106%+ returns, 97% win rate: A fresh list of AI-picked stock is out NOW

Introduction & Market Context

Marathon Petroleum Corporation (NYSE:MPC) presented its first quarter 2025 earnings results on May 6, revealing a mixed performance across its business segments. The company reported a net loss despite strong performance in its midstream operations, while maintaining substantial capital returns to shareholders.

The oil refiner continues to navigate a challenging energy landscape characterized by volatile refining margins and regulatory uncertainty in renewable fuels, while leveraging its integrated value chain and geographically diversified assets to maintain operational resilience.

Quarterly Performance Highlights

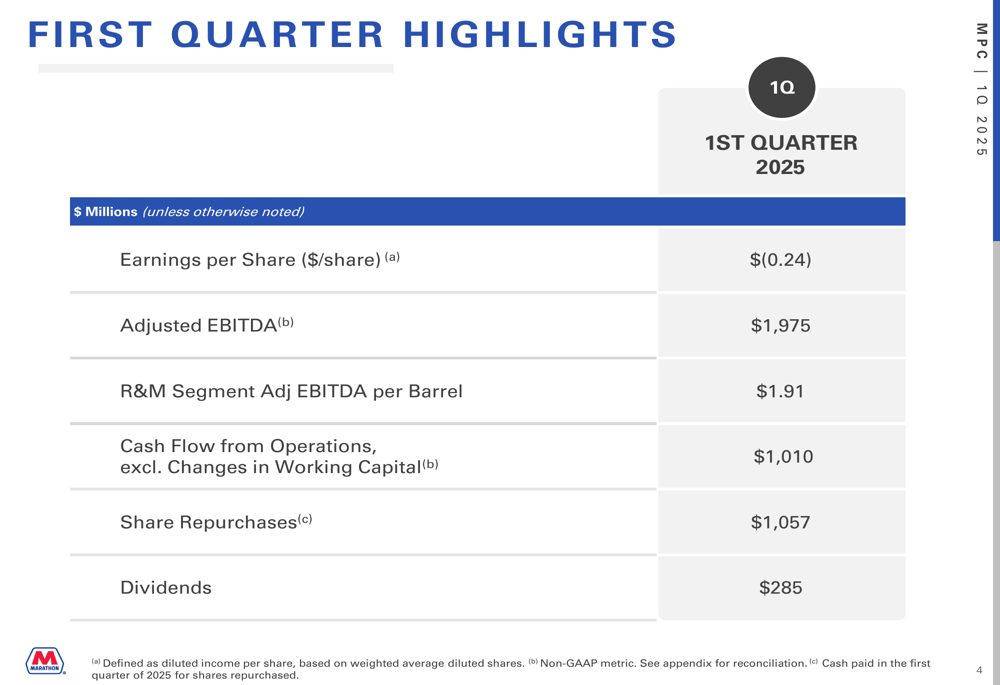

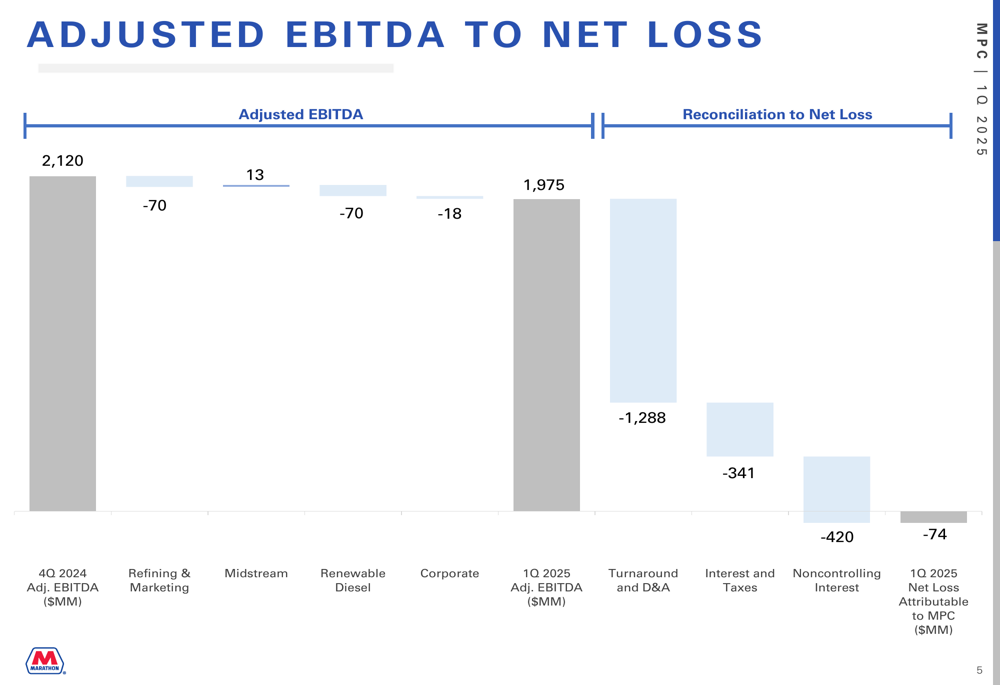

Marathon Petroleum reported a net loss attributable to MPC of $74 million for Q1 2025, translating to earnings per share of $(0.24). Despite the bottom-line loss, the company generated adjusted EBITDA of $1.975 billion, primarily supported by the strength of its midstream business.

As shown in the following financial highlights, the company maintained strong capital returns to shareholders despite the challenging quarter:

Cash flow from operations, excluding changes in working capital, reached $1.01 billion. The company returned $1.3 billion to shareholders during the quarter, including $1.057 billion in share repurchases and $285 million in dividends, demonstrating its commitment to shareholder returns even during a challenging period.

The following chart illustrates the bridge from adjusted EBITDA to net loss, highlighting the impact of depreciation, amortization, and turnaround costs:

Segment Analysis

Marathon’s performance varied significantly across its three main business segments, with midstream operations outperforming while refining and renewable diesel faced headwinds.

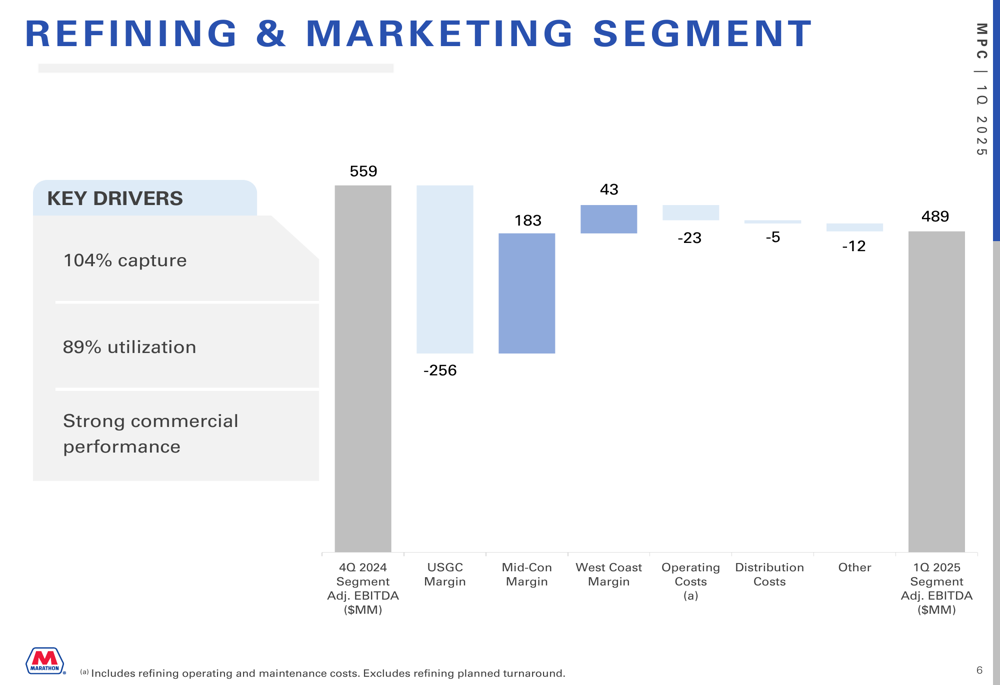

The Refining & Marketing segment generated adjusted EBITDA of $489 million in Q1 2025, down from $559 million in Q4 2024. The segment achieved a 104% capture rate despite operating at 89% utilization. Regional performance was mixed, with Mid-Con and West Coast margins improving while Gulf Coast margins declined significantly.

As illustrated in the following segment performance breakdown:

The company’s R&M margin indicator was $3.284 billion with a 100% capture rate, but actual R&M margin reached $3.43 billion, representing a 104% capture. This outperformance was driven by seasonally strong clean product margins and maximized margins on specialty products.

