CTAs keep buying Treasuries, gold longs face stop-loss risk: BofA

Introduction & Market Context

McCormick & Company (NYSE:MKC) presented its second quarter 2025 results on June 26, showing continued volume-led growth and successful navigation of tariff challenges. The spice and flavor maker’s stock jumped 4.24% in pre-market trading to $76.76, a significant reversal from the 1.43% decline following its Q1 results.

The company’s Q2 performance demonstrates resilience in a challenging economic environment, with particular strength in its Consumer segment offsetting softness in its Flavor Solutions business. This quarter’s results follow a Q1 that saw the company miss earnings expectations, with an EPS of $0.60 versus a forecasted $0.64.

Quarterly Performance Highlights

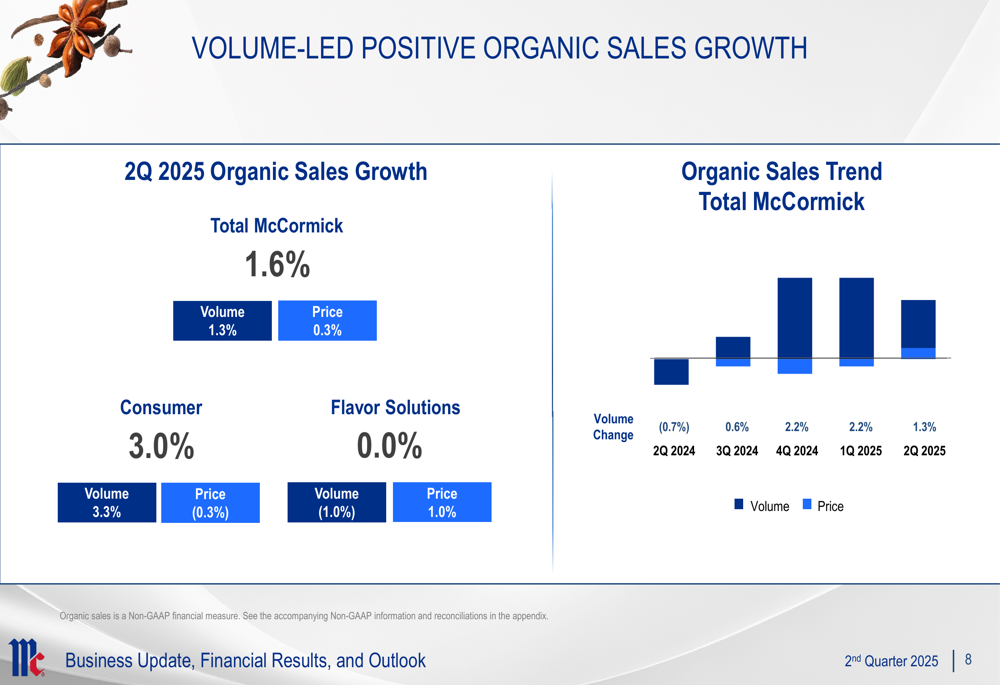

McCormick reported total organic sales growth of 1.6% for Q2 2025, driven primarily by volume growth of 1.3% with a modest price contribution of 0.3%. This performance reflects the company’s continued execution of its growth strategies across regions.

