Capstone Holding Corp. lowers convertible note conversion price to $1.00

Introduction & Market Context

MediaAlpha Inc (NYSE:MAX) showcased impressive growth in its Q1 2025 investor presentation, highlighting a significant rebound in its property and casualty (P&C) insurance segment. The company, which operates one of the largest online customer acquisition platforms for insurance, has benefited from improving conditions in the auto insurance market as carriers return to profitability and increase their marketing investments.

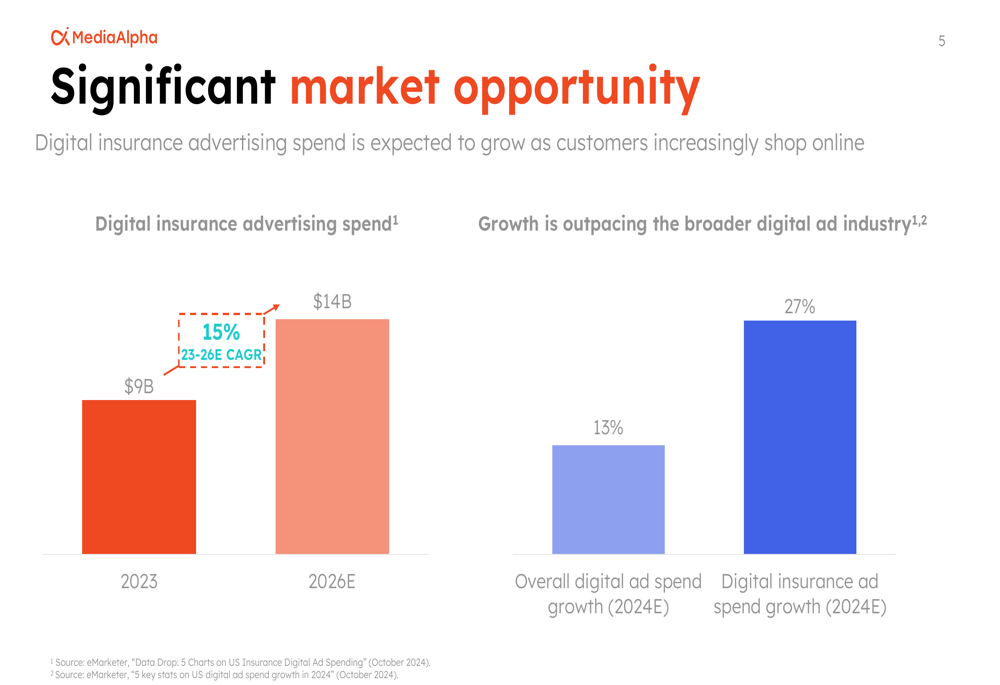

According to the presentation, digital insurance advertising spend is projected to grow from $9 billion in 2023 to $14 billion by 2026, representing a 15% compound annual growth rate. This growth rate significantly outpaces the overall digital advertising market, which is expected to grow at 13% in 2024.

As shown in the following chart of the digital insurance advertising market opportunity:

The company operates a two-sided marketplace connecting insurance carriers with online shoppers, focusing primarily on property & casualty, health, and life insurance verticals. With over 400 supply partners and 700 demand partners as of fiscal year 2024, MediaAlpha has established a strong position in the insurance customer acquisition space.

