Sprouts Farmers Market closes $600 million revolving credit facility

Introduction & Market Context

Macy’s Inc. (NYSE:M) presented its first quarter 2025 earnings results on May 28, 2025, revealing a mixed performance across its portfolio of brands. The department store retailer reported better-than-expected results for the quarter but significantly lowered its full-year guidance, citing concerns about tariff impacts and challenging market conditions.

The company’s stock, which closed at $12.04 on May 27, showed signs of recovery in pre-market trading, up 1.41% to $12.21. This comes after shares have struggled near their 52-week low of $9.76, well off their 52-week high of $20.47.

Quarterly Performance Highlights

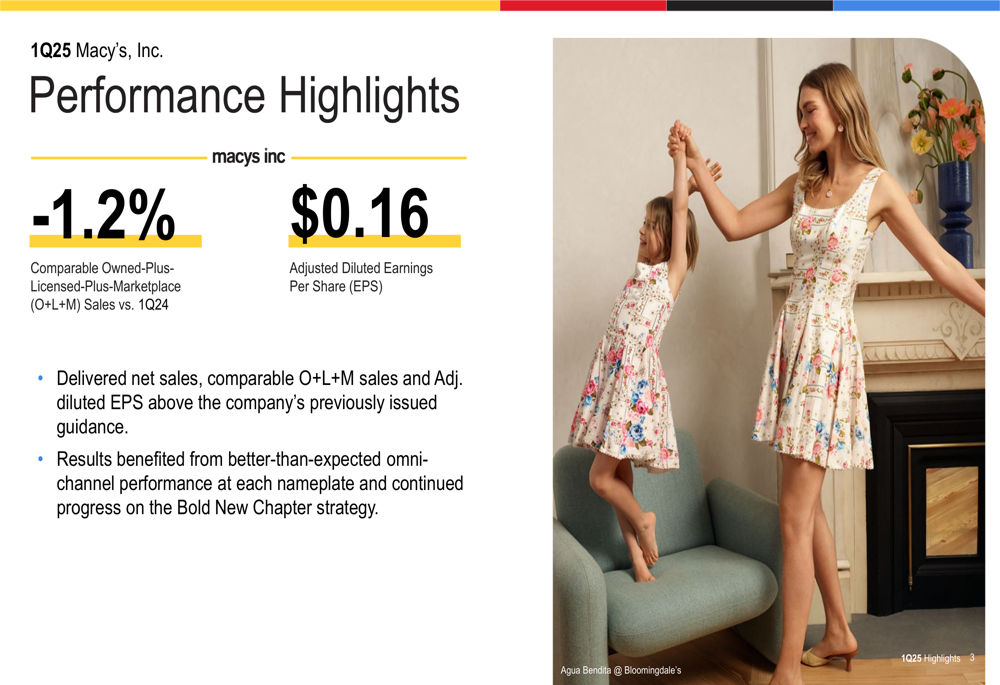

Macy’s reported first-quarter net sales of $4.6 billion, representing a 5.1% decline compared to the same period last year. Comparable Owned-Plus-Licensed-Plus-Marketplace (O+L+M) sales decreased by 1.2% year-over-year, while adjusted diluted earnings per share came in at $0.16, down 40.7% from Q1 2024.

Despite these declines, the company noted that both sales and earnings exceeded their previously issued guidance, driven by better-than-expected omni-channel performance across all nameplates and continued progress on the company’s Bold New Chapter strategy.

