Can anything shut down the Gold rally?

Introduction & Market Context

Logista (BME:LOG) shares fell 6.69% on Friday following the release of its H1 2025 results presentation, which revealed mixed financial performance for the six months ending March 31, 2025. The stock closed at €28.74, down from the previous close of €30.80, as investors reacted to a 5% decline in net profit despite growth in revenue and adjusted EBIT.

The Spanish logistics and distribution company, which operates primarily in Iberia, Italy, and France, reported strong top-line growth but faced headwinds from interest rate cuts and operational challenges in certain segments, particularly in France.

H1 2025 Performance Highlights

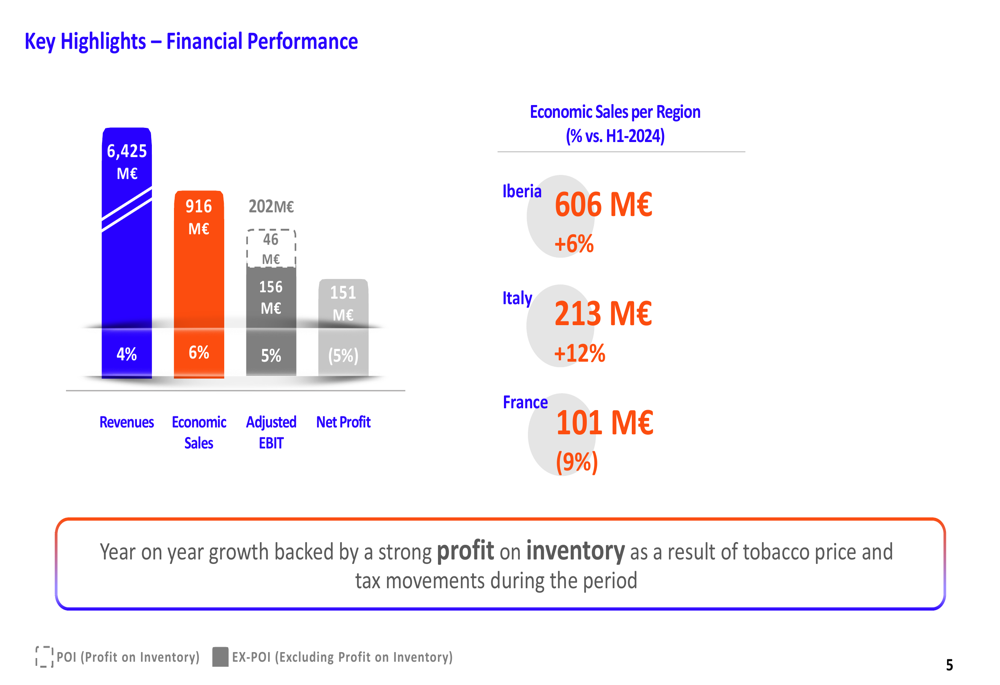

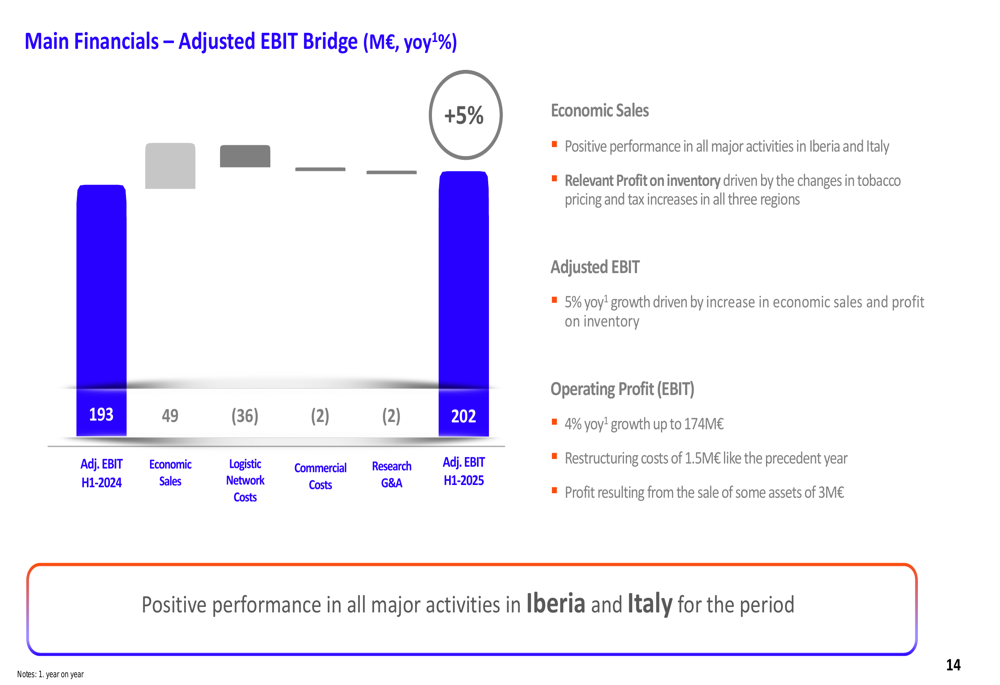

