Stock market today: S&P 500 drops for fifth day as focus shifts to Powell’s speech

Introduction & Market Context

Merck & Co . (NYSE:MRK) released its second-quarter 2025 earnings presentation on July 29, revealing mixed results as the pharmaceutical giant navigates contrasting performance across its product portfolio. The company’s shares fell 3.05% in premarket trading to $81.50, reflecting investor concerns despite some positive developments.

The presentation highlighted a 2% decline in worldwide sales to $15.8 billion, primarily driven by a dramatic 55% drop in GARDASIL sales in China. However, this was partially offset by continued strong performance from KEYTRUDA and the Animal Health segment, allowing the company to slightly raise the lower end of its full-year earnings guidance.

Quarterly Performance Highlights

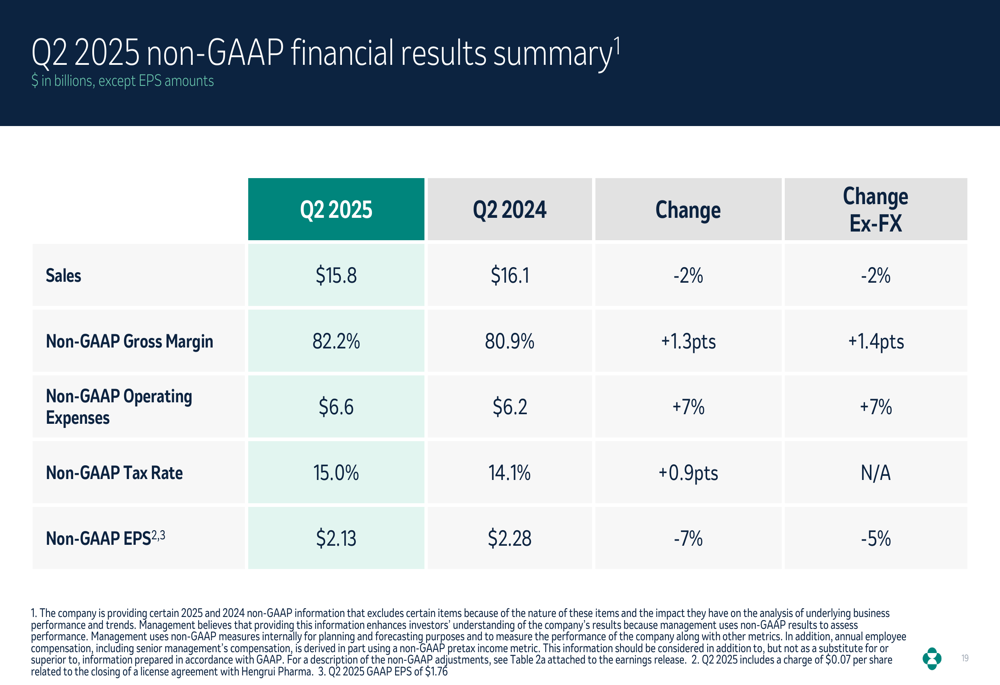

Merck (NSE:PROR) reported second-quarter worldwide sales of $15.8 billion, representing a 2% decline both nominally and excluding foreign exchange effects. However, excluding GARDASIL China, sales would have grown 7%, highlighting the significant impact of this single product in a specific market.

As shown in the following quarterly performance summary:

Non-GAAP earnings per share came in at $2.13, down 7% (5% excluding foreign exchange) compared to the prior year. The company noted that Q2 results included a charge of $0.07 per share related to a license agreement with Hengrui Pharma.

The comprehensive financial summary reveals pressure on earnings despite improved gross margins:

