US stock futures dip as Trump’s firing of Cook sparks Fed independence fears

Introduction & Market Context

Materion Corporation (NYSE:MTRN) released its first quarter 2025 earnings presentation on May 1, highlighting solid performance despite mixed end-market conditions. The advanced materials supplier delivered growth in key financial metrics while warning of potential tariff impacts in the coming quarters. The company’s stock was trading down 1.46% in premarket activity following the release.

The results come against a backdrop of continued strength in aerospace, defense, and semiconductor markets, while consumer electronics and automotive sectors remain challenged. Materion’s performance reflects its strategic positioning in high-growth markets and operational improvements that have enabled margin expansion despite uneven demand.

Quarterly Performance Highlights

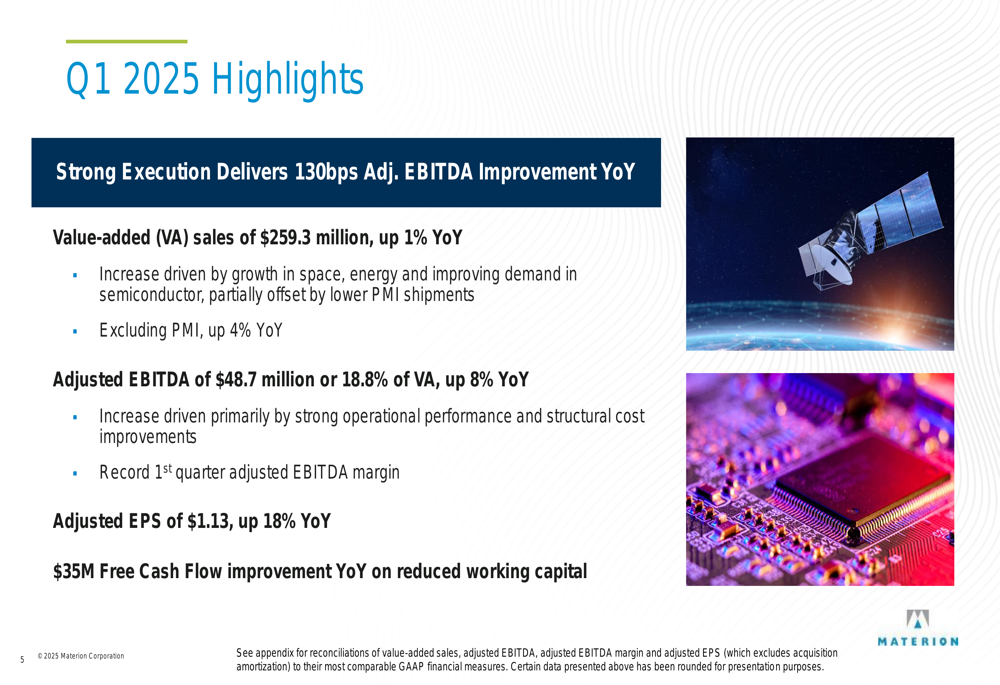

Materion reported value-added sales of $259.3 million for Q1 2025, representing a modest 1% year-over-year increase. More impressively, adjusted EBITDA grew 8% to $48.7 million, with margins expanding 130 basis points to 18.8%. Adjusted earnings per share jumped 18% to $1.13, demonstrating the company’s ability to drive bottom-line growth even with limited top-line expansion.

As shown in the following summary of Q1 2025 highlights, the company achieved record first-quarter adjusted EBITDA margin while generating substantial free cash flow improvement:

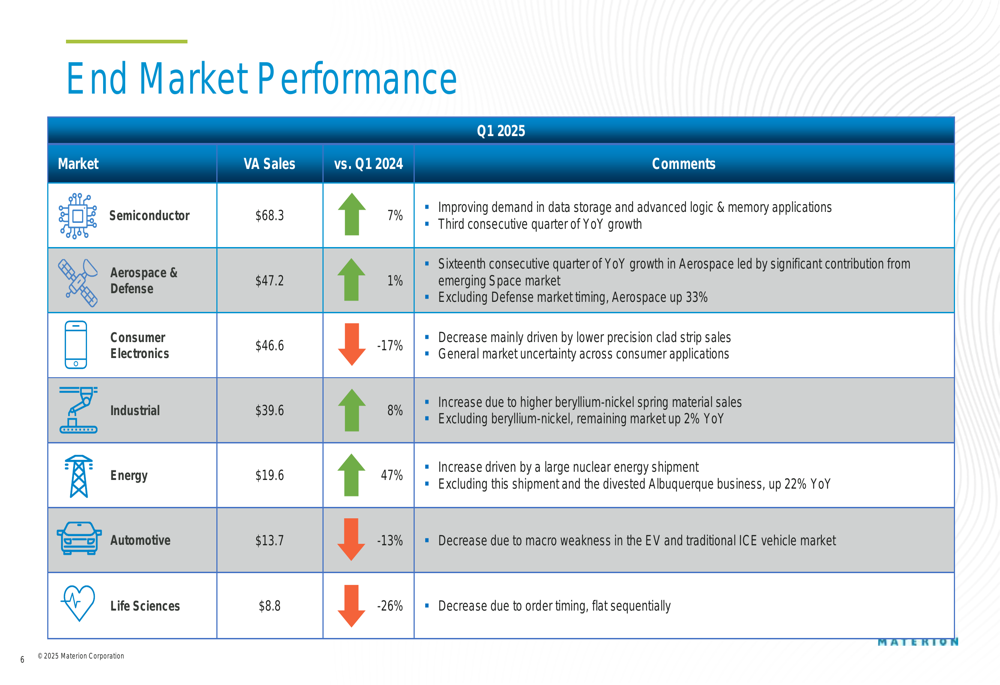

The company’s end market performance revealed significant variability across sectors. Semiconductor sales grew 7% year-over-year to $68.3 million, marking the third consecutive quarter of growth in this segment. Aerospace & Defense continued its strong performance with a 1% increase to $47.2 million, representing the sixteenth consecutive quarter of year-over-year growth in Aerospace.

Energy was the standout performer with 47% growth to $19.6 million, driven by a large nuclear energy shipment. Industrial markets also showed strength with 8% growth to $39.6 million. However, these gains were partially offset by weakness in Consumer Electronics (down 17% to $46.6 million), Automotive (down 13% to $13.7 million), and Life Sciences (down 26% to $8.8 million).

The following breakdown illustrates the company’s performance across various end markets:

Segment Analysis

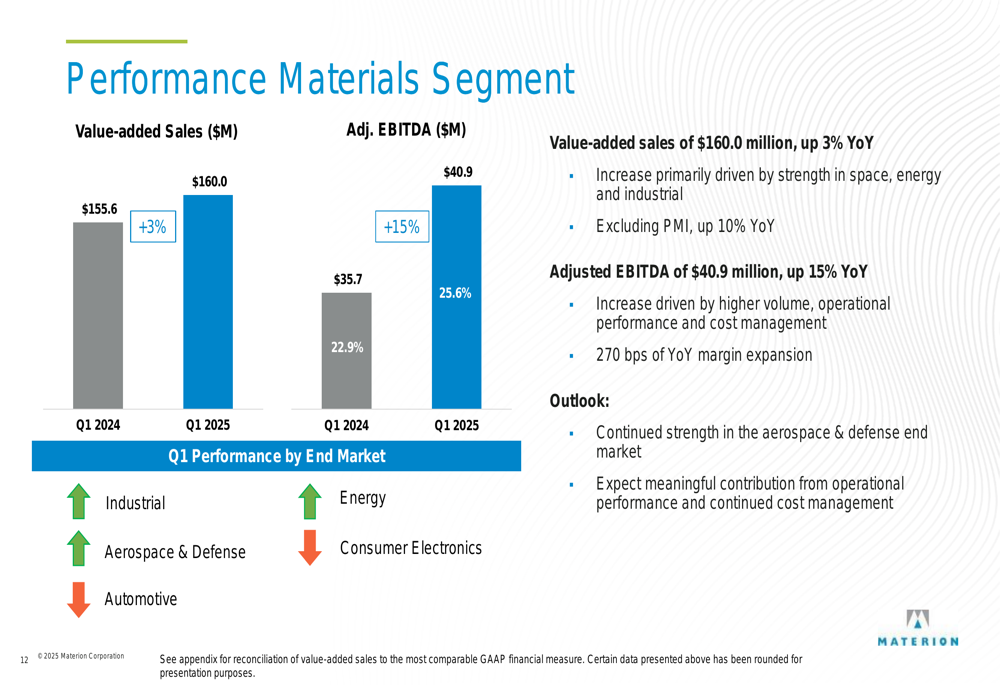

Materion’s three business segments delivered mixed results in the quarter. The Performance Materials segment was the clear standout, with value-added sales increasing 3% year-over-year to $160.0 million and adjusted EBITDA jumping 15% to $40.9 million. This segment benefited from strength in space, energy, and industrial markets, with margins expanding 270 basis points year-over-year.

As shown in the Performance Materials segment results, operational improvements and cost management contributed significantly to profitability:

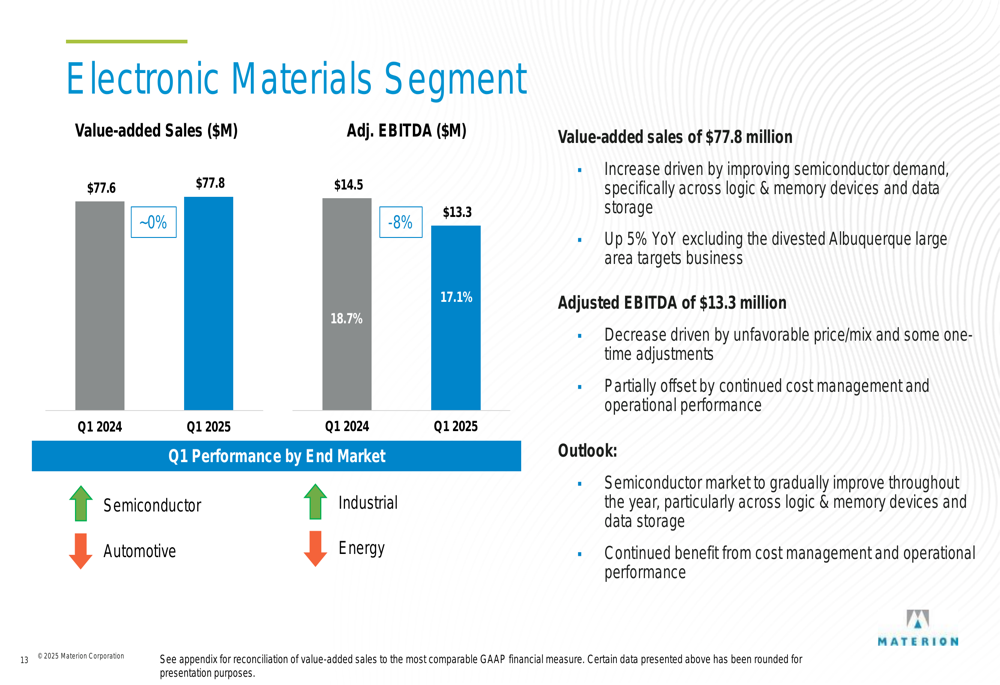

The Electronic Materials segment reported essentially flat value-added sales of $77.8 million but saw adjusted EBITDA decline 8% to $13.3 million. Management noted that while semiconductor demand is improving, particularly in logic & memory devices and data storage, unfavorable price mix and one-time adjustments impacted profitability.

The following chart details the Electronic Materials segment performance:

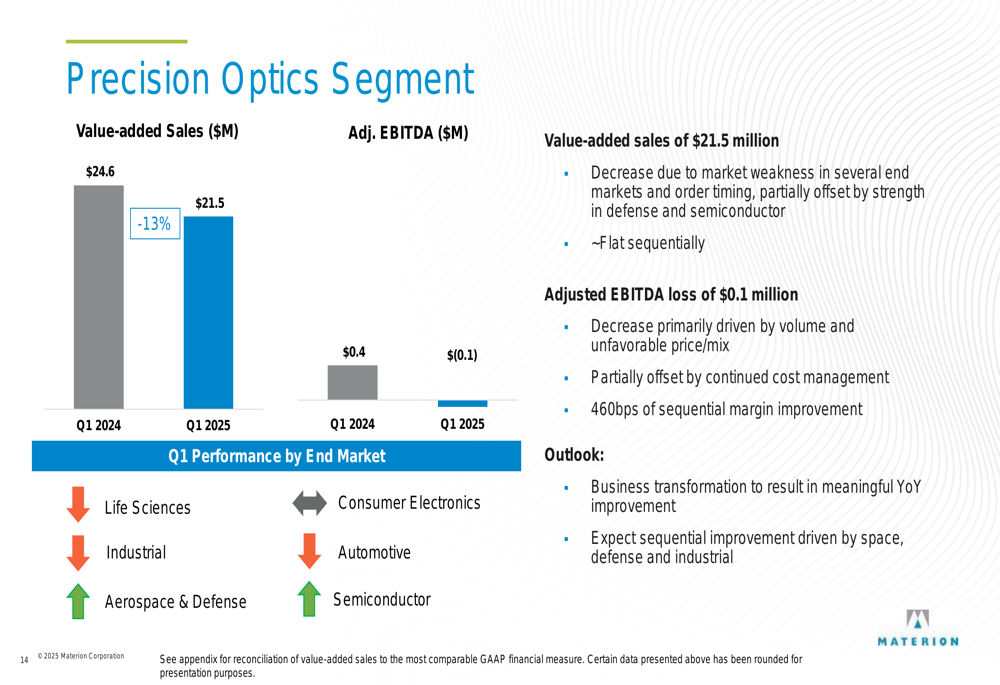

The Precision Optics segment continued to face challenges, with value-added sales declining 13% to $21.5 million and an adjusted EBITDA loss of $0.1 million. The company cited market weakness and order timing as primary factors, though management expressed expectations for sequential improvement driven by space, defense, and industrial applications.

The Precision Optics segment results highlight the ongoing challenges in this business unit:

Tariff Impact and Mitigation Strategies

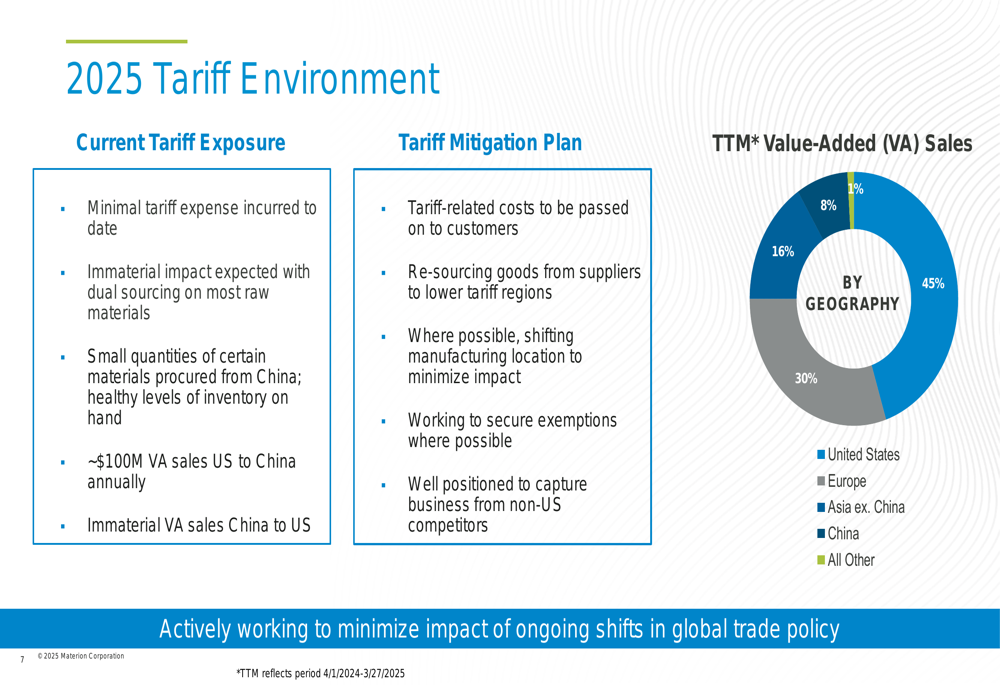

A significant focus of Materion’s presentation was the potential impact of tariffs, particularly related to China. While the company reported minimal tariff expenses to date, management warned of increasing headwinds throughout 2025, estimating a $0.10-0.15 impact on EPS in Q2 and a potential $0.40-0.50 impact in the second half of the year.