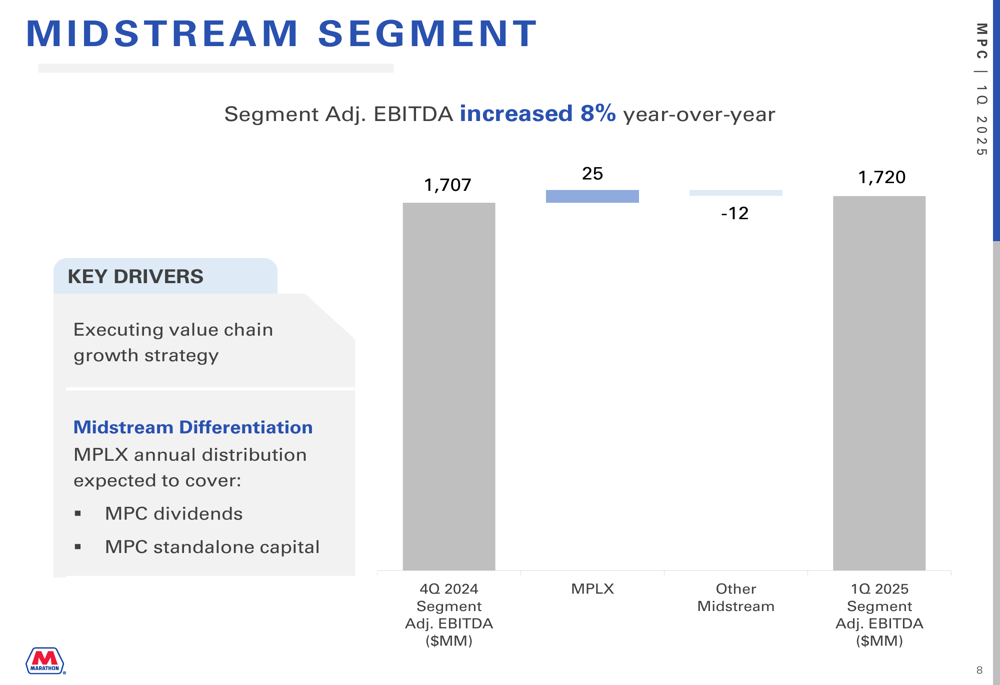

The Midstream segment continued to be the company’s strongest performer, with adjusted EBITDA increasing 8% year-over-year to $1.72 billion. This segment’s performance was bolstered by the execution of Marathon’s value chain growth strategy, including an agreement to acquire 100% ownership in BANGL and a final investment decision on the Traverse natural gas pipeline.

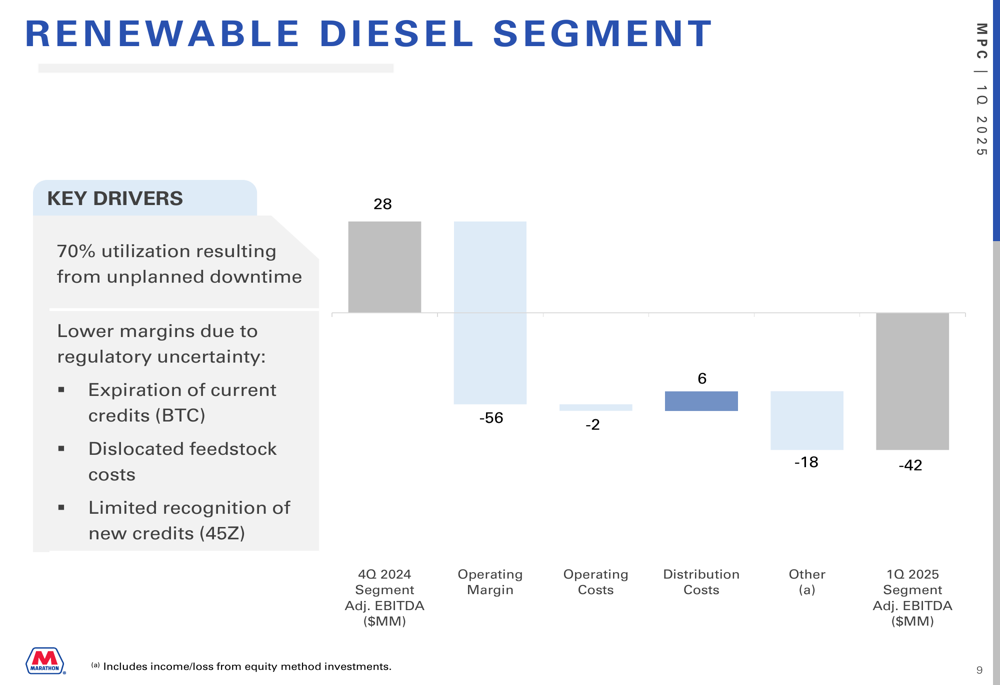

In contrast, the Renewable Diesel segment reported negative adjusted EBITDA of $42 million, deteriorating from positive $28 million in Q4 2024. This decline was attributed to unplanned downtime resulting in 70% utilization, as well as lower margins due to regulatory uncertainty, including the expiration of current credits (BTC), dislocated feedstock costs, and limited recognition of new credits (45Z).

