Street Calls of the Week

Introduction & Market Context

Merck & Co. (NYSE:MRK) presented its second-quarter 2025 financial results on July 29, highlighting a mixed performance with total worldwide sales of $15.8 billion, representing a 2% decrease compared to the same period last year. The pharmaceutical giant’s stock rose slightly in premarket trading, up 0.12% to $89.30, reflecting cautious optimism about the company’s strategic direction despite revenue challenges.

The quarter’s performance was significantly impacted by a sharp decline in GARDASIL sales in China, though this was partially offset by strong growth in the company’s oncology portfolio, particularly KEYTRUDA, and its Animal Health segment. Excluding GARDASIL sales in China, Merck’s worldwide sales increased by 7%, demonstrating underlying strength across other business areas.

"We have over 20 new and potential future growth drivers," emphasized CEO Rob Davis during the presentation, highlighting the company’s focus on innovation and pipeline development to sustain long-term growth.

Quarterly Performance Highlights

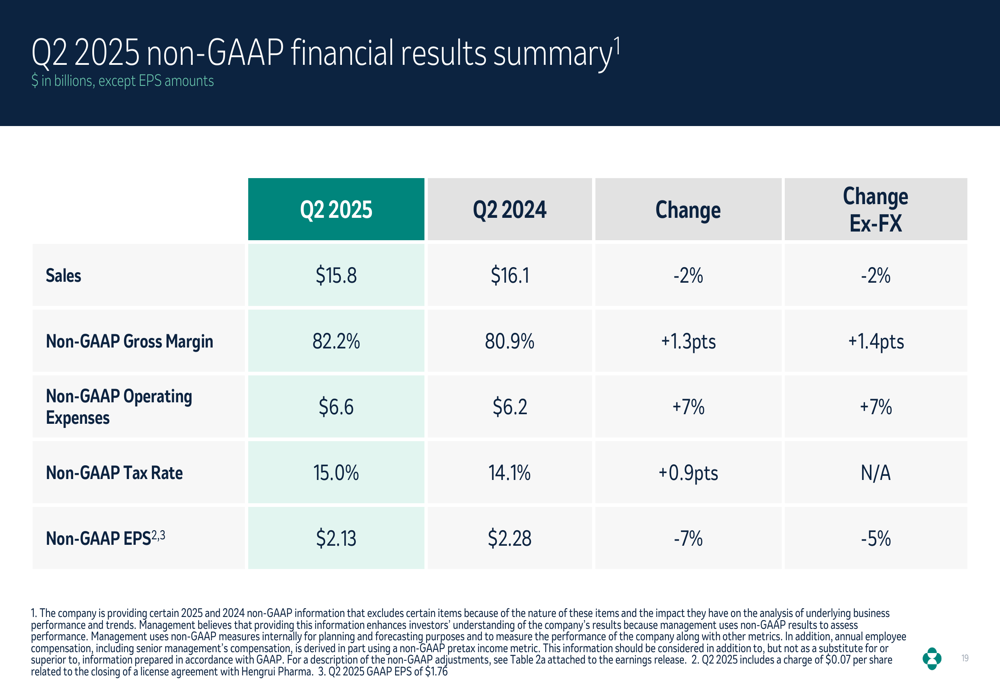

Merck reported Q2 2025 worldwide sales of $15.8 billion, down 2% both nominally and excluding foreign exchange impacts. Non-GAAP earnings per share reached $2.13, including a $0.07 per share charge related to a licensing agreement with Hengrui Pharma.

The company’s Human Health segment generated $14.1 billion in sales, a decrease of 2% nominally and 3% excluding foreign exchange impacts. In contrast, the Animal Health business showed robust performance with sales of $1.6 billion, representing an 11% increase both nominally and excluding foreign exchange effects.

As shown in the following financial results summary:

The company maintained a strong non-GAAP gross margin of 82.2%, reflecting efficient production and favorable product mix. Operating expenses totaled $6.6 billion on a non-GAAP basis, while the company reported a non-GAAP tax rate of 15.0%.

