September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

MDU Resources Group Inc. (NYSE:MDU) presented its second quarter 2025 earnings results on August 7, revealing significant year-over-year declines across all business segments. The company’s stock reacted negatively, dropping 6.69% to close at $16.32 following the presentation.

The utility company reported earnings per share (EPS) of $0.07 from continuing operations for Q2 2025, down from $0.10 in the same period last year. Net income fell sharply to $13.7 million from $60.4 million in Q2 2024, reflecting challenging conditions across its regulated utility businesses.

Despite the disappointing quarterly results, MDU Resources maintained its focus on long-term growth initiatives, particularly highlighting its data center strategy and renewable energy investments as key drivers for future performance.

Quarterly Performance Highlights

MDU Resources’ second quarter results showed declines across all three of its main business segments compared to the previous year.

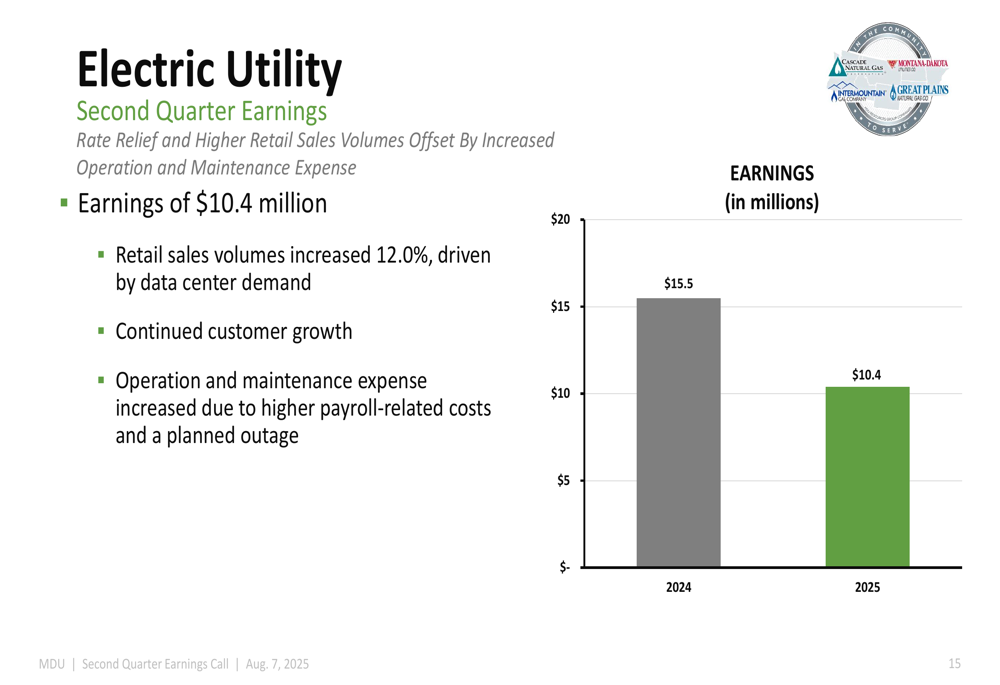

The Electric Utility segment posted earnings of $10.4 million, down from $15.5 million in Q2 2024. The company noted that while retail sales volumes increased 12.0% driven by data center demand and continued customer growth, these gains were offset by higher operation and maintenance expenses, including payroll-related costs and a planned outage.