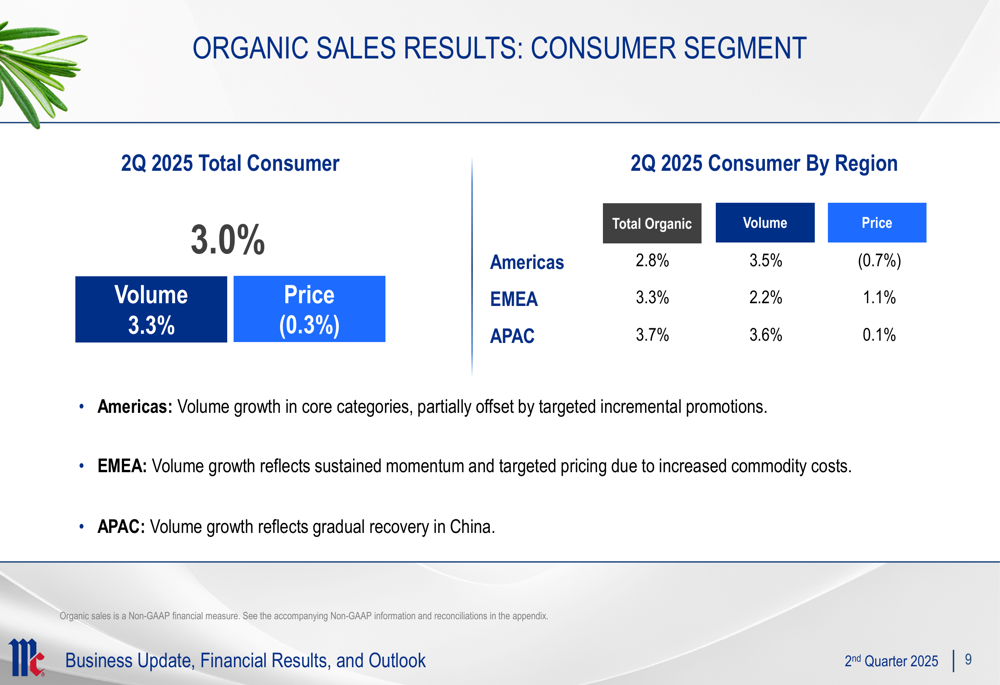

The Consumer segment was the standout performer with 3.0% organic growth, fueled by strong 3.3% volume growth that was partially offset by a 0.3% price decrease. All regions contributed positively to Consumer segment growth, with APAC leading at 3.7%, followed by EMEA at 3.3% and Americas at 2.8%.

As shown in the following chart of organic sales growth by segment:

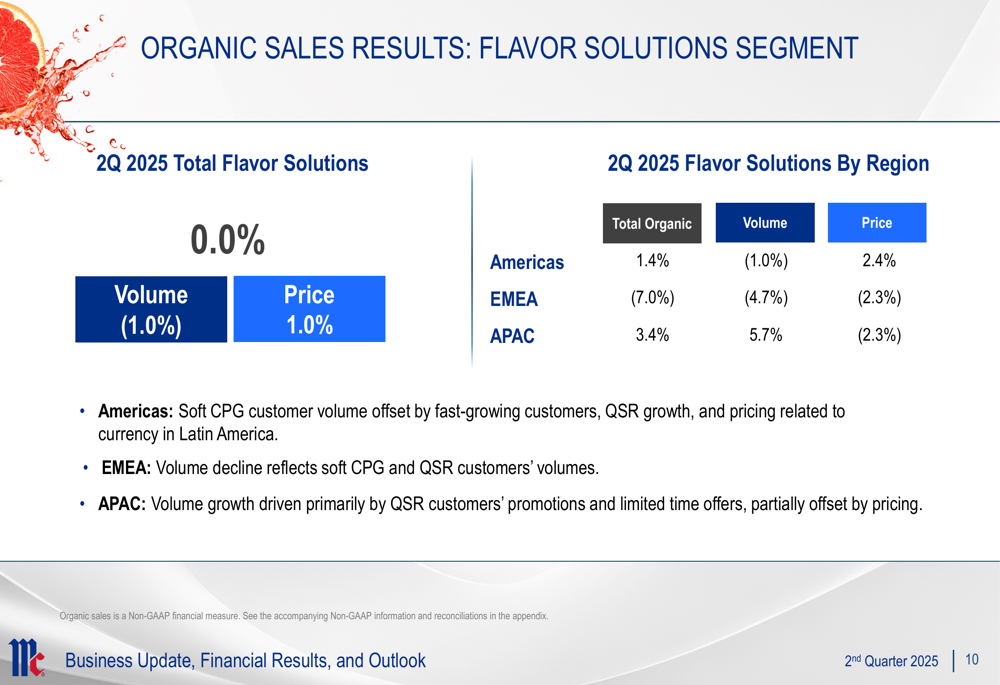

The Flavor Solutions segment faced more challenges, reporting flat organic sales (0.0%) as a 1.0% price increase was offset by a 1.0% volume decline. Regional performance varied significantly, with APAC growing 3.4%, Americas up 1.4%, while EMEA declined by 7.0%.

