IREN proposes $875 million convertible notes offering due 2031

Matson Inc (NYSE:MATX) reported a strong first quarter with doubled net income, but lowered its full-year outlook amid significant trade uncertainties and tariff impacts, according to the company’s Q1 2025 earnings presentation delivered on May 5. The shipping and logistics company saw its stock decline 2.68% to $113.14 during regular trading, with minimal movement in after-hours trading.

Quarterly Performance Highlights

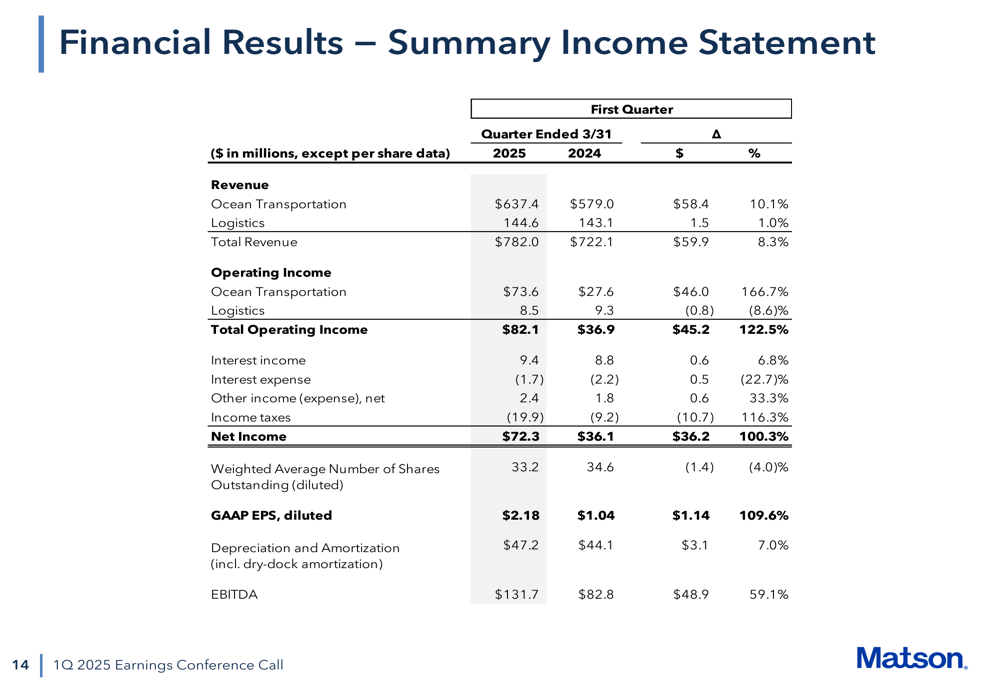

Matson delivered impressive year-over-year growth in Q1 2025, with consolidated operating income more than doubling to $82.1 million compared to $36.9 million in Q1 2024. Net income reached $72.3 million, a 100.3% increase from the $36.1 million reported in the same quarter last year. Diluted earnings per share doubled to $2.18 from $1.04 in the prior year.

Total (EPA:TTEF) revenue increased 8.3% to $782.0 million, with Ocean Transportation revenue rising 10.1% to $637.4 million while Logistics revenue grew modestly by 1.0% to $144.6 million. The company’s EBITDA climbed to $131.7 million, up from $82.8 million in Q1 2024.

As shown in the following summary income statement from the presentation:

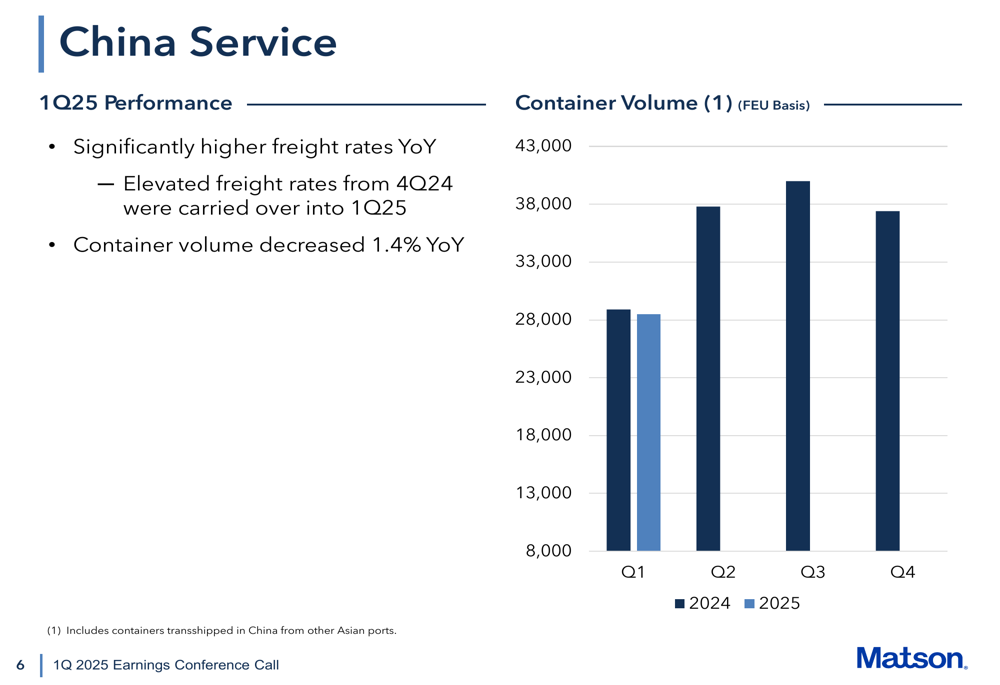

"1Q25 operating income was significantly higher year-over-year. The China service was the primary driver, benefiting from elevated freight rates from 4Q24 and healthy demand following the Lunar New Year," the company stated in its opening remarks.

China Service Impact

The China service remained Matson’s primary performance driver in Q1, benefiting from elevated freight rates carried over from the fourth quarter of 2024. However, container volume in this segment decreased slightly by 1.4% year-over-year.

More concerning for investors is the company’s disclosure that "container volume has declined approximately 30% year-over-year since tariffs were implemented in April." This dramatic drop highlights the immediate impact of recent trade tensions between the U.S. and China.

The following chart illustrates the China service container volume trends:

Matson noted significant uncertainty regarding tariffs, global trade, regulatory measures, the trajectory of the U.S. economy, and other geopolitical factors. The company believes it is "in the early innings of U.S.-China trade negotiations" and expects "disruptive conditions in the Transpacific with ocean carriers blanking China sailings."

