Trump meets Zelenskiy, says Putin wants war to end, mulls trilateral talks

Introduction & Market Context

MainStreet Bancshares, Inc. (NASDAQ:MNSB) presented its second quarter 2025 results on July 22, highlighting significant improvements in profitability metrics and strategic positioning. The bank, which has served the Washington, DC Metropolitan area for over 21 years, operates in a market characterized by high median household income ($125,027) and substantial home values ($907,420).

The bank’s presentation emphasized its presence in a diverse market supported by major universities, federal contractors, and Fortune 500 companies, providing a stable foundation for its operations. With just six branches managing $2.1 billion in assets, MainStreet’s branch-light strategy has enabled it to achieve $12.2 million in assets per employee, indicating strong operational efficiency.

Quarterly Performance Highlights

MainStreet Bancshares reported substantial improvement in its key performance metrics for Q2 2025. Earnings per share jumped to $0.53, more than doubling from $0.25 in the previous quarter and significantly outperforming the $0.27 reported in the same quarter last year. This 20.45% positive surprise against analyst expectations of $0.44 drove an initial 8.35% increase in the stock price following the announcement.

Return on average assets (ROAA) improved to 0.86% from 0.46% in Q1 2025, while return on average tangible common equity (ROATCE) surged to 8.84% from 4.29%. The bank’s net interest margin expanded significantly to 3.75% from 3.30% in the previous quarter.

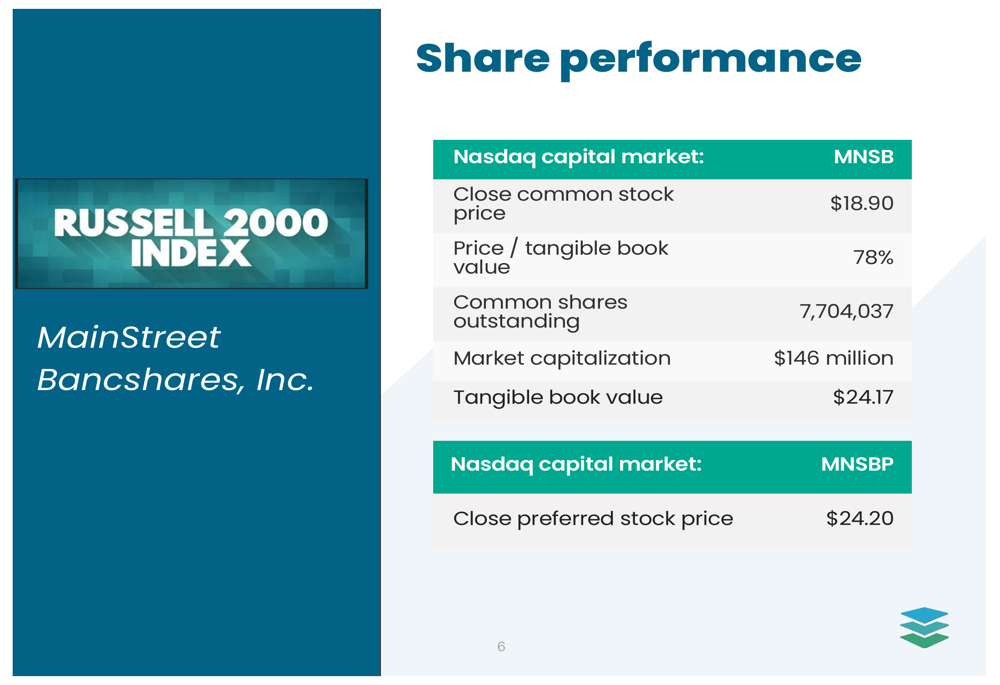

As shown in the following quarterly financial summary:

