Novo Nordisk, Eli Lilly fall after Trump comments on weight loss drug pricing

Introduction & Market Context

Mativ Holdings Inc. (NYSE:MATV) released its first quarter 2025 earnings presentation on May 8, revealing a substantial goodwill impairment charge that significantly impacted financial results. The company reported flat organic sales year-over-year while taking a $411.9 million goodwill impairment charge that drove GAAP net losses to $425.5 million.

The stock, which has been under pressure in recent months, closed at $5.03 on May 7, near its 52-week low of $4.34 and far below its 52-week high of $19.96. However, shares gained 2.39% in after-hours trading following the earnings release, suggesting investors may be focusing on the company’s turnaround strategy rather than the impairment charge.

Quarterly Performance Highlights

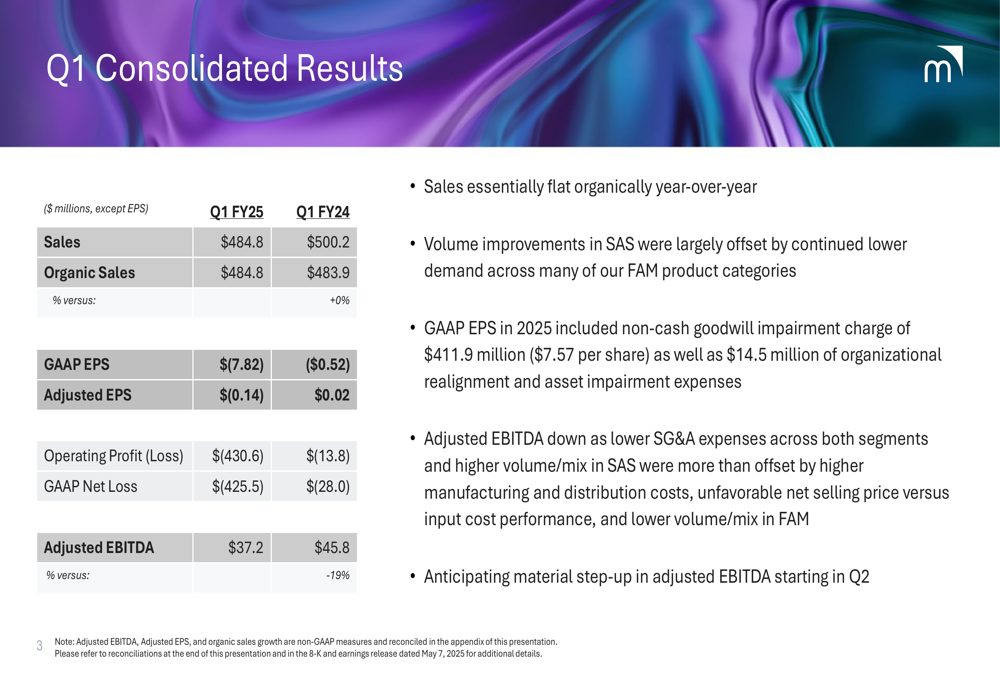

Mativ reported first quarter sales of $484.8 million, down from $500.2 million in the same period last year, with organic sales flat year-over-year. The company posted a GAAP loss per share of $(7.82) compared to $(0.52) in Q1 2024, primarily due to the goodwill impairment. Adjusted EPS was $(0.14) versus $0.02 in the prior year.

As shown in the following consolidated results summary:

Adjusted EBITDA declined 19% to $37.2 million from $45.8 million in Q1 2024. The company’s GAAP operating loss was $430.6 million compared to a loss of $13.8 million in the prior year period, while GAAP net loss expanded to $425.5 million from $28.0 million.

