Durable Goods (Jun F) -9.4% vs 9.3% Prior, Ex-Trans 0.2% vs 0.2%

Introduction & Market Context

LiveRamp Holdings Inc (NYSE:RAMP) presented its fourth quarter fiscal year 2025 results on May 21, 2025, reporting 10% year-over-year revenue growth while showing signs of decelerating expansion in some key metrics. The data connectivity platform closed the trading day at $28.85, down 2.7% amid a broader market that appeared to react cautiously to the company’s results and forward guidance.

The company highlighted its predictable, recurring revenue model while demonstrating improved profitability metrics and strong cash generation capabilities. However, the presentation revealed a gradual slowdown in Annual Recurring Revenue (ARR) growth, which has decelerated from 13% year-over-year in Q2 FY25 to 8% in the most recent quarter.

Quarterly Performance Highlights

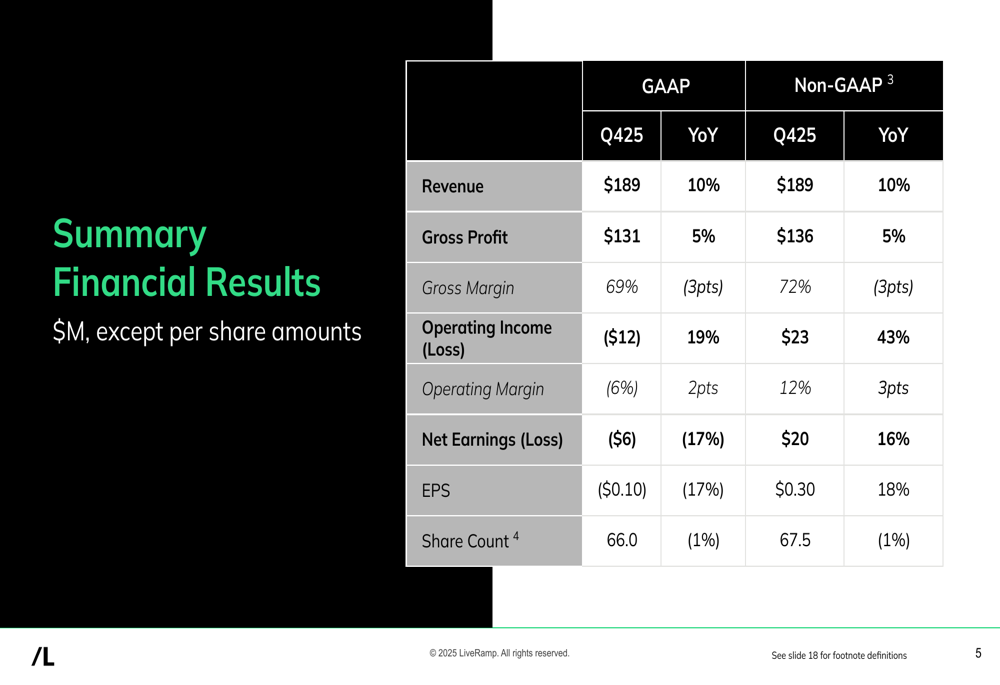

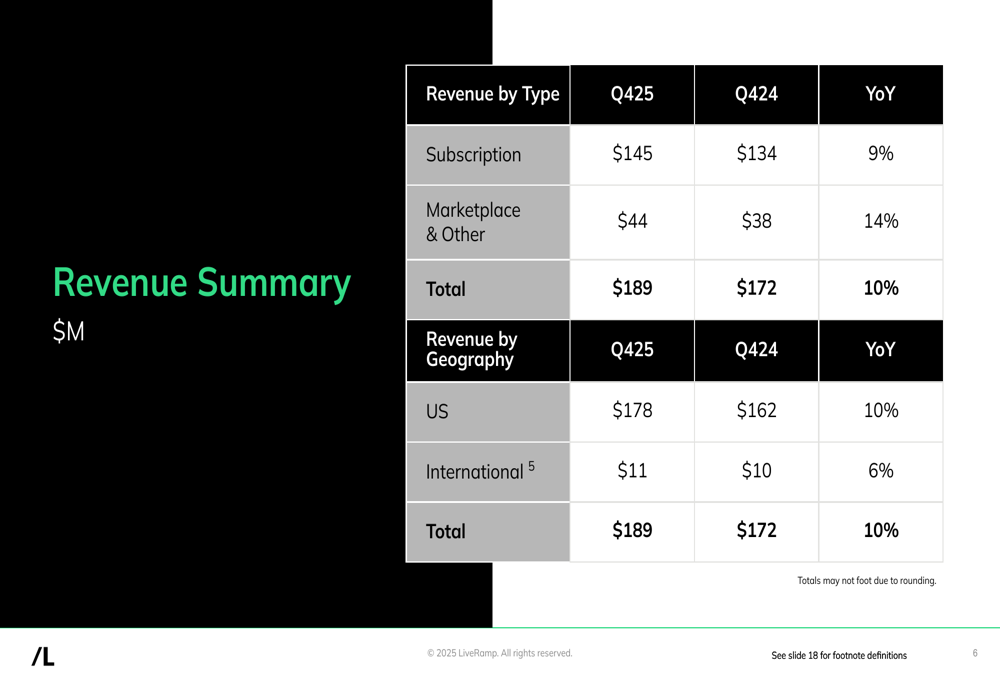

LiveRamp reported Q4 FY25 revenue of $189 million, representing a 10% increase compared to the same period last year. The company’s subscription business, which accounts for 76% of total revenue on a trailing twelve-month basis, grew 9% year-over-year to $145 million, while Marketplace & Other revenue increased 14% to $44 million.

As shown in the following summary of financial results, LiveRamp significantly improved its operating income on a non-GAAP basis while maintaining positive growth in gross profit despite some margin compression:

Non-GAAP operating income reached $23 million, up 43% year-over-year, with operating margin expanding 3 percentage points to 12%. However, gross margins declined by 3 percentage points on both a GAAP and non-GAAP basis, coming in at 69% and 72% respectively.

The company’s revenue breakdown by geography shows continued dominance of the U.S. market, which accounts for 94% of total revenue:

Detailed Financial Analysis

LiveRamp demonstrated strong cash generation capabilities in Q4 FY25, with free cash flow more than doubling year-over-year to $62 million, compared to $26 million in Q4 FY24. This improvement was driven by a significant increase in operating cash flow from $28 million to $63 million.

The company maintains a robust balance sheet with $421 million in cash and short-term investments and no debt, providing substantial financial flexibility for potential investments or acquisitions.