Materion outlined its tariff exposure and mitigation plans, noting that approximately 8% of its value-added sales come from China, with about $100 million in annual sales flowing from the US to China. The company’s mitigation strategy includes passing tariff-related costs to customers, re-sourcing goods from suppliers in lower tariff regions, shifting manufacturing locations where possible, and working to secure exemptions.

The following slide details Materion’s tariff environment and geographic sales distribution:

Outlook and Guidance

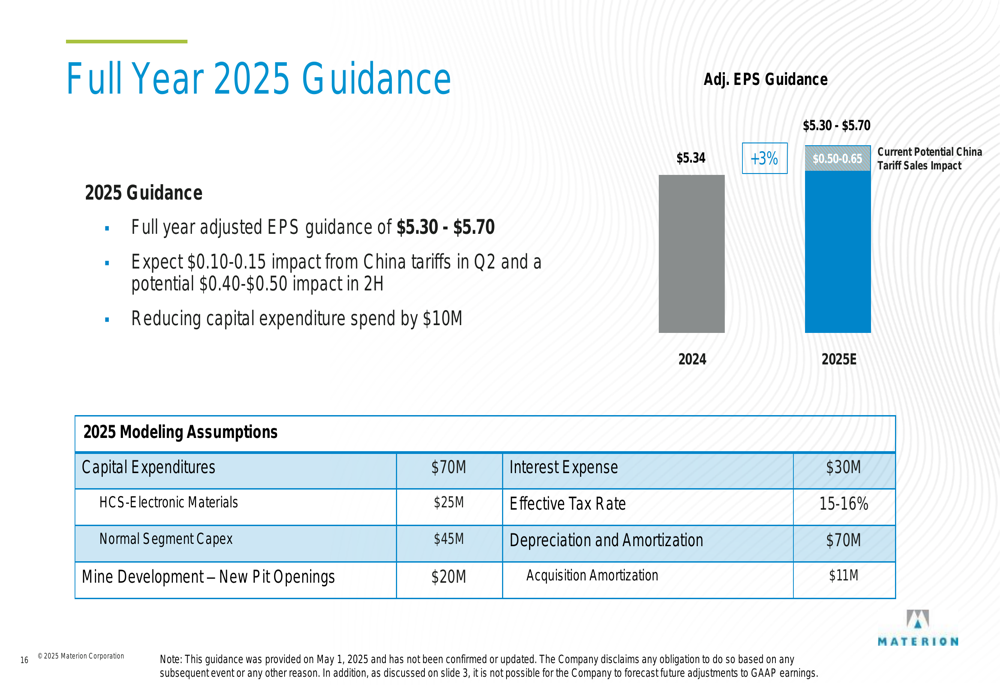

Despite tariff concerns, Materion maintained a positive outlook for 2025, projecting full-year adjusted EPS of $5.30-$5.70. Management expects Q2 performance to be slightly better than Q1, with continued strength in aerospace, defense, and semiconductor markets.

The company is reducing capital expenditure plans by $10 million to $70 million for the year, while maintaining its focus on operational excellence and cost management. Materion expects to deliver 20%+ adjusted EBITDA margin for the full year, reflecting confidence in its ability to navigate market challenges.

As shown in the full-year guidance slide, the company has provided detailed modeling assumptions for investors:

On the balance sheet front, Materion reported net debt of $435.7 million as of Q1 2025, down from $462.2 million in Q1 2024. The company’s leverage ratio improved to 1.9x TTM adjusted EBITDA, down from 2.2x a year earlier, positioning it slightly below the midpoint of its target range of 1.5x-3.0x.

Among strategic developments, Materion highlighted a multi-year agreement with Idaho National Lab to supply materials supporting nuclear energy research and development, reinforcing its position in the growing energy sector.

Management emphasized that despite macroeconomic uncertainties and tariff headwinds, the company’s focus on operational performance, cost management, and strategic positioning in growth markets should enable continued financial improvement throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.