Gold prices dip as hawkish Fed minutes weigh ahead of Jackson Hole

Introduction & Market Context

LivePerson Inc. (NASDAQ:LPSN) presented its second quarter 2025 earnings results on August 11, 2025, revealing a company navigating significant revenue challenges while making progress on operational efficiency and debt restructuring. The customer engagement platform provider reported revenue of $59.6 million, continuing a year-over-year decline trend but exceeding the midpoint of its guidance.

The company’s stock, which has traded between $0.61 and $2.08 over the past year, closed at $1.21 before the earnings announcement, down 3.31% on the day. This earnings release follows a disappointing first quarter where LivePerson significantly missed EPS forecasts, highlighting the ongoing challenges the company faces in its turnaround efforts.

Quarterly Performance Highlights

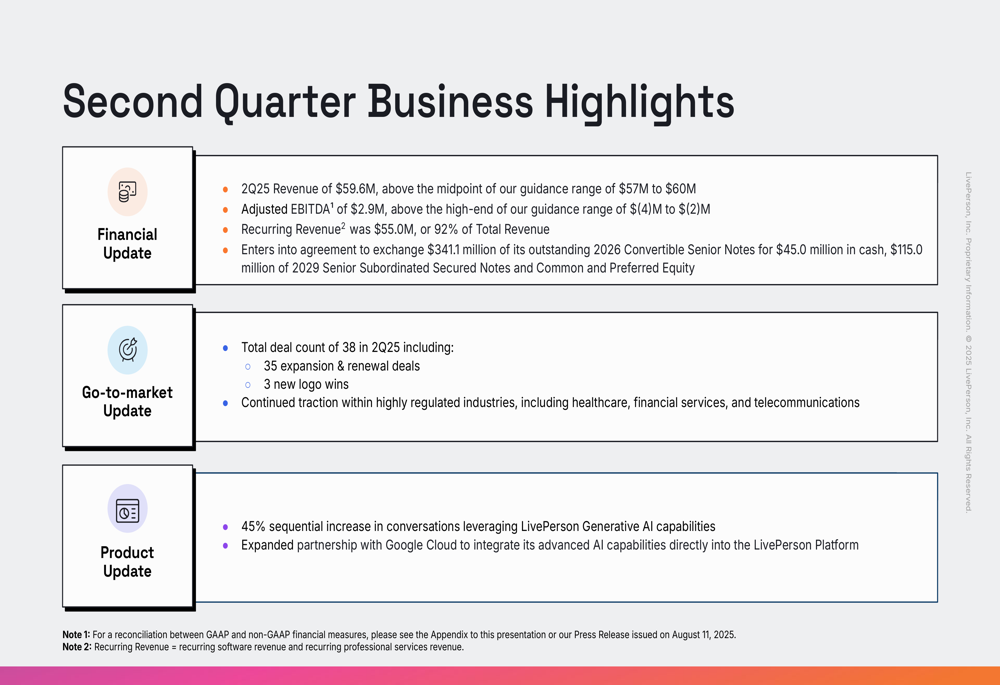

LivePerson reported Q2 2025 revenue of $59.6 million, above the guidance midpoint, while adjusted EBITDA reached $2.9 million, exceeding the high end of guidance. Recurring revenue constituted $55.0 million, representing 92% of total revenue.

As shown in the following chart of recurring revenue as a percentage of total revenue and geographic breakdown:

The company secured 38 total deals during the quarter, including 35 expansion/renewal deals and 3 new logo wins. Management highlighted continued traction in regulated industries, which aligns with previous quarter’s emphasis on this sector as a growth area.

LivePerson also reported a 45% sequential increase in conversations leveraging its Generative AI capabilities, indicating growing adoption of its AI-powered solutions. The company expanded its partnership with Google (NASDAQ:GOOGL) Cloud for AI integration, reinforcing its strategic focus on AI-driven customer engagement.

