Gold prices tick higher on fresh U.S. tariff threats, Fed rate cut hopes

Introduction & Market Context

Match Group (NASDAQ:MTCH) released its Q2 2025 supplemental presentation on August 5, 2025, revealing flat year-over-year revenue but continued divergence in performance across its dating app portfolio. The company’s stock, which had fallen 3.69% following its Q1 earnings miss, traded up 0.47% to $34.04 in after-market trading following the Q2 presentation. The results come as Match Group continues its transformation efforts under CEO Spencer Raskoff, who emphasized a "consumer-first mindset" during the previous quarter’s earnings call.

Quarterly Performance Highlights

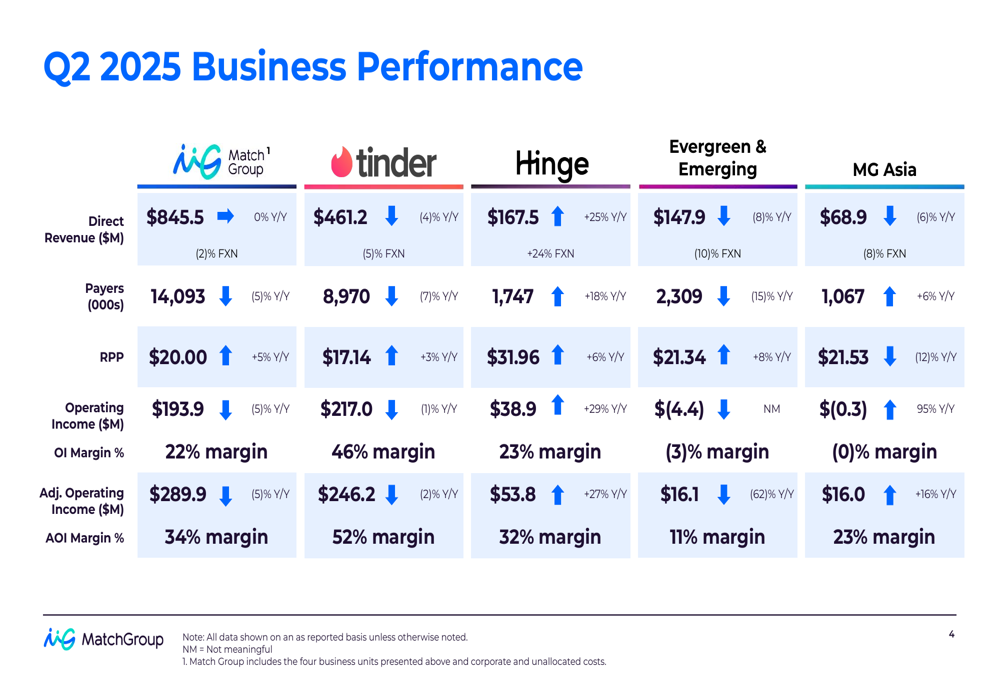

Match Group reported total direct revenue of $845.5 million in Q2 2025, flat year-over-year but down 2% on a foreign exchange neutral (FXN) basis. The company’s payer base continued to decline, falling 5% year-over-year to 14.1 million users, though this was partially offset by a 5% increase in revenue per payer (RPP) to $20.00.

As shown in the following comprehensive business performance snapshot, the company’s operating income declined 5% year-over-year to $193.9 million, with an operating income margin of 22%. Adjusted operating income also fell 5% to $289.9 million, maintaining a 34% margin.

The most striking contrast continues to be between the company’s two flagship apps. Hinge maintained its strong growth trajectory with direct revenue increasing 25% year-over-year to $167.5 million, driven by an 18% increase in payers and a 6% increase in RPP. Meanwhile, Tinder’s direct revenue declined 4% to $461.2 million, with payers down 7% but RPP up 3%.