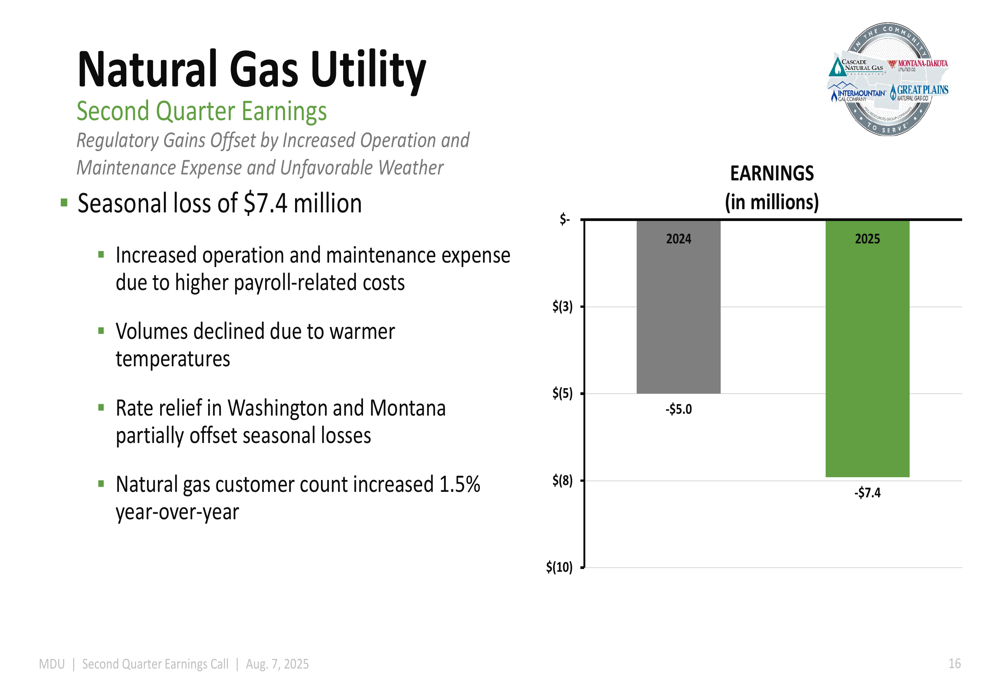

The Natural Gas Utility segment reported a seasonal loss of $7.4 million, deeper than the $5.0 million loss recorded in the same period last year. The company attributed this decline to increased operation and maintenance expenses and unfavorable weather conditions, which were partially offset by rate relief in Washington and Montana. On a positive note, the natural gas customer count increased 1.5% year-over-year.

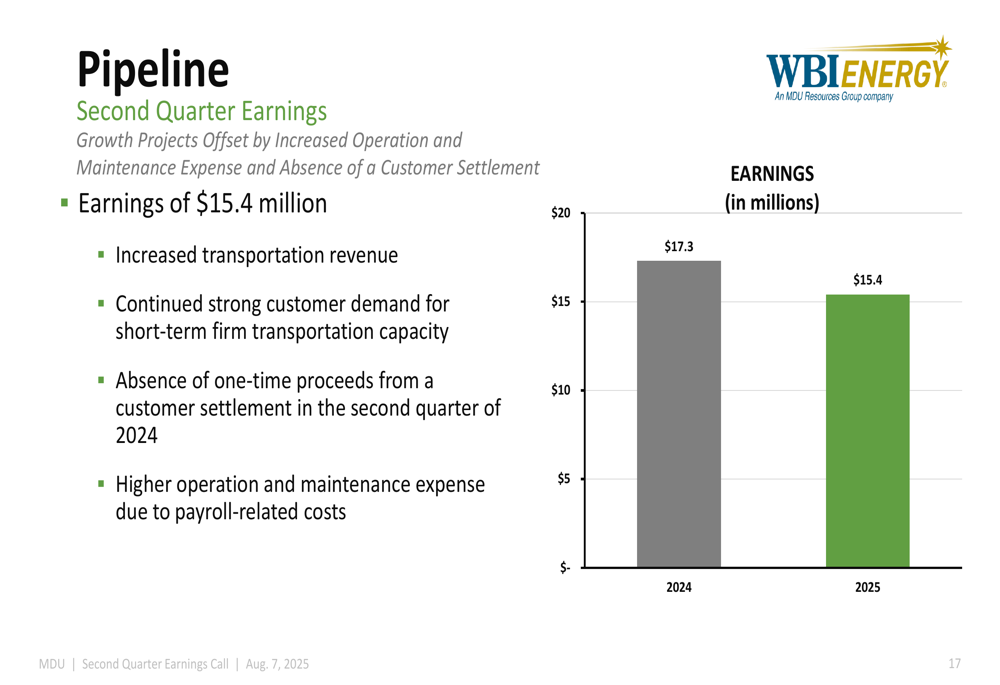

The Pipeline segment earned $15.4 million, down from $17.3 million in Q2 2024. While the company saw increased transportation revenue and strong customer demand for short-term firm transportation capacity, these gains were offset by higher operation and maintenance expenses and the absence of one-time proceeds from a customer settlement that had benefited the second quarter of 2024.

Strategic Initiatives

Despite the earnings pressure, MDU Resources continues to position itself as a pure-play regulated energy delivery business with several strategic growth initiatives underway. The company’s presentation emphasized its "CORE" strategy focused on Customers & Communities, Operational Excellence, Returns Focused, and Employee Driven approaches.

