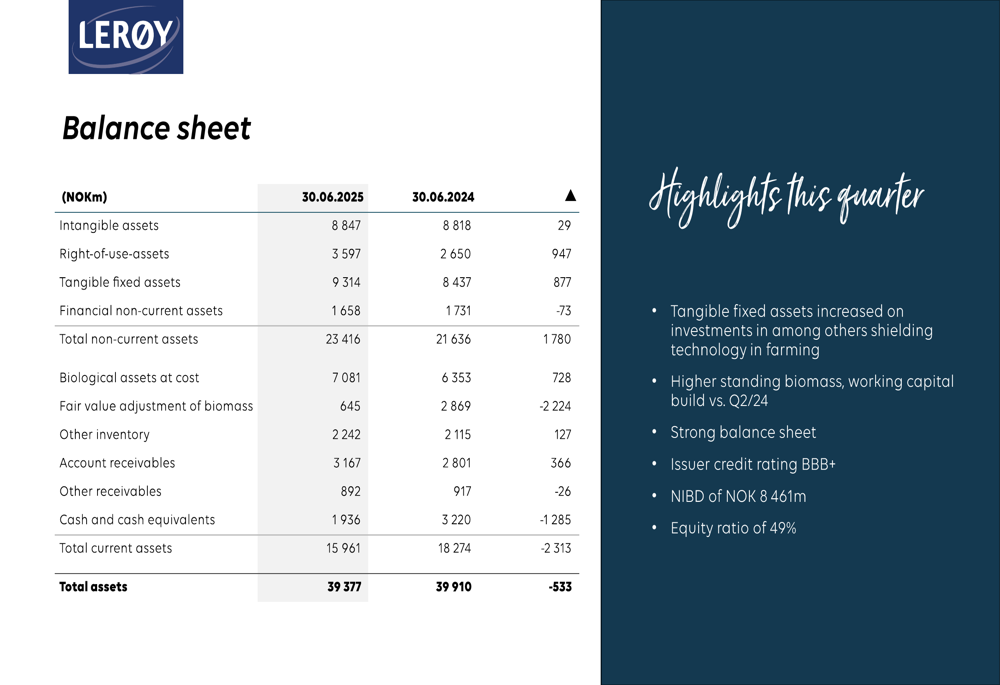

The company’s balance sheet as of June 30, 2025, shows total assets of NOK 39,377 million:

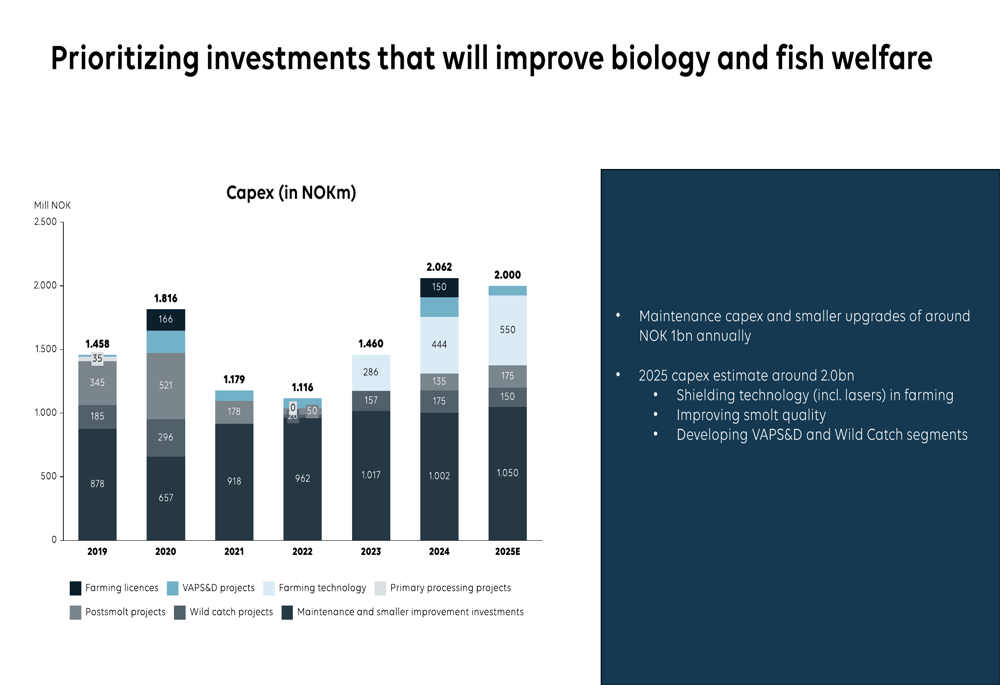

Capital expenditures remain focused on improving biology and fish welfare, with significant investments in shielding technology, smolt quality improvement, and development of the VAPS&D and Wild Catch segments. The 2025 capex estimate is approximately NOK 2 billion.

