Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Luxfer Holdings PLC (NYSE:LXFR) reported strong second-quarter results on July 30, 2025, with adjusted earnings per share rising 25% year-over-year, driven primarily by robust performance in its defense and aerospace markets. The materials technology company’s presentation highlighted continued momentum from its first quarter results, with sequential improvement in both revenue and profitability.

Quarterly Performance Highlights

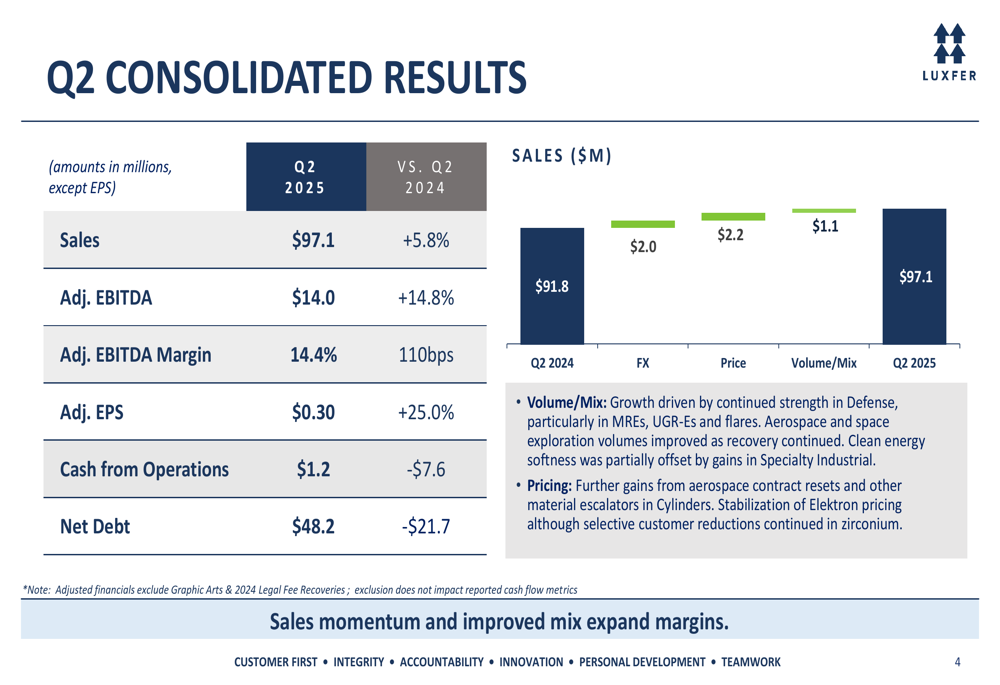

Luxfer reported Q2 2025 adjusted sales of $97.1 million, up 5.8% compared to the same period last year. Adjusted EBITDA increased 14.8% to $14.0 million, with margins expanding 110 basis points to 14.4%. Adjusted earnings per share reached $0.30, representing a 25% year-over-year increase and a 30% sequential improvement from Q1’s $0.23.

As shown in the following chart of consolidated results:

The company’s cash from operations was $1.2 million, down $7.6 million from the prior year. Net debt stood at $48.2 million, a decrease of $21.7 million year-over-year, though slightly higher than the $41.9 million reported at the end of Q1 2025.

"Strong EPS growth and margin performance were key highlights this quarter, with adjusted EPS rising 25% year-over-year and EBITDA margins expanding 110 basis points sequentially," the company noted in its presentation.