Regional Performance

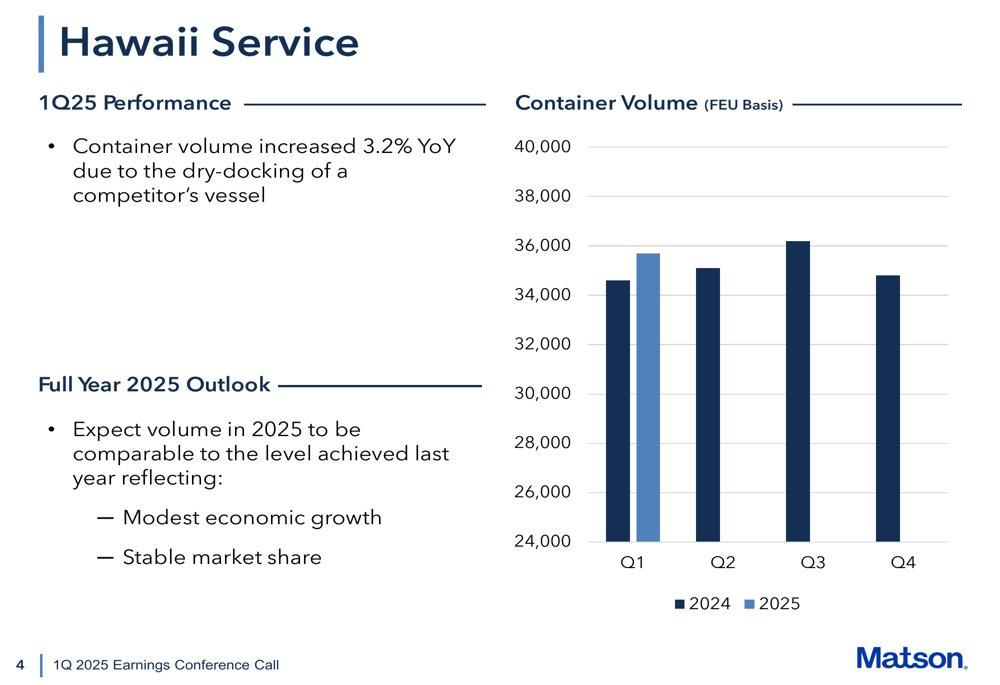

Performance across Matson’s other service regions was mixed. Hawaii service container volume increased 3.2% year-over-year, primarily due to a competitor’s vessel being dry-docked. Alaska service volume grew 4.8% due to higher northbound volume. However, Guam service volume decreased significantly by 14.3%, primarily due to lower demand from retail and food and beverage segments.

The Hawaii service volume is illustrated in the following chart:

The SSAT terminal joint venture contributed $6.6 million, a year-over-year increase of $6.2 million, primarily due to higher lift volume. Meanwhile, Logistics operating income was $8.5 million, a slight year-over-year decrease of $0.8 million due to lower contributions from freight forwarding and transportation brokerage.

Financial Position and Capital Allocation

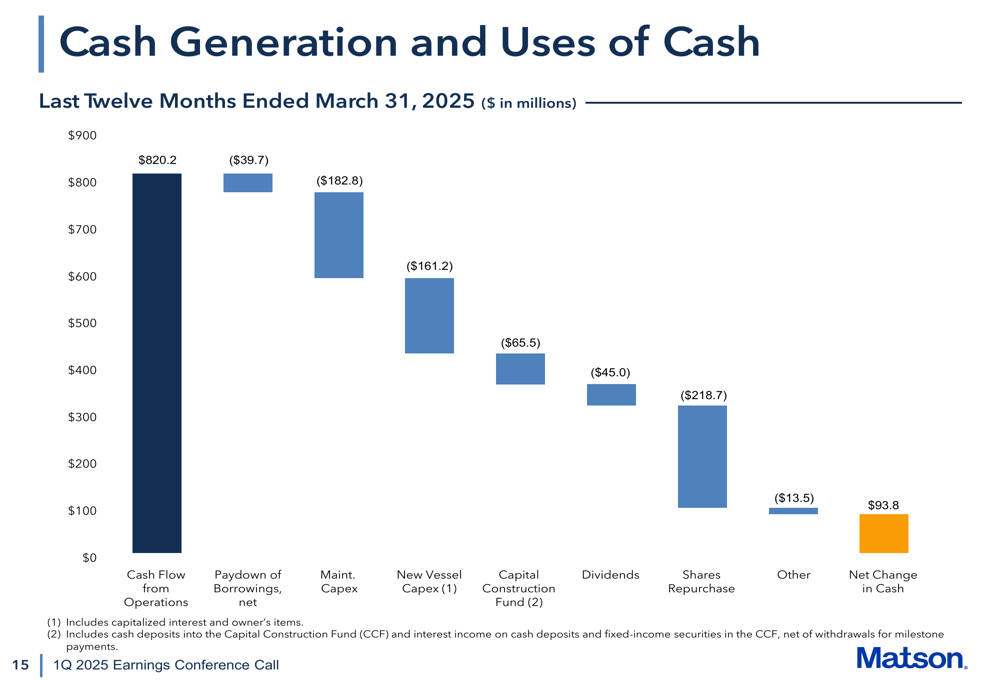

Matson maintained a strong financial position with $122.0 million in cash and cash equivalents as of March 31, 2025, down from $266.8 million at the end of 2024. Total debt stood at $390.8 million, having decreased by $10.1 million in Q1.

The company continued its shareholder return program, repurchasing approximately 0.5 million shares for a total cost of $69.2 million during the quarter. For the twelve months ended March 31, 2025, Matson generated $820.2 million in cash flow from operations, allocating funds to debt reduction, capital expenditures, dividends, and share repurchases.