Logista reported revenues of €6,425 million for the first half of fiscal 2025, representing a 4% increase year-over-year. Economic Sales, equivalent to gross profit, rose 6% to €916 million, while Adjusted EBIT increased 5% to €202 million.

As shown in the following chart of key financial indicators, the company achieved growth in most metrics, with the notable exception of net profit:

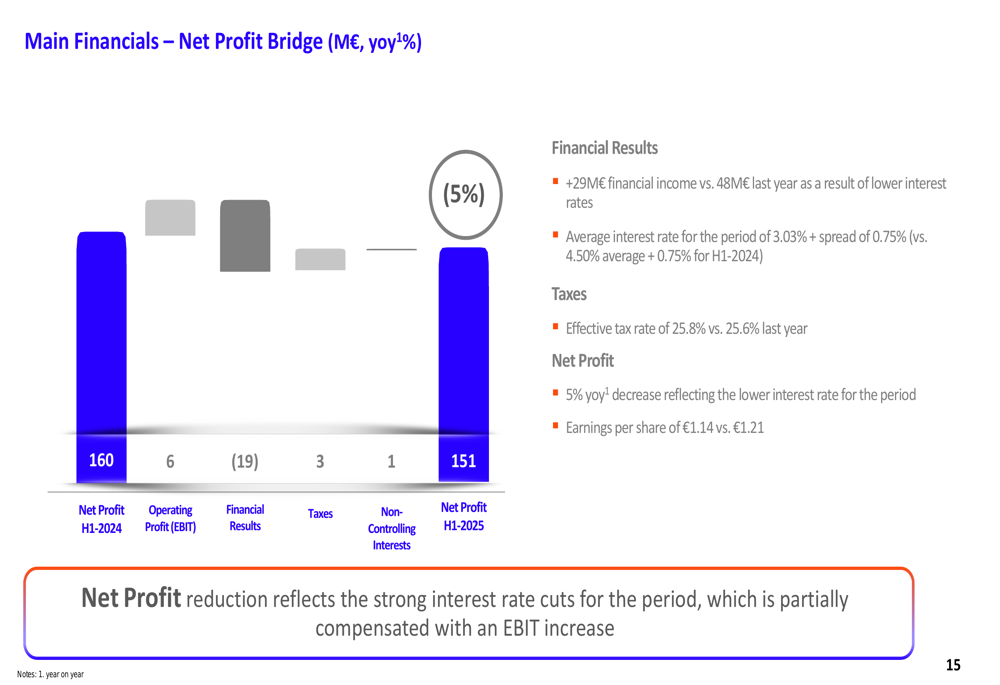

However, net profit declined 5% to €151 million, primarily due to the impact of interest rate cuts on financial results. The company’s net profit bridge illustrates how a €19 million decrease in financial results offset the positive contributions from operating profit:

Segment Analysis

Logista’s performance varied significantly across its three main geographic segments, with Italy showing the strongest results while France experienced notable declines.