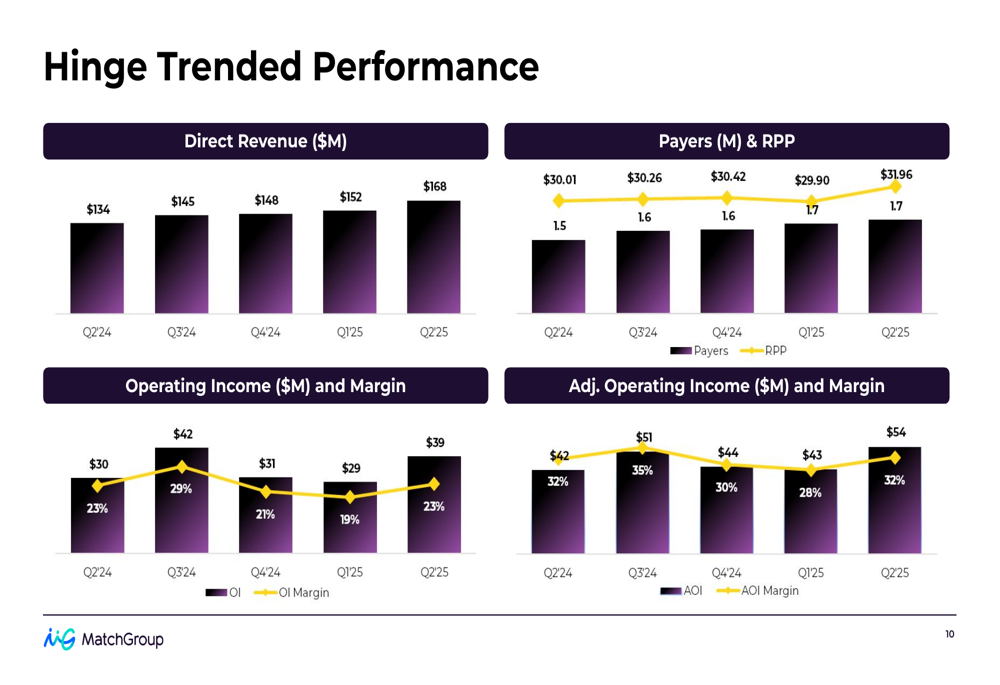

The following chart illustrates Hinge’s impressive performance across key metrics, with operating income growing 29% year-over-year to $38.9 million and adjusted operating income increasing 27% to $53.8 million:

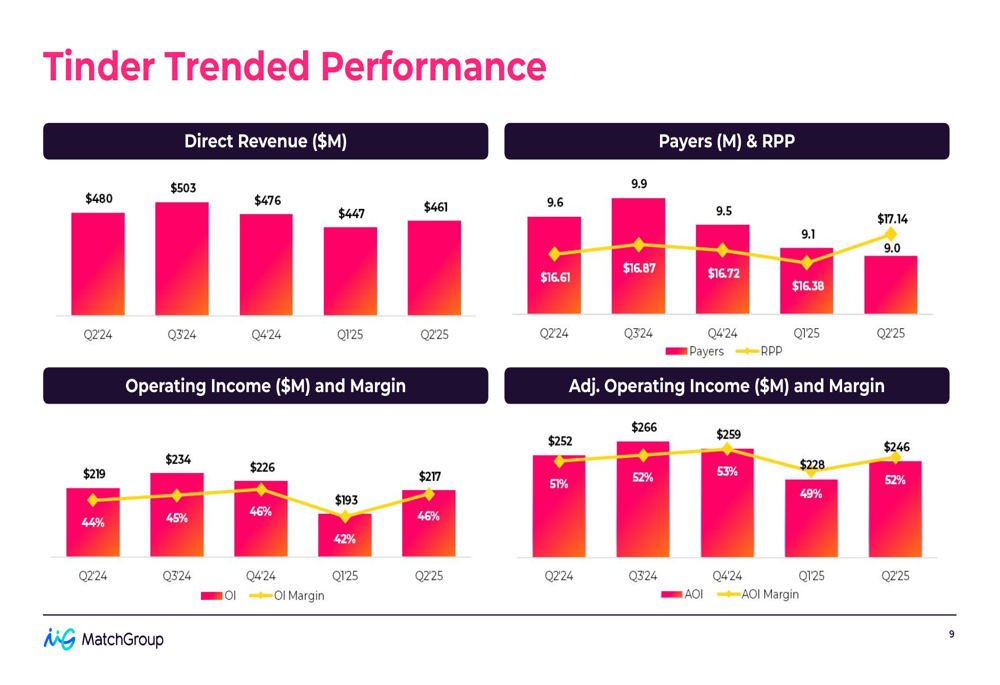

In contrast, Tinder’s performance shows the continued challenges facing Match Group’s largest app, though it maintains strong profitability with a 46% operating income margin:

Detailed Financial Analysis

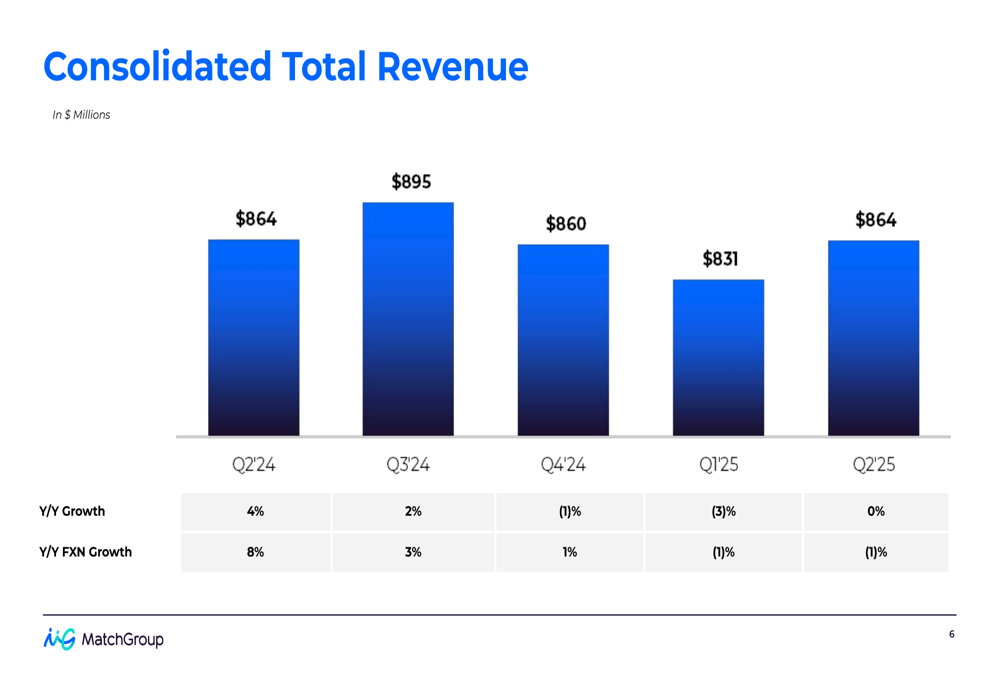

Looking at consolidated revenue trends over the past five quarters, Match Group’s total revenue has remained relatively stable between $831 million and $895 million, with Q2 2025 showing slight improvement from Q1 but still below peak levels seen in Q3 2024:

The company’s profitability metrics show some quarterly fluctuation but remain relatively stable year-over-year. Operating income for Q2 2025 was $194 million (22% margin), while adjusted operating income reached $290 million (34% margin):

