Nvidia among investors in xAI’s $20bn capital raise - Bloomberg News

Introduction & Market Context

Lincoln National Corporation (NYSE:LNC) presented its second-quarter 2025 earnings results on July 31, showing significant improvement in operating performance and capital position. The company’s stock rose 1.32% to $34.65 in premarket trading, building on recent momentum despite closing down 2.4% at $34.20 in the previous session.

The Q2 results mark a substantial improvement from the first quarter, when Lincoln National missed earnings expectations with an EPS of $1.60 against a forecast of $1.64. The company’s strategic partnership with Bain Capital, mentioned in previous earnings, has now closed and is contributing to the strengthened capital position.

Quarterly Performance Highlights

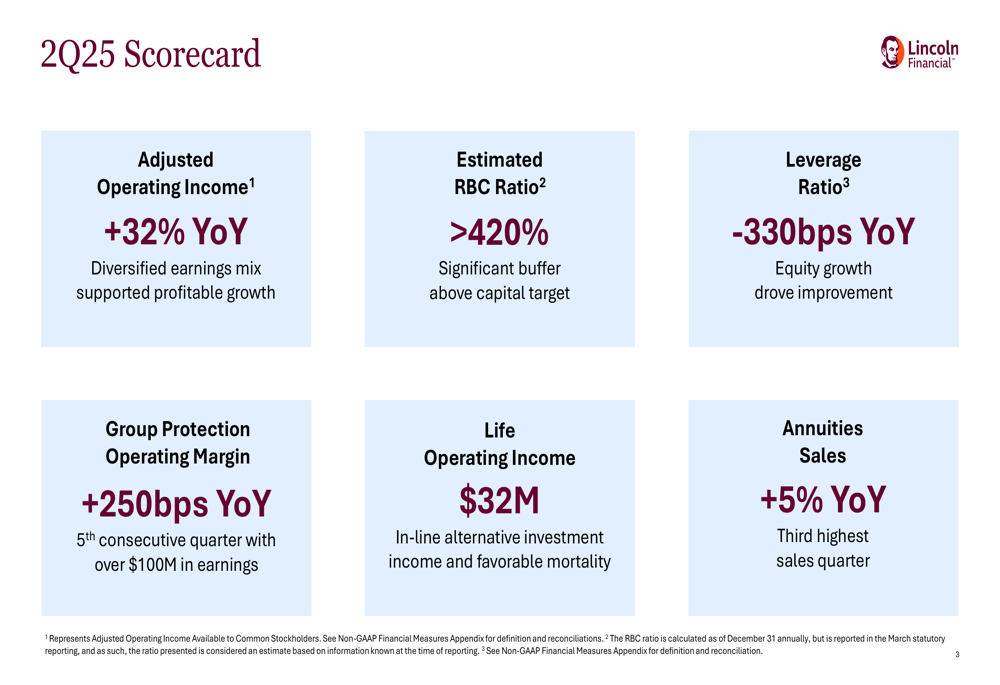

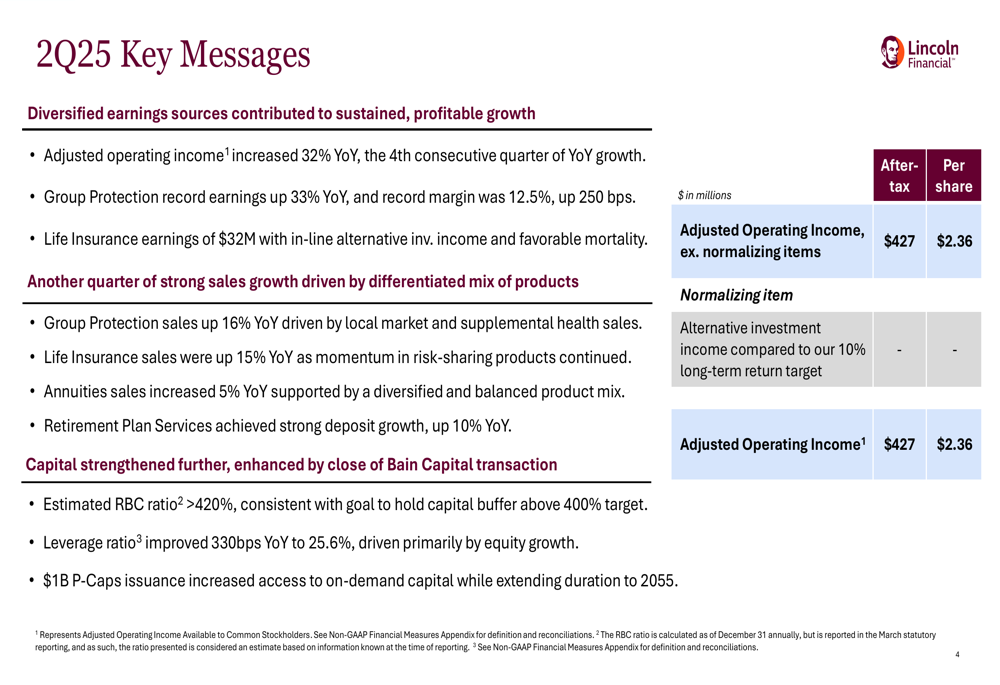

Lincoln National reported a 32% year-over-year increase in adjusted operating income for Q2 2025, driven by strong performance across multiple business segments. The company highlighted its diversified earnings sources as key contributors to sustained, profitable growth.

As shown in the following comprehensive scorecard of Lincoln’s Q2 performance:

The adjusted operating income, excluding normalizing items, reached $427 million, translating to earnings per share of $2.36. This represents a substantial improvement from the previous year and builds on the recovery trend observed in recent quarters.

Lincoln’s key performance metrics for the quarter are further detailed in this overview:

Segment Analysis

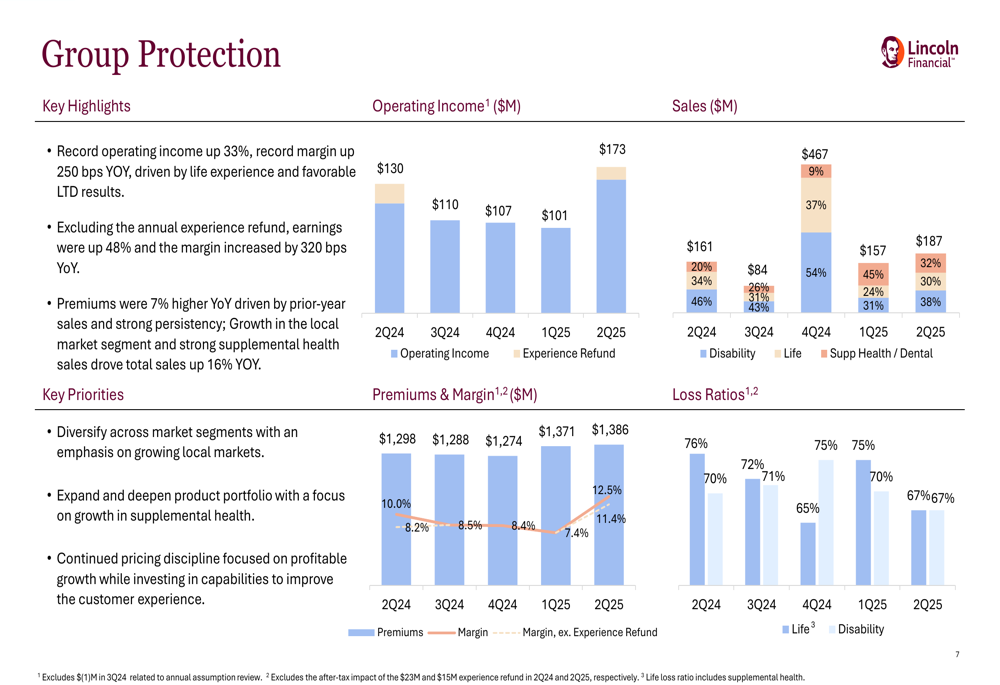

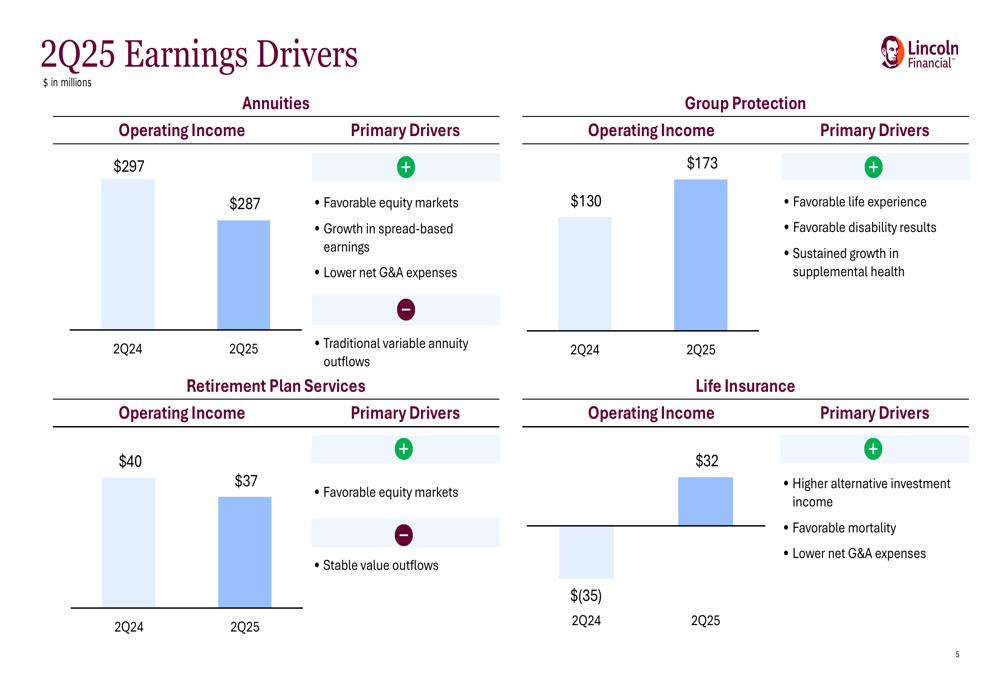

The Group Protection segment emerged as the standout performer, delivering record earnings with a 33% year-over-year increase to $173 million. The segment’s operating margin improved by 250 basis points, driven by favorable life experience and disability results, along with sustained growth in supplemental health products.

The following chart illustrates the strong performance in Group Protection:

Life Insurance (NSE:LIFI) showed a remarkable turnaround, reporting operating income of $32 million compared to a loss of $35 million in the same quarter last year. This $67 million improvement