IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

LSB Industries (NYSE:LXU) presented its Q2 2025 earnings results on July 30, 2025, revealing increased sales volumes but compressed margins due to higher natural gas costs. The stock fell 11.42% following the announcement, closing at $7.72, reflecting investor concerns about profitability despite volume growth.

The chemical manufacturer reported diluted earnings per share of $0.04, down from $0.13 in the same quarter last year, continuing a challenging trend after missing EPS expectations in Q1 2025. While the company made progress on strategic initiatives, including its El Dorado low-carbon ammonia project, the financial results highlighted ongoing operational pressures.

Quarterly Performance Highlights

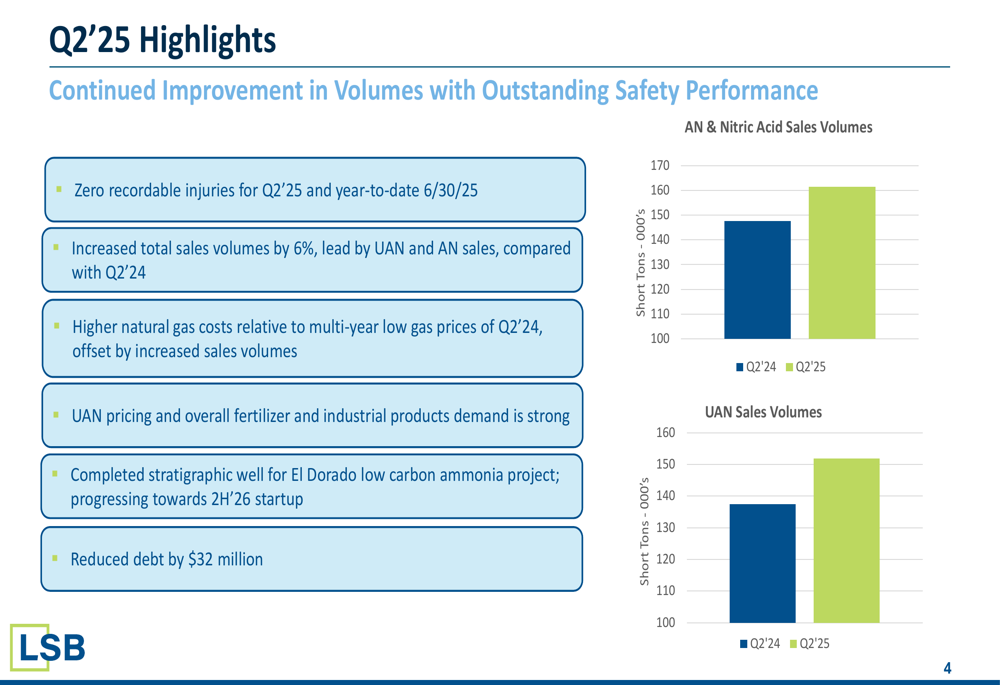

LSB reported zero recordable injuries for Q2 2025 and year-to-date, maintaining its safety record while achieving a 6% increase in total sales volume compared to Q2 2024, primarily driven by UAN (urea ammonium nitrate) and AN (ammonium nitrate) sales.

As shown in the following chart of quarterly sales volumes:

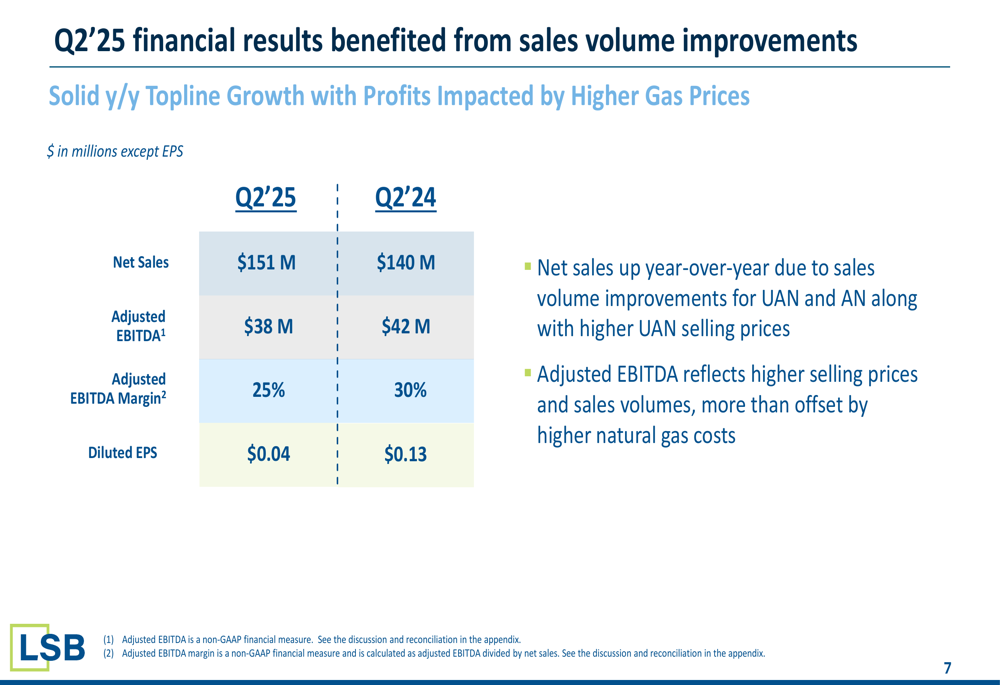

The company’s net sales increased to $151 million in Q2 2025, up from $140 million in Q2 2024. However, adjusted EBITDA declined to $38 million from $42 million in the prior-year period, with adjusted EBITDA margin contracting to 25% from 30%. Diluted EPS fell to $0.04 from $0.13 year-over-year.

Detailed Financial Analysis

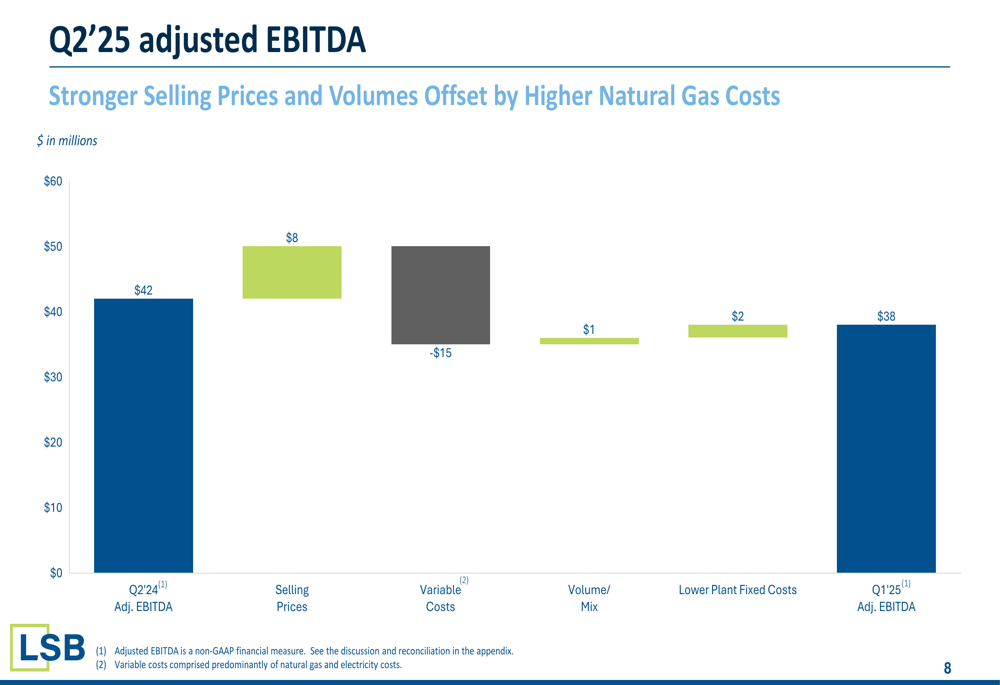

The primary factor impacting LSB’s profitability was higher natural gas costs, which more than offset the benefits from increased sales volumes and higher UAN prices. The company’s waterfall chart clearly illustrates this dynamic:

While selling prices contributed positively with an $8 million boost to adjusted EBITDA, variable costs (primarily natural gas) reduced EBITDA by $15 million. Volume/mix improvements and lower plant fixed costs provided modest offsets of $1 million and $2 million respectively.

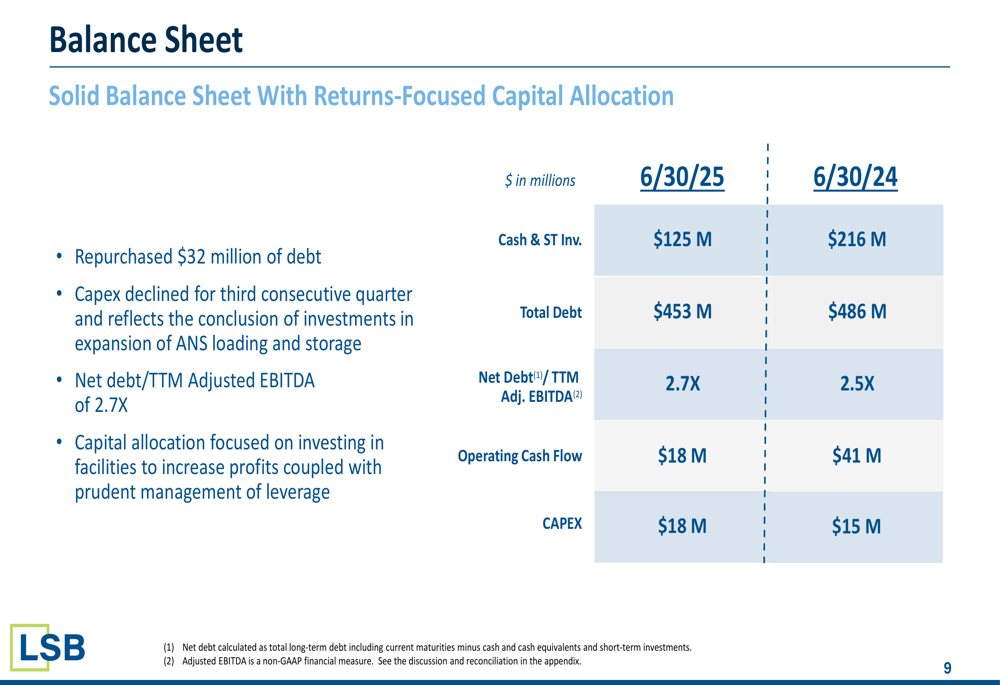

On the balance sheet side, LSB continued its debt reduction efforts, repurchasing $32 million of debt during the quarter. However, the company’s cash position declined significantly to $125 million as of June 30, 2025, compared to $216 million a year earlier. The net debt to trailing twelve-month adjusted EBITDA ratio increased slightly to 2.7x from 2.5x in the prior year.

Operating cash flow decreased substantially to $18 million from $41 million in the prior-year period, while capital expenditures increased slightly to $18 million from $15 million, reflecting continued investment in facilities despite margin pressures.

