Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Lightspeed Commerce Inc. (NYSE:LSPD) released its fourth quarter fiscal 2025 results on May 22, 2025, reporting 10% year-over-year revenue growth amid continued expansion of its payments business. The point-of-sale and e-commerce solutions provider achieved several key milestones in the quarter, though financial results were impacted by a significant goodwill impairment charge.

The company, which serves small and medium-sized businesses in the retail and hospitality sectors, continues to focus on increasing average revenue per user (ARPU) and expanding its payments penetration as core growth strategies. Lightspeed shares closed at $10.77 on May 21, 2025, down 1.82% ahead of the earnings release.

Quarterly Performance Highlights

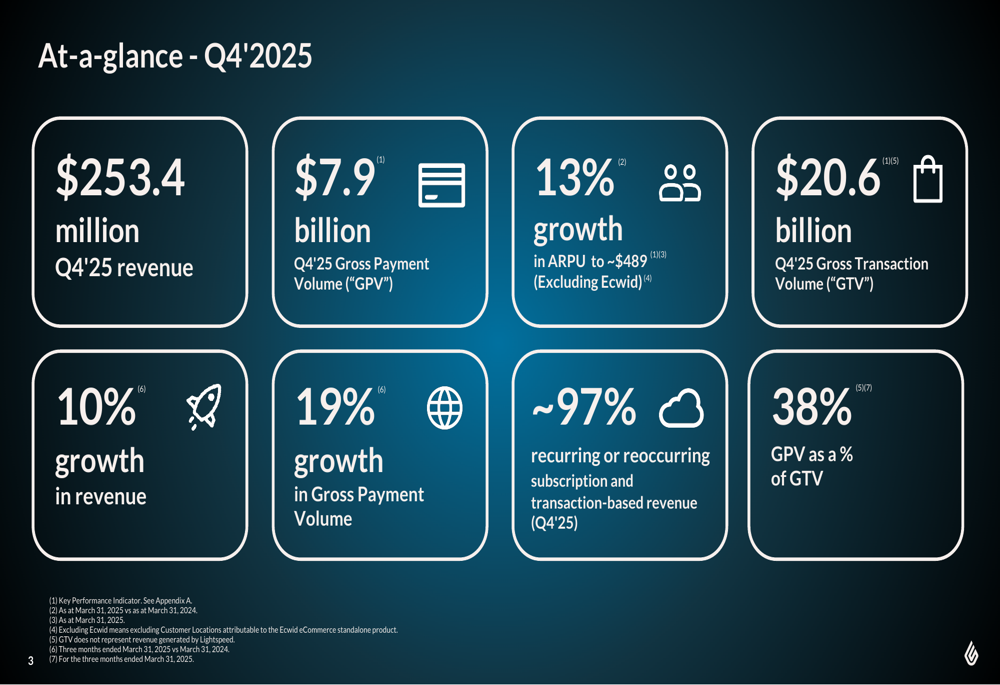

Lightspeed reported Q4 2025 revenue of $253.4 million, representing a 10% increase year-over-year. The company’s gross payment volume (GPV) reached $7.9 billion, growing 19% compared to the same period last year, while gross transaction volume (GTV) totaled $20.6 billion.

As shown in the following quarterly performance summary:

The company highlighted that approximately 97% of its revenue is recurring or reoccurring, coming from subscription and transaction-based sources. Payments penetration, measured as GPV as a percentage of GTV, reached 38% in the quarter, indicating continued adoption of Lightspeed’s payment processing solutions.

Average revenue per user (ARPU) grew 13% year-over-year to approximately $489 (excluding Ecwid), demonstrating the company’s success in expanding revenue from existing customers.