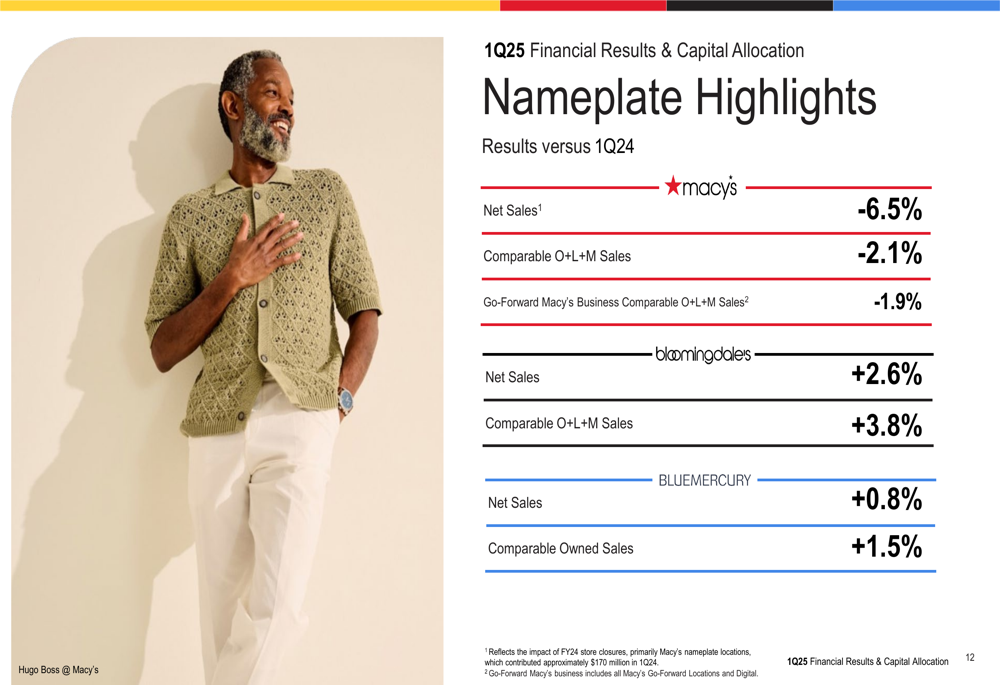

Performance varied significantly across Macy’s portfolio of brands. The flagship Macy’s nameplate struggled with a 2.1% decline in comparable O+L+M sales, though the company’s Reimagine 125 locations (stores selected for strategic reinvestment) outperformed with a more modest 0.8% decline.

In contrast, Bloomingdale’s delivered strong results with comparable O+L+M sales increasing 3.8%, benefiting from brand launches including Prada (OTC:PRDSY) shoes and handbags online, Reformation RTW, and Burberry (LON:BRBY) men’s and RTW. The luxury department store also saw approximately 55% growth in marketplace gross merchandise value compared to Q1 2024.

Bluemercury, the company’s beauty retail chain, continued its positive trajectory with comparable owned sales increasing 1.5%, marking its 17th consecutive quarter of comparable owned sales growth. This performance was driven by new and remodeled locations, strength in dermatological skincare, recent brand launches, and improved loyalty communications.