Quarterly Performance Highlights

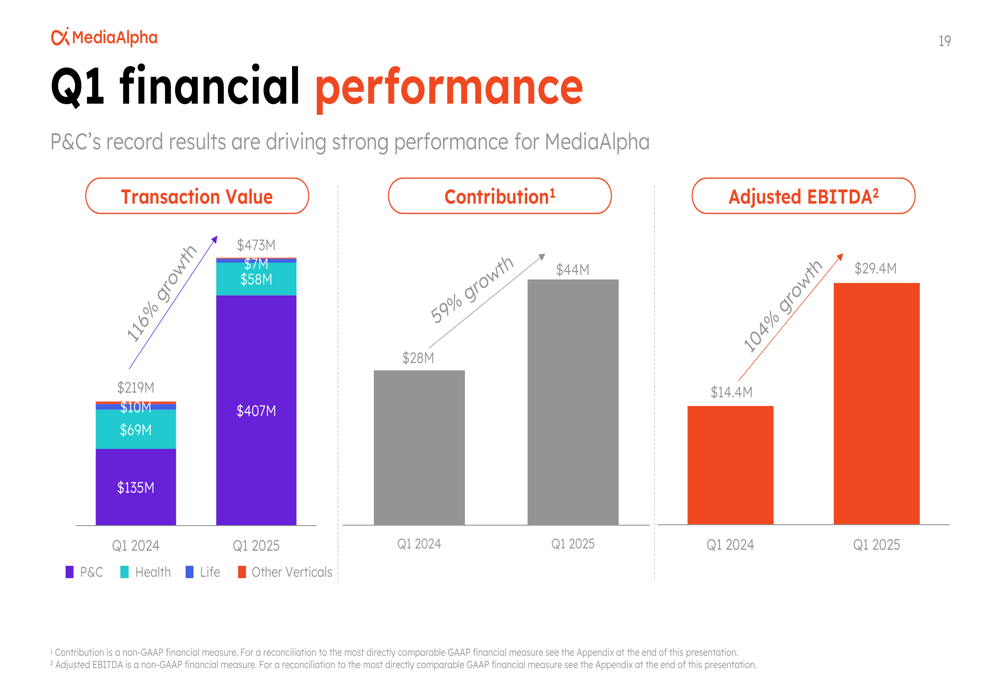

MediaAlpha reported exceptional results for Q1 2025, with transaction value reaching $473 million, representing a 116% year-over-year increase. This growth was primarily driven by the P&C segment, which grew by 200% compared to Q1 2024. The company’s adjusted EBITDA doubled year-over-year to $29.4 million.

The following slide illustrates the company’s Q1 2025 financial performance across key metrics:

The strong performance in P&C offset a 17% decline in the health segment, resulting in overall robust growth. Contribution, defined as revenue less revenue share payments and online advertising costs, increased by 59% year-over-year to $44 million in Q1 2025.

After the earnings release on April 30, 2025, MediaAlpha’s stock initially fell 4% during regular trading hours to close at $8.75, but rebounded 10.26% in aftermarket trading to $9.26, reflecting investor optimism about the company’s growth trajectory.

