Can anything shut down the Gold rally?

Mandatum Oyj (HEL:MANTA) released its Q2 2025 investor presentation on August 14, 2025, revealing mixed financial results with strong fee growth offset by significant declines in other business segments. The company’s stock closed at €6.02 on August 13, down 1.15% ahead of the presentation.

Quarterly Performance Highlights

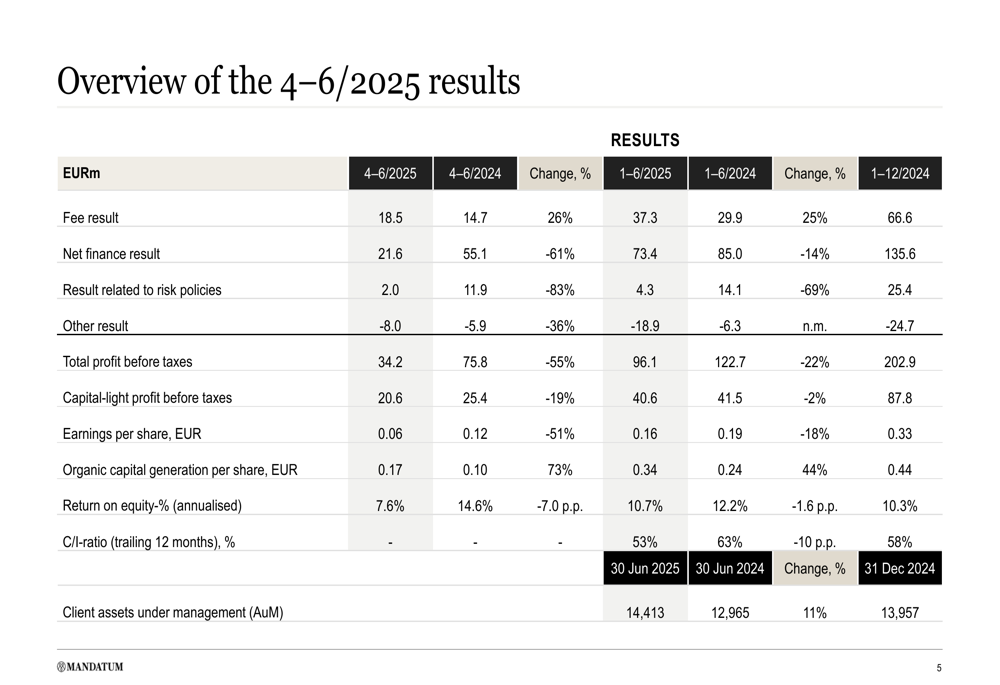

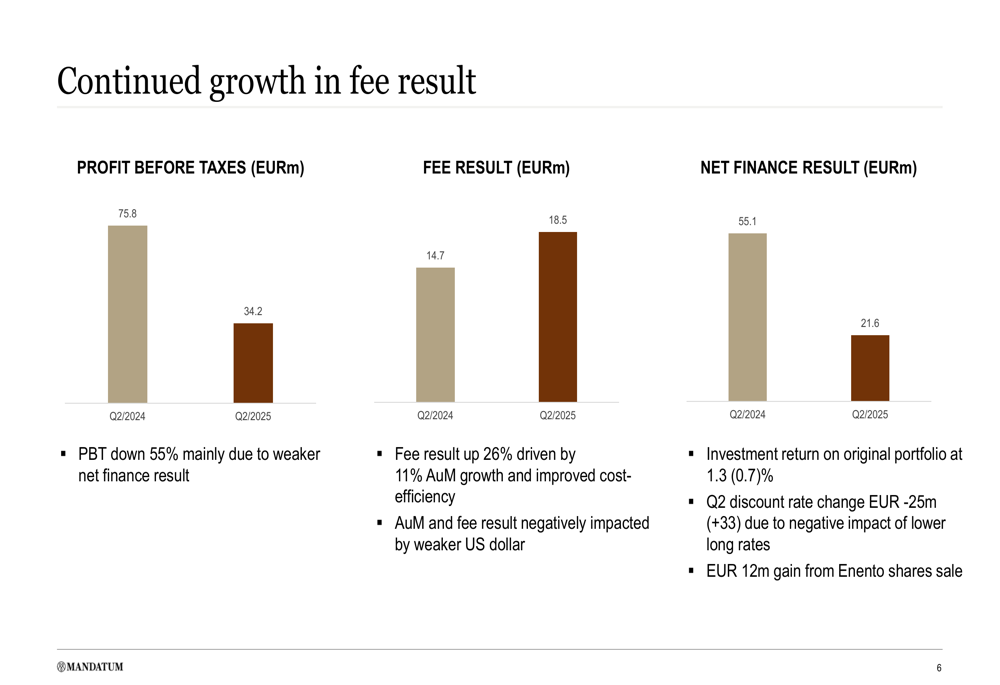

Mandatum reported a 26% year-over-year increase in fee result to €18.5 million for Q2 2025, driven by 11% growth in client assets under management (AuM) to €14.4 