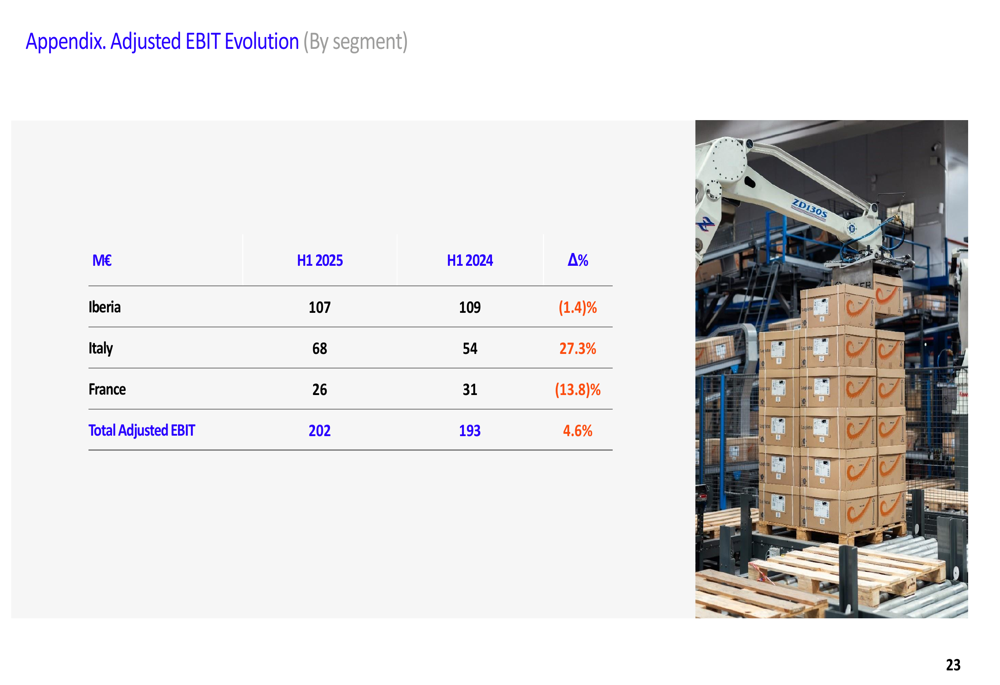

The Iberia segment, which includes Spain and Portugal, posted Economic Sales of €606 million, up 6.4% year-over-year. However, Adjusted EBIT for the region declined slightly by 1.4% to €107 million. The company highlighted 13% growth in its Pharma business and double-digit growth in its Courier business, while noting challenges in Long Distance transport.

Italy emerged as the standout performer with Economic Sales increasing 12.1% to €213 million and Adjusted EBIT surging 27.3% to €68 million. The company cited growth in tobacco distribution services in the Netherlands and continued organic growth in its Pharma business as key drivers.

In contrast, the France segment showed weakness with Economic Sales declining 9.3% to €101 million and Adjusted EBIT falling 13.8% to €26 million. This decline was primarily attributed to a 12% drop in tobacco volume.

The following table illustrates the evolution of Adjusted EBIT across the three segments:

Profit on Inventory Impact

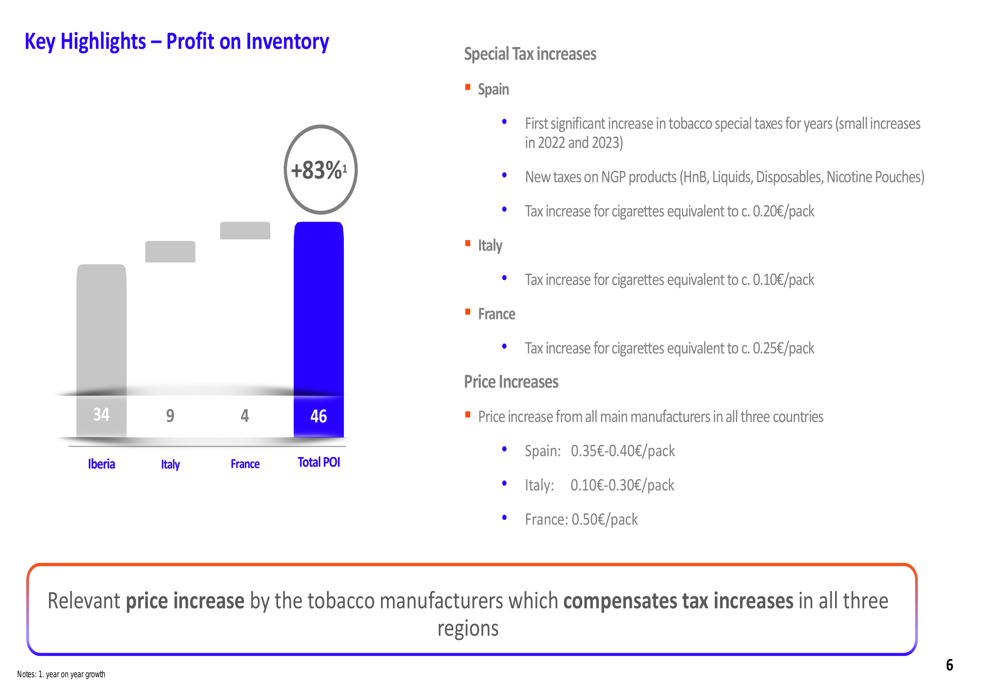

A significant factor in Logista’s financial performance was the substantial increase in Profit on Inventory (POI), which rose 83% compared to the same period last year. This increase was driven by tobacco tax and price increases across all three regions.