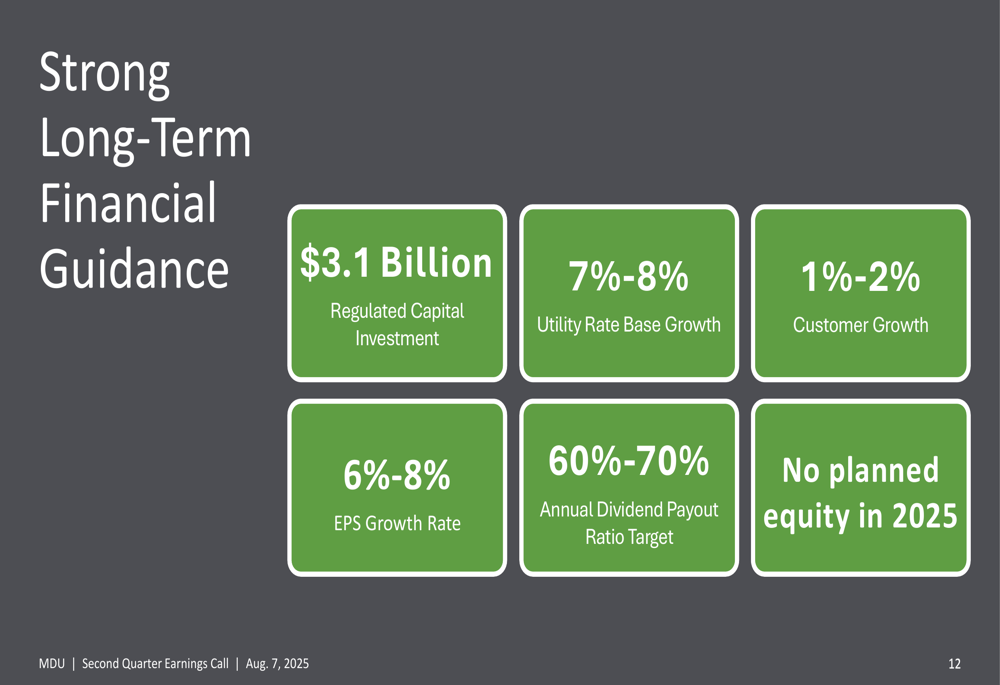

As shown in the following investment highlights, MDU is targeting a 6%-8% long-term EPS growth rate and a 60%-70% annual dividend payout ratio:

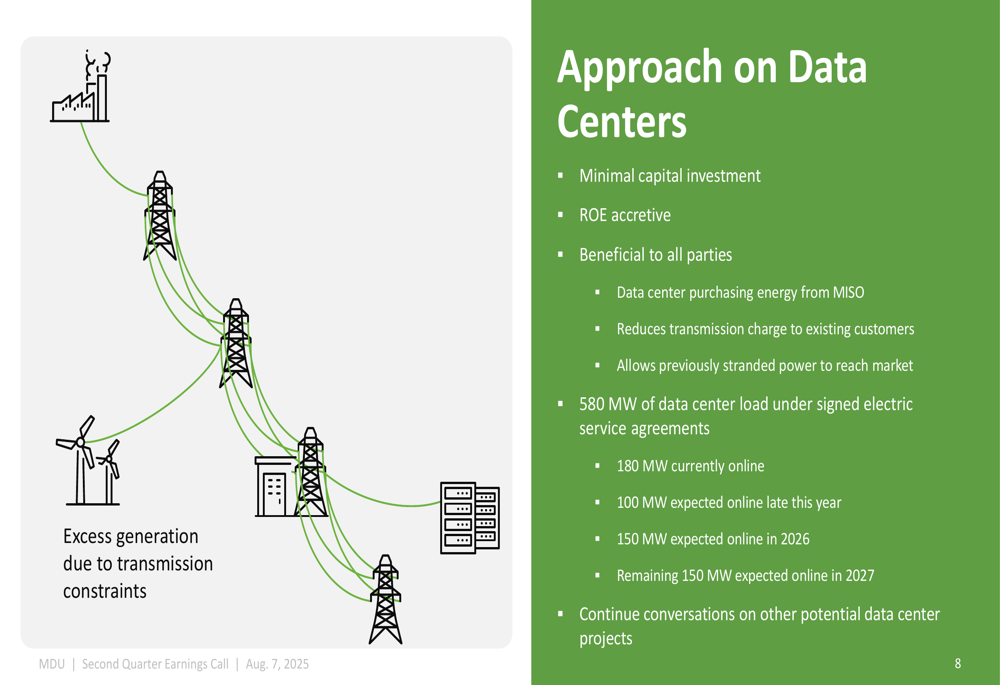

A significant focus of MDU’s growth strategy is its expanding data center business. The company has secured 580 MW of data center load under signed electric service agreements, with 180 MW currently online, 100 MW expected online later this year, 150 MW in 2026, and the remaining 150 MW in 2027. The company’s approach emphasizes minimal capital investment while providing ROE-accretive opportunities.