The company’s regional performance in the Consumer segment is illustrated in this breakdown:

Meanwhile, Flavor Solutions showed more mixed results across regions:

Detailed Financial Analysis

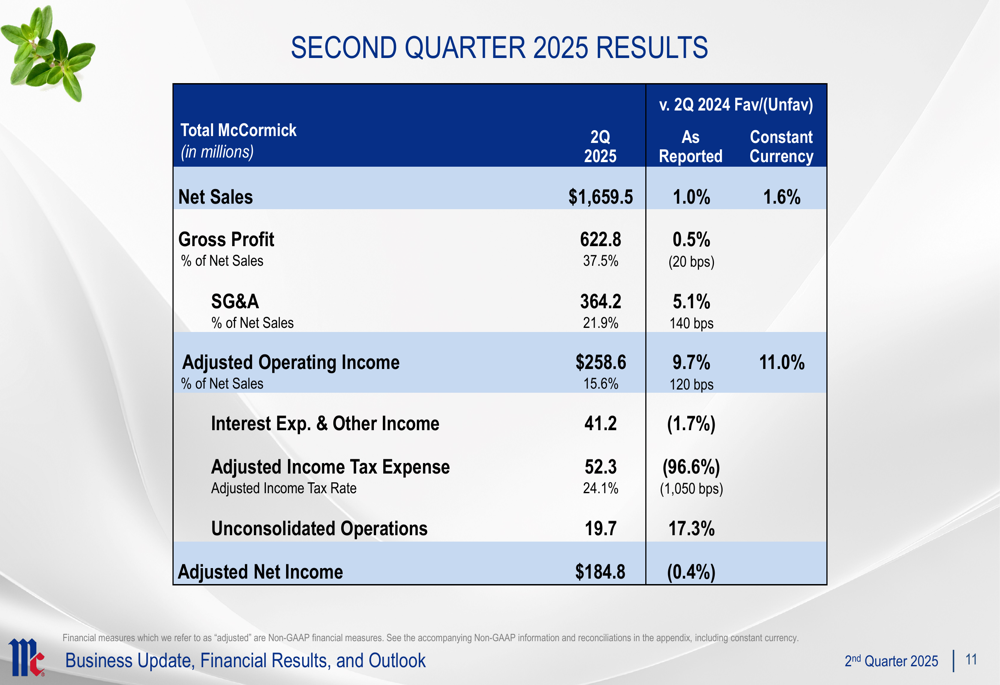

McCormick reported Q2 net sales of $1,659.5 million, up 1.0% as reported and 1.6% in constant currency. Adjusted operating income reached $258.6 million, representing 15.6% of net sales and increasing 9.7% as reported (11.0% in constant currency). This operating income growth significantly outpaced sales growth, indicating improved operational efficiency.

