Street Calls of the Week

Introduction & Market Context

Manulife Financial Corporation (NYSE:MFC) presented its first quarter 2025 financial results on May 8, 2025, highlighting strong top-line growth across its business segments, particularly in Asia, while also revealing the impact of recent reinsurance transactions on its bottom line. The company maintained its focus on portfolio transformation to reduce risk and enhance long-term returns.

The presentation comes after Manulife reported strong growth in the previous quarter (Q3 2024), where it saw significant increases in APE sales and core earnings, particularly in its Asian markets. The company’s stock closed at $31.37 on May 7, 2025, near its 52-week high of $33.07, indicating positive market sentiment ahead of the earnings release.

Quarterly Performance Highlights

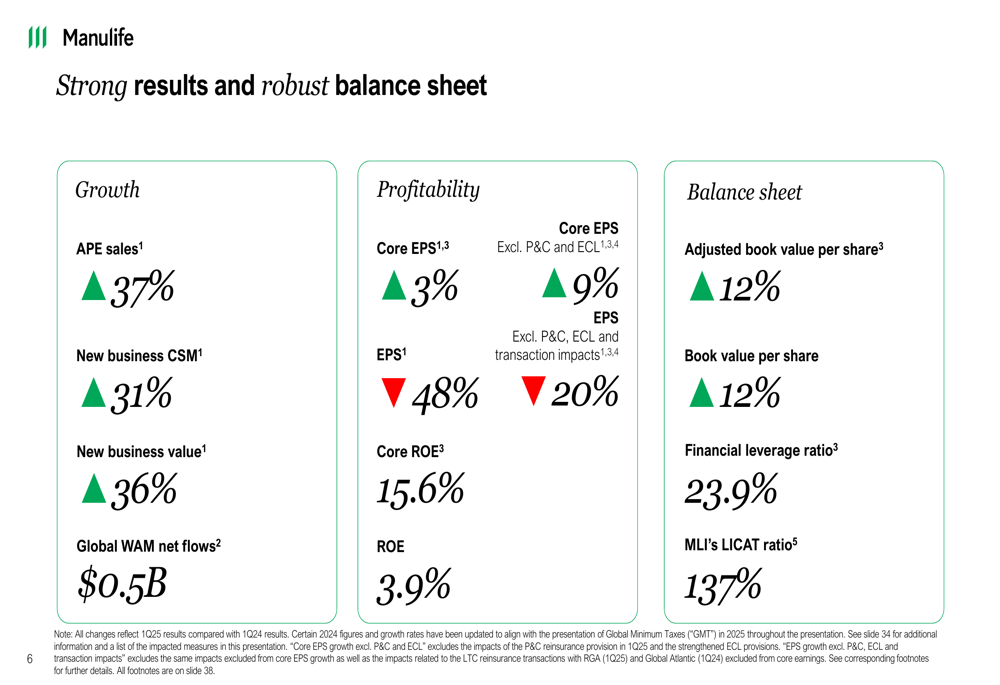

Manulife reported strong top-line growth in Q1 2025, with annualized premium equivalent (APE) sales up 37%, new business contractual service margin (CSM) up 31%, and new business value up 36% compared to the same period last year. However, bottom-line results were mixed, with core earnings per share (EPS) increasing by 3% while reported EPS declined by 48%.

As shown in the following comprehensive overview of key metrics:

The significant gap between core and reported earnings was primarily due to a $732 million realized loss on debt instruments related to the RGA U.S. Reinsurance Transaction (JO:NTUJ). While this transaction negatively impacted short-term earnings, management emphasized that the offsetting change in other comprehensive income (OCI) neutralized the book value impact.