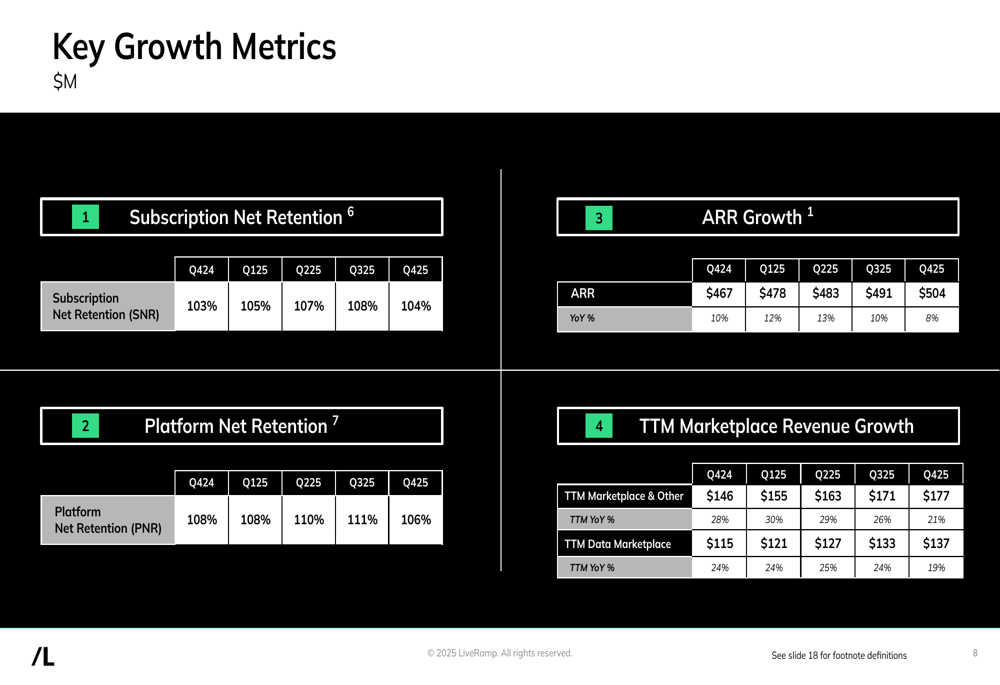

LiveRamp’s subscription-based business model continues to show resilience, with subscription net retention at 104% and platform net retention at 106% in Q4 FY25. However, both metrics have declined from their peaks in Q3 FY25 (108% and 111% respectively), suggesting some moderation in expansion within the existing customer base.

The following chart illustrates the company’s key growth metrics over recent quarters:

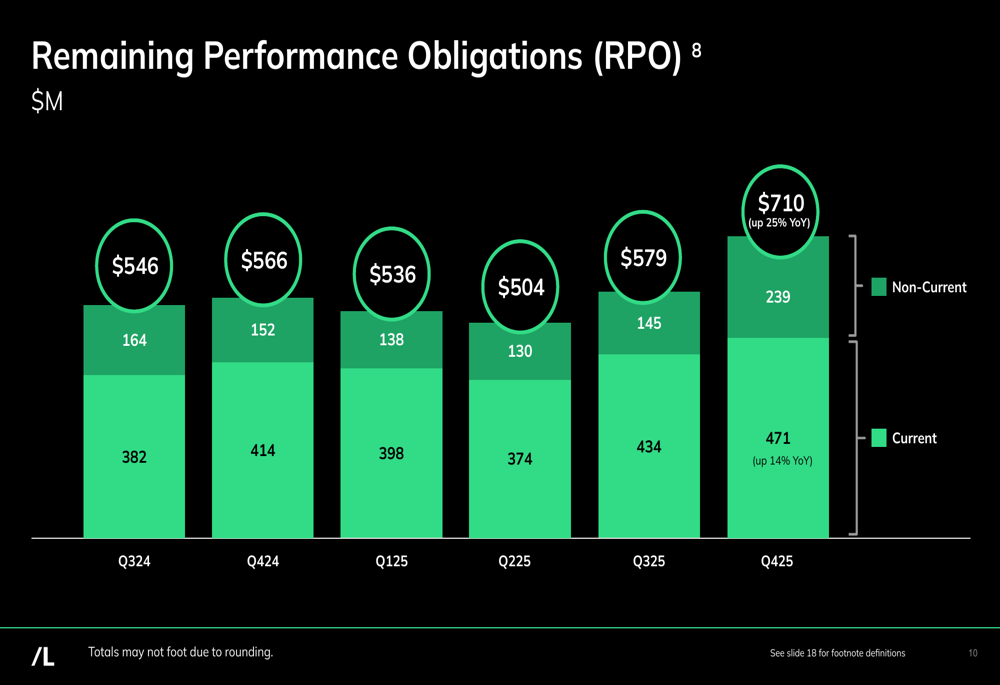

Remaining Performance Obligations (RPO), a measure of contracted future revenue, grew 25% year-over-year to $710 million, indicating a healthy pipeline of committed business. Current RPO, which represents revenue expected to be recognized within 12 months, increased 14% to $471 million.