Strategic Initiatives

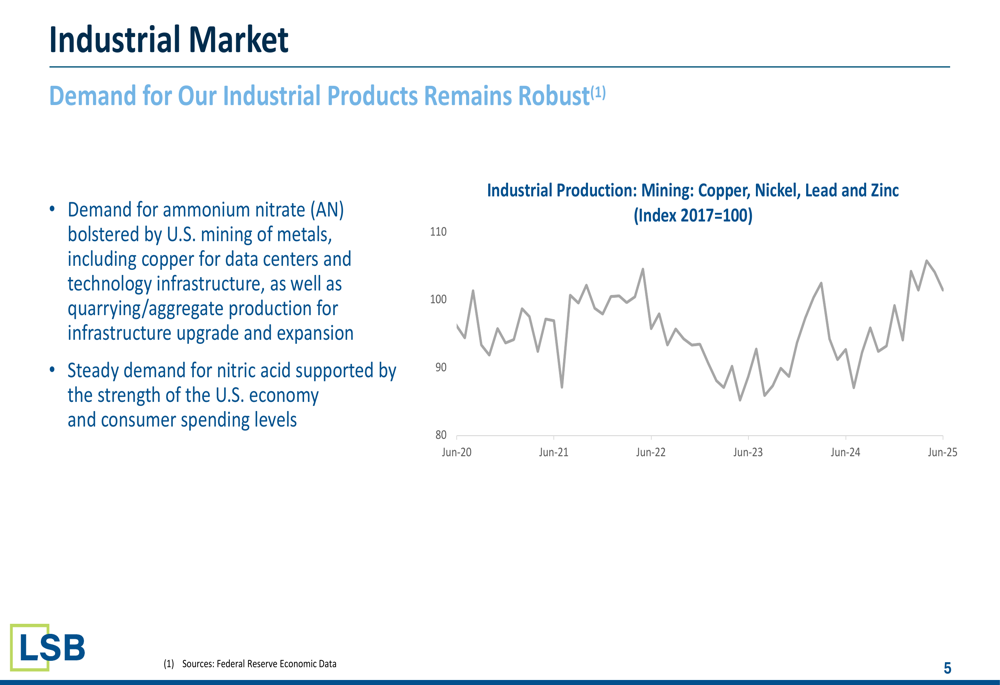

LSB highlighted robust demand for its industrial products, particularly ammonium nitrate, which is benefiting from increased U.S. mining of metals, including copper for data centers, and quarrying/aggregate production for infrastructure upgrades.

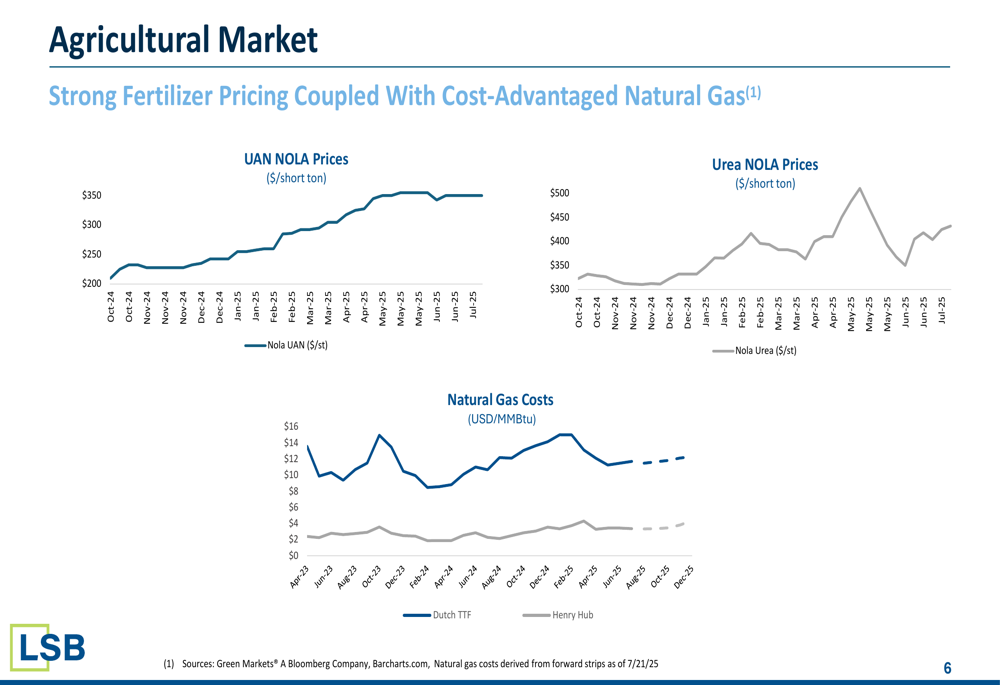

In the agricultural market, the company noted strong fertilizer pricing coupled with its cost-advantaged natural gas position, though this advantage has been partially eroded by rising natural gas costs.

