Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Introduction & Market Context

Lexicon Pharmaceuticals (NASDAQ:LXRX) presented its first quarter 2025 earnings on May 13, highlighting financial restructuring efforts and strategic partnerships amid ongoing revenue challenges. The company’s stock has struggled recently, trading at $0.901 in after-hours, down from its 52-week high of $2.45 but above its low of $0.284. Despite beating earnings expectations with a smaller-than-anticipated loss, Lexicon faces investor skepticism following a significant revenue miss.

The biopharmaceutical company is pursuing opportunities in substantial markets with unmet needs, including diabetic peripheral neuropathic pain (DPNP) and hypertrophic cardiomyopathy (HCM), while advancing its pipeline through strategic partnerships.

Quarterly Performance Highlights

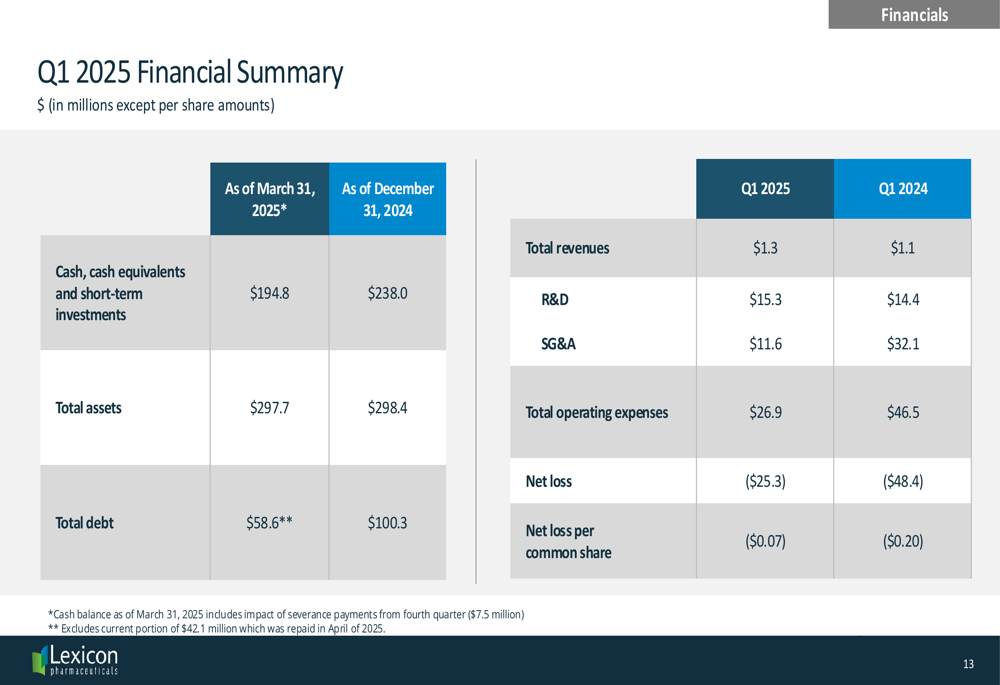

Lexicon reported a net loss of $25.3 million (-$0.07 per share) for Q1 2025, outperforming both analyst expectations of -$0.12 and the prior year’s loss of $48.4 million (-$0.20 per share). However, revenue of $1.3 million fell significantly short of the forecasted $2.82 million, representing only a slight increase from $1.1 million in Q1 2024.

The company made notable progress in reducing operating expenses, which decreased to $26.9 million from $46.5 million in the same period last year. This reduction was primarily driven by lower SG&A expenses ($11.6 million vs. $32.1 million), while R&D expenses increased slightly to $15.3 million from $14.4 million.

As shown in the following financial summary:

Lexicon ended the quarter with $194.8 million in cash and short-term investments, down from $238.0 million at the end of 2024. The company significantly reduced its total debt to $58.6 million from $100.3 million, demonstrating commitment to strengthening its balance sheet.