Product Portfolio Performance

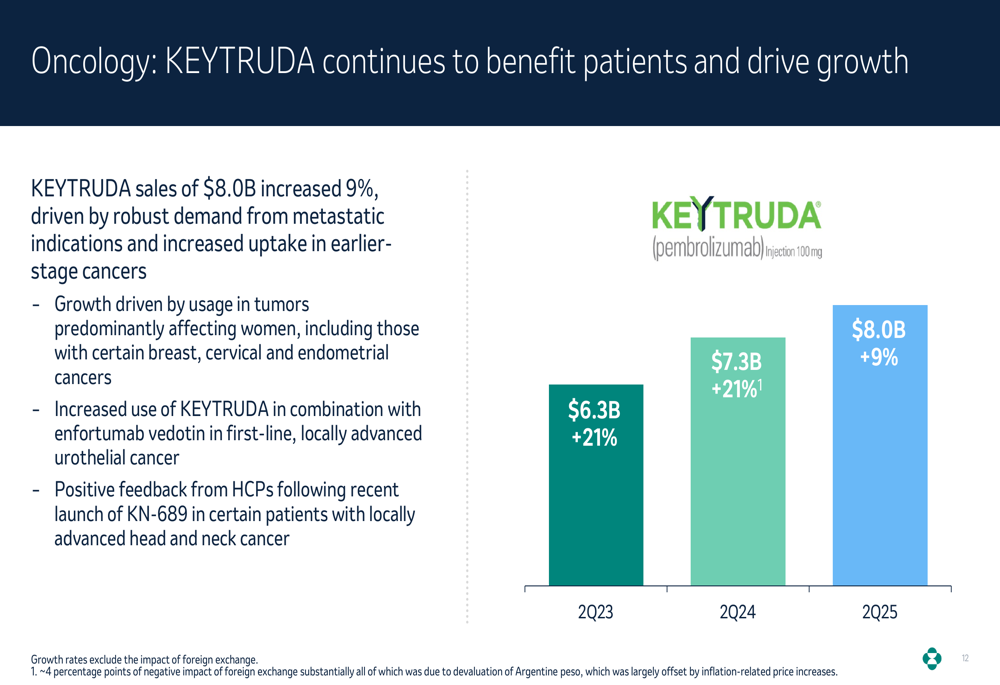

KEYTRUDA remained Merck’s primary growth driver, with sales increasing 9% to $8.0 billion. This growth was attributed to robust demand from metastatic indications and increased uptake in earlier-stage cancers, particularly in tumors predominantly affecting women and increased use in combination with enfortumab vedotin.

The following chart illustrates KEYTRUDA’s consistent growth trajectory:

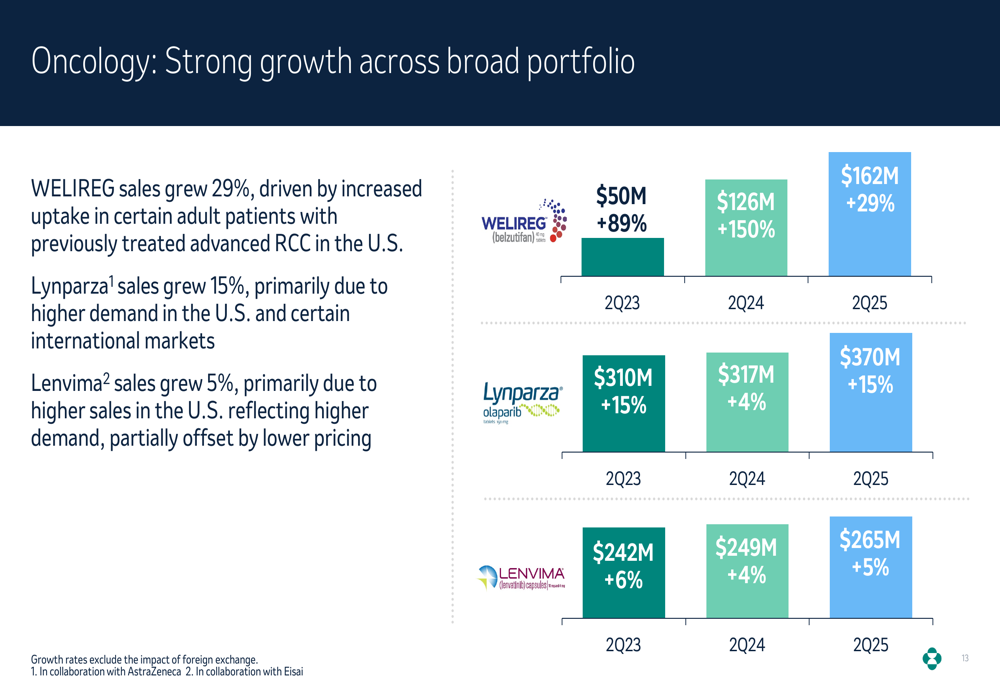

The broader oncology portfolio also demonstrated strong performance. WELIREG sales grew 29% to $162 million, Lynparza sales increased 15% to $370 million, and Lenvima sales rose 5% to $265 million, as shown in the following chart:

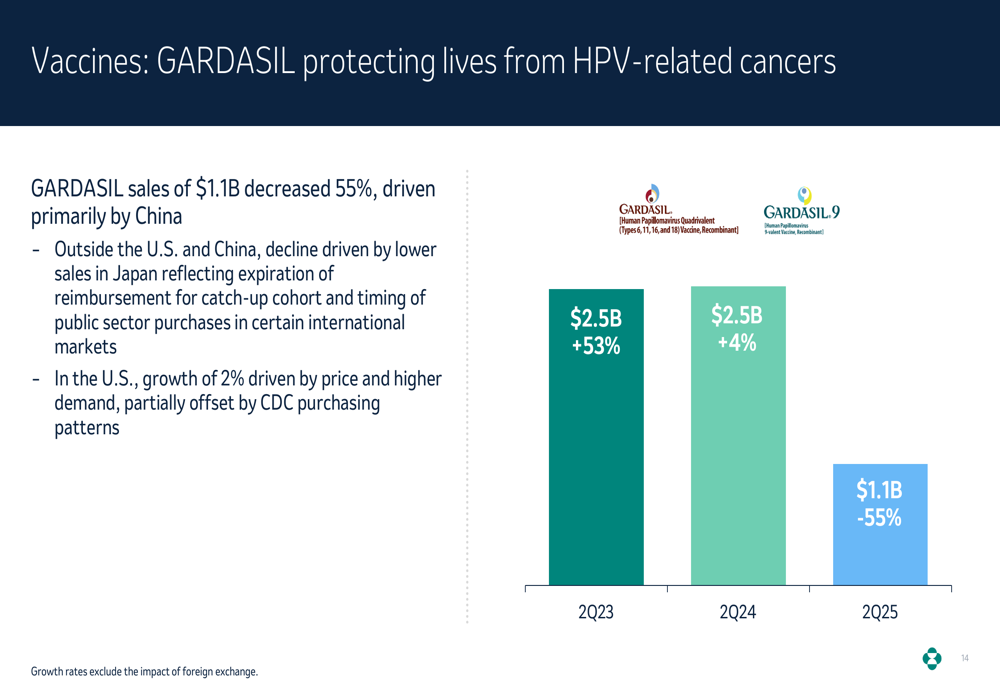

In contrast, GARDASIL experienced a significant decline, with sales decreasing 55% to $1.1 billion. This drop was primarily driven by challenges in China, where inventories remain elevated and demand continues to be soft. In the U.S., GARDASIL saw modest growth of 2%, driven by price increases and higher demand, partially offset by CDC purchasing patterns.