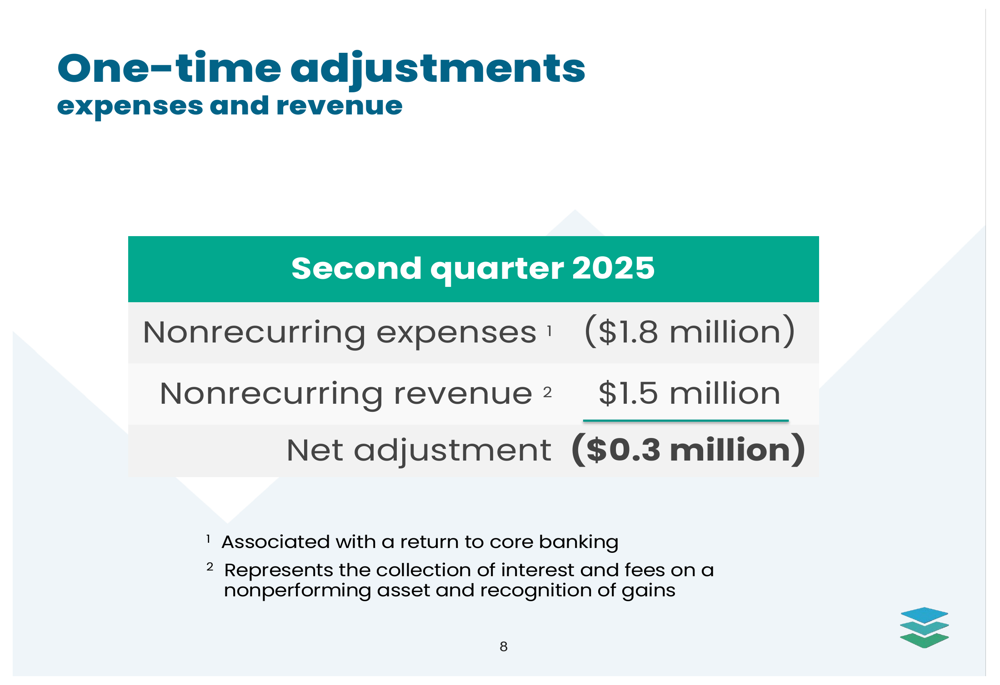

The bank reported one-time adjustments in Q2 2025, including $1.8 million in nonrecurring expenses associated with a return to core banking and $1.5 million in nonrecurring revenue from the collection of interest and fees on a nonperforming asset, resulting in a net adjustment of -$0.3 million.

Detailed Financial Analysis

MainStreet’s balance sheet showed total assets of $2.115 billion in Q2 2025, a decrease from $2.223 billion in Q1 2025, suggesting a focus on quality over quantity. Net loans stood at $1.767 billion, down from $1.812 billion, while total deposits decreased to $1.799 billion from $1.908 billion.

The bank’s net interest margin has shown consistent improvement, reaching 3.75% in Q2 2025, a 19 basis point increase from the previous quarter and a 29 basis point increase year-over-year. This expansion has been a key driver of the bank’s improved profitability.

The following chart illustrates the positive trend in net interest margin:

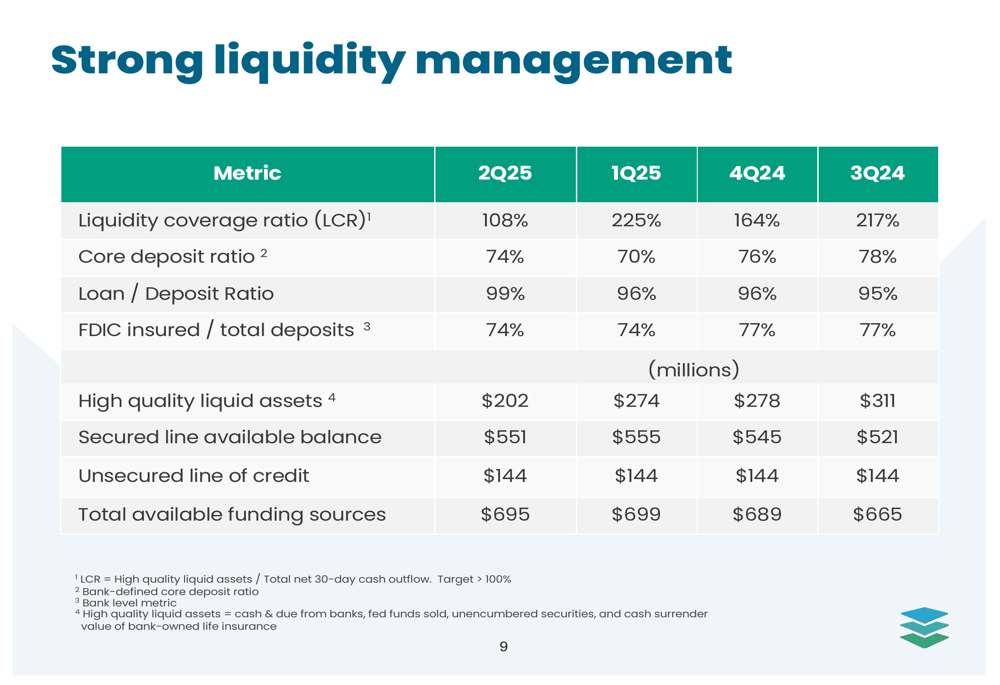

MainStreet has maintained strong liquidity management with a liquidity coverage ratio of 108% in Q2 2025. While this represents a decrease from 225% in Q1 2025, it remains well above regulatory requirements. The bank reported $202 million in high-quality liquid assets and $695 million in total available funding sources.

As demonstrated in the following liquidity management metrics:

The bank has successfully managed its commercial real estate (CRE) concentrations, with investor CRE as a percentage of total capital decreasing to 366% in Q2 2025 from 388% in Q1 2025. This reduction reflects the bank’s prudent risk management approach in a segment that often attracts regulatory scrutiny.

Strategic Initiatives

MainStreet Bancshares has maintained a diversified loan portfolio, with non-owner occupied CRE representing 30%, owner-occupied CRE at 21%, construction at 18%, multi-family at 14%, residential real estate at 11%, and C&I at 6%. This diversification helps mitigate concentration risks and provides stability across economic cycles.

The loan portfolio composition is illustrated in the following chart:

The bank has positioned its loan pricing for a stable or falling rate environment, with 70% of loans having rate resets beyond 6 months and 45% featuring a weighted average floor rate of 6.50%. This strategy should help maintain net interest margin stability if interest rates decline.

A notable achievement in Q2 2025 was the full recovery of $13.2 million on the 2626 Penn property, which had been classified as a nonperforming asset. This successful resolution included collecting the non-accrual balance of $11.2 million, plus $0.7 million in charge-offs and $1.3 million in fees and interest.

The bank’s government contracting relationships continue to be a significant source of deposits, with 29 asset-based lines of credit totaling $13.0 million outstanding and $79.2 million committed. These relationships contributed $75.5 million in average DDA deposits, providing a stable funding source.