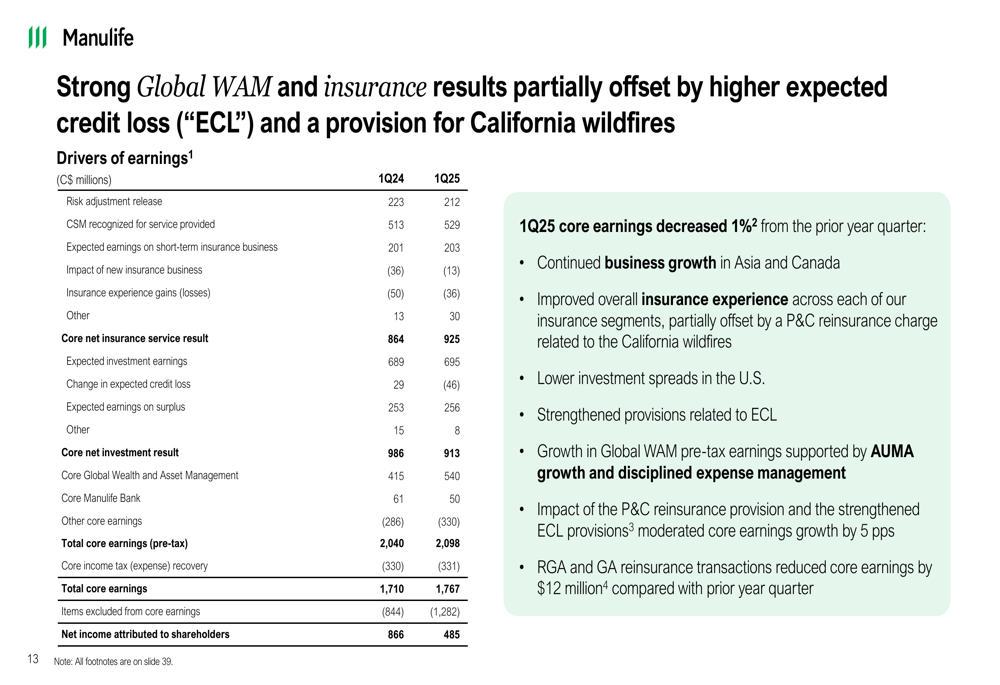

Core return on equity (ROE) remained strong at 15.6%, though slightly down from 16.2% in Q1 2024, while reported ROE fell to 3.9%. The company’s core earnings increased by 1% year-over-year to $1,767 million, with growth in Global Wealth and Asset Management (WAM) and insurance segments partially offset by higher expected credit losses (ECL) and a provision for California wildfires.

The following breakdown illustrates the drivers behind Manulife’s earnings performance:

Regional Performance Analysis

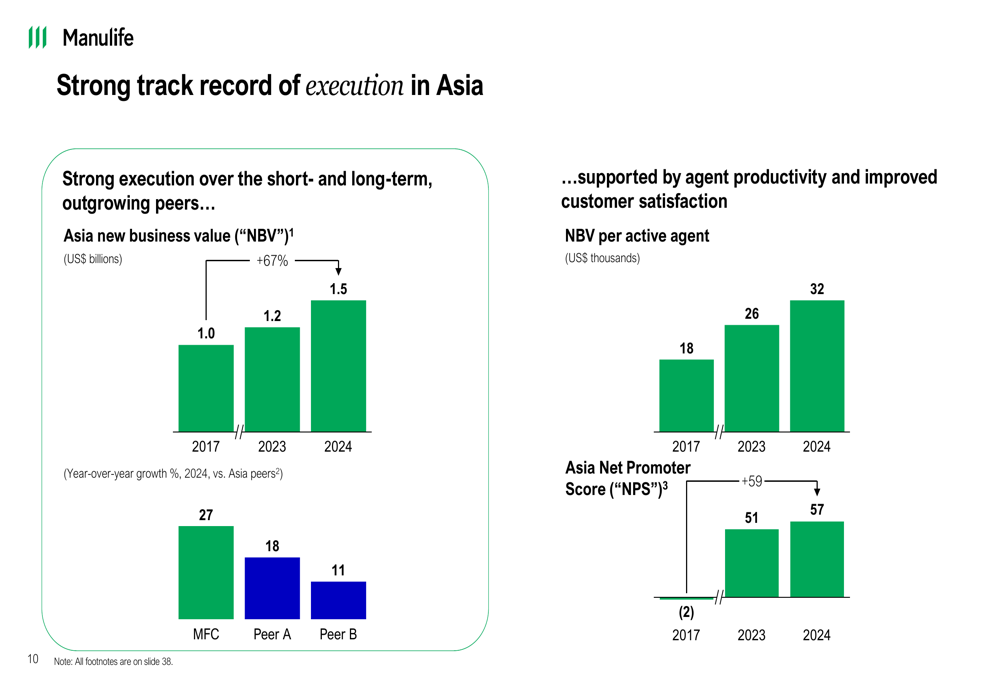

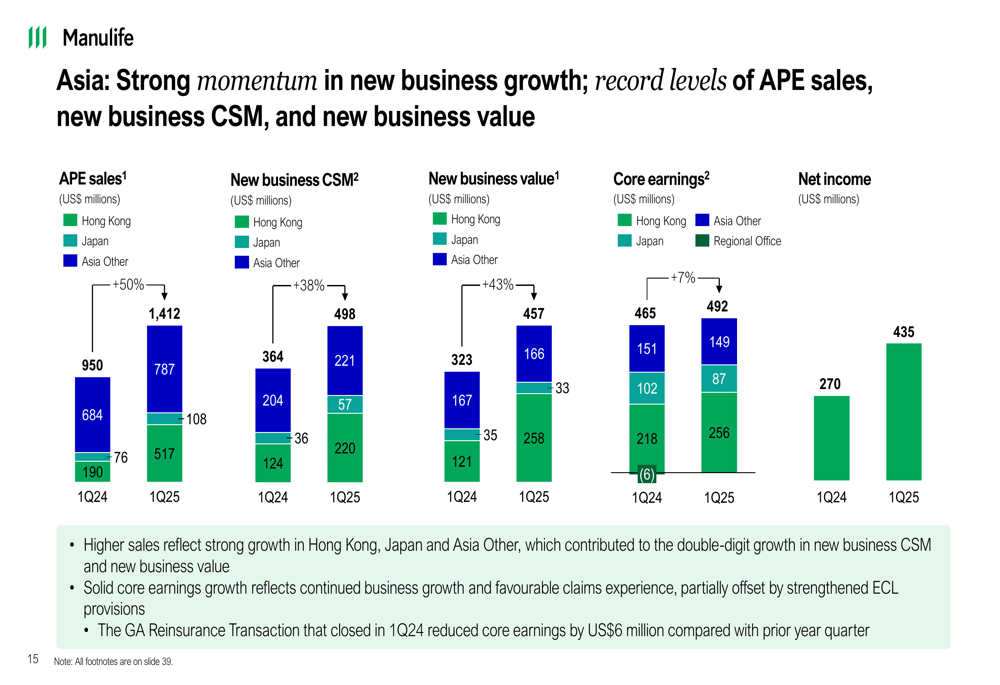

Asia continued to be a growth engine for Manulife, with record levels of APE sales, new business CSM, and new business value. The region’s performance has shown consistent improvement over the years, with new business value increasing from $1.0 billion in 2017 to $1.5 billion in 2024, representing a 67% increase.