Segment Analysis

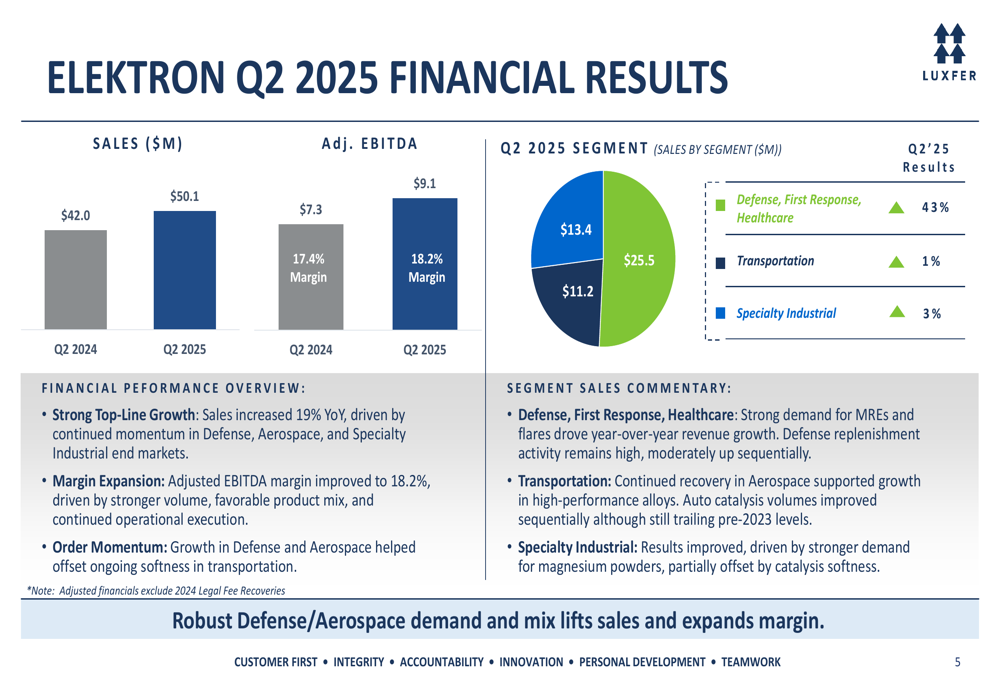

Luxfer’s performance showed a clear divergence between its two main segments. The Elektron segment, which focuses on magnesium alloys and powders, delivered exceptional results with sales of $50.1 million, up 19.3% from $42.0 million in Q2 2024. Adjusted EBITDA for this segment increased to $9.1 million from $7.3 million, with margins improving to 18.2%.

The segment breakdown reveals the strength in Luxfer’s defense, first response, and healthcare markets:

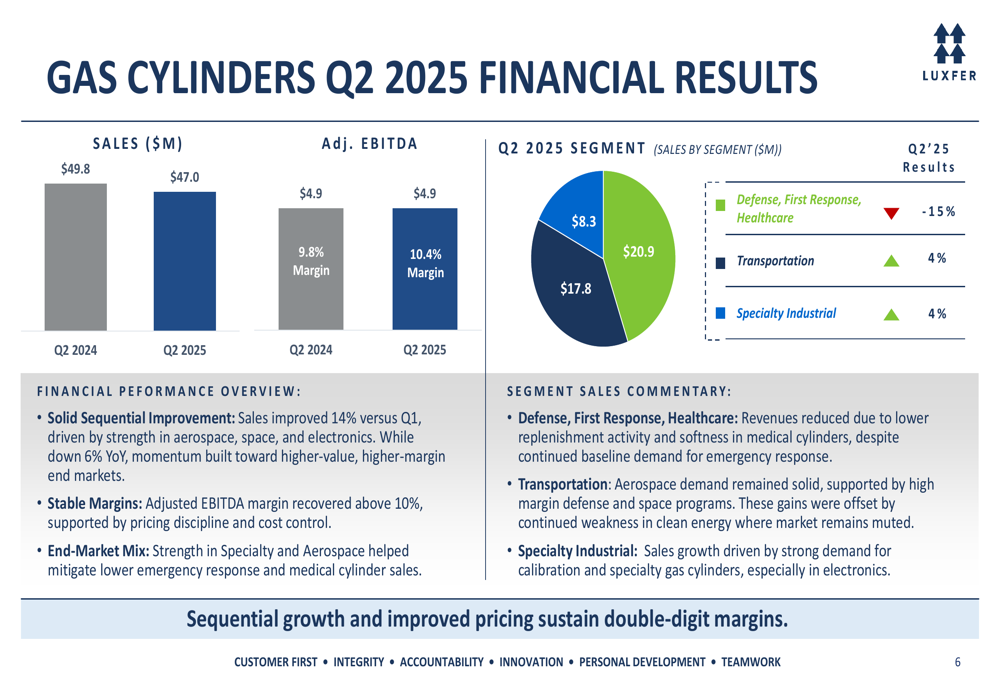

In contrast, the Gas Cylinders segment experienced a revenue decline to $47.0 million from $49.8M in the prior year. Despite the sales decrease, the segment maintained its adjusted EBITDA at $4.9 million and improved its margin to 10.4% from 9.8% in Q2 2024.

The following chart illustrates the Gas Cylinders segment performance:

This segment performance aligns with trends observed in Q1, where the company noted continued weakness in the alternative fuel cylinder market while seeing strength in defense and aerospace applications.

Strategic Initiatives & Outlook

Luxfer highlighted several strategic moves during the quarter, including the completed divestiture of its Graphic Arts business, which the company described as sharpening "focus on high-margin, core growth platforms." The company is also undertaking operational optimization, including the initiation of a Pomona relocation project expected to streamline its manufacturing footprint.

The presentation emphasized Luxfer’s strategic pivot toward higher-margin opportunities in aerospace, space exploration, and defense markets, building on momentum seen in these sectors.

As shown in the company’s key highlights and achievements:

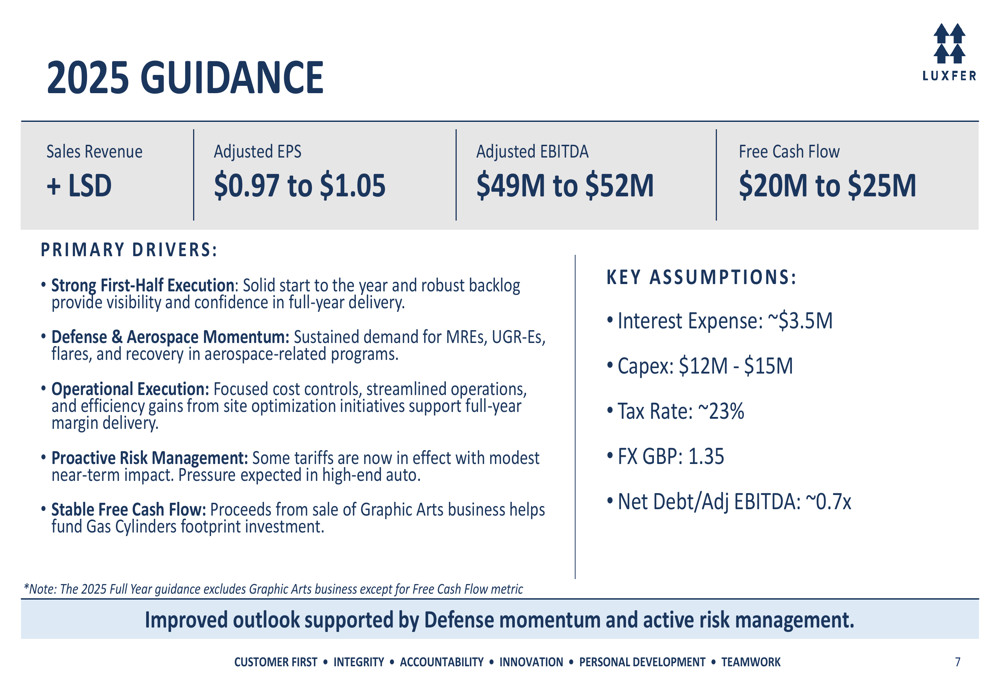

For the full year 2025, Luxfer maintained its guidance, projecting:

The company expects sales revenue to increase in the low single digits, with adjusted EPS between $0.97 and $1.05. Adjusted EBITDA is projected between $49 million and $52 million, with free cash flow of $20-$25 million.

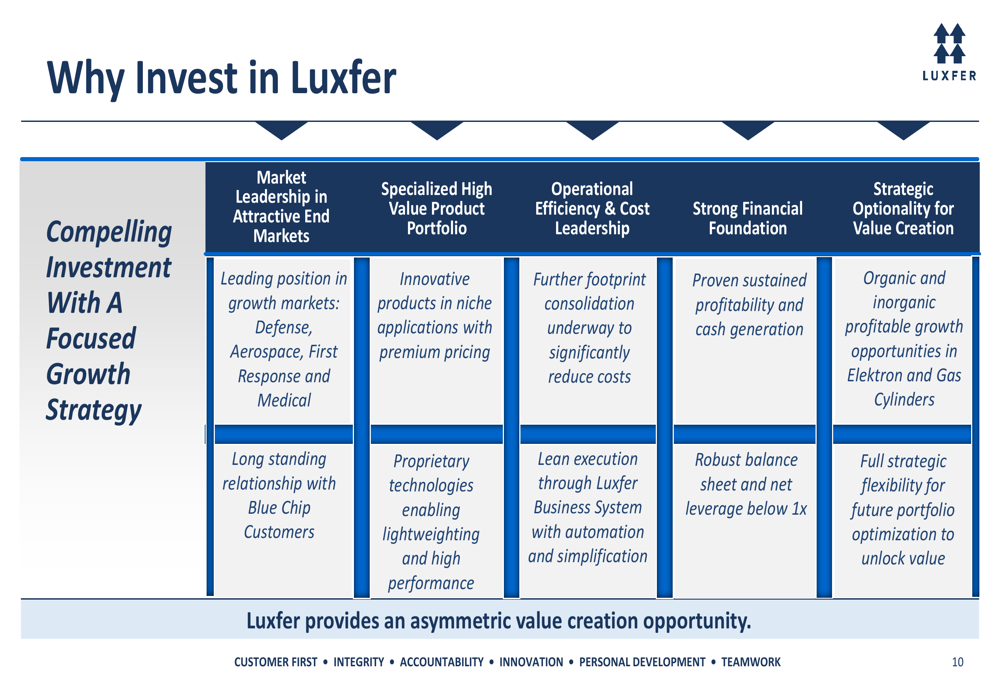

Financial Position & Investment Case

Luxfer continues to maintain a strong balance sheet with net leverage at 0.9x adjusted EBITDA. The company’s presentation emphasized its market leadership in attractive end markets, specialized high-value product portfolio, and operational efficiency as key investment considerations.

The following slide outlines Luxfer’s investment case:

The company highlighted its "strong financial foundation" through "proven sustained profitability and cash generation" and a "robust balance sheet with net leverage below 1x." This financial stability provides Luxfer with "strategic optionality" for both organic and inorganic growth opportunities.

Luxfer’s stock closed at $12.28 on July 29, 2025, up 0.9% ahead of the earnings release. The shares have traded between $9.41 and $15.64 over the past 52 weeks, according to available market data.

The Q2 results represent a continuation of the positive momentum seen in Q1 2025, when Luxfer exceeded EPS expectations but missed revenue forecasts. The current quarter shows improvement on both metrics, with particular strength in the company’s high-margin defense and aerospace markets offsetting continued challenges in certain industrial sectors.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.