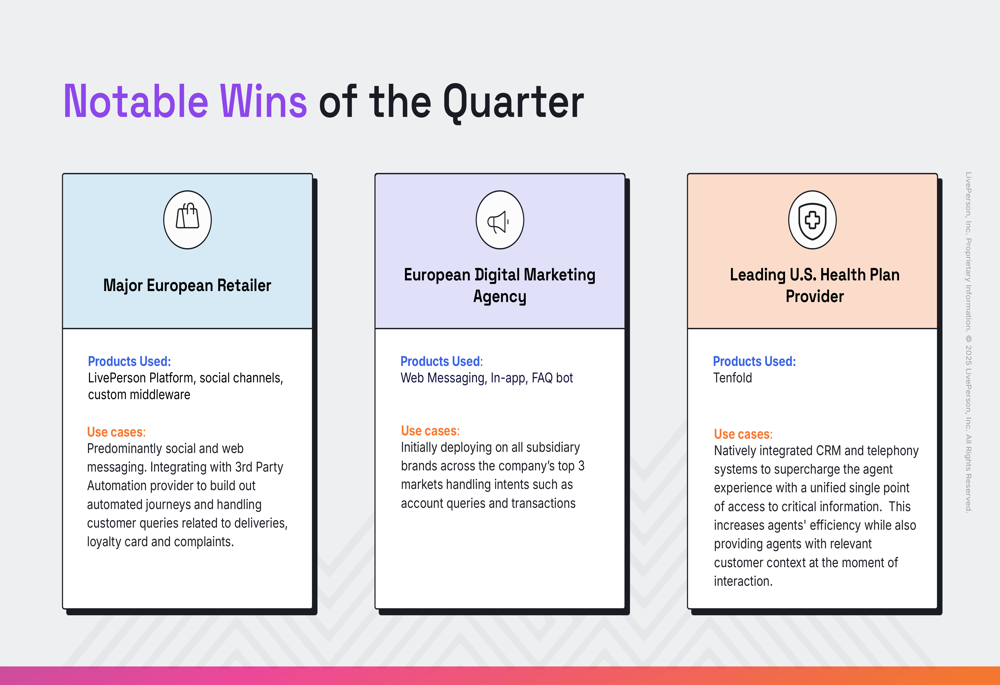

The following slide details some of the notable customer wins during the quarter:

Detailed Financial Analysis

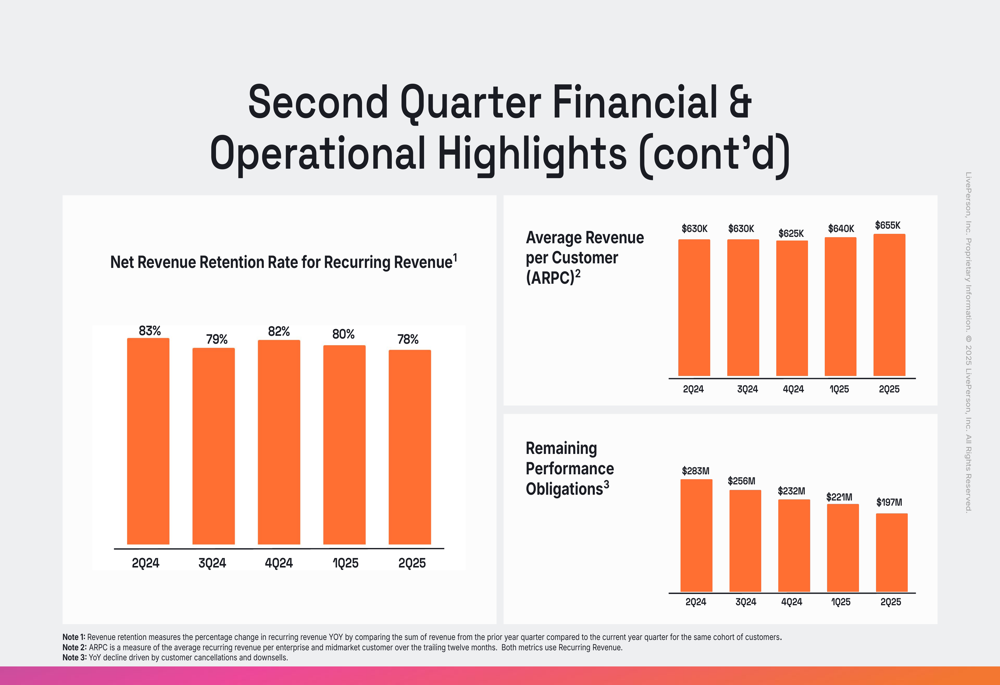

LivePerson’s financial metrics reveal a company in transition, with declining overall revenue but some positive indicators in customer value. The company’s average revenue per customer (ARPC) increased to $655,000 in Q2 2025, up from $625,000 in the same quarter last year, suggesting a focus on higher-value engagements despite the overall revenue contraction.

However, net revenue retention rate declined to 79% in Q2 2025 from 83% in Q2 2024, indicating ongoing challenges in maintaining revenue from existing customers. Similarly, remaining performance obligations decreased to $197 million from $283 million a year earlier.

The following chart illustrates these key operational metrics:

In terms of geographic distribution, LivePerson has seen a shift toward international markets, with international revenue increasing to 38% of total revenue in Q2 2025 compared to 28% in Q2 2024. This diversification may help buffer against regional economic challenges.

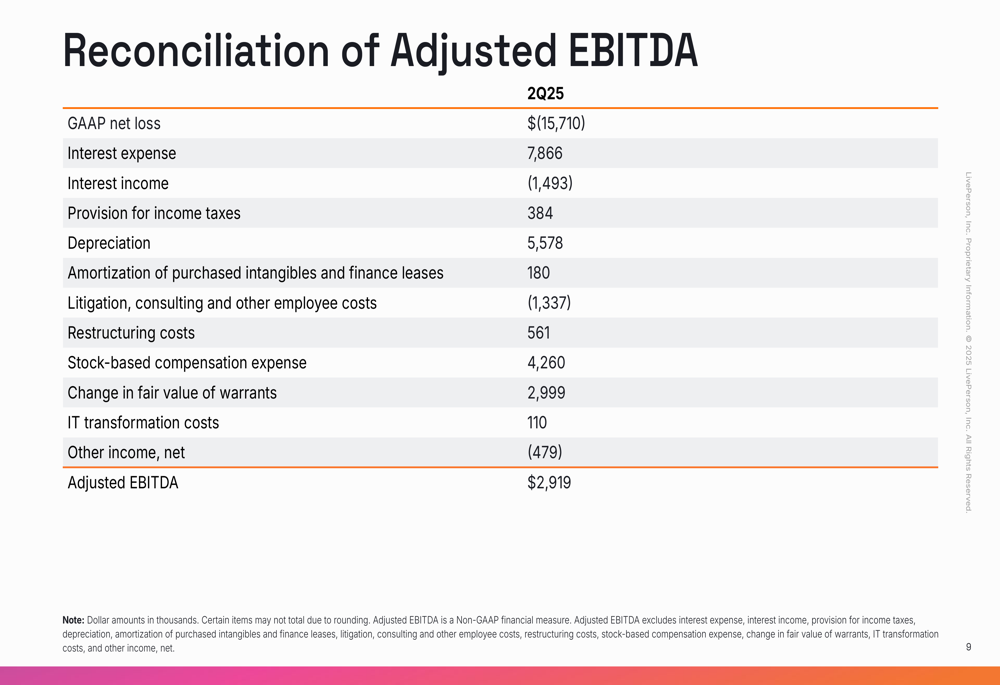

The reconciliation of adjusted EBITDA shows the various factors affecting the company’s profitability:

Strategic Initiatives & Debt Restructuring

A significant development in the quarter was LivePerson’s agreement to exchange $341.1 million of its outstanding 2026 Convertible Senior Notes for $45.0 million in cash, $115.0 million of 2029 Senior Subordinated Secured Notes, and Common and Preferred Equity. This restructuring addresses concerns about the company’s debt burden, which was highlighted as a significant issue in previous earnings reports.

