Gold rally takes a breather amid Gaza ceasefire, Fed minutes

Martin Marietta Materials Inc (NYSE:MLM) reported record first-quarter results on April 30, 2025, showcasing strong performance in its aggregates business despite weather challenges early in the quarter. The company maintained its positive full-year guidance, highlighting infrastructure spending and data center construction as key growth drivers offsetting weakness in residential markets.

Quarterly Performance Highlights

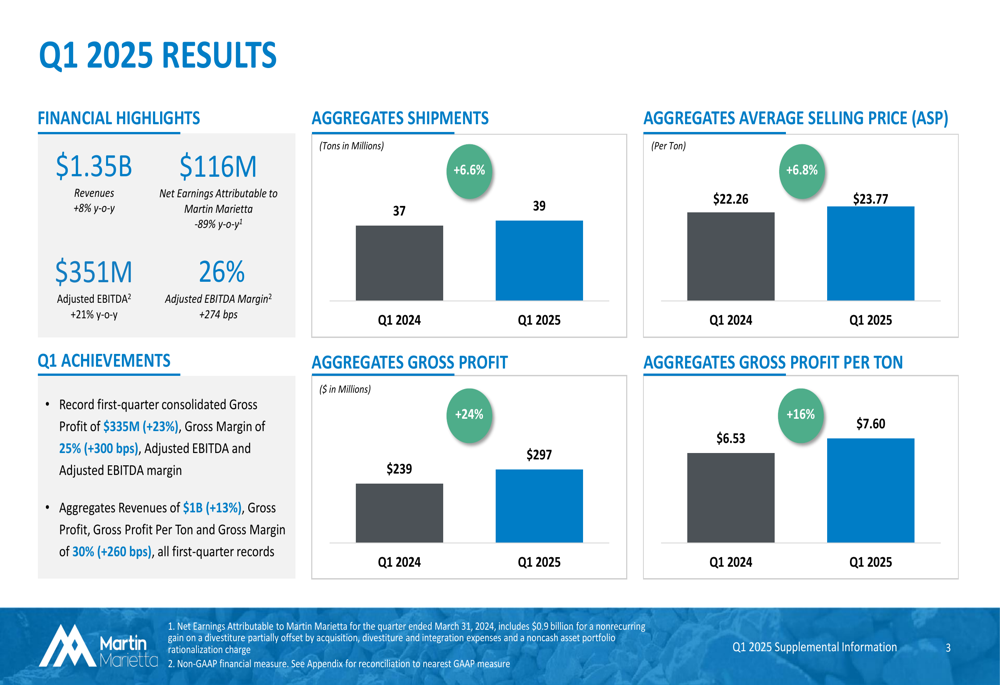

Martin Marietta delivered consolidated revenues of $1.35 billion in Q1 2025, representing an 8% increase year-over-year. While net earnings attributable to Martin Marietta fell to $116 million from $1.05 billion in the prior year, the company noted that Q1 2024 included a significant nonrecurring gain. Adjusted EBITDA, which excludes one-time items, increased 21% to $351 million, with the adjusted EBITDA margin expanding 274 basis points to 26%.

The company achieved record first-quarter results across multiple metrics, including consolidated gross profit of $335 million (up 23%) and gross margin of 25% (up 300 basis points).

As shown in the following financial and operational highlights:

The aggregates business, Martin Marietta’s largest segment, delivered particularly strong results with revenues reaching $1 billion, a 13% increase year-over-year. Aggregates shipments rose 6.6% to 39 million tons, while average selling price increased 6.8% to $23.77 per ton. These improvements drove a 24% increase in aggregates gross profit to $297 million and a 16% rise in gross profit per ton to $7.60.