Detailed Financial Analysis

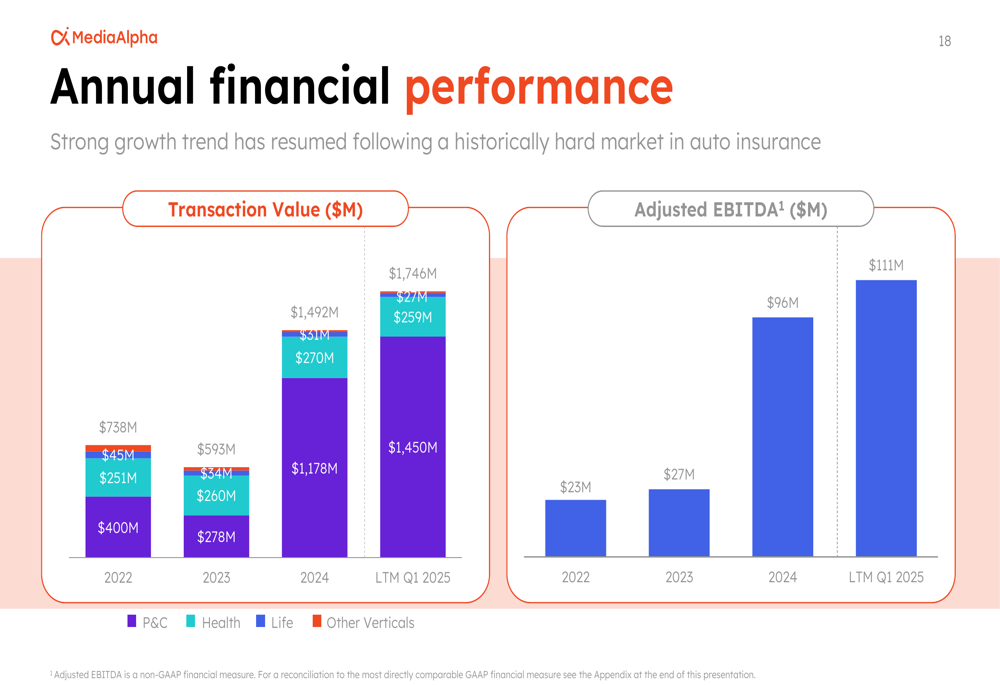

MediaAlpha’s financial recovery has been impressive following a challenging period in 2023. The company’s annual transaction value declined from $738 million in 2022 to $593 million in 2023 during what it described as a "historically hard market in auto insurance," but rebounded strongly to $1.49 billion in 2024. For the twelve months ended March 31, 2025, transaction value reached $1.75 billion.

The following chart shows the company’s annual financial performance:

Adjusted EBITDA has shown similar growth, increasing from $27 million in 2023 to $96 million in 2024, and reaching $111 million for the twelve months ended March 31, 2025. This represents a significant improvement in profitability as the company scales.

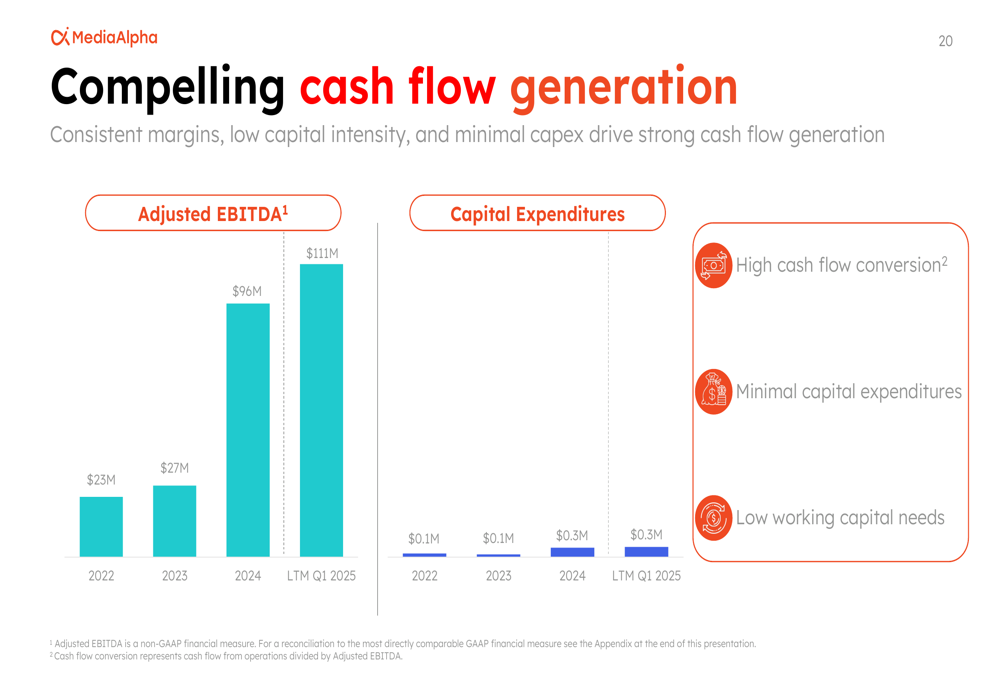

MediaAlpha’s business model is characterized by low capital intensity and strong cash flow generation. For the twelve months ended March 31, 2025, capital expenditures were just $0.3 million, representing less than 0.3% of adjusted EBITDA.

The following slide highlights the company’s cash flow generation capabilities:

Strategic Initiatives & Growth Drivers

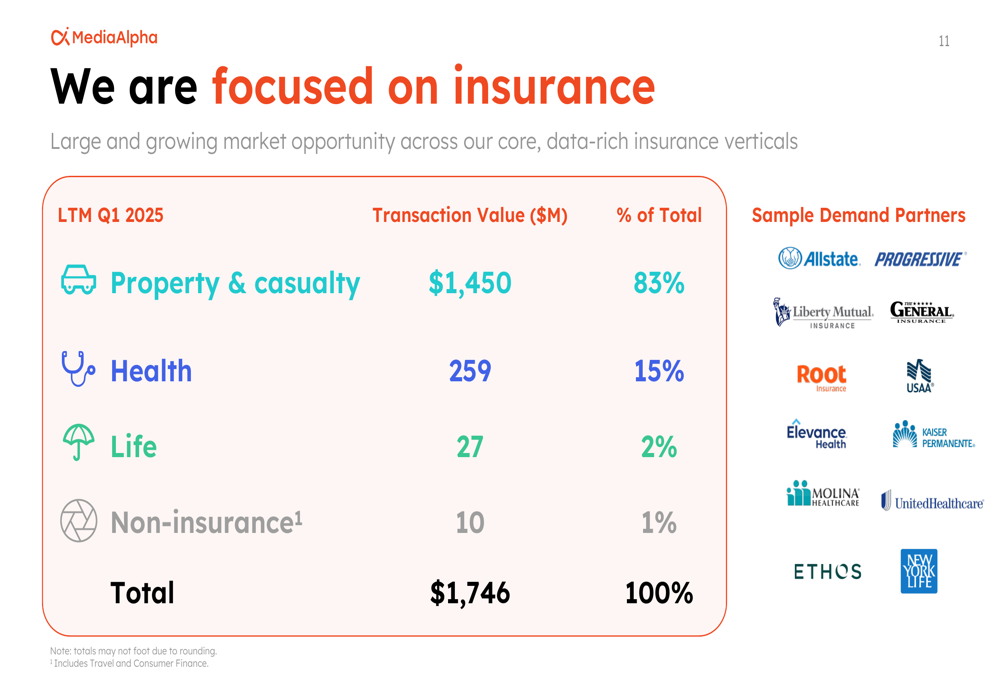

MediaAlpha’s business is heavily concentrated in the insurance sector, with 83% of transaction value coming from property & casualty, 15% from health, 2% from life, and 1% from non-insurance verticals. This focus allows the company to develop deep expertise and relationships within the insurance industry.

The following breakdown illustrates the company’s concentration in insurance verticals:

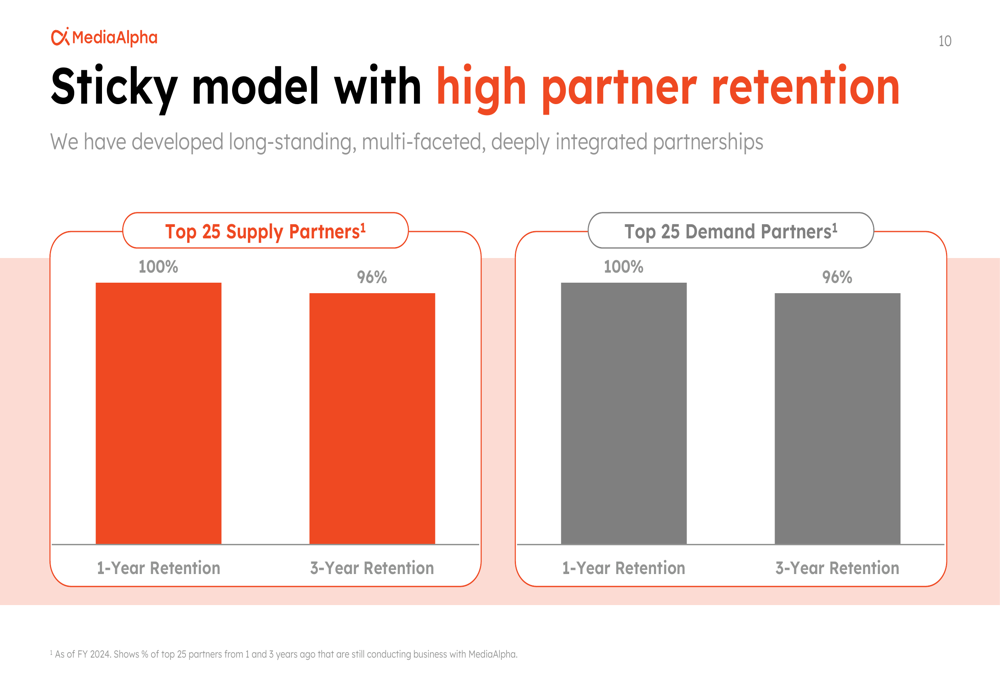

A key strength of MediaAlpha’s business model is its high partner retention rates. The company reported that 100% of its top 25 supply and demand partners from one year ago are still conducting business with MediaAlpha, and 96% of partners from three years ago remain active. This stickiness reflects the value proposition of MediaAlpha’s platform and the deep integration with partners’ systems.