Forward-Looking Statements

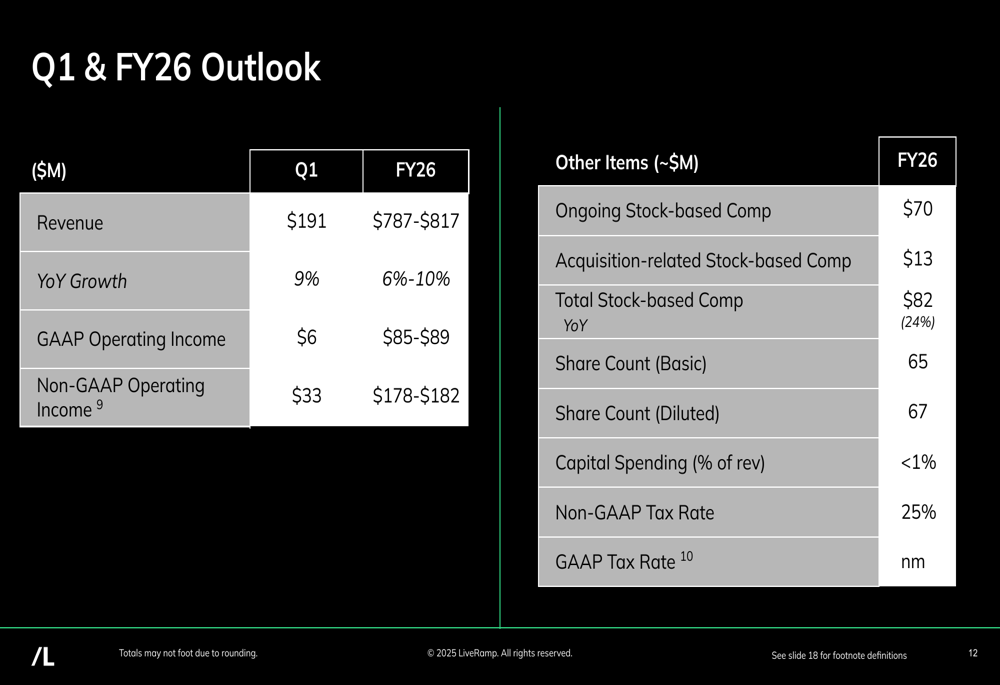

For fiscal year 2026, LiveRamp projects revenue between $787 million and $817 million, representing year-over-year growth of 6% to 10%. This guidance suggests a potential deceleration from the 10% growth achieved in Q4 FY25.

The company’s outlook for Q1 FY26 indicates revenue of $191 million, up 9% year-over-year, with non-GAAP operating income of $33 million. For the full fiscal year 2026, LiveRamp expects non-GAAP operating income between $178 million and $182 million.

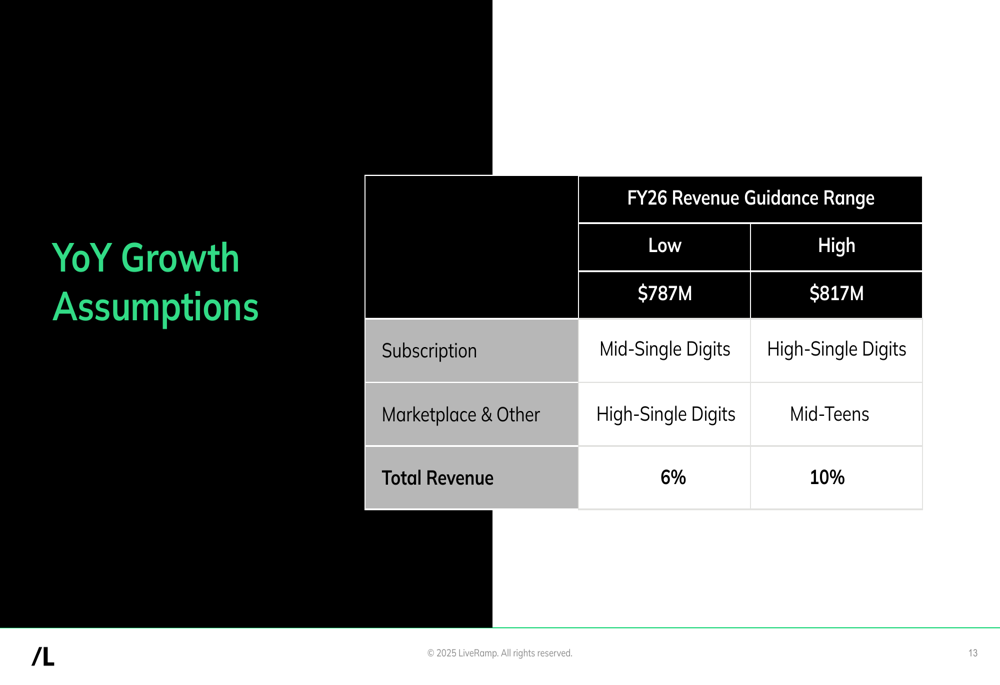

The revenue growth assumptions underlying the FY26 guidance show varying expectations across business segments:

Subscription revenue, which forms the core of LiveRamp’s business, is projected to grow at mid to high single digits, while the faster-growing Marketplace & Other segment is expected to deliver high single-digit to mid-teens growth.