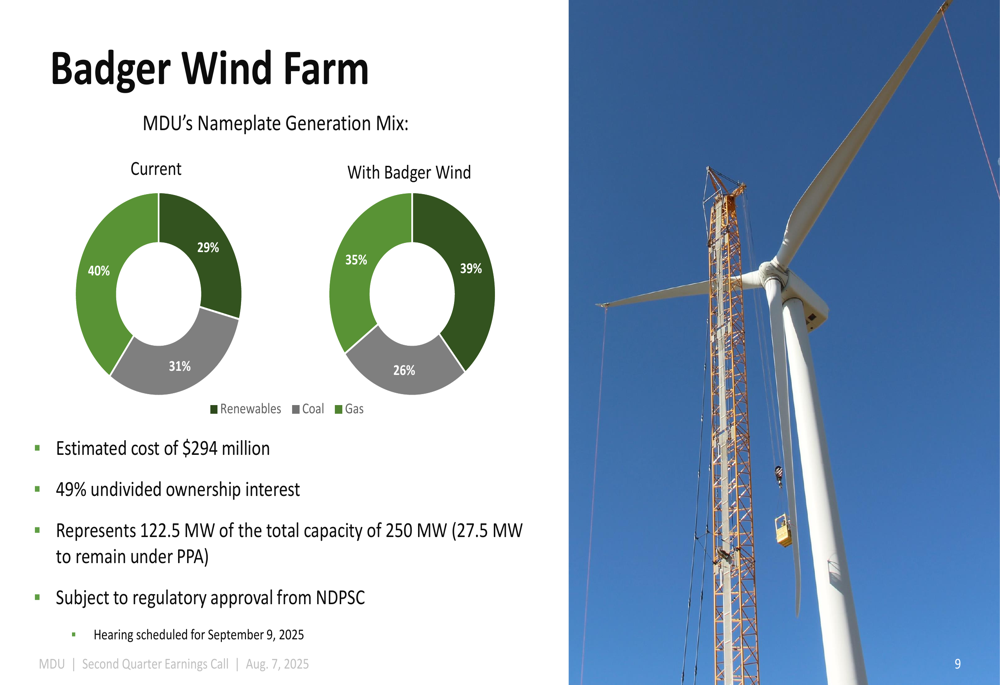

MDU is also advancing its renewable energy portfolio through the Badger Wind Farm project, which represents a 49% undivided ownership interest at an estimated cost of $294 million. This project will add 122.5 MW of capacity to MDU’s generation mix, subject to regulatory approval from the North Dakota Public Service Commission, with a hearing scheduled for September 9, 2025.

Forward-Looking Statements

In light of its year-to-date performance, MDU Resources narrowed its 2025 earnings guidance to $0.88-$0.95 per share, compared to the previous range of $0.88-$0.98 mentioned in the Q1 earnings report. This guidance assumes normal weather, economic, and operating conditions for the remainder of the year, along with continued customer growth of 1%-2% annually.

Despite the narrowed near-term outlook, MDU maintained its strong long-term financial guidance, highlighting plans for $3.1 billion in regulated capital investment, 7%-8% utility rate base growth, and 6%-8% EPS growth. The company also reiterated its 60%-70% annual dividend payout ratio target and confirmed no planned equity issuances in 2025.