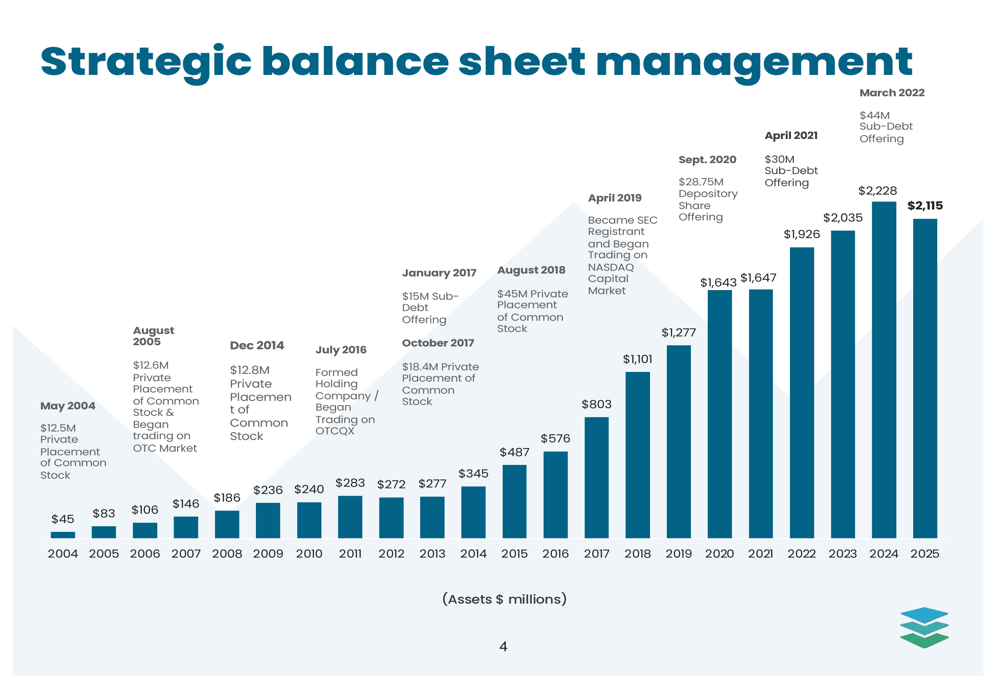

MainStreet’s long-term strategic balance sheet management has driven consistent growth from $45 million in assets in 2004 to $2.115 billion in 2025, as shown in the following chart:

Forward-Looking Statements

Looking ahead, MainStreet Bancshares has announced a stock buyback program with $3.1 million in available capacity, reflecting confidence in its financial position and commitment to enhancing shareholder value.

The bank projects a stable expense run rate for the remainder of 2025, with Q3 estimated at $12.9 million and Q4 at $12.6 million, excluding nonrecurring expenses. This disciplined approach to expense management should support continued profitability improvement.

MainStreet’s earning asset stress tests show good results, with the bank maintaining well-capitalized positions even under stressed scenarios. The stress loss estimate for Q2 2025 was $46.79 million, an increase from $44.18 million in Q1 2025, demonstrating the bank’s thorough risk assessment practices.

The following chart illustrates the bank’s capital position under stress scenarios:

According to the earnings call, MainStreet projects low single-digit loan growth and targets a 1% return on assets by 2026. The bank expects a stable or potentially improving net interest margin, with $152 million in certificates of deposit repricing in the second half of the year.

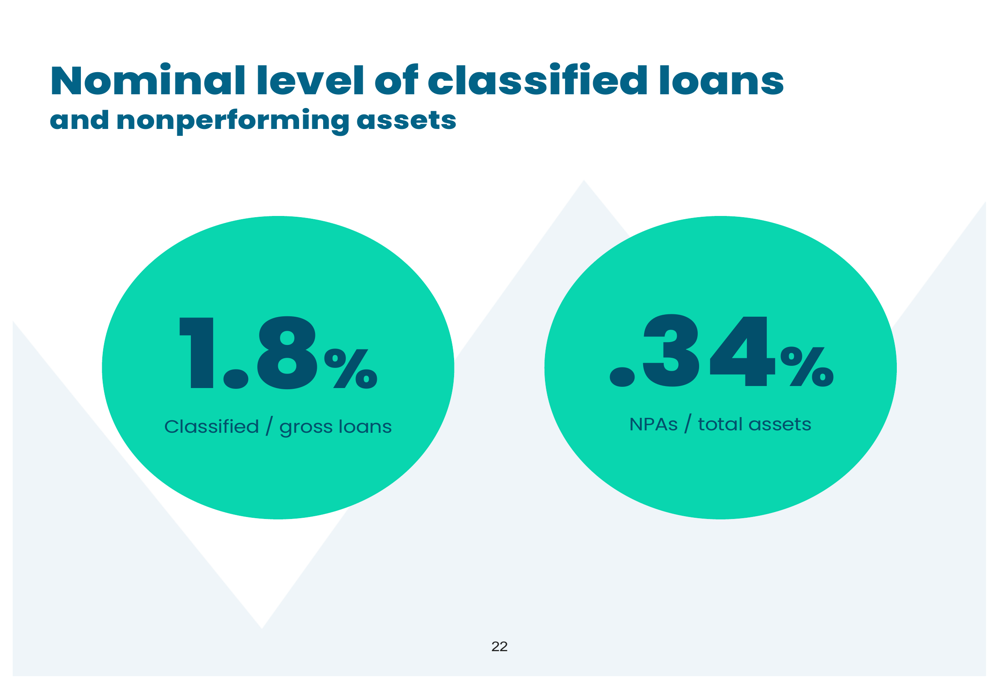

With classified loans at just 1.8% of gross loans and nonperforming assets at 0.34% of total assets, MainStreet Bancshares appears well-positioned to continue its positive performance trajectory in the coming quarters, balancing growth with prudent risk management in its diverse Washington, DC metropolitan market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.