The variance analysis reveals the specific factors affecting performance:

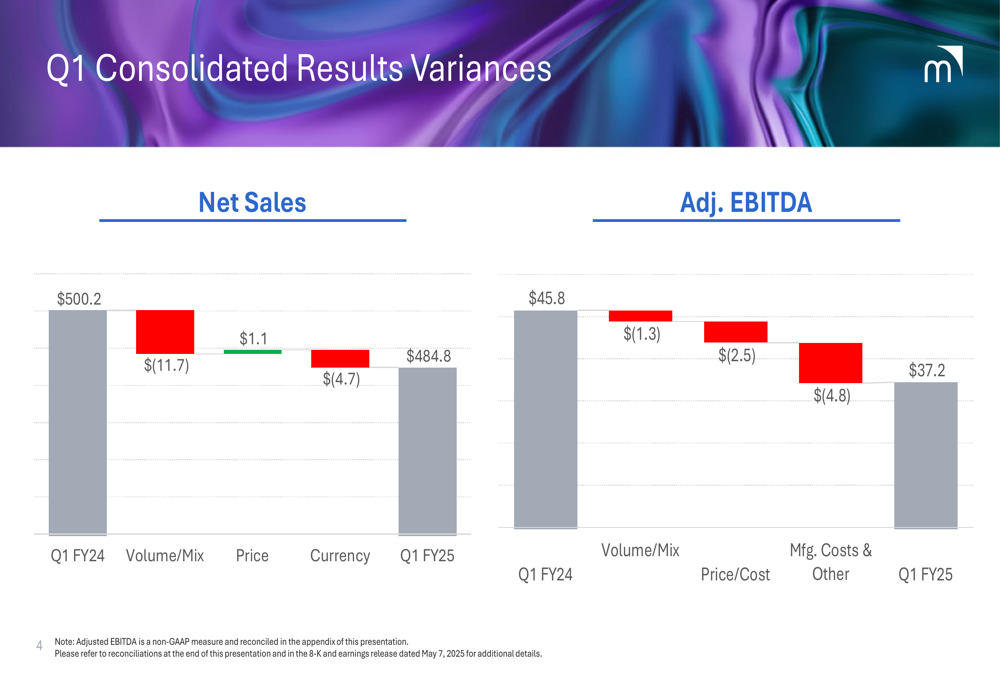

Volume and mix had the most significant negative impact on both net sales and adjusted EBITDA, with an $11.7 million reduction in sales and a $1.3 million decrease in EBITDA. Manufacturing costs and other factors further reduced adjusted EBITDA by $4.8 million, while price/cost dynamics negatively impacted EBITDA by $2.5 million.

Segment Performance Analysis

Mativ’s two business segments showed divergent performance in the first quarter. The Fiber-Based Materials (FAM) segment continued to struggle, while the Specialty Advanced Solutions (SAS) segment demonstrated resilience with organic growth.

The segment results highlight this performance divergence:

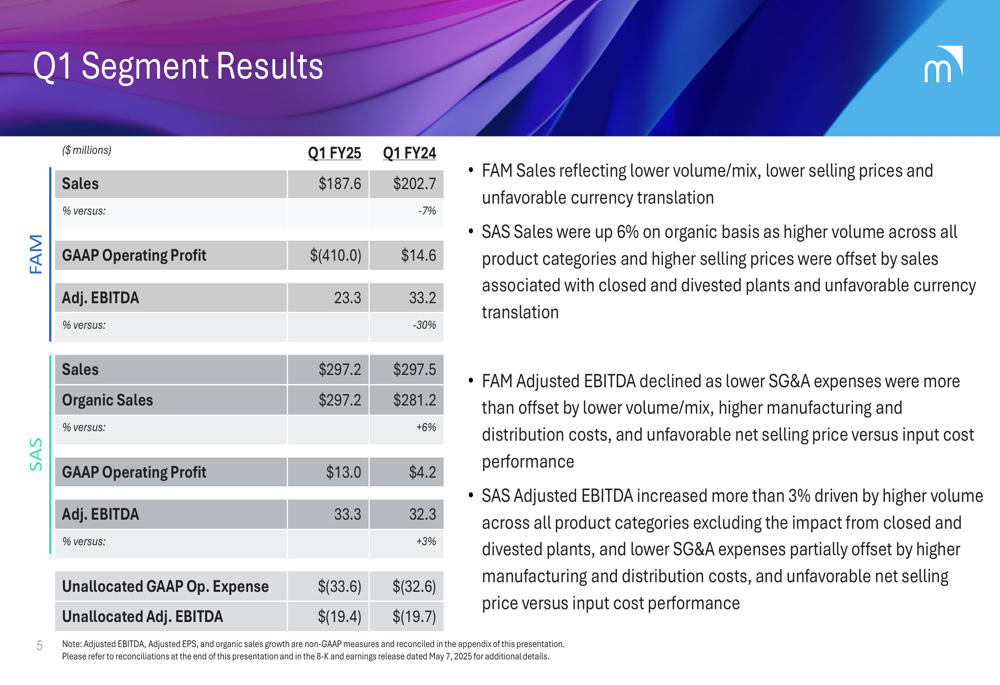

The FAM segment reported sales of $187.6 million, down from $202.7 million in Q1 2024, and adjusted EBITDA declined 30% to $23.3 million. This segment was also the primary target of the goodwill impairment, resulting in a GAAP operating loss of $410.0 million compared to a profit of $14.6 million in the prior year.

In contrast, the SAS segment delivered 6% organic sales growth, with total sales of $297.2 million, essentially flat compared to $297.5 million in Q1 2024. SAS adjusted EBITDA increased 3% to $33.3 million, and GAAP operating profit improved to $13.0 million from $4.2 million.

Strategic Initiatives

Mativ outlined three key strategic priorities for 2025 aimed at improving performance and strengthening its financial position:

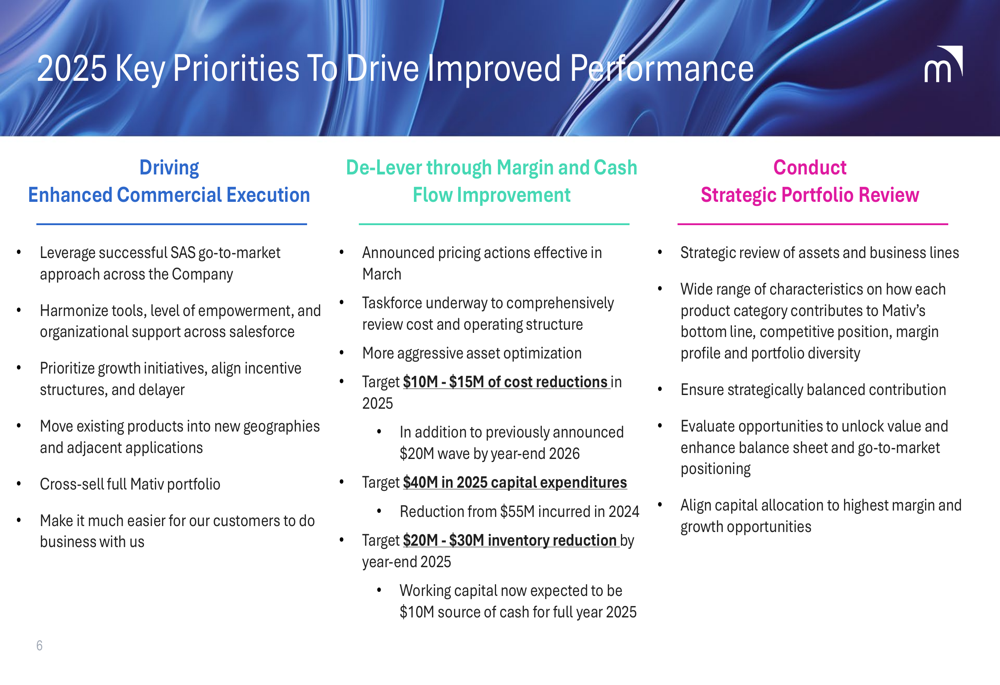

The company is focusing on enhancing commercial execution, particularly by leveraging the successful go-to-market approach from its SAS segment across the organization. This includes implementing a more targeted approach to customer and product profitability and accelerating innovation in high-growth areas.