Strategic Initiatives

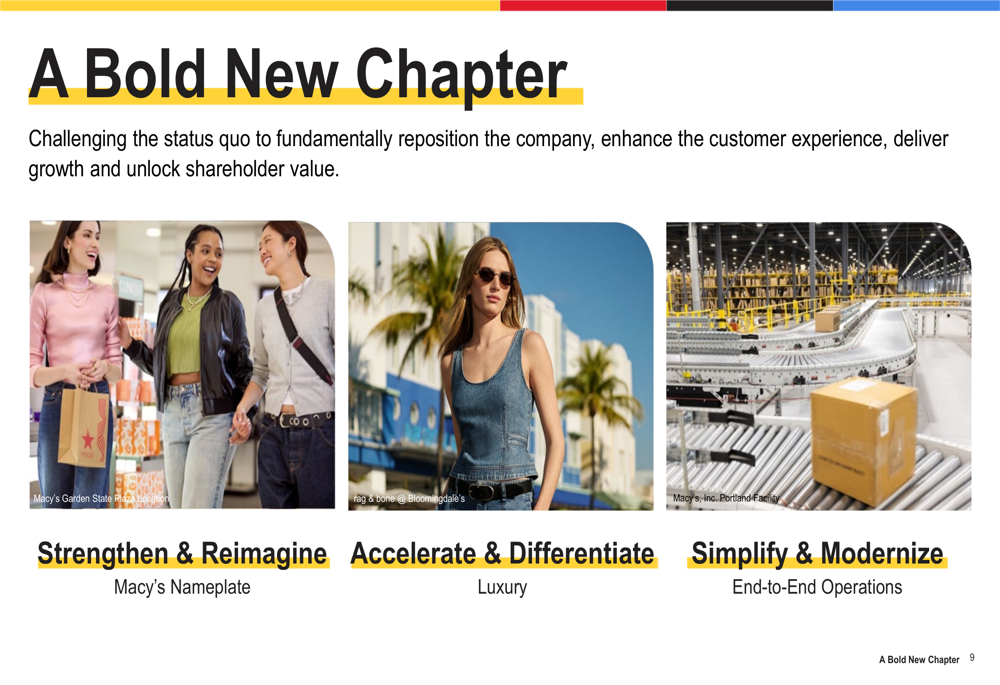

Macy’s continued to advance its Bold New Chapter strategy, which focuses on three key pillars: Strengthen & Reimagine the Macy’s nameplate, Accelerate & Differentiate luxury offerings, and Simplify & Modernize end-to-end operations.

The company highlighted progress in its Reimagine 125 initiative, with these locations outperforming across all categories. Additionally, Backstage store-within-store locations outperformed the full-line Macy’s stores in which they operate by several hundred basis points, while the Macy’s Marketplace achieved approximately 40% growth in gross merchandise value compared to Q1 2024.

On the operational front, Macy’s reported a 0.5% reduction in inventory compared to Q1 2024, reflecting a disciplined approach to receipts. The company also improved its speed of delivery by 340 basis points year-over-year as part of its efforts to modernize operations.