Competitive Industry Position

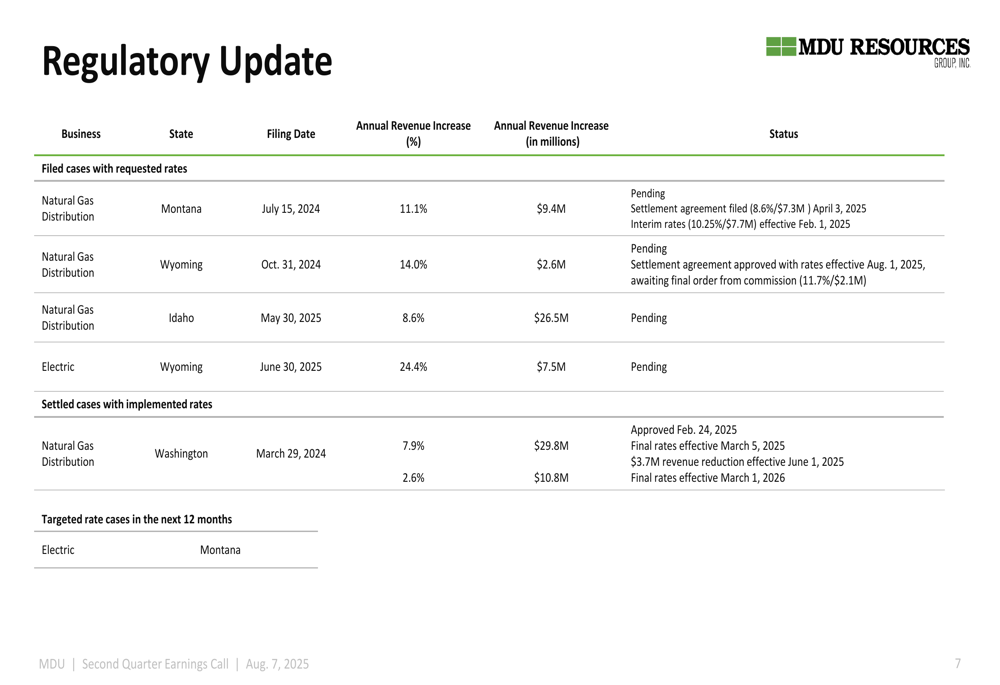

MDU Resources continues to emphasize its position as a pure-play regulated energy delivery business operating in a supportive regulatory environment. The company’s presentation detailed several rate cases in various stages across its service territories.

The regulatory update showed pending rate cases in Montana, Wyoming, and Idaho, with requested increases ranging from 8.6% to 24.4%. The company has already secured settlements in some jurisdictions, including a recently approved settlement in Wyoming for natural gas distribution with an 11.7% increase effective August 1, 2025.

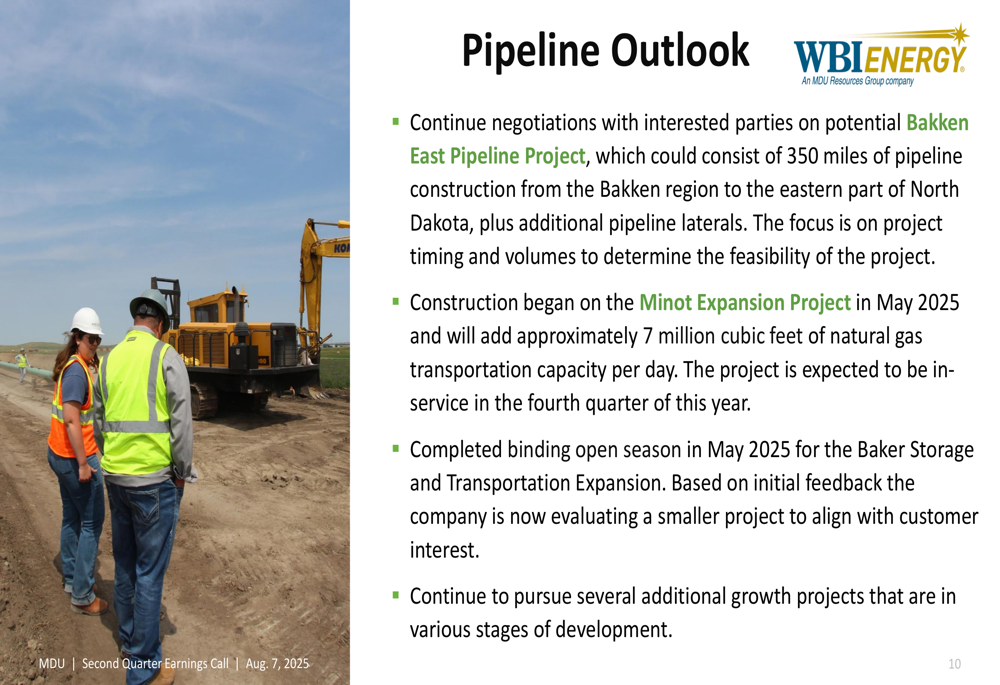

In the pipeline business, MDU continues to pursue growth through several projects, including ongoing negotiations for the potential Bakken East Pipeline Project, which could consist of 350 miles of pipeline construction. The company has also begun construction on the Minot Expansion Project, which will add approximately 7 million cubic feet of natural gas transportation capacity per day when completed in Q4 2025.

While MDU Resources faces near-term challenges as evidenced by its Q2 results and stock performance, the company’s presentation emphasized its long-term strategic positioning in regulated utilities with specific growth opportunities in data centers and renewable energy projects. Investors will be watching closely to see if these initiatives can reverse the current earnings trend and deliver on the company’s long-term growth targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.