The company’s strategic initiatives are summarized in the following business highlights slide:

The focus on AI capabilities appears to be gaining traction, with the 45% sequential increase in conversations leveraging LivePerson’s Generative AI capabilities representing a bright spot amid the revenue challenges. This aligns with the executive commentary from the previous quarter, where CEO John Sabino emphasized "innovation without disruption" as a key focus.

Forward-Looking Statements

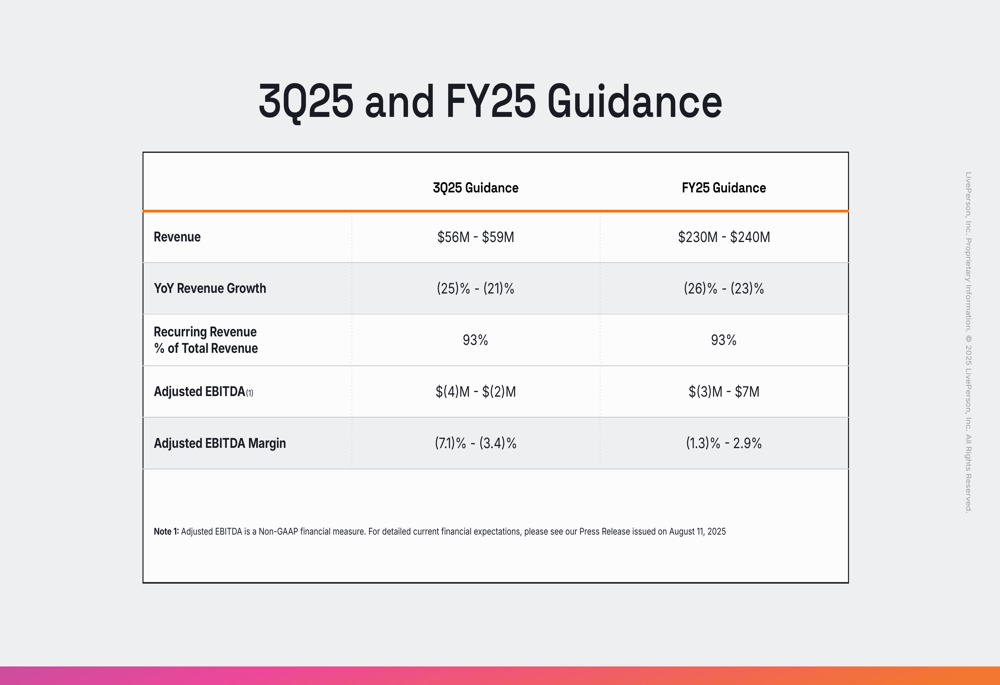

LivePerson provided guidance for both Q3 2025 and the full fiscal year, projecting continued year-over-year revenue declines but maintaining a high percentage of recurring revenue.

For Q3 2025, the company expects revenue between $56 million and $59 million, representing a year-over-year decline of 21-25%. Adjusted EBITDA is projected to be between $(4) million and $(2) million, with an adjusted EBITDA margin of (7.1)% to (3.4)%.

For the full fiscal year 2025, LivePerson anticipates revenue of $230 million to $240 million, a year-over-year decline of 23-26%. The company projects adjusted EBITDA between $(3) million and $7 million, with an adjusted EBITDA margin ranging from (1.3)% to 2.9%.

The following slide details the company’s guidance:

This guidance aligns with management’s previous statements about expecting sequential revenue declines throughout most of 2025, though the company had previously anticipated positive net new annual recurring revenue in the second half of the year. The current presentation did not specifically reaffirm this expectation, raising questions about whether the timeline for revenue stabilization has shifted.

As LivePerson continues its transformation efforts, investors will be watching closely for signs that the company’s AI investments and debt restructuring are translating into improved financial performance and a return to growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.