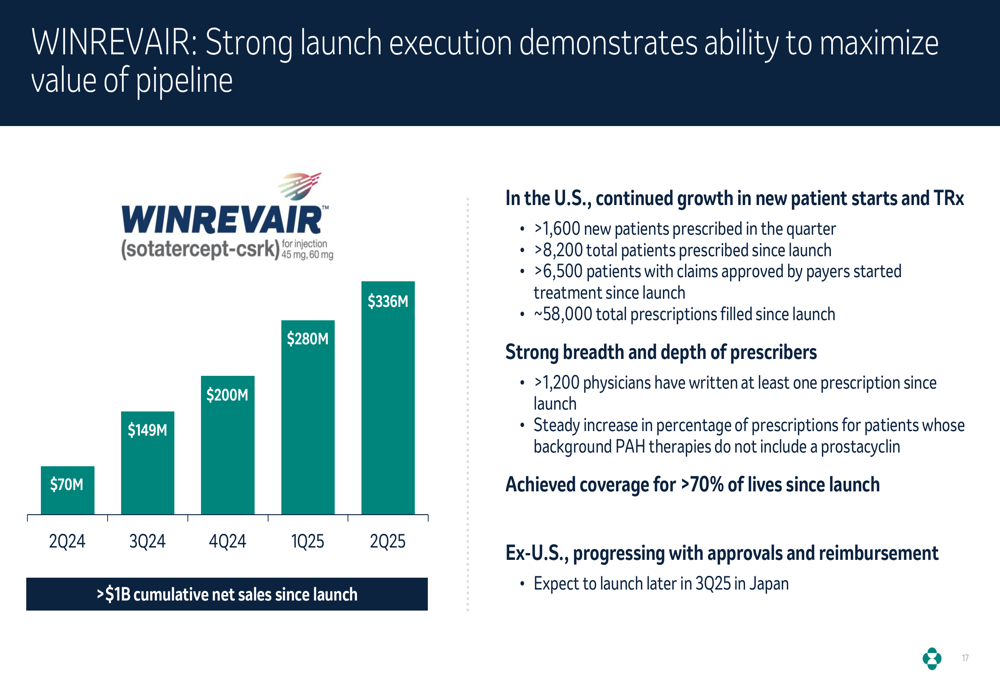

Merck’s newer products showed promising results. WINREVAIR, a treatment for pulmonary arterial hypertension, demonstrated strong launch execution with sales growing from $70 million in Q2 2024 to $336 million in Q2 2025. The company reported over 1,600 new patients prescribed in the quarter, bringing the total to over 8,200 patients since launch.

Strategic Initiatives & Pipeline Progress

Merck outlined its strategy to navigate the future loss of exclusivity for KEYTRUDA, focusing on three key areas: advancing early and late-phase pipeline candidates, launching new growth drivers with a commercial opportunity exceeding $50 billion by the mid-2030s, and executing strategic business development.

A significant element of this strategy is the pending acquisition of Verona Pharma, which will strengthen Merck’s cardiopulmonary portfolio. The acquisition brings Ohtuvayre, the first novel inhaled COPD maintenance treatment that combines bronchodilatory and non-steroidal anti-inflammatory activity.

The company highlighted important pipeline advancements across therapeutic areas:

1. In cardiopulmonary, positive topline results from the Phase 3 HYPERION trial showed that adding WINREVAIR to background PAH therapy significantly reduced the risk of clinical worsening events.

2. In infectious diseases, the FDA approved ENFLONSIA for the prevention of RSV lower respiratory tract disease in infants, and the company initiated its first Phase 3 trial to evaluate V181, an investigational quadrivalent vaccine for the prevention of dengue disease.

3. In oncology, Merck received its 10th approval for KEYTRUDA in earlier-stage cancers and has three ongoing Phase 3 trials evaluating ifinatamab deruxtecan.