was attributed to higher alternative investment income, favorable mortality experience, and lower net G&A expenses. Life Insurance sales increased 15% year-over-year to $121 million.

The segment-by-segment earnings drivers reveal the varied performance across Lincoln’s business lines:

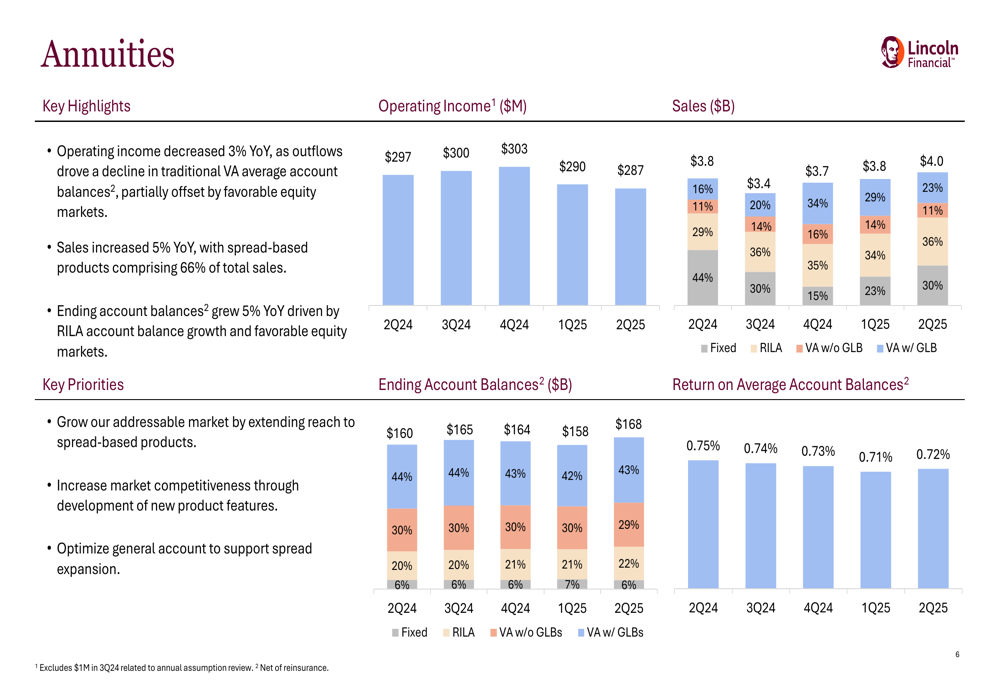

The Annuities segment, while still the largest contributor to earnings, saw a slight 3% year-over-year decrease in operating income to $287 million. However, sales increased 5% year-over-year to $4.0 billion, with a continued shift toward registered index-linked annuities (RILA) and fixed annuities, reflecting Lincoln’s strategy to diversify its product mix.