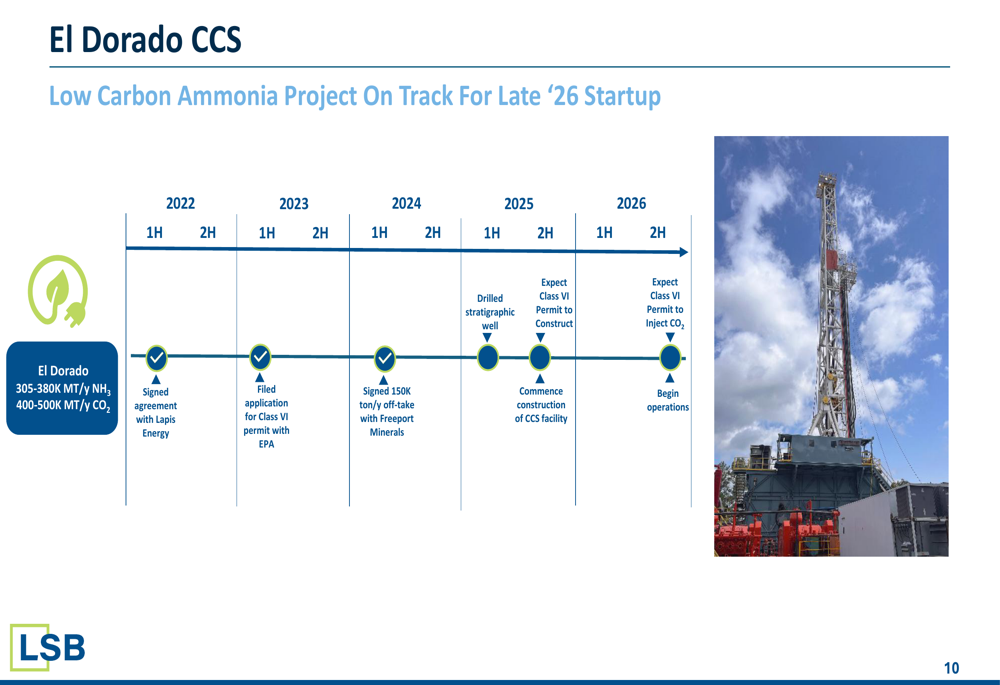

A key strategic focus remains the El Dorado Carbon Capture and Storage (CCS) project, which is on track for late 2026 startup. The company recently completed a stratigraphic well for the project and signed a 150,000 ton/year off-take agreement with Freeport Minerals in 2024. When operational, El Dorado is expected to produce 305-380K MT/year of ammonia and capture 400-500K MT/year of CO2.

Forward-Looking Statements

Looking ahead, LSB faces continued challenges balancing volume growth with cost pressures. The company’s focus on increasing cost-plus contracts, which reached approximately 30% in Q1 2025 with a target of 35% by year-end (as mentioned in the previous earnings call), represents a strategic shift toward more predictable revenue streams.

The El Dorado CCS project remains a significant long-term growth driver, positioning LSB to capitalize on increasing demand for low-carbon ammonia. However, in the near term, the company must navigate volatile natural gas prices and competitive market dynamics.

After reporting an EPS miss in Q1 2025 and continued margin compression in Q2, investor focus will likely remain on LSB’s ability to control costs while maintaining volume growth. The stock’s performance, now trading well below its 52-week high of $10.40, reflects these ongoing concerns despite the company’s strategic initiatives and debt reduction efforts.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.