Fiserv earnings missed by $0.61, revenue fell short of estimates

Introduction & Market Context

MedAdvisor Limited (ASX:MDR) presented its fourth quarter fiscal year 2025 results on July 31, 2025, revealing a significant strategic pivot with the completed divestment of its Australia and New Zealand operations amid challenging performance in its US business. The company’s stock closed at $0.079, up 2.6% on the day, as investors digested the mixed results and strategic changes.

The presentation, delivered by Managing Director and CEO Rick Ratliff alongside incoming CFO Sean Slattery, highlighted the contrasting performance between MedAdvisor’s geographic segments and outlined the company’s path forward as a potentially US-focused operation.

Quarterly Performance Highlights

MedAdvisor reported group revenue of $18.6 million for Q4 FY25, representing a 16.6% decline compared to the same period last year. Group gross profit fell more sharply, down 28.4% to $11.1 million, with gross margin contracting by 9.8 percentage points to 59.7%.

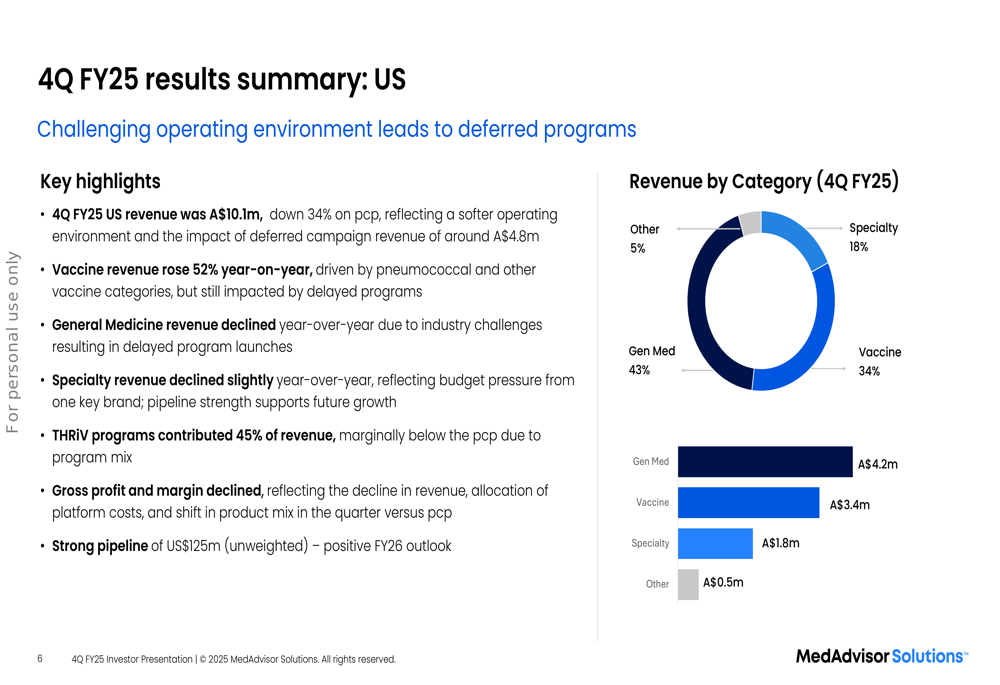

The performance diverged significantly between regions. The US business faced substantial headwinds, with revenue dropping 34% to $10.1 million and gross profit plummeting 54.2% to $4.3 million. US gross margin contracted significantly to 42.6%, down 18.5 percentage points.

As shown in the following breakdown of US revenue by category:

In contrast, the ANZ business demonstrated strong growth in its final quarter under MedAdvisor ownership, with revenue increasing 21.4% to $8.5 million and gross profit rising 16.1% to $7.2 million. The ANZ segment maintained a robust gross margin of 84.7%, though this represented a 3.9 percentage point decline.