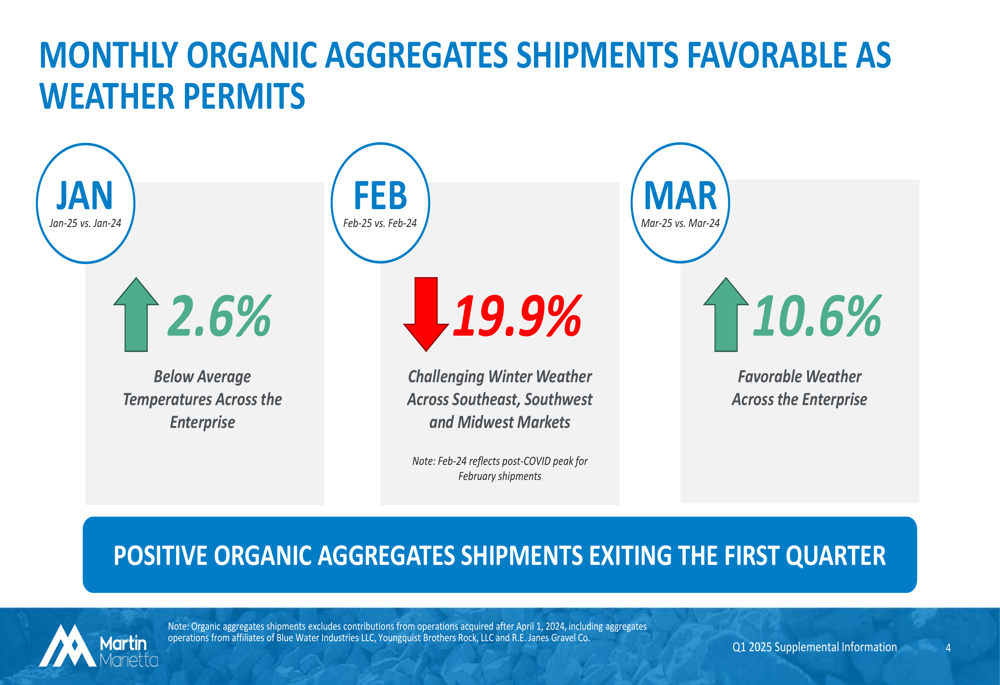

However, the quarterly performance was not without challenges, as weather conditions significantly impacted monthly shipment volumes. The company experienced below-average temperatures across its operations in January, followed by challenging winter weather across Southeast, Southwest, and Midwest markets in February, before conditions improved in March.

The following chart illustrates the monthly organic aggregates shipment trends:

"Despite weather challenges early in the quarter, we delivered record first-quarter results across multiple metrics, demonstrating the resilience of our business model and the effectiveness of our pricing strategy," the company stated in its presentation.

End Market Outlook

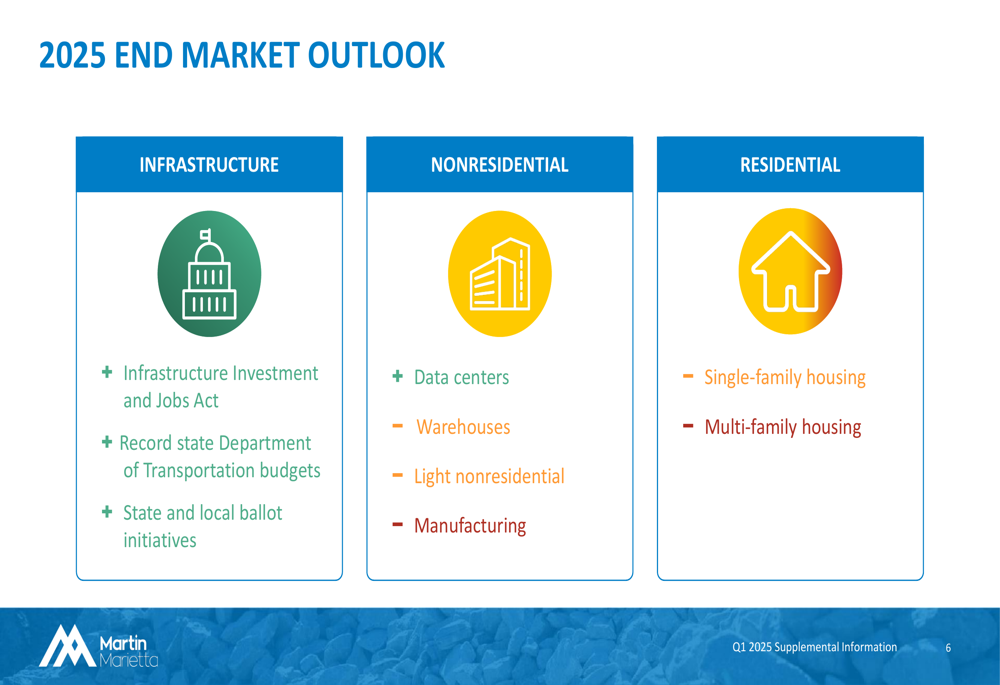

Martin Marietta provided a mixed outlook for its end markets in 2025, with infrastructure spending and certain nonresidential segments expected to drive growth, while residential construction remains challenged.

The infrastructure market outlook is positive, supported by funding from the Infrastructure Investment and Jobs Act (IIJA), record state Department of Transportation budgets, and state and local ballot initiatives. In the nonresidential sector, data centers, warehouses, and light nonresidential construction are expected to perform well, though manufacturing construction is projected to decline. The residential market outlook remains negative for both single-family and multi-family housing, reflecting the impact of higher interest rates.