billion. However, overall profit before taxes declined significantly by 55% year-over-year to €34.2 million, primarily due to a weaker net finance result.

As shown in the following comprehensive financial overview:

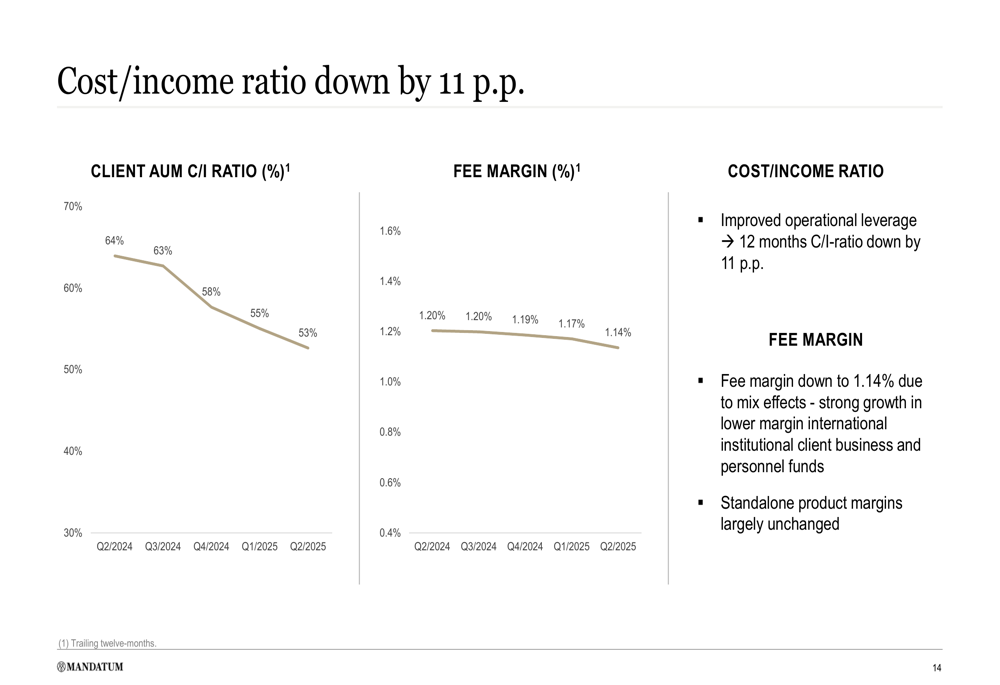

The company’s net finance result fell sharply by 61% to €21.6 million compared to €55.1 million in Q2 2024. Results related to risk policies also declined substantially by 83% to €2.0 million. These declines were partially offset by the strong fee result performance and improved cost efficiency, with the cost-to-income ratio decreasing by 11 percentage points to 53%.