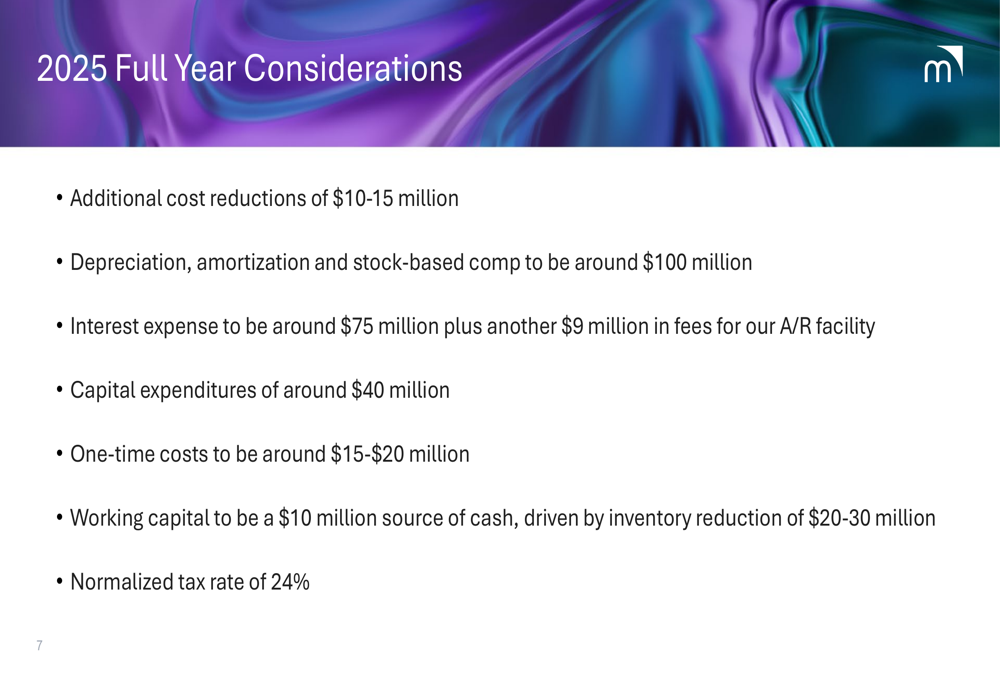

De-leveraging through margin and cash flow improvement represents another critical priority. Mativ plans to optimize its asset base, reduce inventory by $20-30 million, and limit capital expenditures to approximately $40 million for the year. The company is also implementing additional cost reduction measures of $10-15 million.

The third strategic pillar involves a comprehensive portfolio review to evaluate assets and business lines, suggesting potential divestitures or restructuring of underperforming units in the future.

Forward-Looking Statements

For the remainder of 2025, Mativ provided several financial considerations and targets:

The company expects depreciation, amortization, and stock-based compensation to total approximately $100 million for the year. Interest expense is projected at around $75 million, plus an additional $9 million in fees for an accounts receivable facility.

Management anticipates one-time costs of $15-20 million related to restructuring and strategic initiatives. Working capital is expected to be a $10 million source of cash, primarily driven by the planned $20-30 million inventory reduction. The company is targeting a normalized tax rate of 24%.

Most notably, Mativ expressed confidence in a "material step-up in adjusted EBITDA starting in Q2," suggesting that the first quarter may represent a low point in the company’s performance for the year.

Conclusion

Mativ’s first quarter 2025 results reflect a company in transition, taking significant accounting charges while implementing a strategic turnaround plan. The substantial goodwill impairment has severely impacted reported results, but management appears focused on operational improvements and financial discipline moving forward.

The divergent performance between the struggling FAM segment and the growing SAS segment highlights both challenges and opportunities. Investors will likely focus on whether the company can deliver on its promise of improved EBITDA performance in the coming quarters and successfully execute its strategic priorities to strengthen its financial position and return to sustainable profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.