Competitive Industry Position

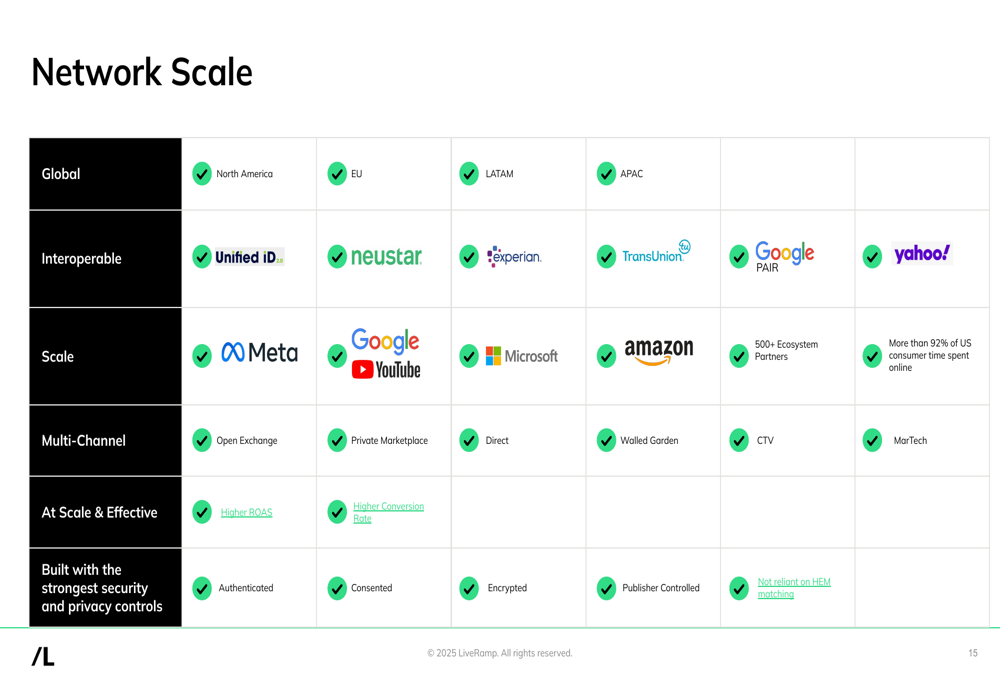

LiveRamp emphasized its extensive network scale and interoperability with major platforms as key competitive advantages. The company’s presentation highlighted partnerships with major technology and data companies including Google (NASDAQ:GOOGL), Meta (NASDAQ:META), Microsoft (NASDAQ:MSFT), Amazon (NASDAQ:AMZN), and various identity providers.

The company also showcased customer success stories across multiple industries, including hospitality (Omni Hotels & Resorts), retail (Albertsons (NYSE:ACI) Media Collective), job recruitment (Indeed), healthcare (CVS Media Exchange), and consumer packaged goods ( Danone (EPA:DANO)). These case studies demonstrate LiveRamp’s ability to deliver measurable results across diverse business sectors and use cases.

Executive Summary

LiveRamp’s Q4 FY25 results reflect a company with a stable, recurring revenue model that continues to grow while improving profitability metrics and cash generation. However, the deceleration in ARR growth and retention rates, combined with the relatively conservative outlook for FY26, suggest the company may be entering a more mature phase of its growth trajectory.

The strong balance sheet and improving operating margins provide LiveRamp with financial flexibility to navigate potential challenges while continuing to invest in strategic initiatives. Investors will likely focus on whether the company can reaccelerate growth in key metrics like ARR and subscription net retention in the coming quarters while maintaining its improved profitability profile.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.