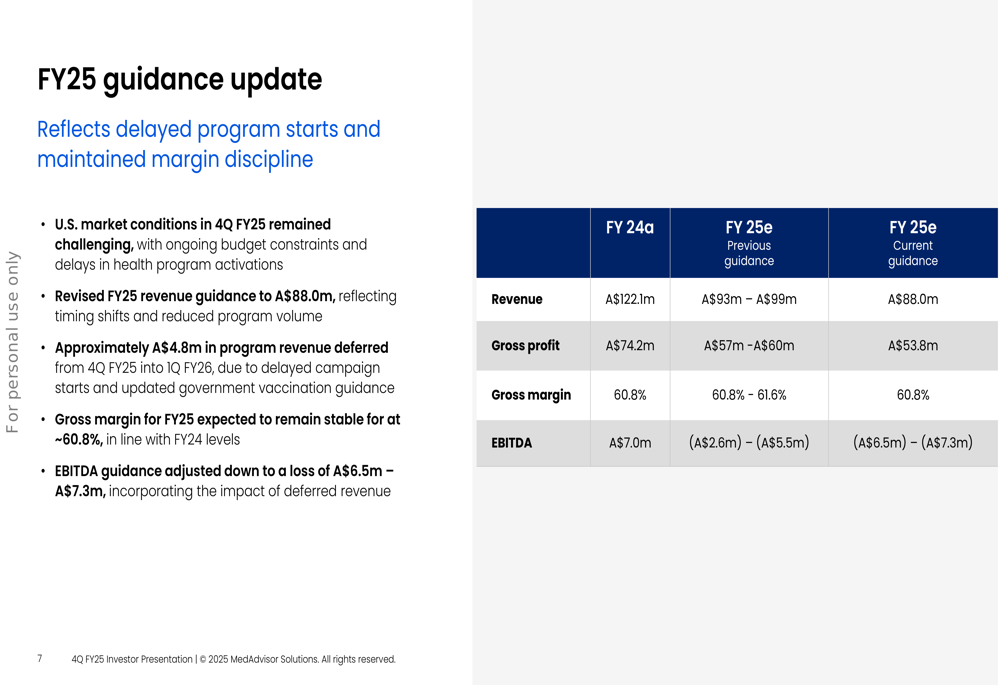

The company also updated its full-year FY25 guidance, reflecting the challenging market conditions and delayed program starts:

Strategic Initiatives

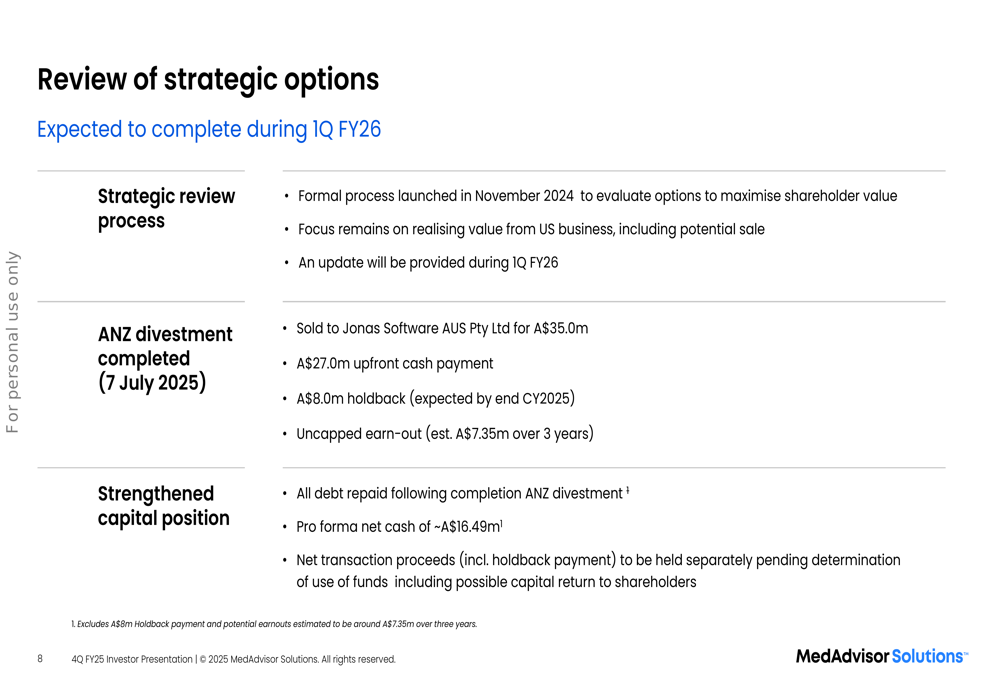

The most significant development in the quarter was the completed sale of MedAdvisor’s ANZ business operations to Jonas Software (ETR:SOWGn) AUS Pty Ltd for A$35.0 million, plus potential earn-outs estimated at A$7.35 million over three years. The transaction, which closed on July 7, 2025, included an upfront cash payment of A$27.0 million with an A$8.0 million holdback expected by the end of calendar year 2025.

"The ANZ divestment represents a significant milestone in our strategic evolution," said Rick Ratliff, CEO and Managing Director. "It provides us with a strengthened balance sheet and the flexibility to consider various options for our US operations."

Following the ANZ sale, MedAdvisor reported a pro forma net cash position of approximately A$16.49 million. The company indicated that net transaction proceeds will be held separately pending determination of use of funds, including a possible capital return to shareholders.

The company has also launched a formal strategic options review for its US business, expected to complete during Q1 FY26:

US Market Dynamics and Business Initiatives

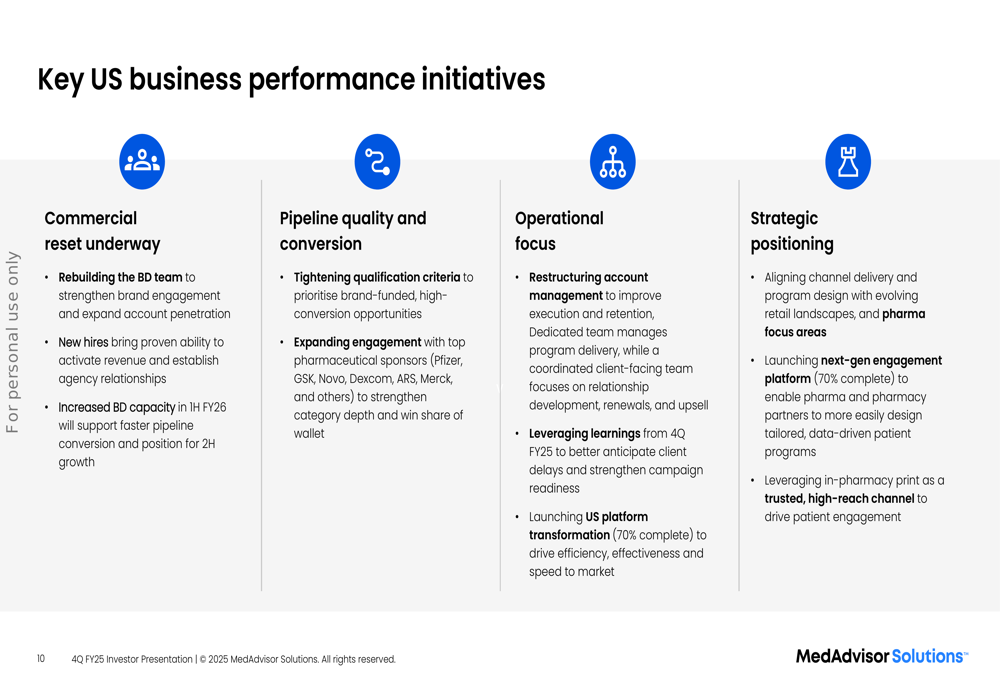

MedAdvisor identified several market trends reshaping the US pharmacy and pharmaceutical landscape that have contributed to its challenging performance. These include health program budget pressures, a shift to direct-to-consumer models, channel fragmentation, and competitive threats from digital entrants.

The company outlined the following key initiatives to address these challenges:

Despite the recent performance challenges, MedAdvisor reported that its THRIV-powered programs now contribute 45% of US revenue, and vaccine programs have shown strong growth, up 52% year-on-year. However, general medicine and specialty medication revenues declined, contributing to the overall revenue drop.