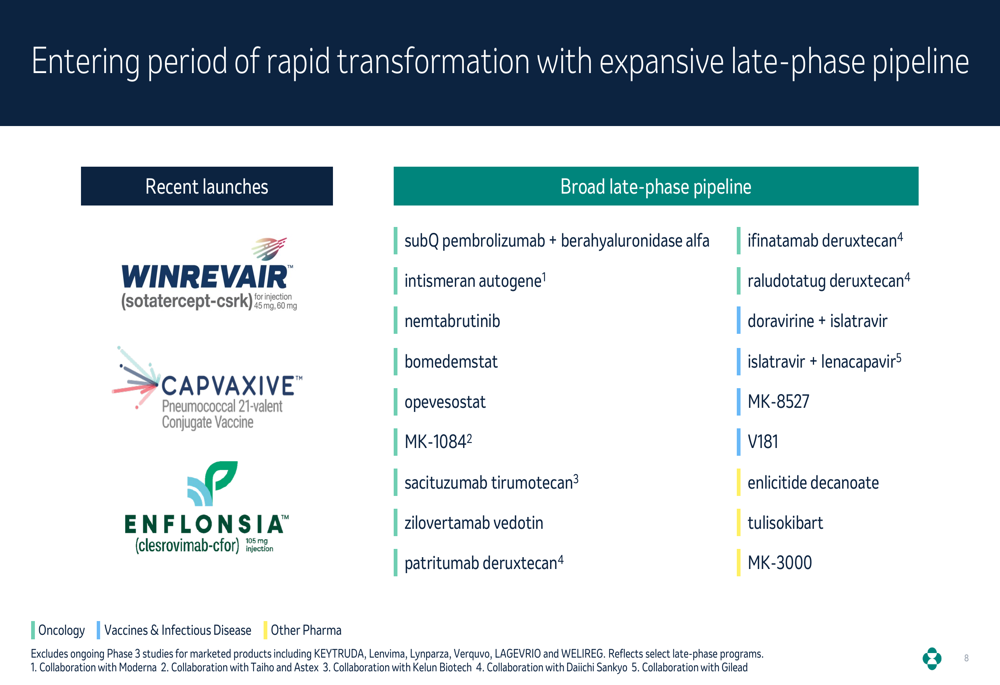

The following slide illustrates the company’s broad late-phase pipeline and recent launches:

Financial Outlook & Guidance

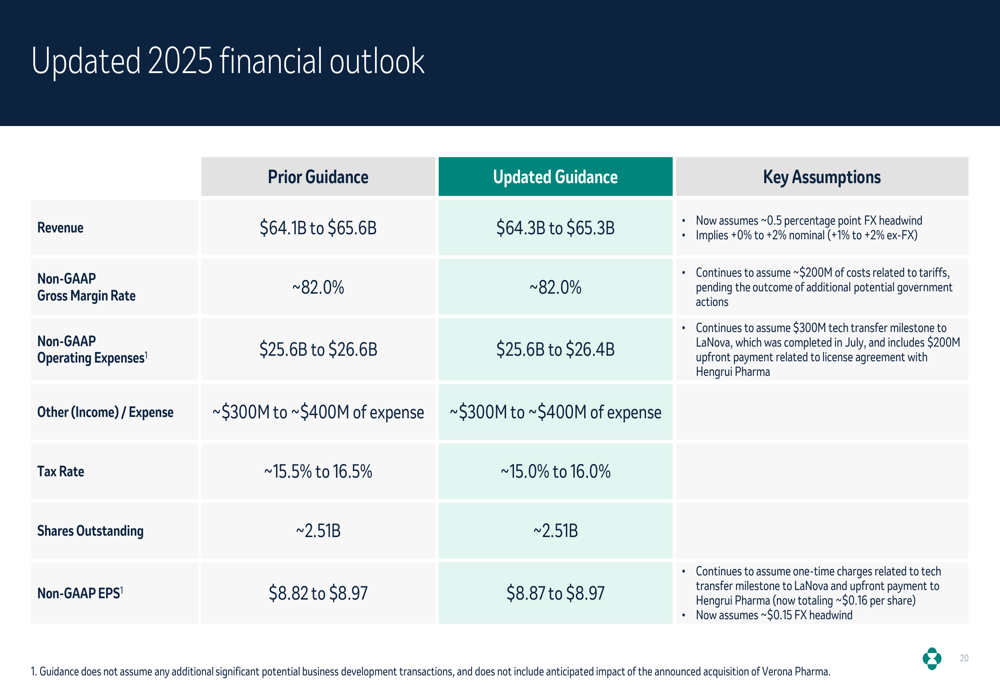

Merck updated its 2025 financial outlook, slightly narrowing its revenue guidance from $64.1-$65.6 billion to $64.3-$65.3 billion. The company maintained its non-GAAP EPS guidance of $8.53-$8.65.

CFO Caroline Litchfield expressed confidence in Merck’s growth trajectory, stating, "We are confident in our ability to drive growth in our business this year." She noted that the guidance does not include the anticipated impact of the announced acquisition of Verona Pharma.

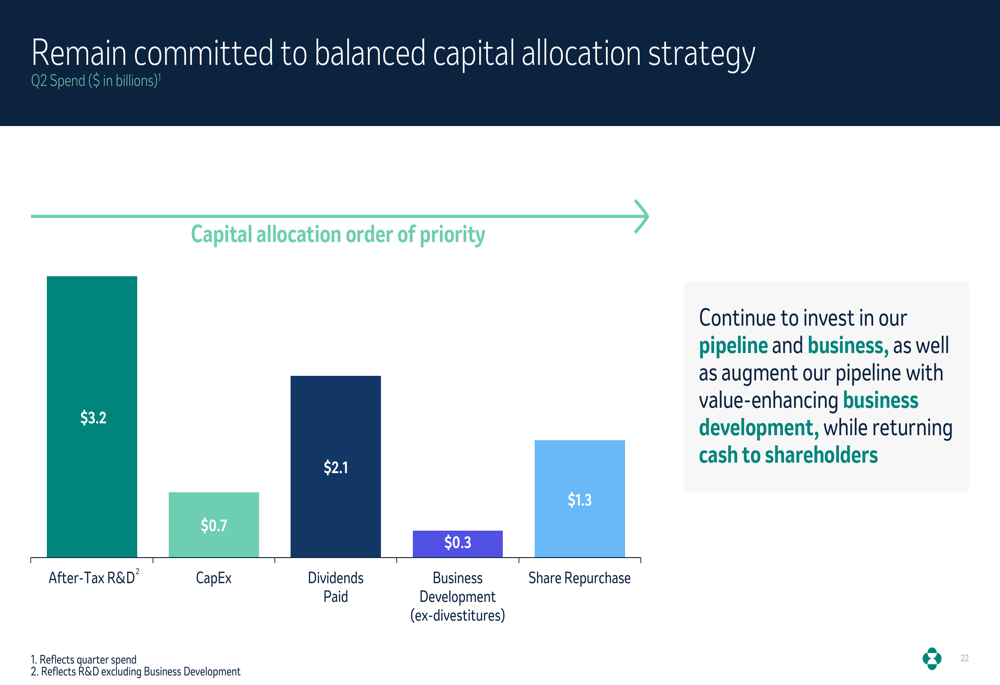

The company’s capital allocation strategy continues to prioritize investments in research and development, which totaled $3.2 billion after tax in the quarter. Merck also allocated $0.7 billion to capital expenditures, $2.1 billion to dividends, $0.3 billion to business development, and $1.3 billion to share repurchases.

Looking ahead, Merck identified several key milestones for the second half of 2025, including PDUFA dates in September and October for oncology and cardiopulmonary candidates, respectively, and the expected closing of the Verona Pharma acquisition in the fourth quarter of 2025.

Despite challenges in certain segments, particularly GARDASIL in China, Merck’s diversified portfolio and robust pipeline position the company to navigate near-term headwinds while building foundations for future growth. With an Altman Z-Score of 5.07 indicating strong financial health and a beta of 0.37 showing low volatility, Merck demonstrates resilience in current market conditions as it executes its long-term strategic vision.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.