Strategic Initiatives & Partnerships

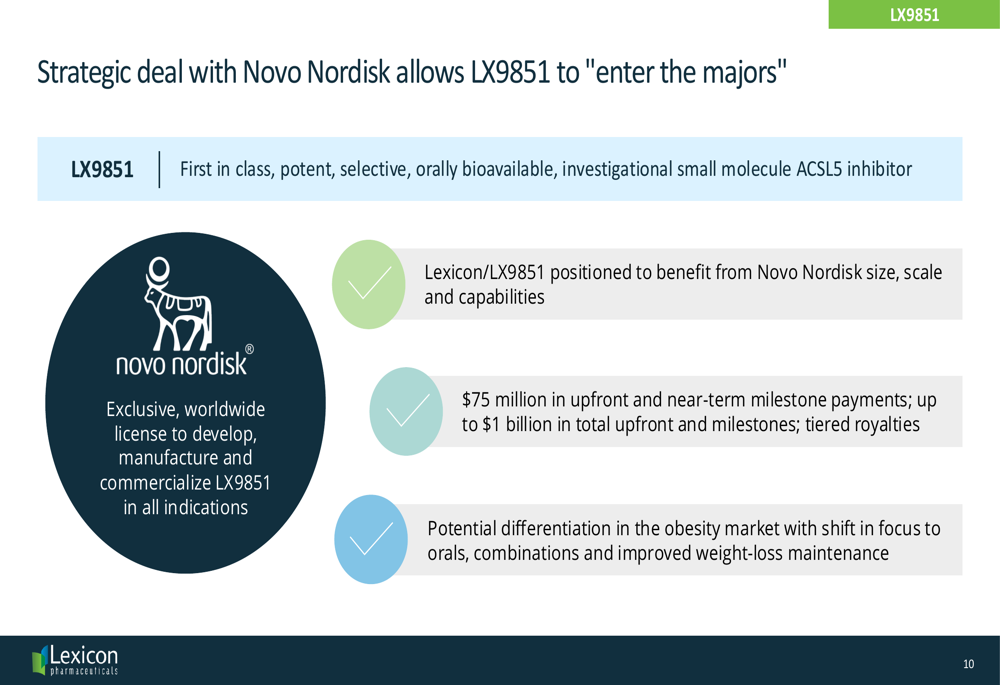

A centerpiece of Lexicon’s strategy is its exclusive worldwide licensing agreement with Novo Nordisk (NYSE:NVO) for LX9851, a first-in-class, orally bioavailable ACSL5 inhibitor being developed for obesity and weight management. The deal provides Lexicon with substantial financial support, including $75 million in upfront and near-term milestone payments, with potential for up to $1 billion in total payments plus tiered royalties.

The partnership with Novo Nordisk positions LX9851 to benefit from Novo’s established leadership in the competitive obesity market, with a focus on oral treatments, combinations, and improved weight-loss maintenance.

As illustrated in the following slide detailing the partnership:

Lexicon is pursuing a flexible partnership approach to maximize the value of its assets. In addition to the Novo Nordisk collaboration, the company has partnered with Viatris for geographical expansion of sotagliflozin, receiving $25 million upfront with potential for almost $200 million in milestone payments.

The company’s strategic objectives for 2025 include:

Pipeline Development & Clinical Progress

Lexicon’s pipeline is led by pilavapadin (LX9211) for diabetic peripheral neuropathic pain, which showed promising results in Phase 2 trials. The company has identified a de-risked 10mg dose to advance into Phase 3 trials, addressing a significant market need.

