Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

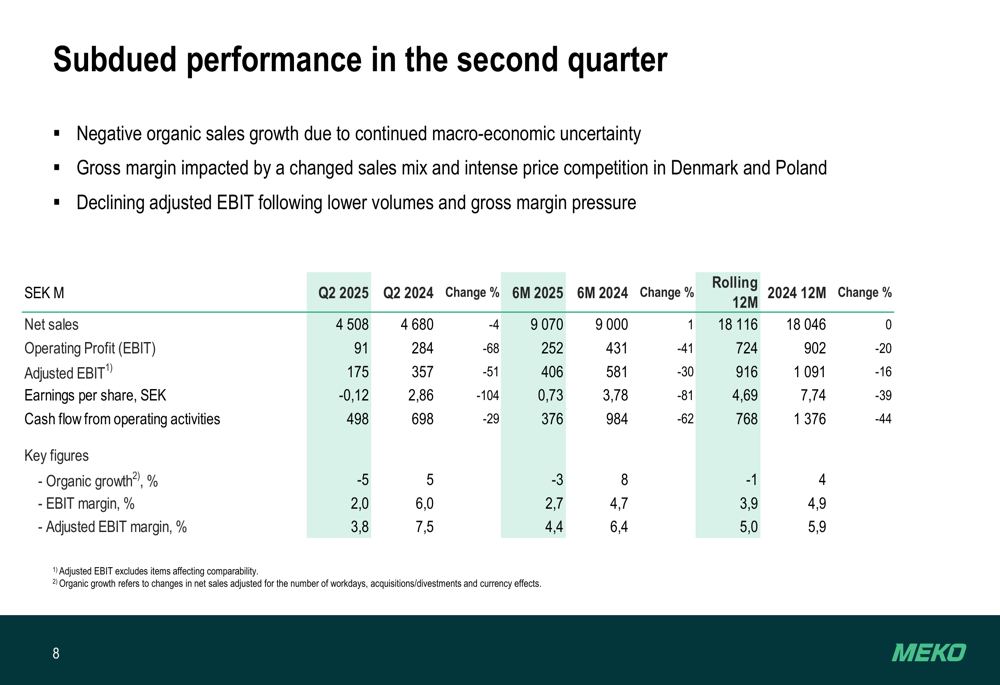

Mekonomen AB (STO:MEKO), a leading player in the Northern European automotive aftermarket, presented its Q2 2025 results on July 25, revealing a significant decline in profitability amid challenging market conditions. The company’s stock closed at 112.6 SEK on the day of the presentation, up 0.72% despite the underwhelming results.

The second quarter marked a substantial deterioration from Q1 2025, when the company had reported a 6% increase in net sales. The latest presentation highlighted subdued demand and intense price competition across multiple markets, forcing the company to implement additional efficiency measures.

Quarterly Performance Highlights

Mekonomen reported a 4% decrease in net sales to 4,508 MSEK for Q2 2025, compared to 4,680 MSEK in the same period last year. Organic growth turned sharply negative at -5%, worsening from the -1% reported in Q1 2025.

The company’s profitability suffered significantly, with adjusted EBIT plummeting 51% to 175 MSEK (versus 357 MSEK in Q2 2024). This resulted in an adjusted EBIT margin of just 3.8%, down from 7.5% a year earlier. Earnings per share turned negative at -0.12 SEK, compared to 2.86 SEK in Q2 2024.

As shown in the following comprehensive financial overview:

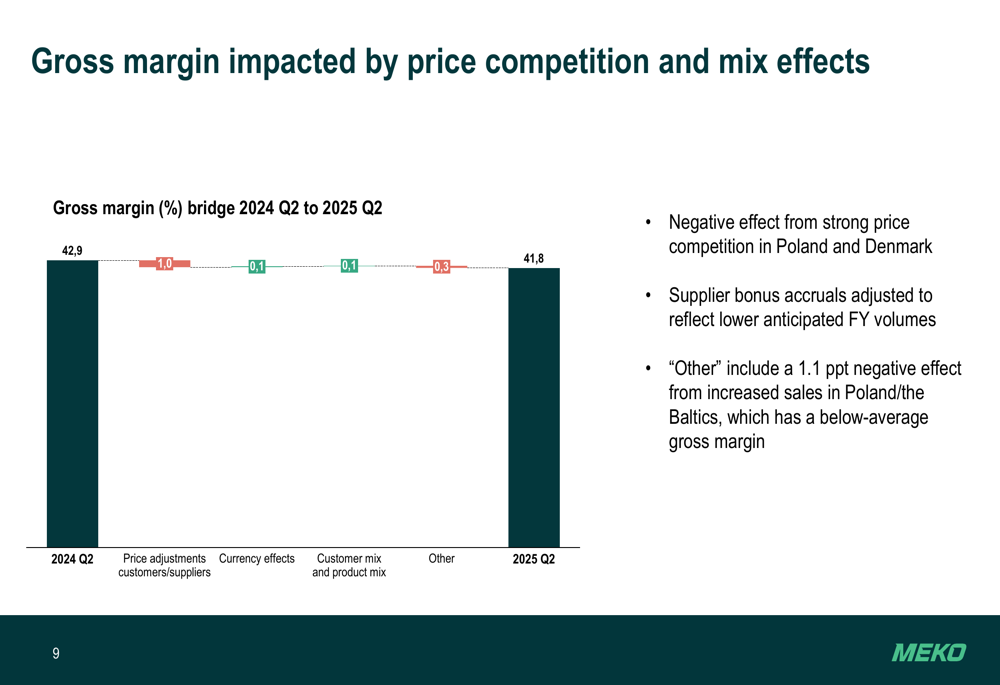

Gross margin declined to 41.8% from 42.9% in Q2 2024, primarily due to price competition and unfavorable sales mix. The following chart breaks down the factors affecting gross margin:

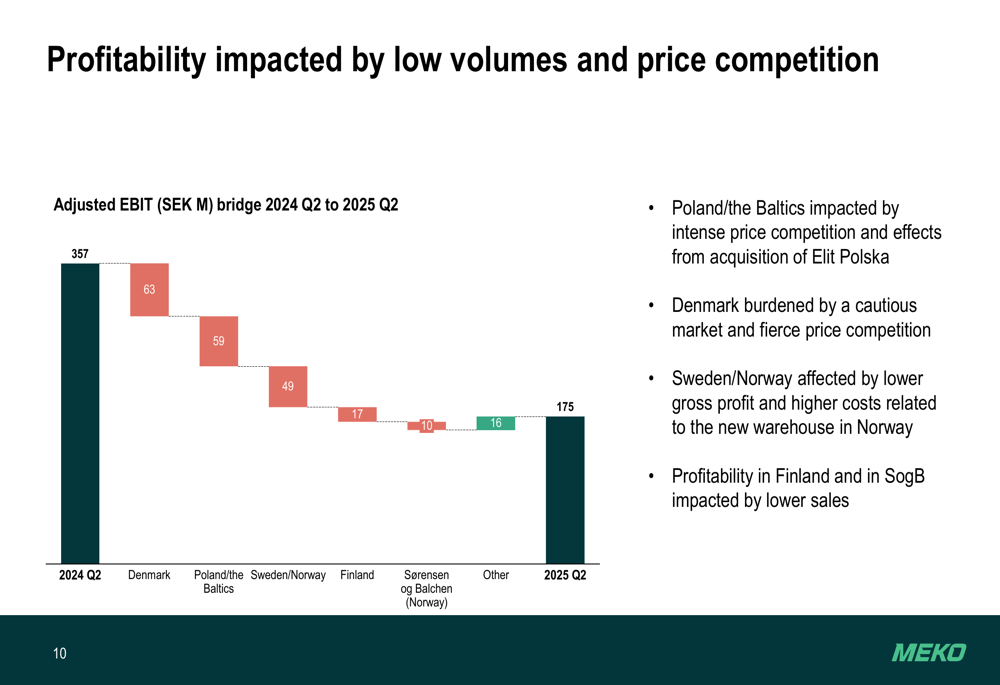

The company’s profitability was impacted differently across regions, with the most significant EBIT declines in Denmark (-63 MSEK), Poland/Baltics (-59 MSEK), and Sweden/Norway (-49 MSEK), as illustrated in this bridge analysis:

Detailed Financial Analysis

Regional performance varied significantly across Mekonomen’s markets:

Denmark (22% of net sales): Reported a 14% decrease in net sales, with organic growth at -8%. Adjusted EBIT fell by 68% to 30 MSEK, with margin dropping to 2.9% from 7.9%. The decline was attributed to strong competition, subdued demand, and higher depreciation related to the new warehouse.

Poland/Baltics (28% of net sales): Despite a 24% increase in reported net sales, adjusted EBIT turned negative at -23 MSEK, down 164% from the previous year. This region was particularly affected by intense price competition and integration costs from the Elit Polska acquisition.

Sweden/Norway (37% of net sales): Reported a 9% decrease in net sales with organic growth at -6%. Adjusted EBIT declined by 23% to 163 MSEK, though this region maintained the highest EBIT margin at 9.6%.

Finland (8% of net sales): Reported a 13% decrease in net sales with organic growth at -7%. Adjusted EBIT turned negative at -14 MSEK, impacted by lower gross margin and temporary higher warehouse and IT costs.

Sørensen og Balchen (6% of net sales): Despite a 10% decrease in net sales, this business unit maintained the highest profitability with an adjusted EBIT margin of 18.1%, though down from 19.8% in Q2 2024.

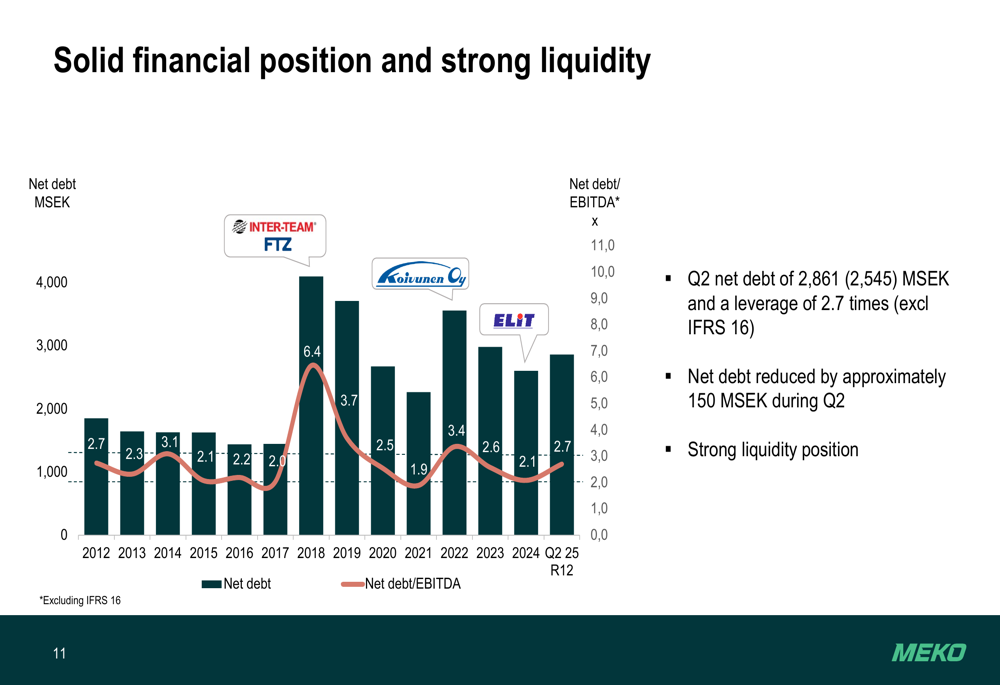

The company maintained a solid financial position with net debt of 2,861 MSEK and a leverage ratio of 2.7x (excluding IFRS 16), as shown in the following debt trend:

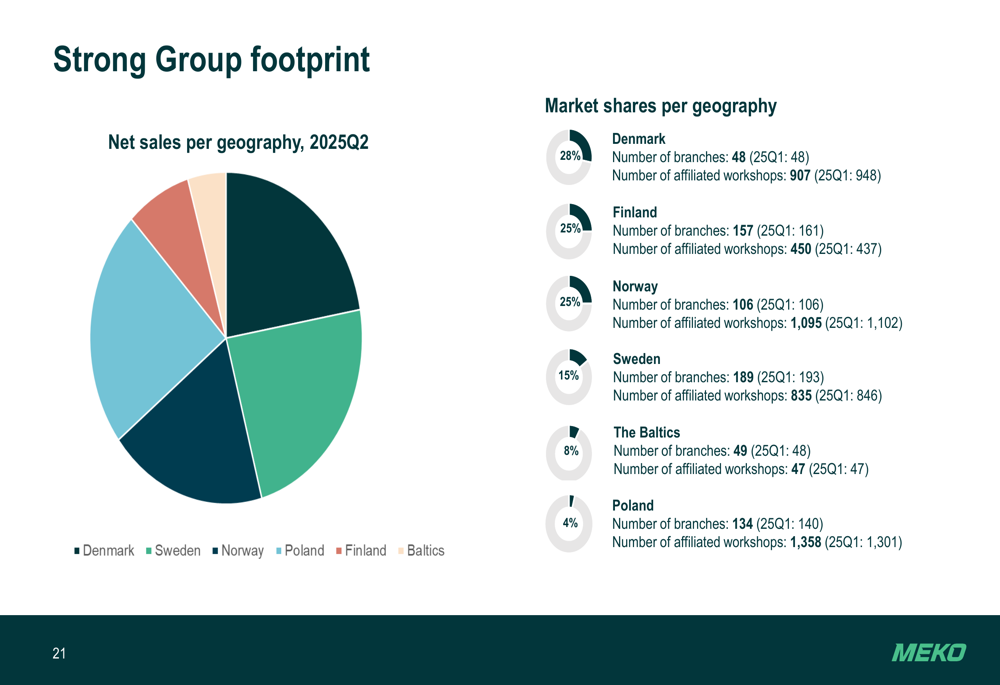

Mekonomen’s geographic footprint remains strong across Northern Europe, with a balanced distribution of branches and affiliated workshops:

Strategic Initiatives

In response to the challenging market conditions, Mekonomen is implementing several strategic initiatives:

1. Cost reduction program targeting 100 MSEK in annual savings, including consolidation of branch networks and organizational simplification.

2. Completion of strategic logistics upgrades, with the new warehouse in Norway going live in Q2 and expected to be fully operational in Q3 2025.

3. Reinforced focus on exclusive brands, expanding product ranges from premium to affordable segments under brands like ProMeister and carwise.

4. Implementation of a common ERP system, launched first in Poland.

5. Successful bond issue of SEK 1.25 billion to manage debt maturity profile, with a five-year tenor and floating interest rate of 3-month STIBOR plus 215 basis points.

The company’s long-term financial targets remain unchanged, as outlined below:

Forward-Looking Statements

Mekonomen expects the cautious market conditions to persist in the near term but anticipates that its efficiency measures will gradually improve profitability. The company remains committed to its sustainability strategy, with climate targets approved by the Science Based Targets initiative.

Management emphasized that significant benefits from the ongoing efficiency program are still to be realized, with an EBIT improvement of approximately 200 MSEK achieved to date. The additional 100 MSEK cost reduction target is specifically designed to adapt to current market headwinds.

The company’s strategic logistics upgrades are expected to deliver substantial operational improvements once fully implemented, though they are currently causing temporary cost increases, particularly in Norway and Finland.

Looking ahead, Mekonomen’s focus on exclusive brands and supplier optimization is intended to strengthen gross margins, which have been under pressure due to intense price competition, particularly in Poland and Denmark. The company’s tagline, "We enable mobility - today, tomorrow and in the future," underscores its commitment to long-term market leadership despite current challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.