Detailed Financial Analysis

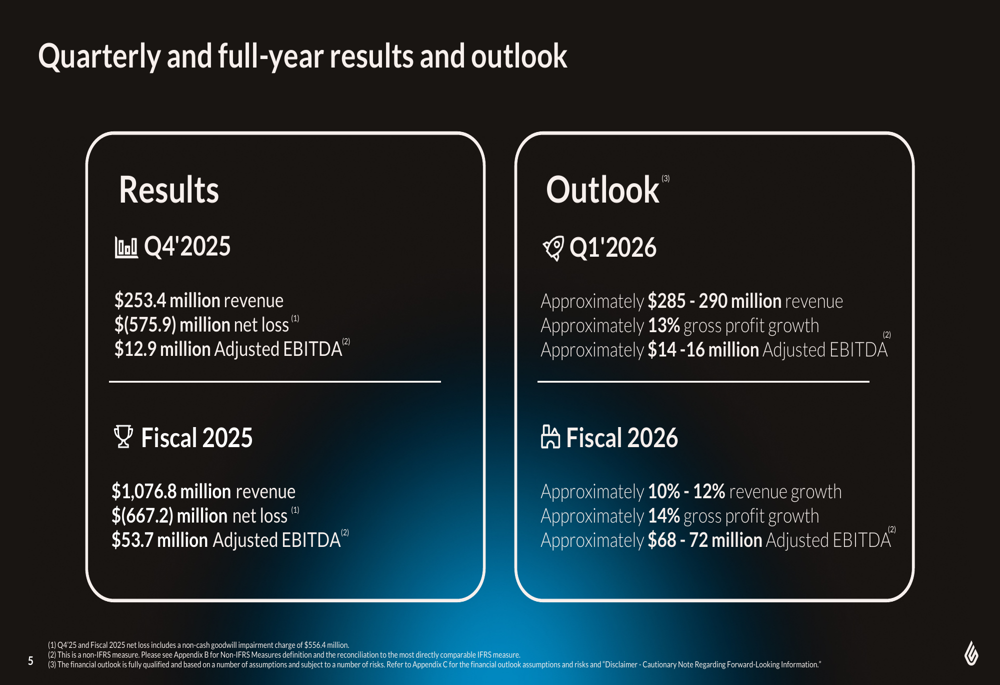

While Lightspeed showed revenue growth and operational improvements, the company reported a substantial net loss of $575.9 million for Q4 2025, primarily due to a $556.4 million goodwill impairment charge. Excluding this non-cash charge, the company achieved Adjusted EBITDA of $12.9 million for the quarter, compared to $4.4 million in Q4 2024.

For the full fiscal year 2025, Lightspeed generated revenue of $1,076.8 million with a net loss of $667.2 million and Adjusted EBITDA of $53.7 million. The following slide illustrates these results alongside the company’s outlook for the coming periods:

Gross margin improved to 44%, reflecting the company’s focus on operational efficiency and higher-margin revenue streams. Lightspeed also actively managed its capital structure, repurchasing approximately 18.7 million shares (about 12% of total shares outstanding) for total consideration of approximately $219 million over the last 12 months.