The following chart demonstrates Manulife’s strong track record in Asia:

In Q1 2025, Asia’s performance was particularly impressive, with detailed metrics by market showing strong momentum:

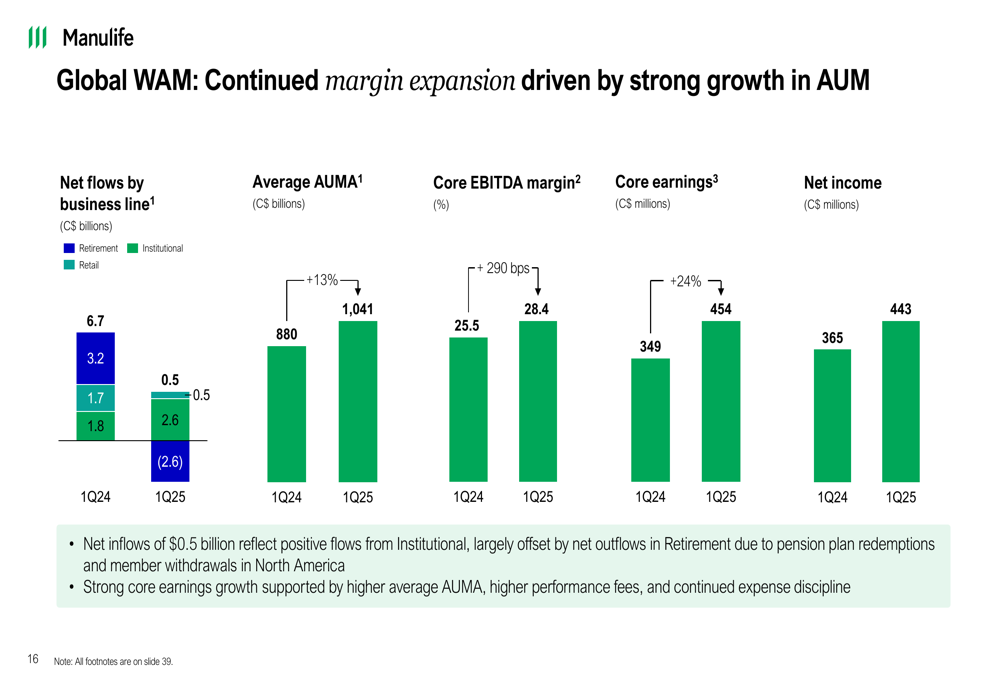

The Global WAM segment also delivered strong results, with core earnings increasing from $349 million in Q1 2024 to $454 million in Q1 2025. This growth was supported by higher average assets under management and administration (AUMA), which increased by 13% to $1,041 billion, and improved core EBITDA margin, which expanded from 25.5% to 28.4%.

As illustrated in the following chart of Global WAM performance:

The U.S. segment faced challenges, with core earnings impacted by lower investment spreads and higher expected credit losses. Despite solid new business results, net income for the U.S. segment declined significantly, reflecting the impact of the reinsurance transaction.