Forward-Looking Statements

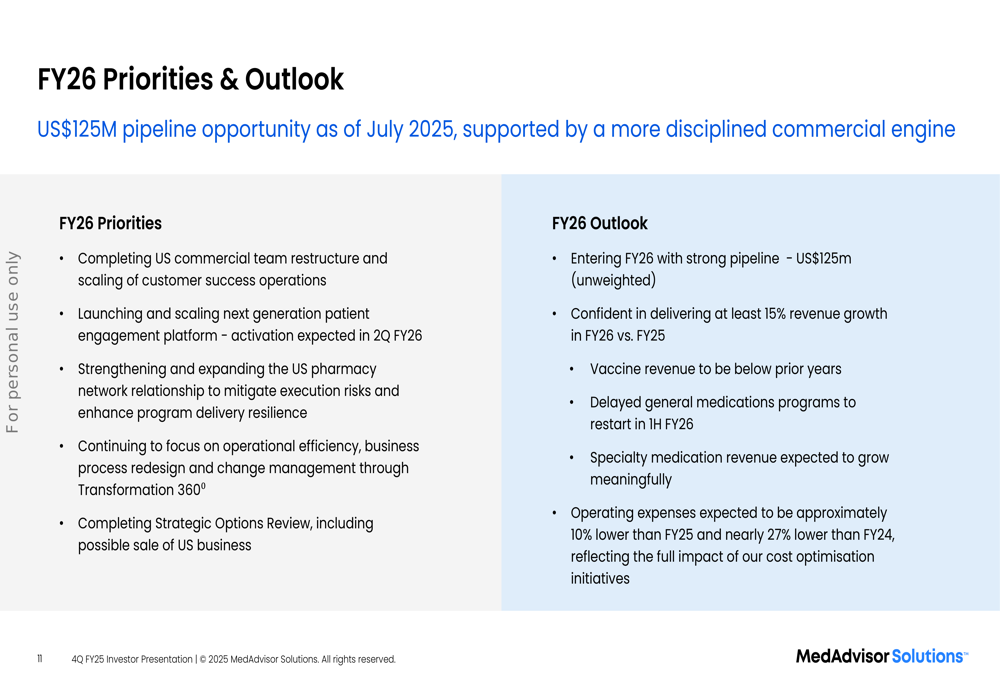

Looking ahead to FY26, MedAdvisor expressed confidence in its growth prospects despite recent challenges. The company reported entering the new fiscal year with a strong pipeline of US$125 million (unweighted) and forecasted at least 15% revenue growth in FY26 compared to FY25.

Management expects operating expenses to be approximately 10% lower than FY25 and nearly 27% lower than FY24, reflecting ongoing cost-cutting measures. The company also anticipates meaningful growth in specialty medication revenue and the restart of delayed general medications programs in the first half of FY26.

Financial Analysis

MedAdvisor’s Q4 FY25 results reflect a company in transition. The strong performance of the now-divested ANZ business contrasts sharply with the challenges in the US operations, which now represent the company’s sole focus.

The revised FY25 guidance indicates a significant downgrade from previous expectations, with revenue now projected at A$88.0 million compared to the previous range of A$93-99 million. The EBITDA loss is now expected to be A$6.5-7.3 million, deeper than the previously guided range of A$2.6-5.5 million.

Notably, approximately A$4.8 million in program revenue was deferred from Q4 FY25 into Q1 FY26, which partially explains the revenue shortfall. The company maintained its gross margin guidance at 60.8%, suggesting that pricing discipline remains intact despite volume challenges.

The company’s strategic pivot comes amid challenging market conditions in the US healthcare sector. Major pharmacy chains are closing stores, with Rite Aid (NYSE:US90274J5618=UBSS)’s bankruptcy highlighting the pressures facing traditional pharmacy models. Meanwhile, regulatory changes to vaccine coverage and market uncertainty are affecting vaccine uptake, though MedAdvisor reported 52% growth in its vaccine revenue.

As MedAdvisor completes its strategic options review in the coming months, investors will be watching closely to see whether the company can successfully reposition its US business for sustainable growth or whether a sale of this business segment might be the ultimate outcome.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.