Strategic Initiatives

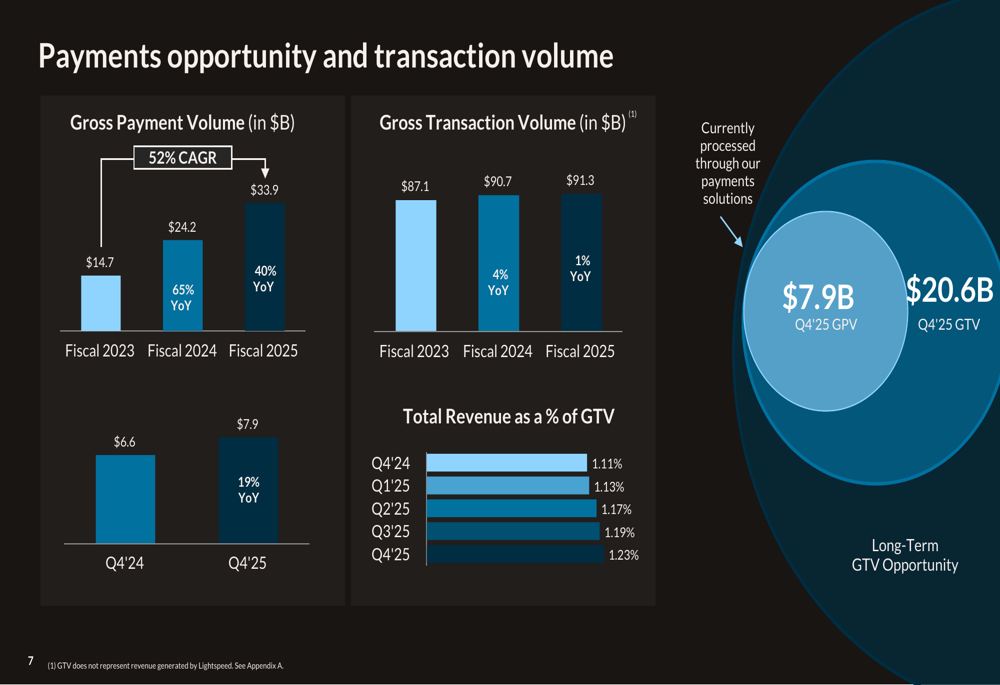

Lightspeed continues to focus on expanding its payments business as a key growth driver. The company’s GPV has shown consistent growth over time, increasing from $14.7 billion in fiscal 2023 to $33.9 billion in fiscal 2025. This expansion represents a significant opportunity, as illustrated in the following chart:

Total (EPA:TTEF) revenue as a percentage of GTV has steadily increased from 1.11% in Q4 2024 to 1.23% in Q4 2025, indicating improved monetization of transaction volume flowing through Lightspeed’s platform.

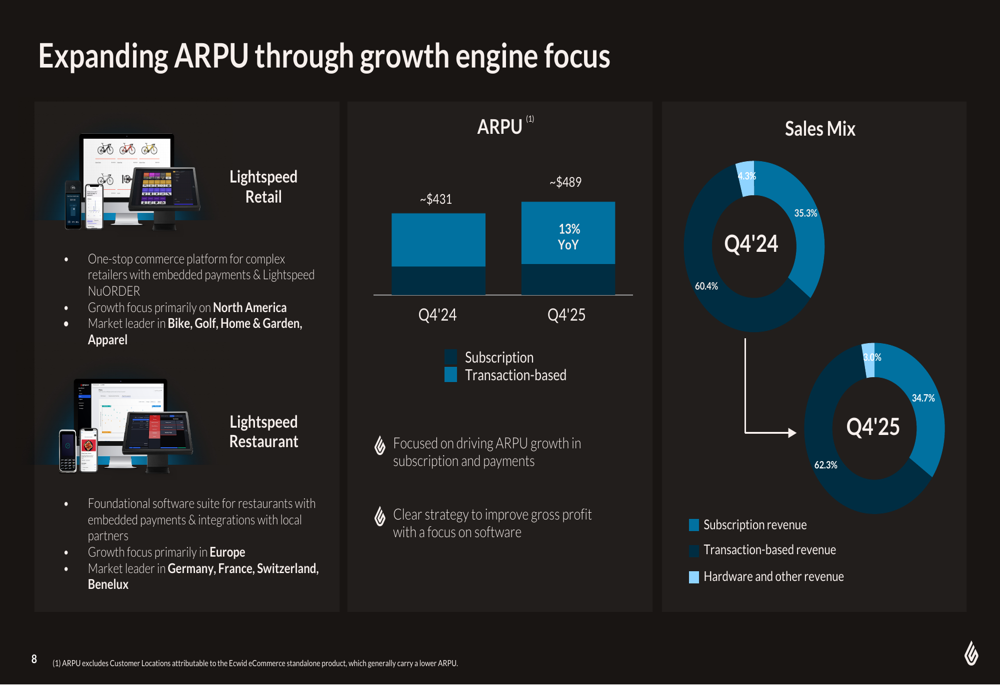

Another strategic priority for Lightspeed is expanding ARPU through its focus on two core product lines: Lightspeed Retail (a one-stop commerce platform) and Lightspeed Restaurant (a foundational software suite). The company’s strategy is yielding results, as demonstrated by the 13% year-over-year ARPU growth:

Customer Success Stories

Lightspeed highlighted several customer wins during the quarter, showcasing the company’s ability to attract and retain businesses across different segments. Notable customer examples include Éclore, a Parisian restaurant group adding seven Michelin-recommended restaurants; Runners Roost, an apparel and footwear retailer that saved money on payments; and Burger & Sauce, a UK restaurant chain that switched from another cloud-based POS provider.