Balance Sheet and Capital Management

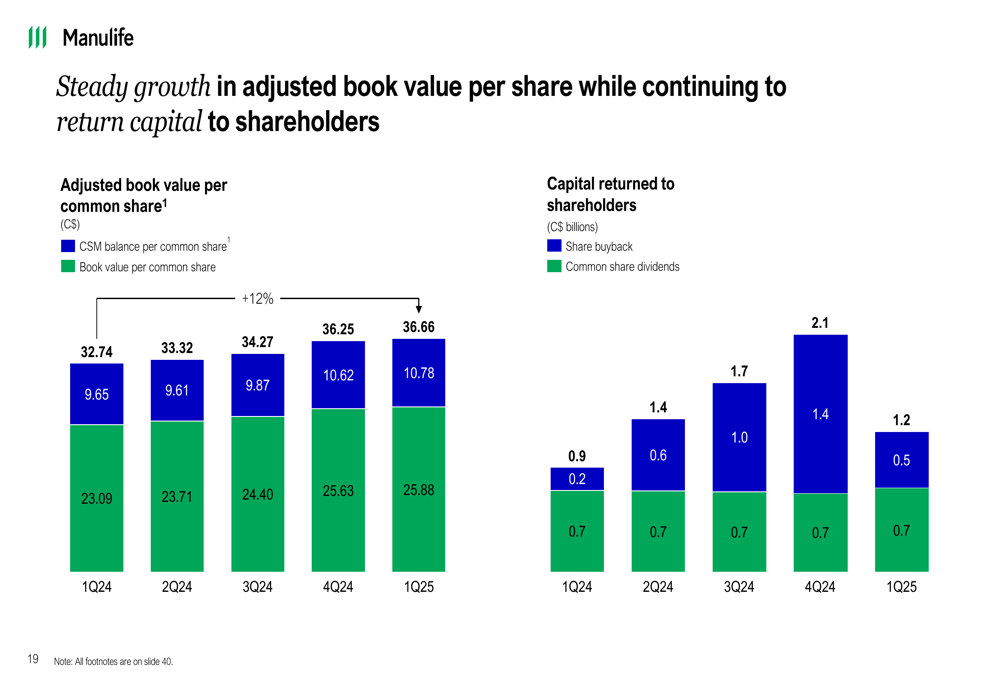

Manulife maintained a strong balance sheet in Q1 2025, with adjusted book value per share increasing by 12% year-over-year to $36.66. The company continued to return capital to shareholders through dividends and share buybacks, as shown in the following chart:

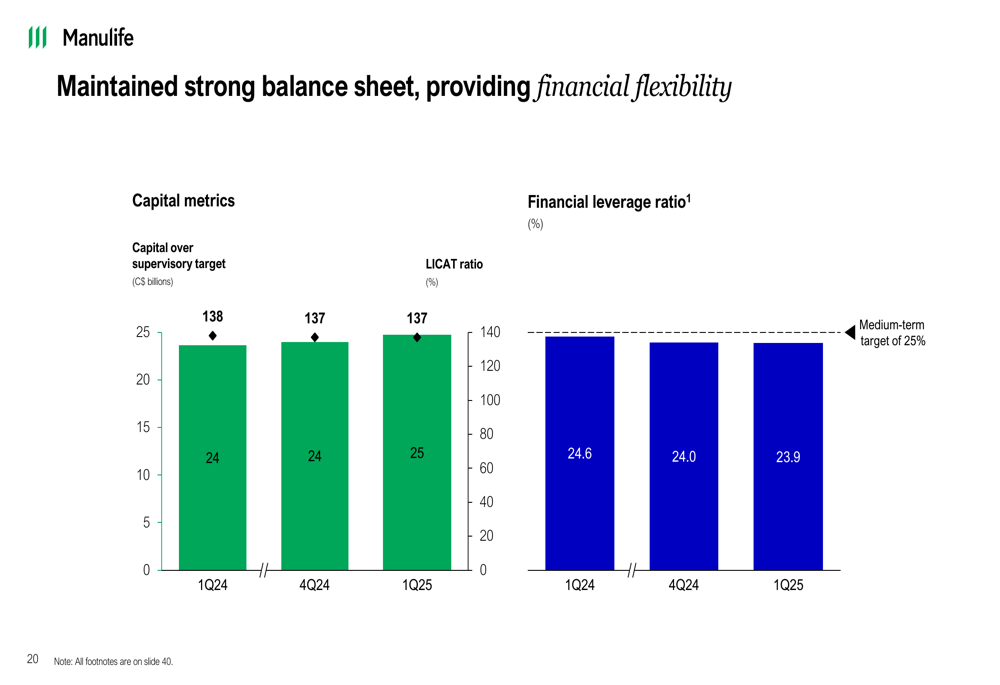

The company’s financial leverage ratio improved to 23.9%, below its medium-term target of 25%, while MLI’s LICAT ratio remained strong at 137%. These metrics provide Manulife with financial flexibility for future growth and capital deployment.