Capital Allocation & Balance Sheet

Marathon maintained a strong balance sheet with $3.812 billion in cash and cash equivalents as of March 31, 2025. The company’s consolidated gross debt-to-capital ratio stood at 57%. During the quarter, Marathon issued $2.0 billion in aggregate principal amount of unsecured senior notes.

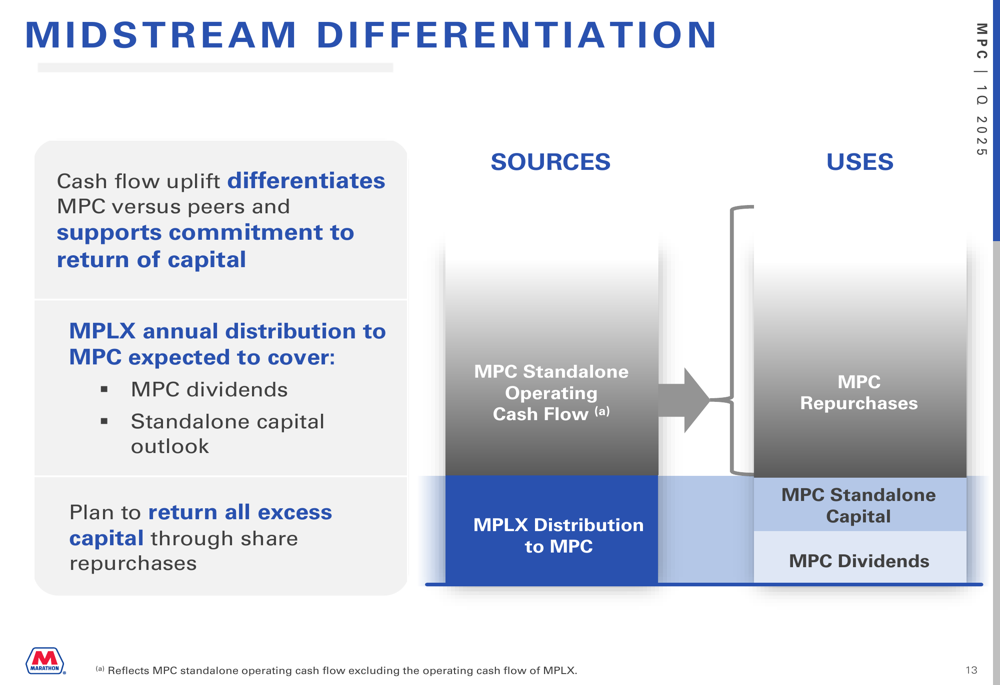

The company’s midstream business, primarily through MPLX (NYSE:MPLX), continues to be a significant source of cash flow. Management highlighted that MPLX’s annual distribution to MPC is expected to cover MPC dividends and standalone capital requirements, creating a differentiated cash flow profile compared to peers.