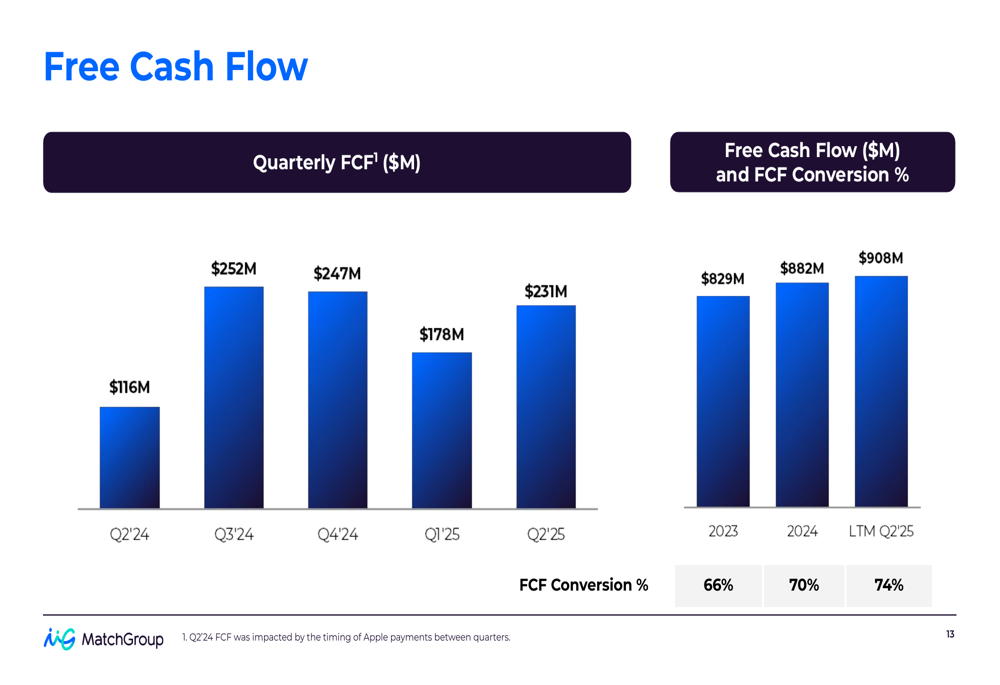

Free cash flow has shown significant improvement, reaching $231 million in Q2 2025 compared to $116 million in Q2 2024. On a last twelve months (LTM) basis, free cash flow reached $908 million with a 74% conversion rate, up from 70% in 2024:

Strategic Initiatives

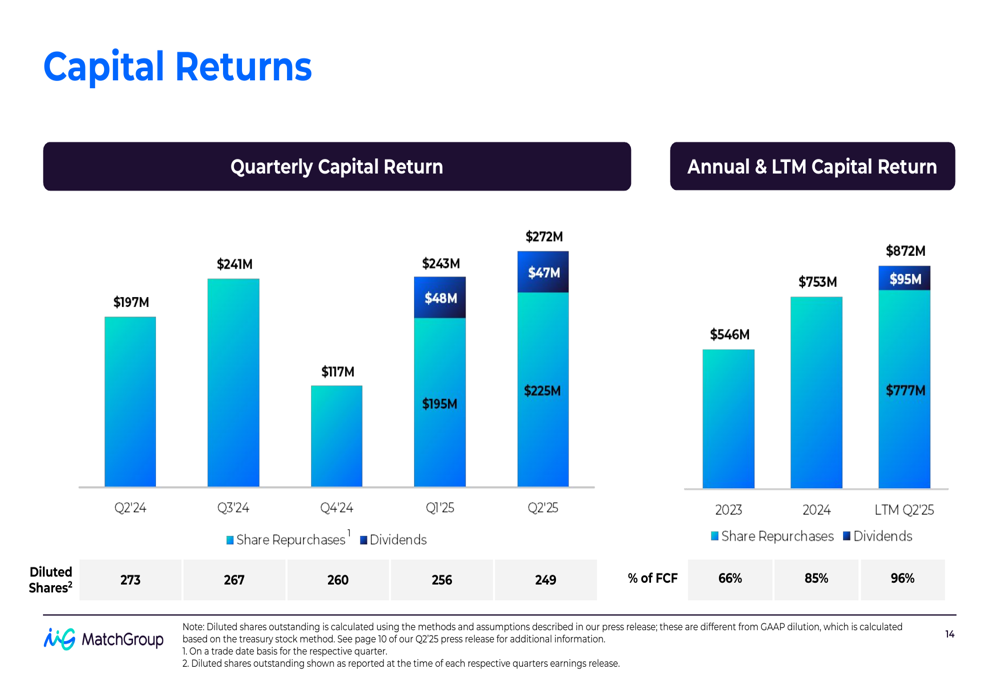

Match Group has significantly enhanced its capital return program, introducing dividends in Q1 2025 while maintaining robust share repurchases. In Q2 2025, the company returned $272 million to shareholders through $225 million in share repurchases and $47 million in dividends.