As shown in the following chart, the POI impact was most pronounced in Iberia:

The company benefited from the first significant increase in tobacco special taxes in Spain, along with price increases ranging from €0.35-€0.40 per pack in Spain, €0.10-€0.30 in Italy, and €0.50 in France. These increases were implemented by tobacco manufacturers to compensate for the tax hikes.

However, the reliance on POI to drive financial results raises questions about the sustainability of growth, particularly as the company noted in its outlook that Adjusted EBIT excluding POI for FY2025 is expected to be slightly below 2024 levels.

Strategic Initiatives & Outlook

Logista highlighted its ongoing diversification strategy, noting that 52% of Economic Sales now come from non-tobacco businesses. The company also detailed measures implemented to improve operations within recently acquired companies, including leadership changes and enhanced compliance and control measures.

The company’s Adjusted EBIT bridge shows how increased Economic Sales of €49 million were partially offset by higher logistics network costs of €36 million:

Looking ahead, Logista provided the following outlook for 2025:

The company remains committed to its dividend policy, pledging to distribute at least €2.09 per share, the same as in 2024. Management also indicated plans to continue seeking small and mid-size acquisitions for geographical and business diversification.

Market Reaction & Conclusion

The 6.69% drop in Logista’s share price following the results presentation suggests investors were concerned about the decline in net profit and the company’s reliance on one-time tobacco tax and price increases to drive performance.

While the company’s diversification strategy and growth in non-tobacco businesses represent positive long-term developments, the expected decline in Adjusted EBIT excluding POI for FY2025 points to potential underlying operational challenges.

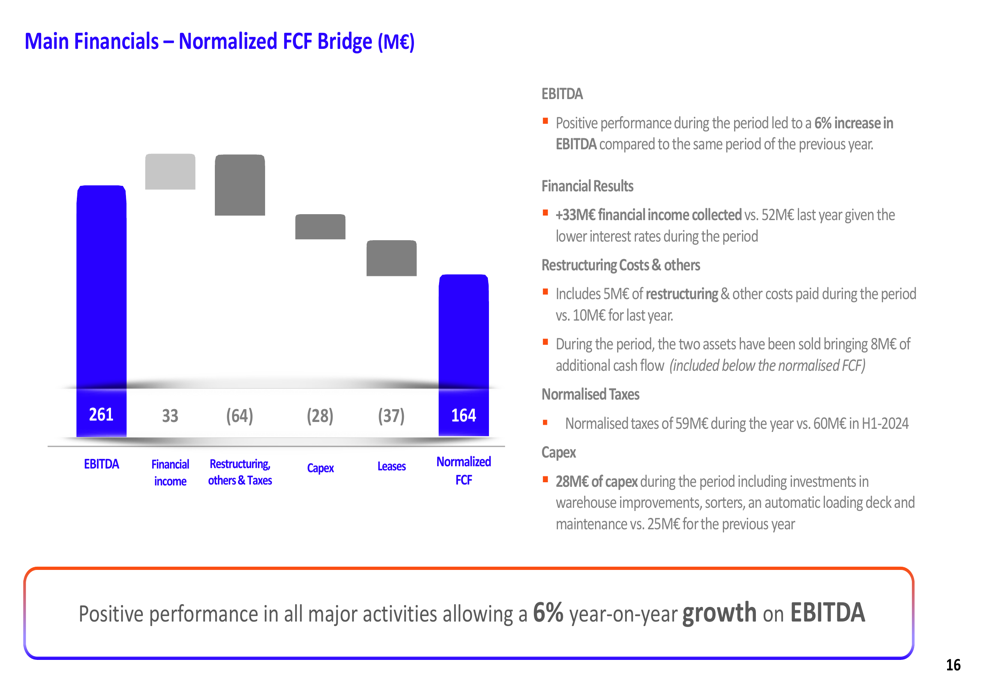

The company’s normalized free cash flow remained strong at €164 million, as illustrated in the following bridge chart:

As Logista continues to navigate a challenging environment, particularly in France, investors will likely focus on the company’s ability to generate sustainable growth beyond the temporary boost from tobacco price and tax increases, while monitoring progress in its diversification strategy and operational improvements in acquired businesses.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.