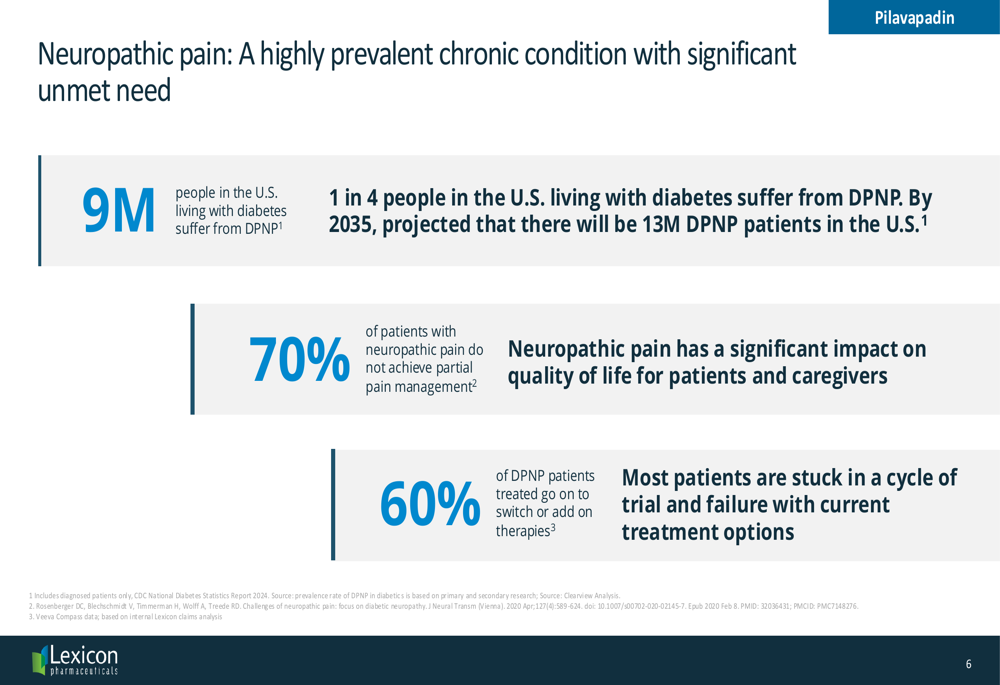

The DPNP market represents a substantial opportunity, with 9 million people in the U.S. currently affected and projections of 13 million by 2035. According to company data, 70% of patients with neuropathic pain do not achieve partial pain management, highlighting the unmet need:

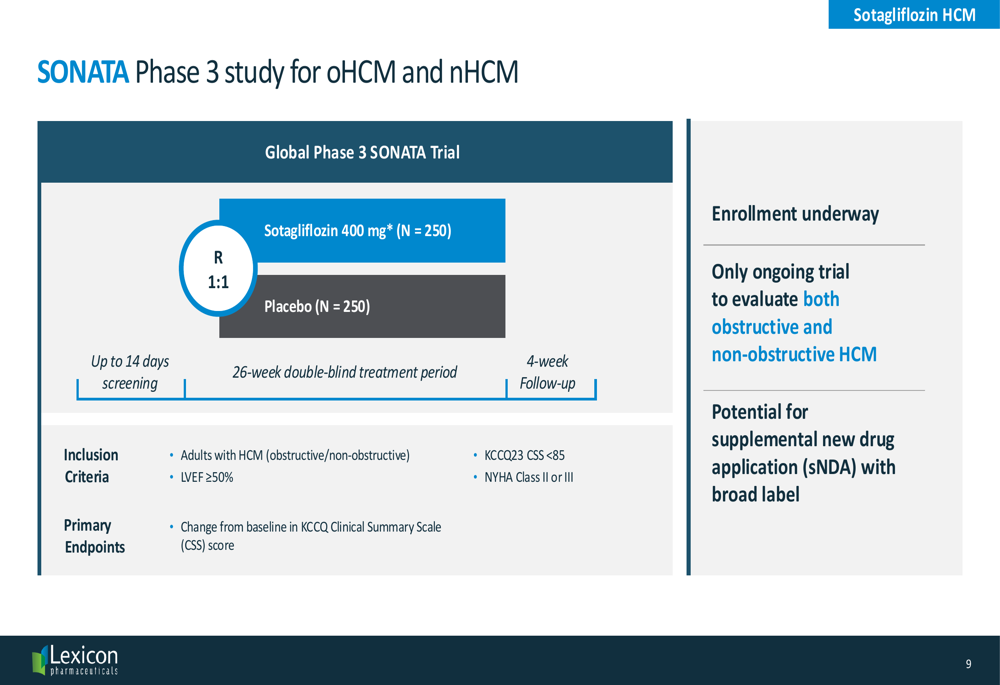

For sotagliflozin, Lexicon is conducting the global Phase 3 SONATA trial for both obstructive and non-obstructive hypertrophic cardiomyopathy (HCM), a condition affecting approximately 1.1 million people in the U.S. The study design includes 500 patients randomized 1:1 to receive either sotagliflozin 400 mg or placebo, with the primary endpoint being change from baseline in KCCQ Clinical Summary Scale score:

Lexicon positions sotagliflozin as potentially advantageous for HCM treatment due to its once-daily oral dosing, broad proposed indication for both obstructive and non-obstructive HCM, and established safety profile in heart failure without observed increased risk of atrial fibrillation.