Tariff Impact & Mitigation

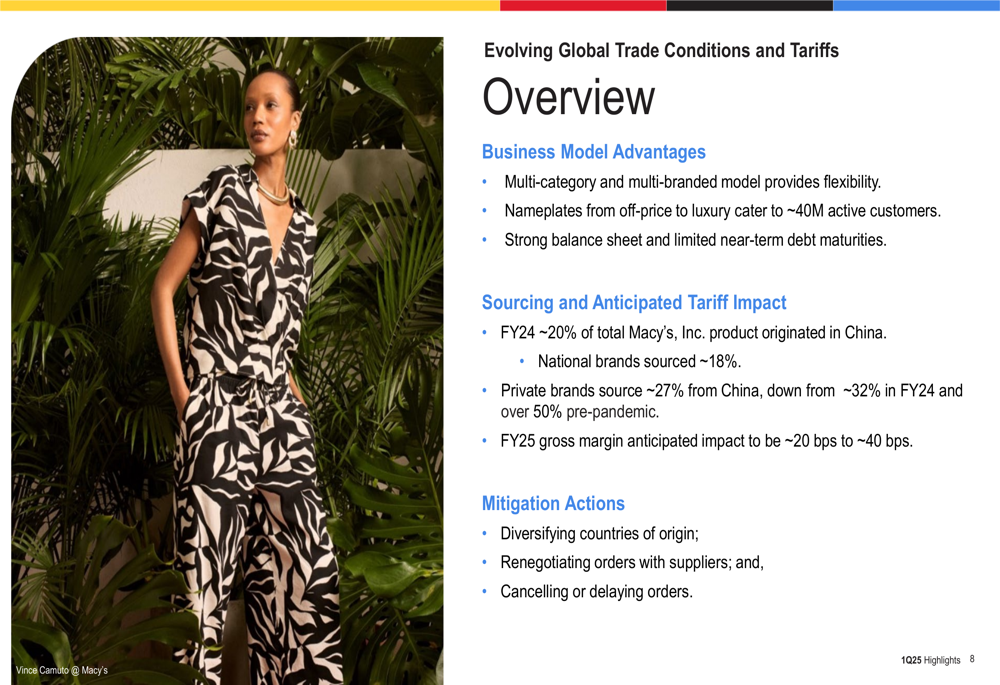

A significant portion of the presentation addressed concerns about evolving global trade conditions and tariffs, particularly regarding Chinese imports. Macy’s disclosed that approximately 20% of its total product originated in China in fiscal year 2024, with national brands sourcing about 18% and private brands about 27% from China.

The company has been actively reducing its China sourcing exposure, noting that private brand sourcing from China has decreased from over 50% pre-pandemic to approximately 27% currently. Despite these efforts, Macy’s anticipates tariffs will impact its fiscal year 2025 gross margin by approximately 20 to 40 basis points, translating to $0.10 to $0.25 of annual EPS.

To mitigate these impacts, the company outlined several strategies including diversifying countries of origin, renegotiating orders with suppliers, and canceling or delaying certain orders. Macy’s emphasized that its multi-category and multi-branded model provides flexibility to navigate these challenges.

Revised Guidance & Outlook

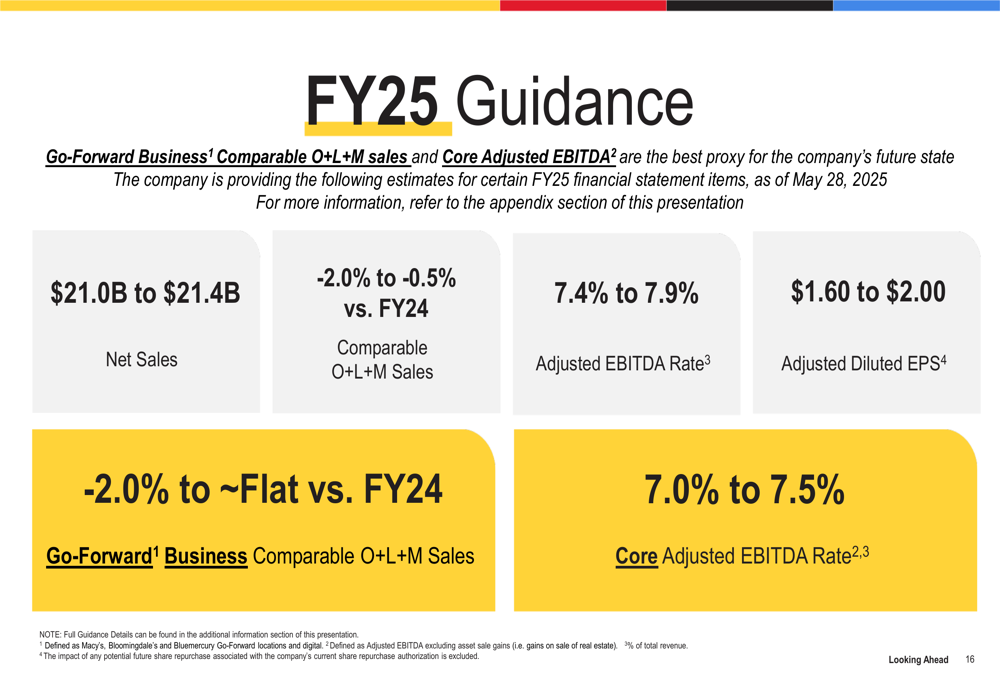

Perhaps the most significant news from the presentation was Macy’s substantial downward revision to its full-year 2025 guidance. The company maintained its net sales forecast of $21.0 billion to $21.4 billion and comparable sales expectations of -2.0% to -0.5%, but significantly reduced its profitability outlook.