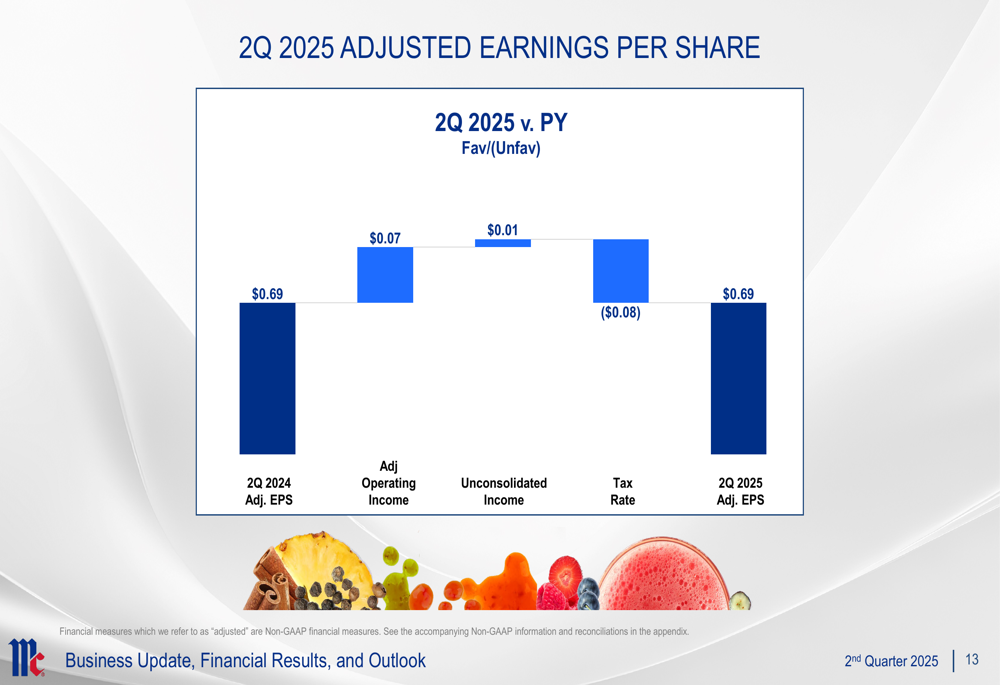

Despite the strong operating performance, adjusted net income decreased slightly by 0.4% to $184.8 million, primarily due to a higher adjusted income tax rate of 24.1%. Adjusted earnings per share remained flat at $0.69 compared to Q2 2024.

The comprehensive financial summary is presented in this table:

Breaking down performance by segment, Consumer delivered adjusted operating income of $163.6 million (17.6% of net sales), up 9.6%, while Flavor Solutions contributed $95.0 million (13.0% of net sales), up 9.8%. Both segments showed significant margin improvement despite varying sales performance.

The following chart illustrates the components affecting the quarter’s adjusted EPS:

Strategic Initiatives

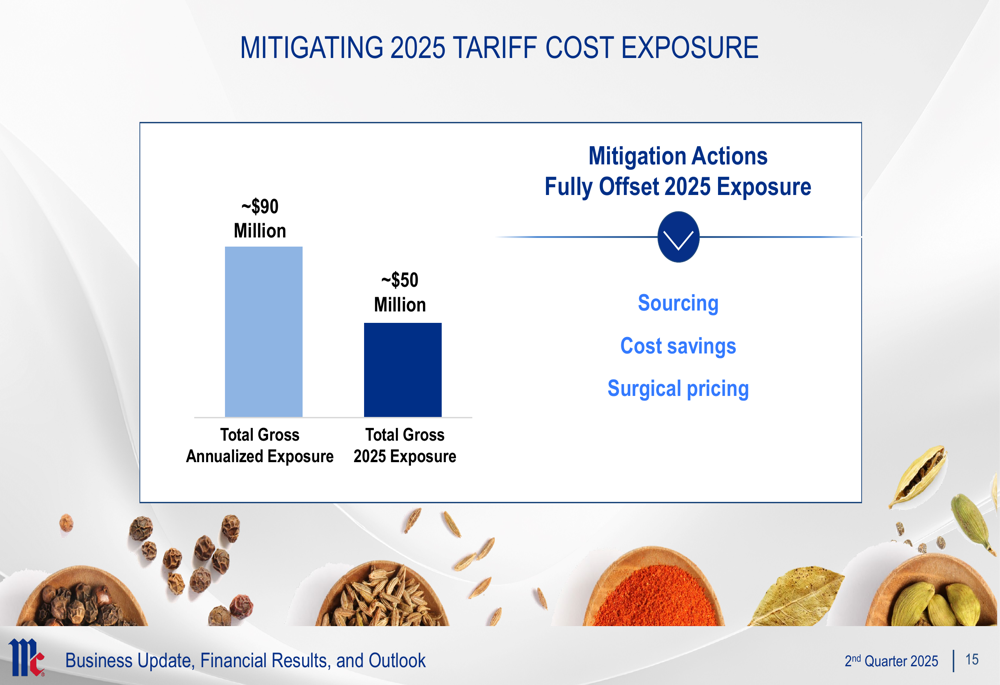

A key focus of McCormick’s Q2 presentation was its strategy to mitigate approximately $90 million in gross annualized tariff exposure. Through a combination of alternative sourcing, cost savings initiatives, and targeted pricing actions, the company expects to reduce the 2025 impact to approximately $50 million.