The following slide demonstrates the company’s strong partner retention:

MediaAlpha’s platform enables insurance carriers to target consumers with remarkable precision. The company’s technology allows for automated, micro-level, real-time bidding based on numerous consumer attributes, helping carriers optimize their customer acquisition efforts.

Forward-Looking Statements

Looking ahead, MediaAlpha expects continued strong performance in Q2 2025, with transaction value projected between $470 million and $495 million, representing approximately 50% year-over-year growth at the midpoint. Revenue is expected to range from $235 million to $255 million, with adjusted EBITDA between $25 million and $27 million.

The company sees several long-term growth drivers, including capitalizing on secular trends in online insurance shopping, extending market leadership through network effects, gaining wallet share with existing demand partners, and bringing on new supply partners.

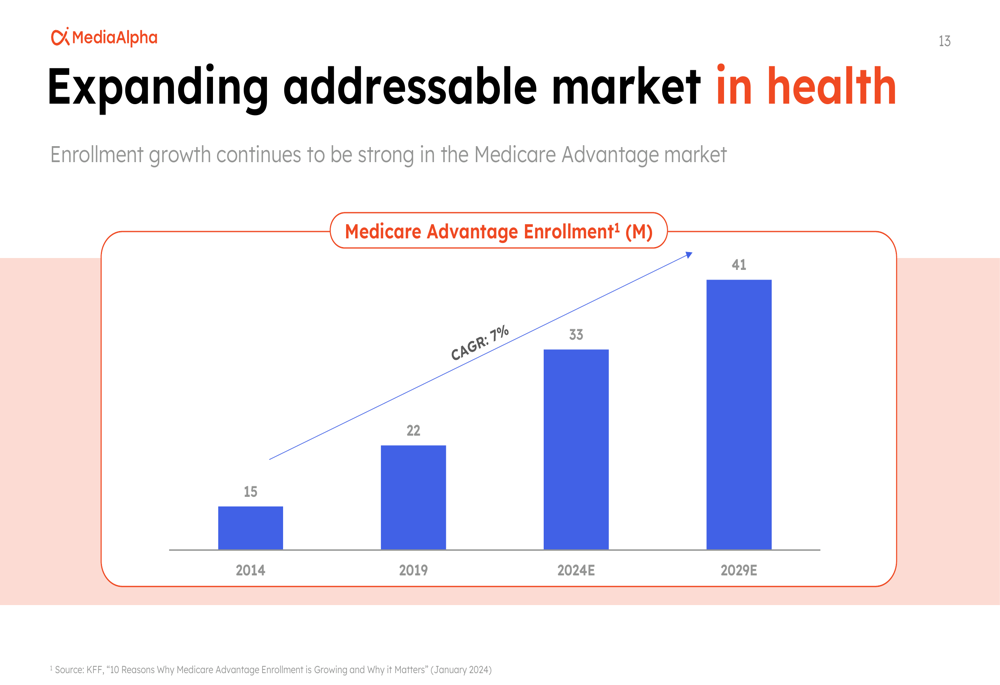

While the P&C segment is showing robust growth, MediaAlpha also sees opportunity in the Medicare Advantage market, where enrollment is projected to grow from 33 million in 2024 to 41 million by 2029, representing a 7% CAGR.

The following chart illustrates the growth potential in the Medicare Advantage market:

During the earnings call, executives noted some challenges, including regulatory matters with the FTC and potential impacts from automotive tariffs expected in the second half of 2025. The company also mentioned scaling back its under-65 health business, which may explain the decline in health segment transaction value.

Despite these challenges, MediaAlpha’s Q1 2025 presentation paints a picture of a company with strong growth momentum, an efficient business model, and significant opportunities in the expanding digital insurance advertising market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.