The following chart details Matson’s cash generation and uses:

Strategic Initiatives and Adaptation

In response to shifting trade patterns, Matson announced a new direct service connecting Ho Chi Minh City to its CLX and MAX Shanghai departures in Q1 2025. The company expects higher volumes from Vietnam in the near term as it accelerates the diversification of its "catchment basin" in Asia.

"We will run our business with a focus on speed, on-time arrivals, and customer service," the company stated, emphasizing its positioning as a trusted supply chain partner. "We have the resources and assets to move quickly to adapt to a changing environment and find opportunities."

Matson also addressed the United States Trade Representative’s Section 301 action, noting that while the company is exempt from the USTR’s notice of action due to its size, it "will still be negatively impacted directly by lower volume and indirectly by merchandise tariffs paid by our customers."

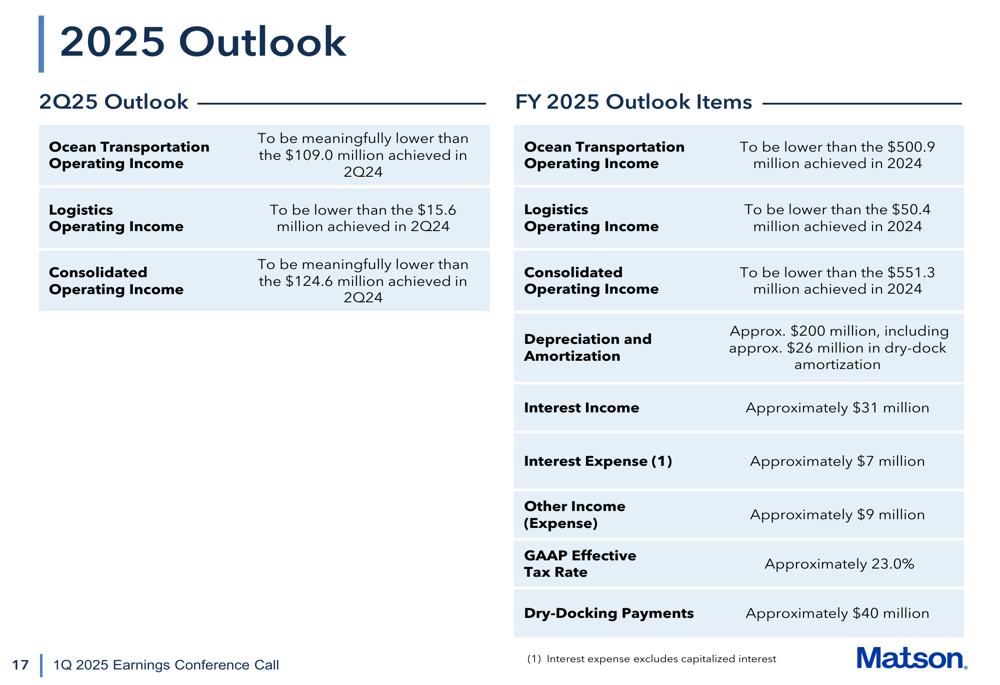

Outlook and Guidance

Despite strong Q1 results, Matson significantly lowered its outlook for the remainder of 2025. For Q2 2025, the company expects Ocean Transportation operating income to be "meaningfully lower" than the $109.0 million achieved in Q2 2024. Similarly, full-year 2025 Ocean Transportation and Logistics operating income is projected to be lower than 2024 levels.

The following slide details the company’s outlook:

Capital expenditures for 2025 are expected to total approximately $425 million, including $305 million for new vessel construction milestone payments and $100-120 million for maintenance and other capital expenditures.

In closing remarks, Matson acknowledged it is "navigating an unsettled and rapidly changing environment" while reaffirming its commitment to returning capital to shareholders through dividends and share repurchases.

The stock’s significant decline from its 52-week high of $169.12 to current levels around $113 reflects investor concerns about the company’s near-term prospects amid escalating trade tensions and tariff impacts.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.