The company’s end market outlook is illustrated below:

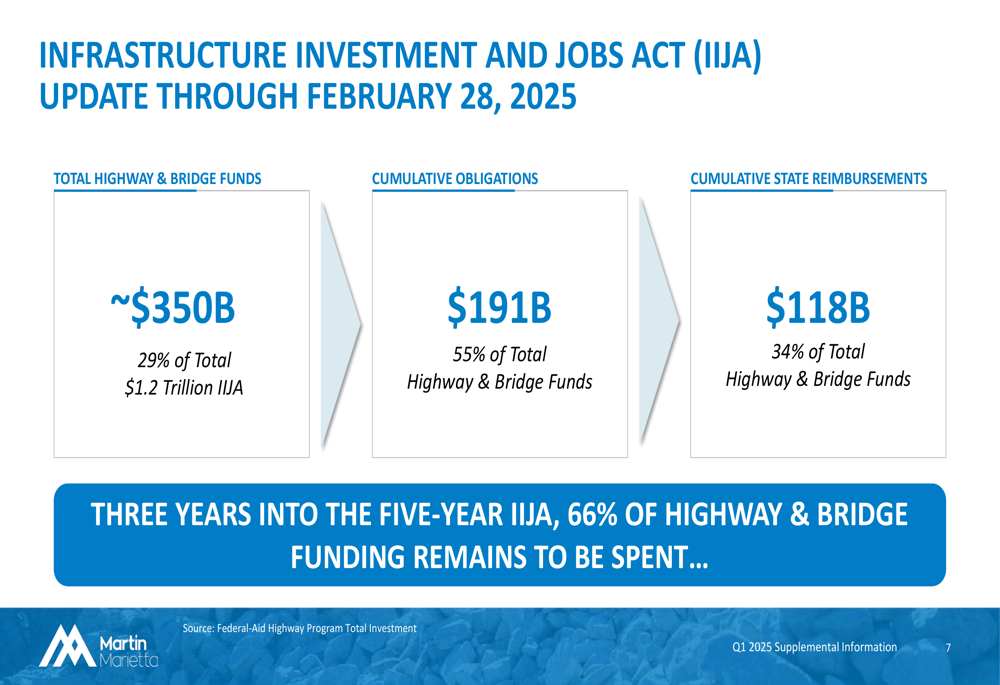

A key growth driver for Martin Marietta is the ongoing implementation of the Infrastructure Investment and Jobs Act (IIJA). As of February 28, 2025, approximately $191 billion (55%) of the total $350 billion in highway and bridge funds had been obligated, with $118 billion (34%) reimbursed to states. This indicates significant remaining spending potential over the coming years.

The following chart shows the IIJA funding status:

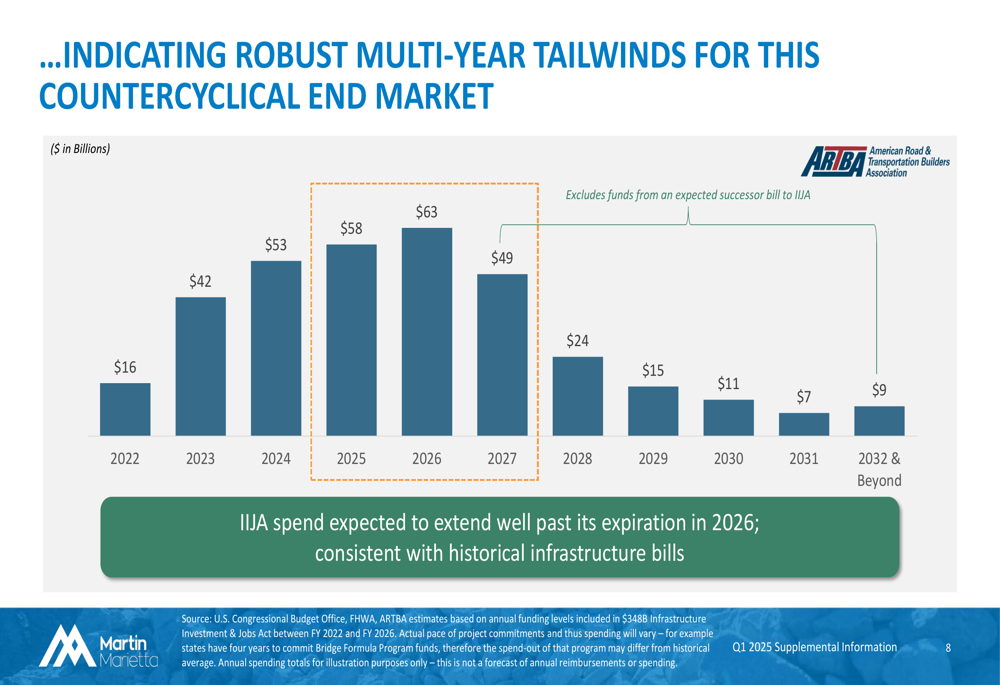

Martin Marietta expects IIJA spending to extend well beyond the program’s official expiration in 2026, providing multi-year tailwinds for the company’s aggregates business. The spending is projected to peak in 2026 at approximately $63 billion before gradually declining in subsequent years.