The company’s investment strategy is illustrated in this capex allocation chart:

Strategic Initiatives and Outlook

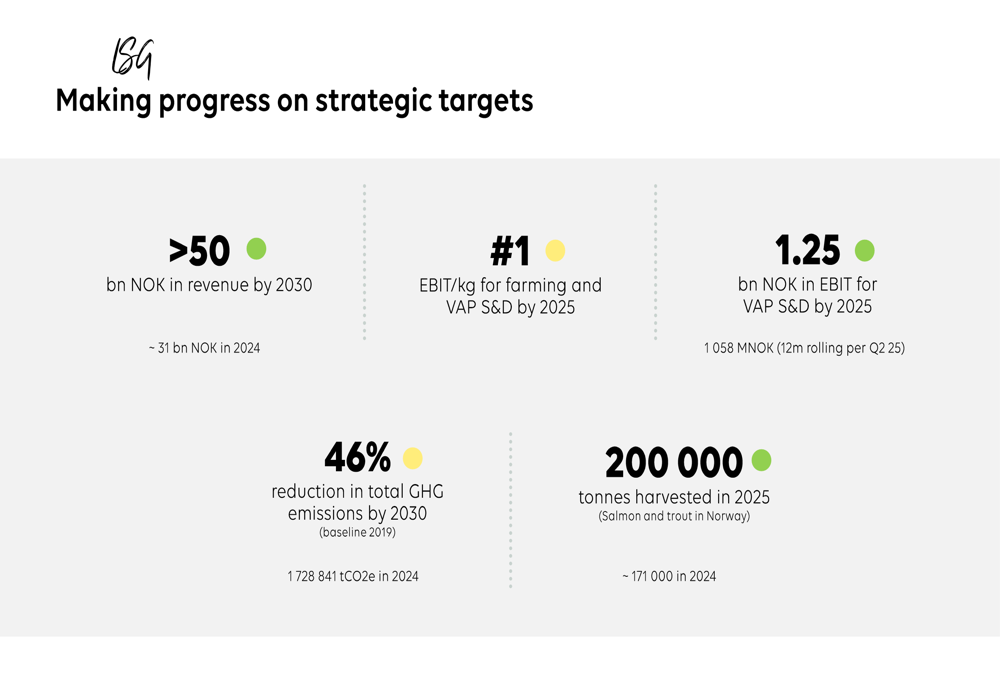

Lerøy’s strategic targets include achieving more than NOK 50 billion in revenue by 2030, becoming #1 in EBIT/kg for farming and VAPS&D by 2025, reaching NOK 1.25 billion in EBIT for VAPS&D by 2025, and reducing total greenhouse gas emissions by 46% by 2030.

These ambitious targets are supported by concrete initiatives:

For the farming segment, the outlook includes continued focus on biological improvements, with a contract share expected to be around 25%. However, spot prices are anticipated to remain below production costs in the near term. The Wild Catch segment faces limited quotas but benefits from positive price development. The VAPS&D segment is progressing toward its 2025 profitability targets, with lower fish prices expected to help build markets.

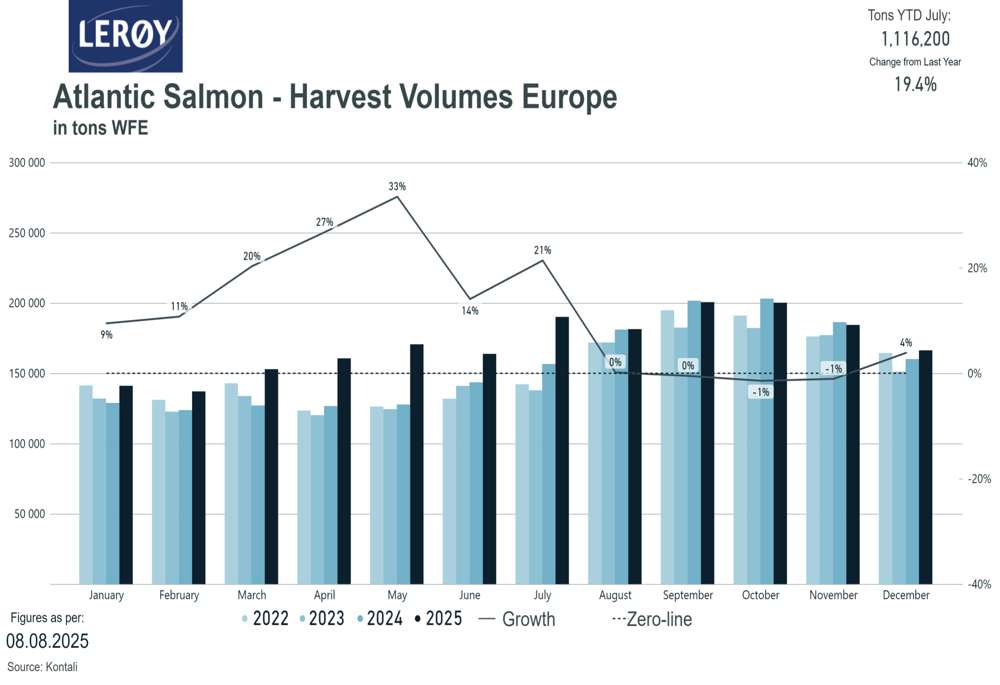

European harvest volumes show strong growth potential, with a 19.4% increase year-to-date through July 2025:

Lerøy’s continued investments in shielding technology and other operational improvements position the company to navigate current market challenges while building long-term competitive advantages through its integrated value chain approach.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.