The following chart illustrates the contrasting performance between fee result growth and declining profit before taxes:

Detailed Financial Analysis

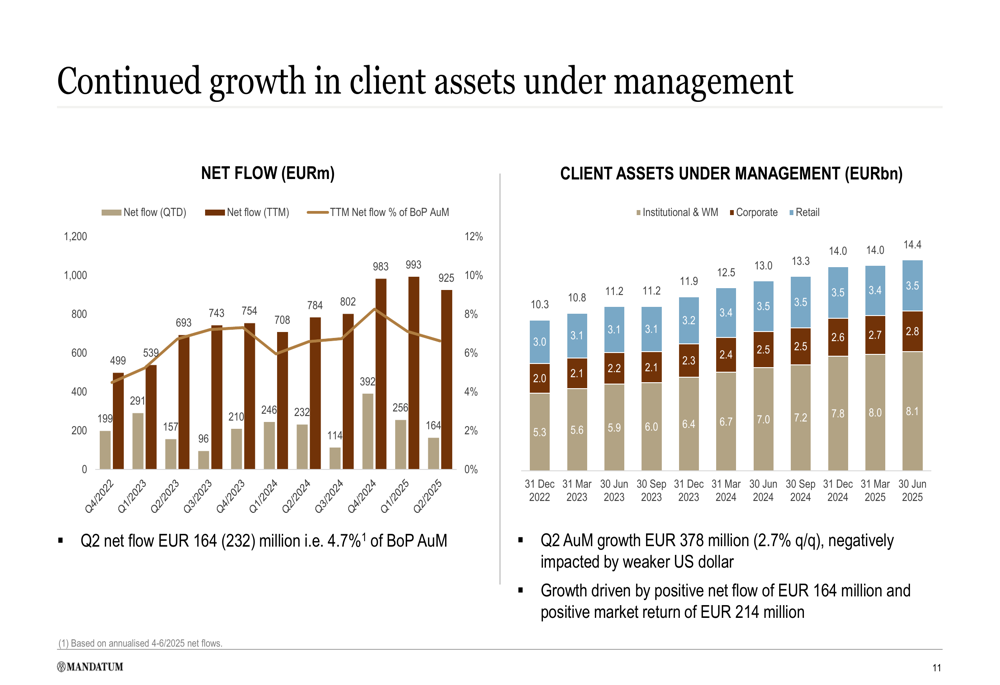

Mandatum’s capital-light business segments showed good underlying growth despite the overall profit decline. The company’s client assets under management continued to grow, with Q2 net flow reaching €164 million, representing 4.7% of beginning-of-period AuM. However, this was down 29% from €232 million in Q2 2024.

The following chart shows the continued growth in client assets under management:

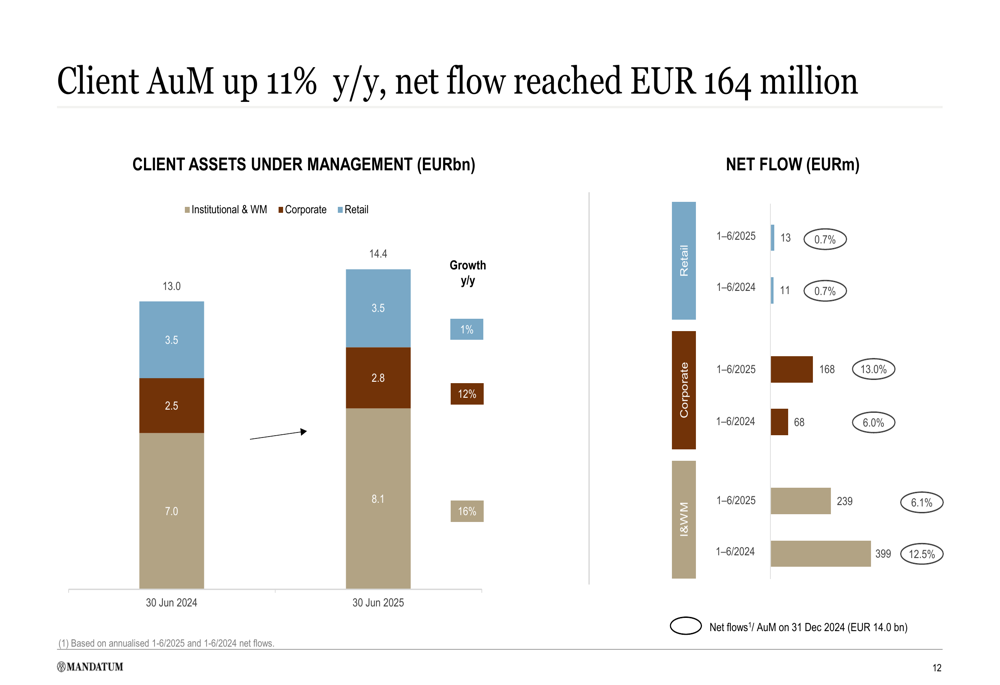

Breaking down the AuM by segment, the Institutional & Wealth Management segment showed the strongest growth, increasing from €7.0 billion to €8.1 billion year-over-year:

A key positive development was the significant improvement in operational efficiency, with the cost-to-income ratio decreasing by 11 percentage points:

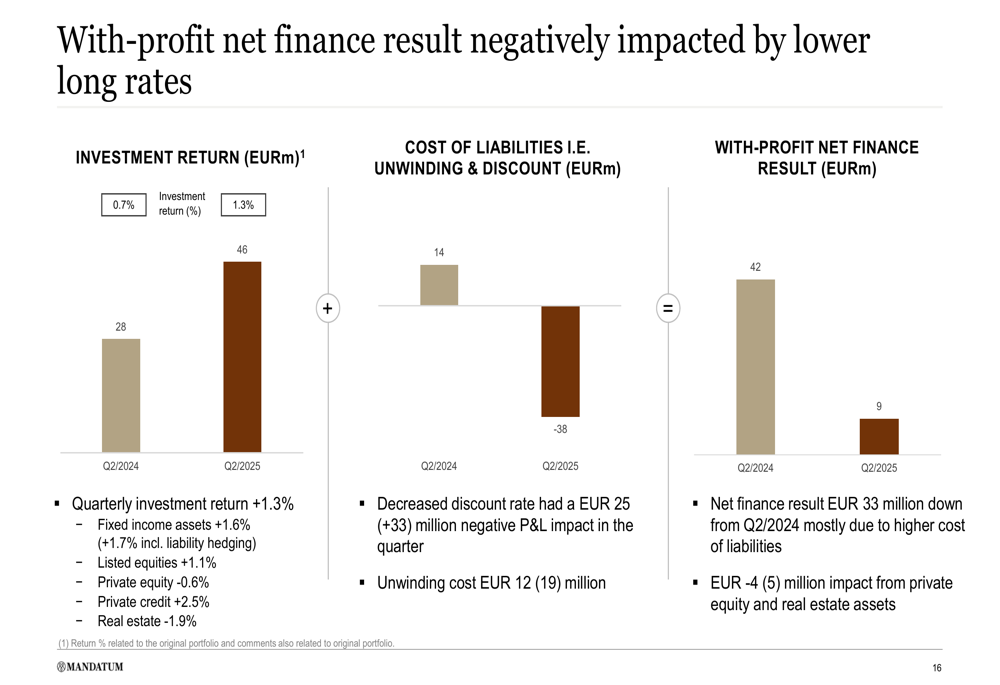

The with-profit segment faced challenges, with its net finance result negatively impacted by lower long-term interest rates. The quarterly investment return was 1.3%, but the decreased discount rate had a €25 million negative P&L impact in the quarter, compared to a positive €33 million impact in Q2 2024.