Financial Outlook & Guidance

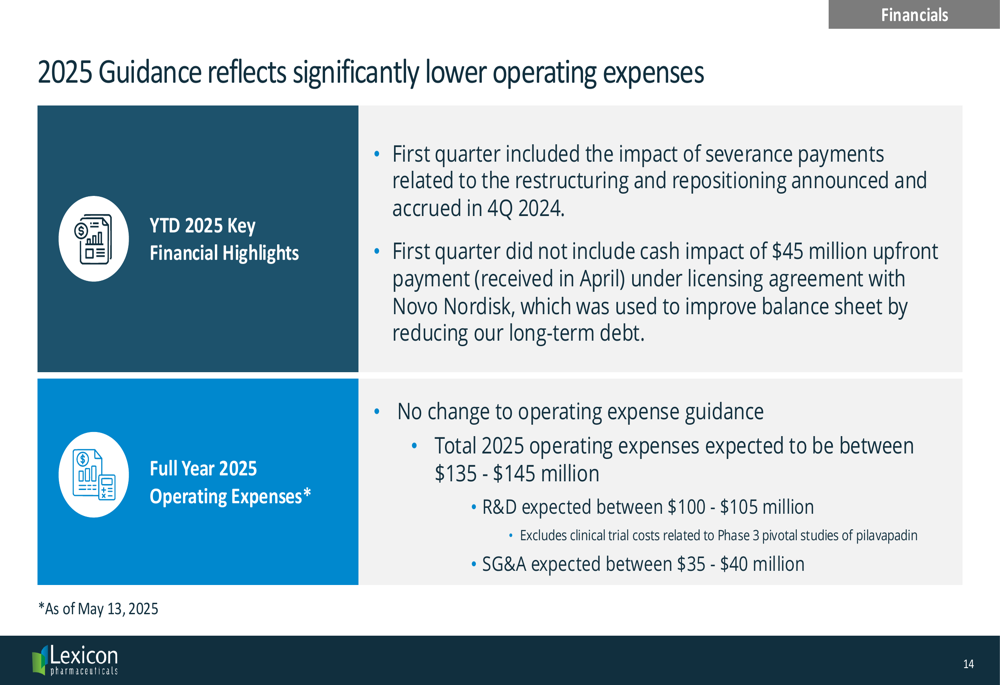

Looking ahead, Lexicon provided financial guidance for 2025, projecting operating expenses between $135-145 million, with R&D expenses of $100-105 million (excluding clinical trial costs for Phase 3 pivotal studies of pilavapadin) and SG&A expenses of $35-40 million.

The company noted that Q1 included severance payments related to restructuring announced in Q4 2024, while the $45 million upfront payment from Novo Nordisk (received in April) was used to reduce long-term debt:

Forward-Looking Statements

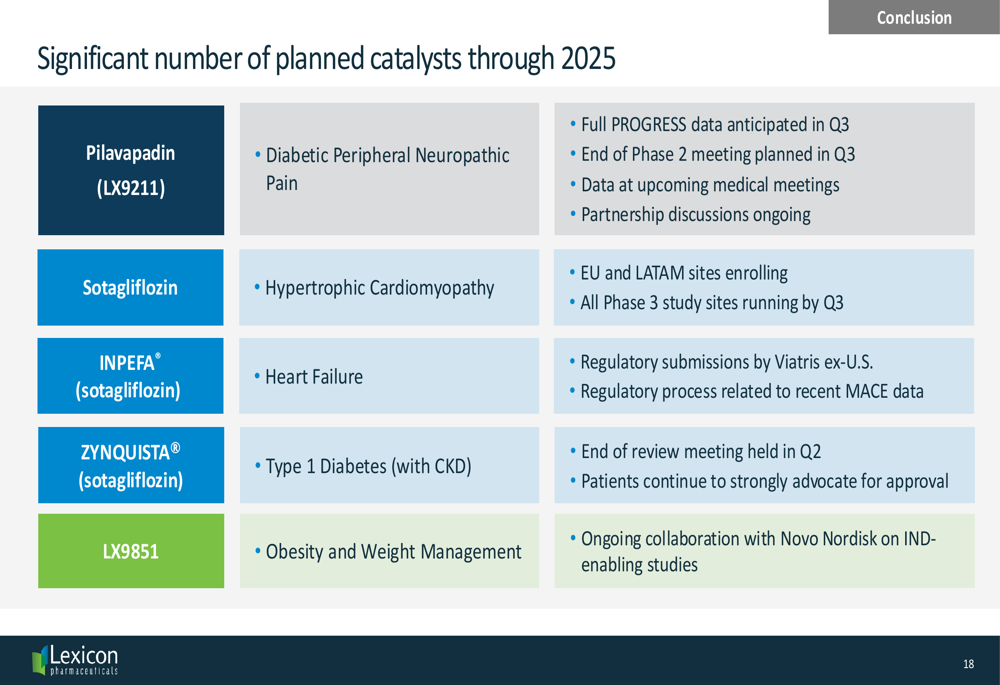

Lexicon outlined several potential catalysts for 2025, including:

- Full PROGRESS data for pilavapadin expected in Q3

- End of Phase 2 meeting for pilavapadin planned in Q3

- All Phase 3 study sites for sotagliflozin in HCM running by Q3

- Ongoing regulatory submissions by Viatris for INPEFA (sotagliflozin) in heart failure outside the U.S.

- Continued collaboration with Novo Nordisk on IND-enabling studies for LX9851

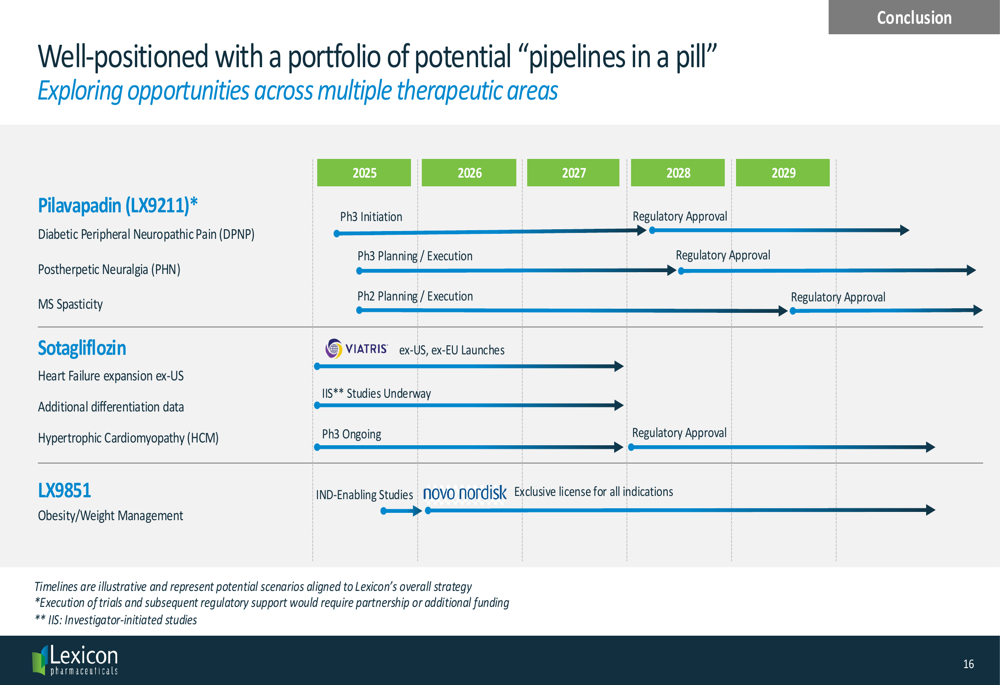

The company’s pipeline development timeline extends through 2029, with potential regulatory approvals and launches dependent on successful clinical outcomes and partnerships:

Despite the positive developments in pipeline and partnerships, investors should note the discrepancy between the company’s optimistic outlook and its current financial performance, particularly the significant revenue shortfall against expectations. The stock’s decline following earnings suggests continued market skepticism about Lexicon’s path to profitability, even as it makes progress in reducing expenses and advancing its clinical programs.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.