Adjusted diluted EPS guidance was cut to $1.60-$2.00 from the previous $2.05-$2.25 range provided in March. Similarly, the company lowered its Adjusted EBITDA margin rate guidance to 7.4%-7.9% from 8.4%-8.6%, and Core Adjusted EBITDA margin rate to 7.0%-7.5% from 8.0%-8.2%.

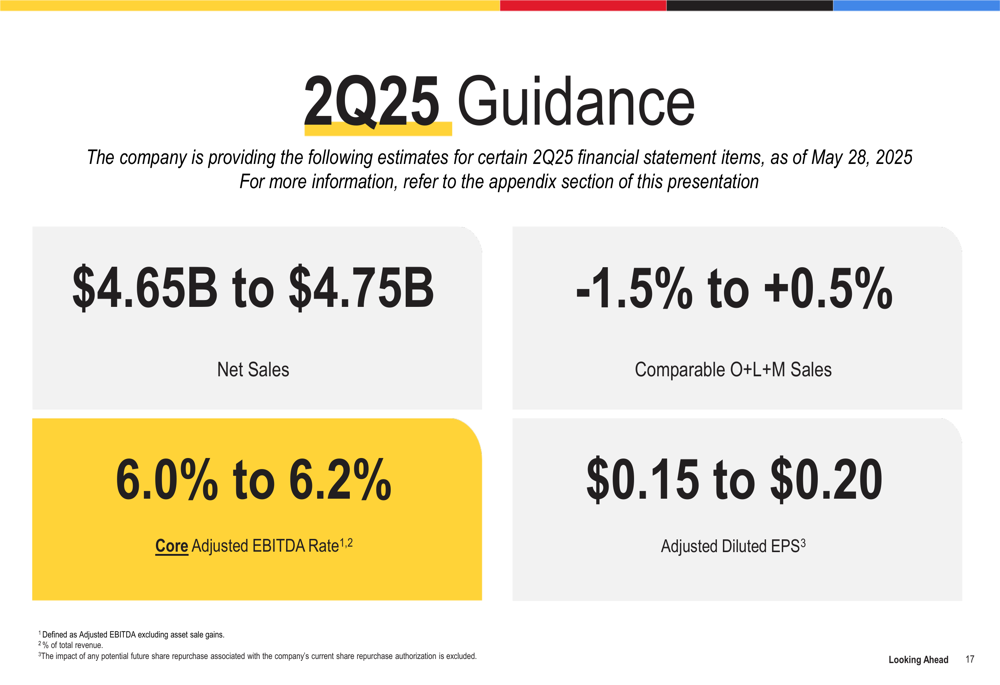

For the second quarter of 2025, Macy’s expects net sales of $4.65 billion to $4.75 billion, with comparable O+L+M sales ranging from -1.5% to +0.5%. Adjusted diluted EPS is projected to be between $0.15 and $0.20.

The guidance revision reflects several factors, including the anticipated impact of tariffs on Chinese imports and a more challenging consumer environment. The company noted that the tariff impact is expected to be most pronounced in the second quarter as products bought under the higher tariff rates flow through.

Capital Allocation Strategy

Despite the challenges, Macy’s continues to return capital to shareholders. In the first quarter, the company paid $51 million in dividends and repurchased $101 million in shares. Management emphasized three capital allocation priorities: maintaining a healthy balance sheet and driving working capital efficiencies, strategically investing in growth initiatives while lowering capital expenditures, and returning capital to shareholders via dividends and share buybacks.

Macy’s financial position remains relatively stable with limited near-term debt maturities, providing flexibility as the company navigates the current retail environment. The company’s disciplined approach to inventory management and operational improvements continue to support its financial strategy.

In conclusion, while Macy’s delivered better-than-expected results for the first quarter of 2025, the significant downward revision to full-year guidance signals ongoing challenges for the department store retailer. The divergent performance across nameplates—with luxury and beauty segments outperforming the core Macy’s business—highlights the company’s complex position in a rapidly evolving retail landscape, further complicated by tariff concerns and shifting consumer preferences.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.