The tariff mitigation strategy is illustrated in this chart:

CEO Brendan Foley emphasized the company’s execution of proven growth strategies, noting strong volume growth in spices and seasonings across all regions, positive recipe mix performance in Americas, and strong hot sauce performance with share and distribution gains. The company also highlighted success in expanding total distribution points across core categories in Americas and EMEA.

Areas of pressure included softness in CPG customers’ volumes in Americas and EMEA, slowdown in foodservice foot traffic affecting Americas Branded Foodservice, and pressured QSR customer volume in EMEA.

Forward-Looking Statements

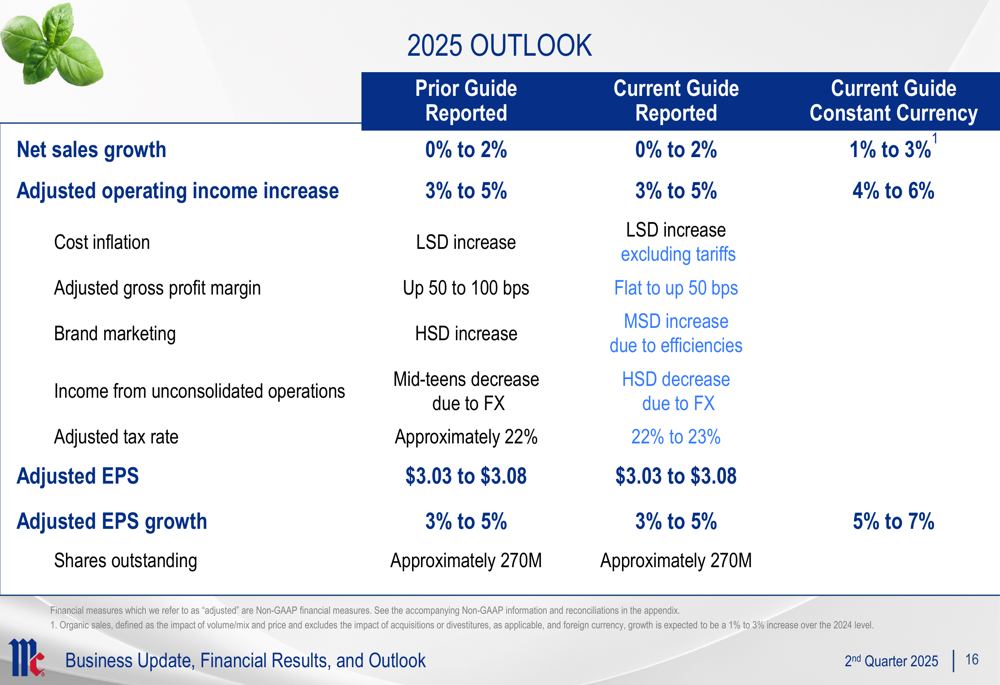

McCormick maintained its full-year 2025 guidance, projecting net sales growth of 0% to 2% (1% to 3% in constant currency) and adjusted EPS of $3.03 to $3.08, representing growth of 3% to 5% (5% to 7% in constant currency).

The company expects adjusted operating income to increase by 3% to 5% (4% to 6% in constant currency) and anticipates low single-digit cost inflation, excluding tariffs. Gross profit margin is expected to be flat to up 50 basis points, a slight reduction from the previous guidance of up 50 to 100 basis points, likely reflecting the tariff impact.

The complete 2025 outlook is detailed in this comprehensive guidance table:

"Our performance and growth plans support confidence in achieving our near and long-term objectives," stated Foley during the presentation. This sentiment represents a more positive outlook compared to Q1, when he noted "increasing consumer uncertainty and concern over returning to more inflation."

The company’s ability to maintain its full-year guidance while successfully addressing tariff challenges suggests management’s confidence in its strategic direction and operational execution for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.