The long-term infrastructure spending outlook is illustrated below:

Forward-Looking Statements

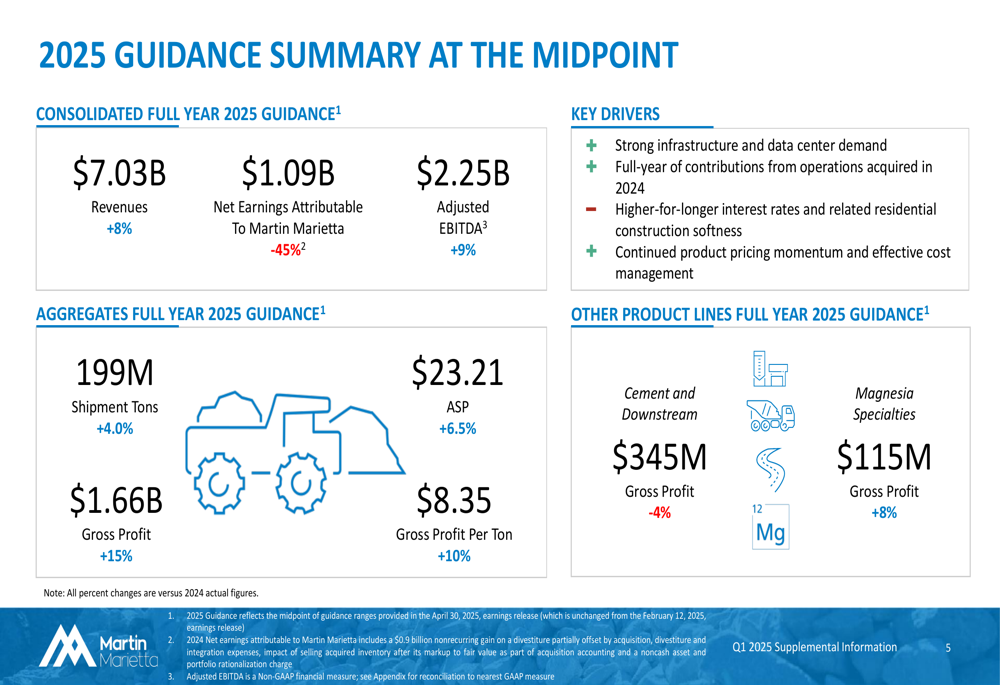

Martin Marietta maintained its full-year 2025 guidance, projecting consolidated revenues of $7.03 billion (up 8% year-over-year) and adjusted EBITDA of $2.25 billion (up 9%). Net earnings attributable to Martin Marietta are expected to reach $1.09 billion, down 45% from 2024, which included a $0.9 billion nonrecurring gain.

For its aggregates business, the company forecasts shipments of 199 million tons (up 4.0%), average selling price of $23.21 per ton (up 6.5%), and gross profit of $1.66 billion (up 15%). Gross profit per ton is expected to increase 10% to $8.35.

The company’s 2025 guidance summary is presented below:

Key drivers supporting the guidance include strong infrastructure and data center demand, full-year contributions from operations acquired in 2024, continued product pricing momentum, and effective cost management. These positive factors are partially offset by "higher-for-longer interest rates and related residential construction softness," according to the presentation.

Strategic Positioning

Martin Marietta’s Q1 2025 results and full-year outlook reflect the company’s strategic focus on its aggregates-led business model, which has demonstrated resilience amid varying market conditions. The company’s ability to achieve record first-quarter results despite weather challenges highlights the effectiveness of its pricing strategy and operational efficiency initiatives.

The company is well-positioned to benefit from infrastructure spending, which provides a countercyclical buffer against weakness in residential construction. Additionally, the growing demand for data centers represents an emerging opportunity in the nonresidential sector.

Martin Marietta’s stock closed at $504.86 on April 29, 2025, with a slight increase in pre-market trading on the day of the earnings release. The stock remains within its 52-week range of $441.95 to $633.23, reflecting investor confidence in the company’s ability to navigate the current market environment while capitalizing on long-term growth opportunities in infrastructure and select nonresidential segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.