Retirement Plan Services reported an 8% year-over-year decrease in operating income to $37 million, despite first-year sales growing nearly 50% and total deposits increasing 10% year-over-year. Ending account balances grew 8% year-over-year to $55 billion, benefiting from favorable equity markets.

Capital Position and Investment Portfolio

Lincoln National continued to strengthen its capital position, reporting an estimated risk-based capital (RBC) ratio above 420% and improving its leverage ratio by 330 basis points year-over-year to 25.6%. The company completed a $1 billion preferred capital securities (P-Caps) issuance, which increased access to on-demand capital while extending duration to 2055.

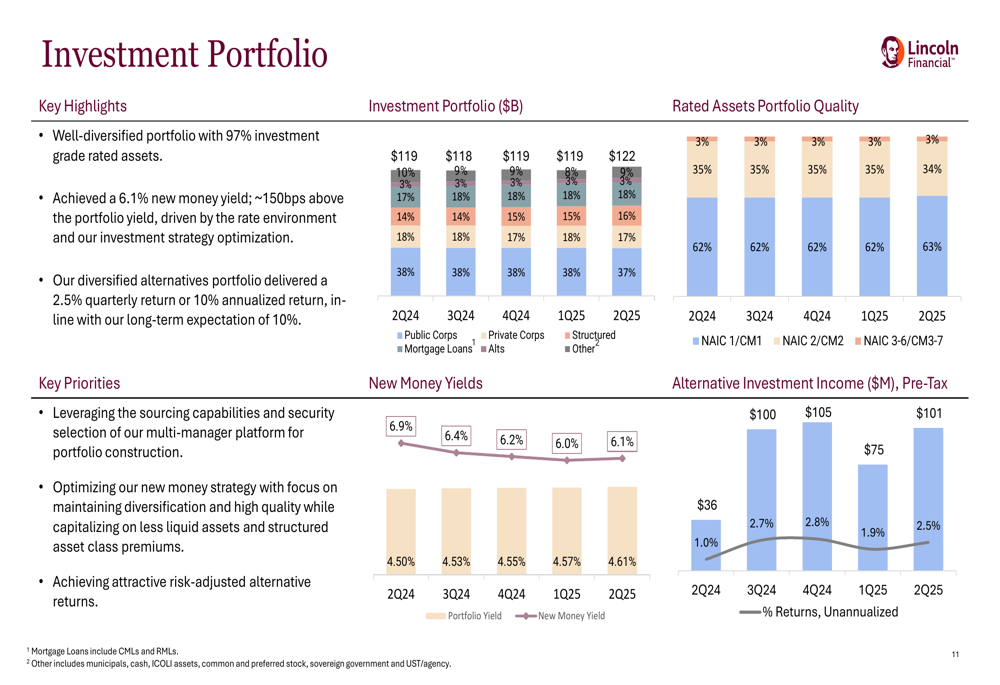

The company’s investment portfolio remains well-diversified with 97% investment-grade rated assets. Lincoln achieved a 6.1% new money yield and reported a 2.5% quarterly return on its alternatives portfolio.

The "Other Operations" segment, which includes corporate activities, reported an operating loss of $91 million, a 6% improvement from the prior year. Interest expense decreased by $5 million year-over-year to $81 million, contributing to the improved leverage ratio.

Forward-Looking Statements

Lincoln National emphasized its continued focus on diversified earnings sources and product mix to drive sustained, profitable growth. The company highlighted the successful close of the Bain Capital transaction as a strategic milestone that further enhances its capital position.

Management expressed confidence in the company’s ability to maintain strong sales momentum across all business segments, particularly in Group Protection and Life Insurance. The improved capital flexibility, bolstered by the P-Caps issuance, positions Lincoln to navigate market conditions while pursuing strategic growth opportunities.

The company’s performance represents a significant improvement from Q1 2025, when it missed earnings expectations. The 32% growth in adjusted operating income and strengthened capital position suggest Lincoln’s strategic initiatives are gaining traction, though challenges remain in segments like Annuities and Retirement Plan Services where operating income declined year-over-year.

With the stock trading at $34.65 in premarket, still well below its 52-week high of $39.85, investors appear to be responding positively to the improved performance and strengthened capital position demonstrated in the Q2 2025 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.