Strategic Initiatives

Mandatum outlined its vision to become the fastest-growing Nordic asset and wealth manager with optimized growth in Finnish life and pension businesses. The company’s strategic priorities for 2025-2028 include:

1. Expanding its Nordic foothold in asset management

2. Accelerating the growth of Finnish wealth management

3. Leveraging its leading corporate market position

4. Focusing on operational efficiency

Financial targets for this period include:

- Return on equity above 20%

- Capital-light profit before taxes growth (CAGR) above 10%

- Solvency margin of 160-180% with cumulative shareholder payouts exceeding €1 billion

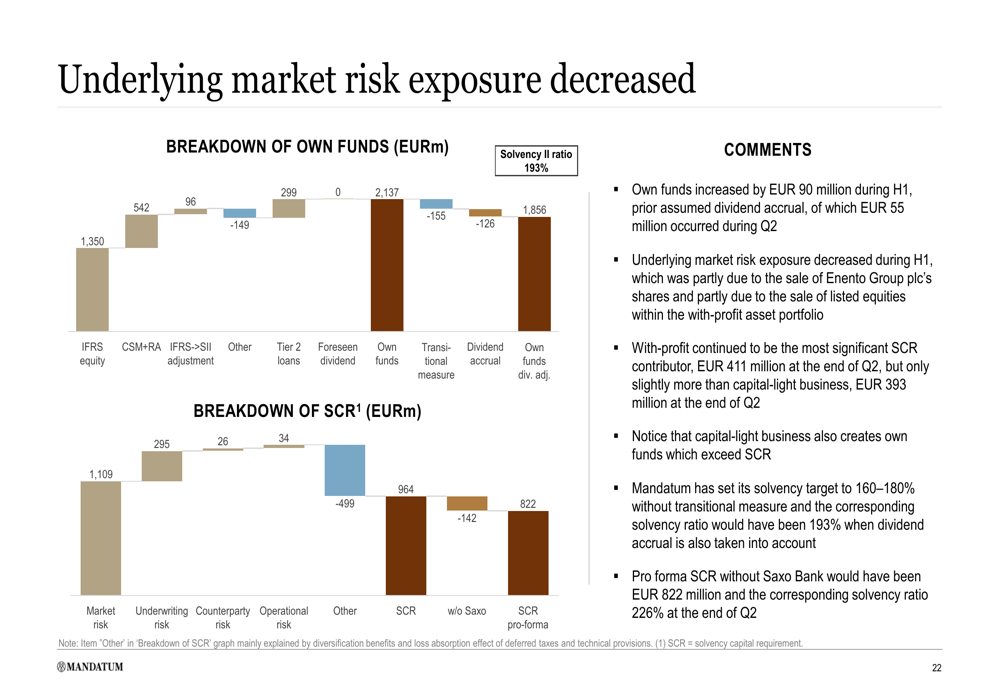

The company’s solvency position remained strong at 193%, with underlying market risk exposure decreasing during the first half of 2025:

Forward-Looking Statements

Mandatum maintained its outlook for 2025, expecting the fee result to increase from 2024 levels. However, the company noted that the with-profit portfolio is expected to continue decreasing, which could create relatively high volatility in the net finance result due to changes in the market environment.

The company’s Q2 results show a significant shift from Q1 2025, when it reported a profit before taxes of €62 million and a net finance result that surged 73% to €51.8 million. The Solvency II ratio has also decreased from 207% in Q1 to 193% in Q2.

Mandatum is continuing its sustainability initiatives, announcing new interim climate targets in pursuit of net zero emissions, including reducing the carbon intensity of direct listed equities and corporate bonds by 75% by 2030 compared to the 2020 baseline.

Overall, while Mandatum’s fee-based business continues to show strong growth momentum, the significant decline in net finance result and profit before taxes highlights the challenges the company faces in the current interest rate environment. The company’s strategic focus on expanding its capital-light business segments and improving operational efficiency appears well-positioned to navigate these challenges over the medium term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.