These customer stories reinforce Lightspeed’s value proposition in both the retail and restaurant verticals, which remain the company’s core focus areas.

Forward-Looking Statements

Looking ahead, Lightspeed provided guidance for both Q1 2026 and the full fiscal year 2026. For Q1 2026, the company expects revenue of approximately $285-290 million, representing about 13% gross profit growth, and Adjusted EBITDA of approximately $14-16 million.

For fiscal 2026, Lightspeed forecasts:

- 10-12% revenue growth

- Approximately 14% gross profit growth

- Adjusted EBITDA of approximately $68-72 million

This outlook suggests continued momentum in the business and further improvement in profitability metrics, building on the progress made in fiscal 2025. The company’s focus remains on enhancing recurring subscription revenue and expanding payments adoption among its customer base.

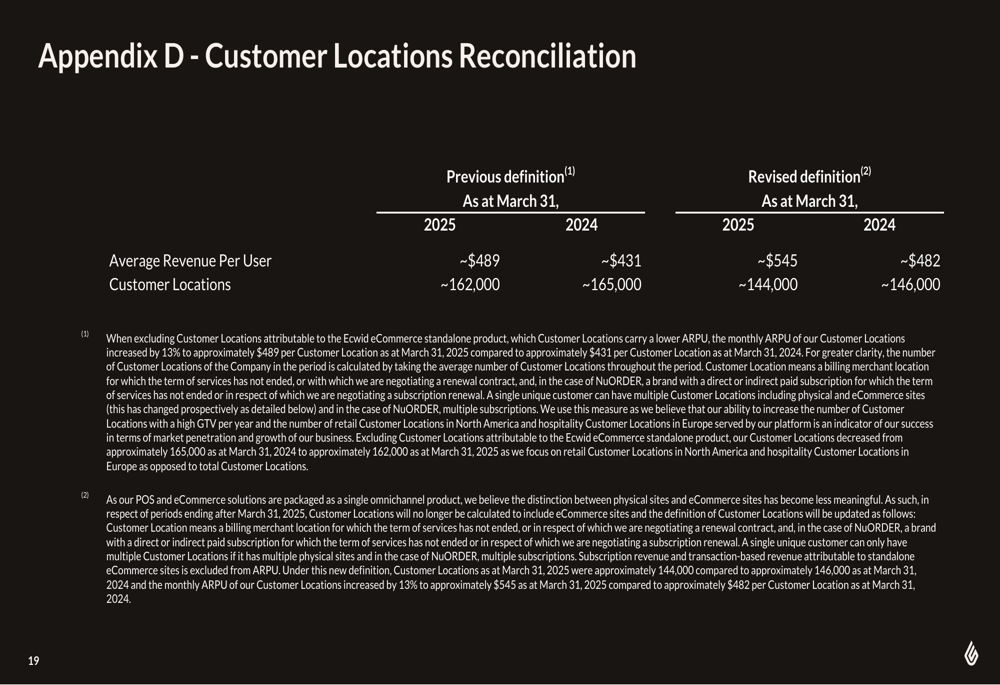

Revised Customer Metrics

Lightspeed also disclosed a revision to its customer location definition, which impacts how it reports ARPU and customer counts. Under the revised definition, which focuses on more valuable customer relationships, Q4 2025 ARPU was $545 (versus $489 under the previous definition) and customer locations totaled 144,000 (versus 162,000).

The following reconciliation table illustrates the impact of this change:

This revision reflects Lightspeed’s strategic focus on higher-value customers and provides a more accurate representation of its core business.

In summary, Lightspeed’s Q4 2025 results demonstrate continued growth in key metrics despite the significant goodwill impairment charge. The company’s strategic focus on payments expansion and ARPU growth appears to be yielding positive results, with an optimistic outlook for fiscal 2026 suggesting further improvements in revenue and profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.