The following chart shows the company’s consistent capital return strategy, which has reduced diluted shares outstanding from 273 million in Q2 2024 to 249 million in Q2 2025:

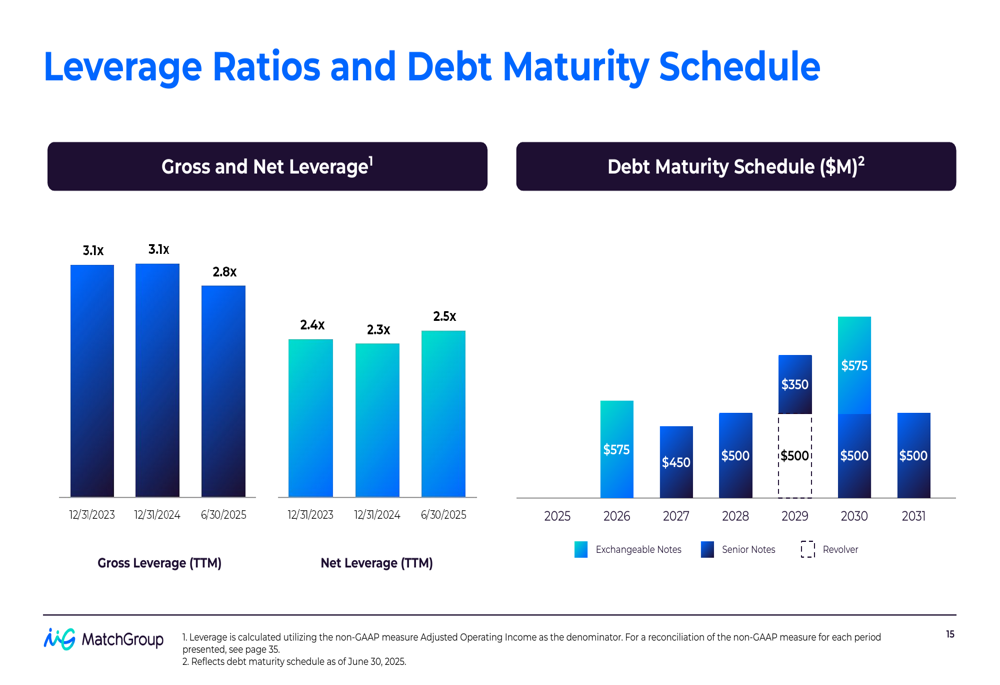

The company has also improved its financial position, with gross leverage decreasing to 2.8x and net leverage to 2.5x as of June 30, 2025. The debt maturity schedule remains well-structured with no immediate refinancing pressures:

Forward-Looking Statements

While the Q2 presentation did not include specific forward guidance, the previous quarter’s earnings report indicated that Match Group maintained its full-year 2025 revenue guidance between $3.375 billion and $3.500 billion. For Q2 2025, the company had projected revenue between $850 million and $860 million with adjusted operating income between $295 million and $300 million.

The actual Q2 2025 results show revenue of $863.7 million, slightly exceeding the upper end of guidance, while adjusted operating income of $289.9 million fell just short of the projected range. This suggests the company is executing reasonably well against its financial targets despite ongoing challenges with its Tinder business.

The divergent performance between Hinge and Tinder highlights the strategic importance of portfolio diversification for Match Group. While Tinder continues to generate substantial profits despite declining user numbers, Hinge’s growth trajectory provides a critical offset that supports overall company stability. Meanwhile, the enhanced capital return program signals management’s confidence in sustainable cash generation despite the mixed operational performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.