As demonstrated in the following capital metrics chart:

Strategic Initiatives and Outlook

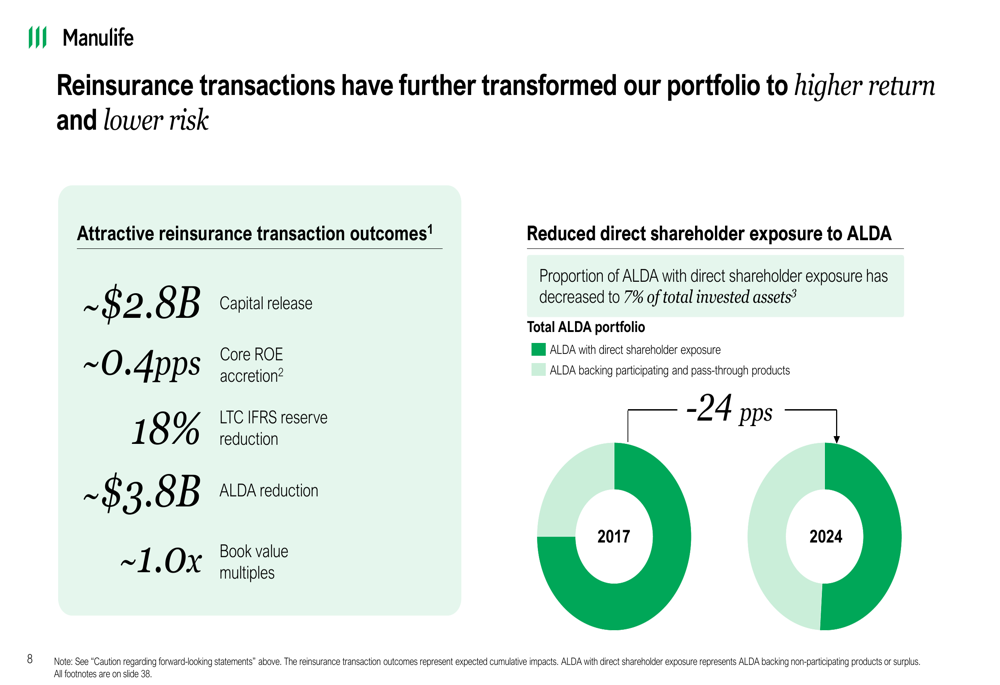

A key strategic focus for Manulife has been transforming its portfolio through reinsurance transactions to reduce risk and enhance returns. These transactions have resulted in approximately $2.8 billion in capital release, 0.4 percentage points of Core ROE accretion, and an 18% reduction in long-term care IFRS reserves.

The company has also significantly reduced its exposure to alternative long-duration assets (ALDA) with direct shareholder exposure, which has decreased to 7% of total invested assets, as illustrated in the following chart:

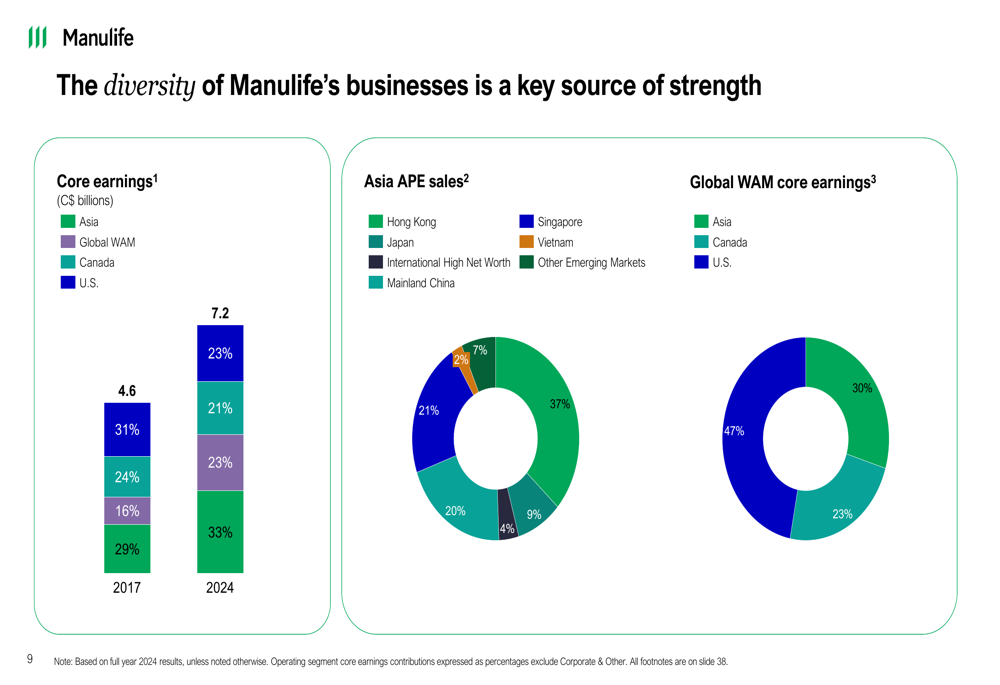

Manulife emphasized the diversity of its business as a key strength, with a balanced distribution of core earnings across Asia, Global WAM, Canada, and the U.S. This diversification provides resilience against regional economic fluctuations and market volatility.

The following pie charts illustrate the evolution of Manulife’s business mix:

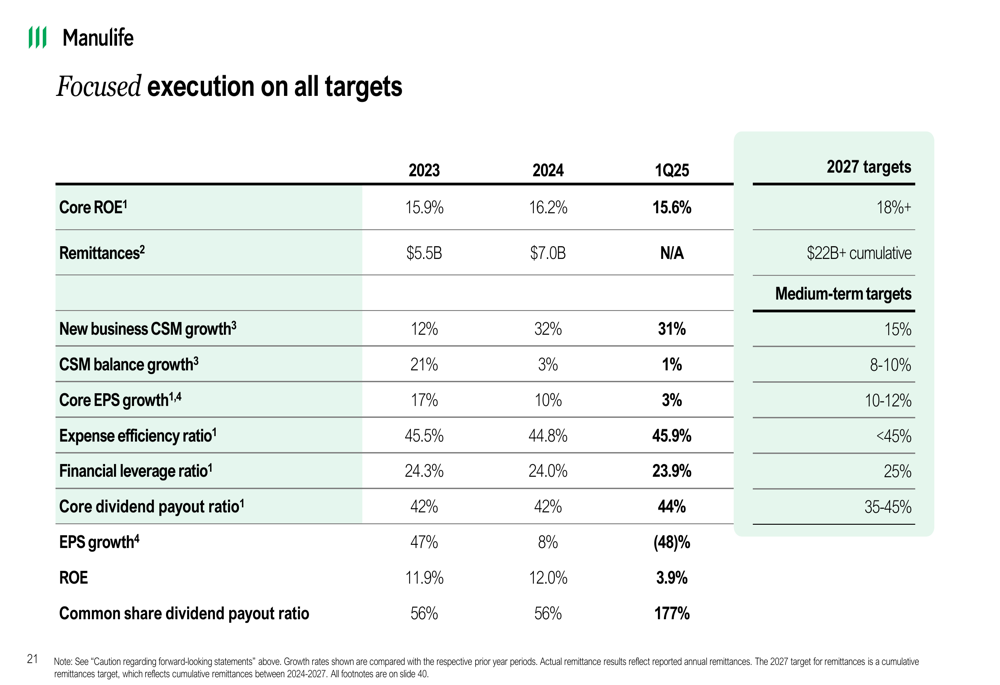

Looking ahead, Manulife remains focused on executing its strategic priorities, with targets for 2027 including core ROE of 18%+ and cumulative remittances of $22 billion+. The company is tracking well against most of its medium-term targets, including new business CSM growth, expense efficiency, and financial leverage.

As shown in the following performance scorecard:

In conclusion, Manulife’s Q1 2025 results demonstrate strong top-line momentum across its businesses, particularly in Asia and Global WAM, while the bottom line was impacted by reinsurance transactions and specific provisions. The company’s strategic transformation continues to reduce risk and position it for sustainable long-term growth, supported by a strong balance sheet and disciplined capital management.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.