Sustainability Initiatives

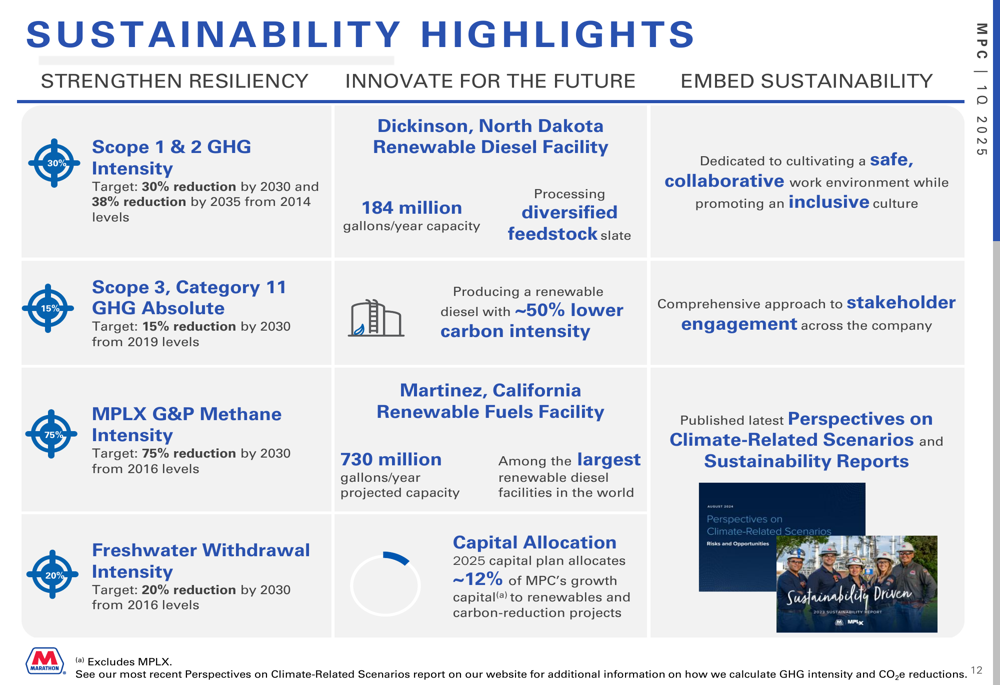

Marathon continues to advance its sustainability strategy across three key areas: strengthening resiliency, innovating for the future, and embedding sustainability throughout the organization. The company has established specific targets including a 30% reduction in Scope 1 & 2 GHG intensity by 2030 and a 15% reduction in Scope 3 Category 11 GHG absolute emissions by 2030.

The company’s renewable fuels facilities include the Dickinson Renewable Diesel Facility with 184 million gallons per year capacity and the Martinez Renewable Fuels Facility with 730 million gallons per year capacity. Approximately 12% of MPC’s growth capital is allocated to renewable and carbon reduction projects.

Forward Outlook & Guidance

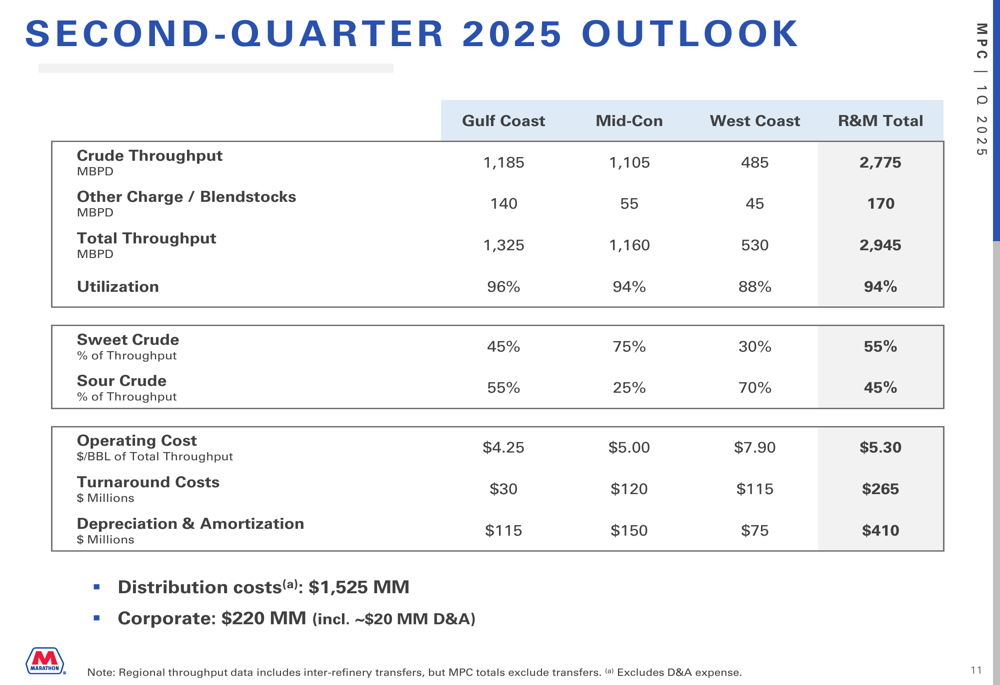

Looking ahead to Q2 2025, Marathon projects improved operational performance with total crude throughput of 2,775 thousand barrels per day (MBPD) and total throughput of 2,945 MBPD, representing a utilization rate of 94% – a significant improvement from Q1’s 89% utilization.

The company expects operating costs of $5.30 per barrel of total throughput, with turnaround costs projected at $265 million and depreciation & amortization at $410 million for the second quarter.

Marathon’s management emphasized its commitment to creating exceptional value in 2025 by prioritizing peer-leading status in safety & reliability, operational excellence, commercial performance, and profitability per barrel. The company’s strategic focus remains on optimizing its portfolio, leveraging value chain advantages, ensuring competitive assets, and investing in talent.

Despite the challenges faced in Q1 2025, Marathon’s integrated value chain and geographically-diversified assets position the company to navigate through market cycles, with management expressing confidence in delivering peer-leading execution and shareholder returns throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.