Product Performance Analysis

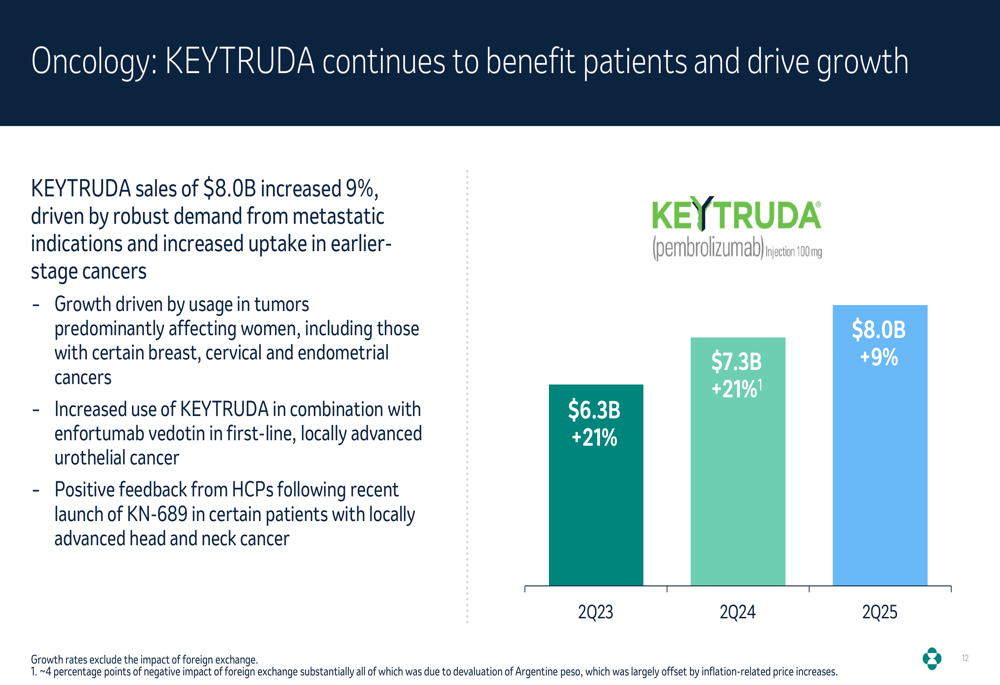

KEYTRUDA remained Merck’s primary growth driver, with sales increasing 9% to $8.0 billion. Growth was driven by usage in tumors predominantly affecting women and increased uptake in earlier-stage cancers, as illustrated in the following chart:

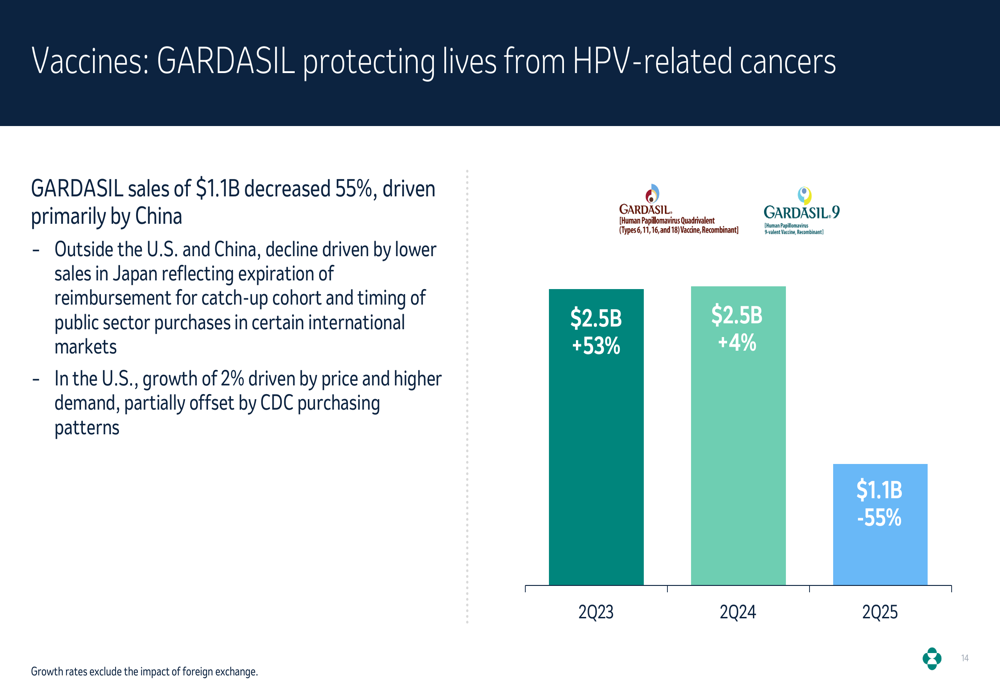

In stark contrast, GARDASIL sales plummeted 55% to $1.1 billion, primarily due to challenges in China. The company noted that channel inventories remain elevated in China with soft demand, leading to a decision to suspend shipments through at least the end of 2025.

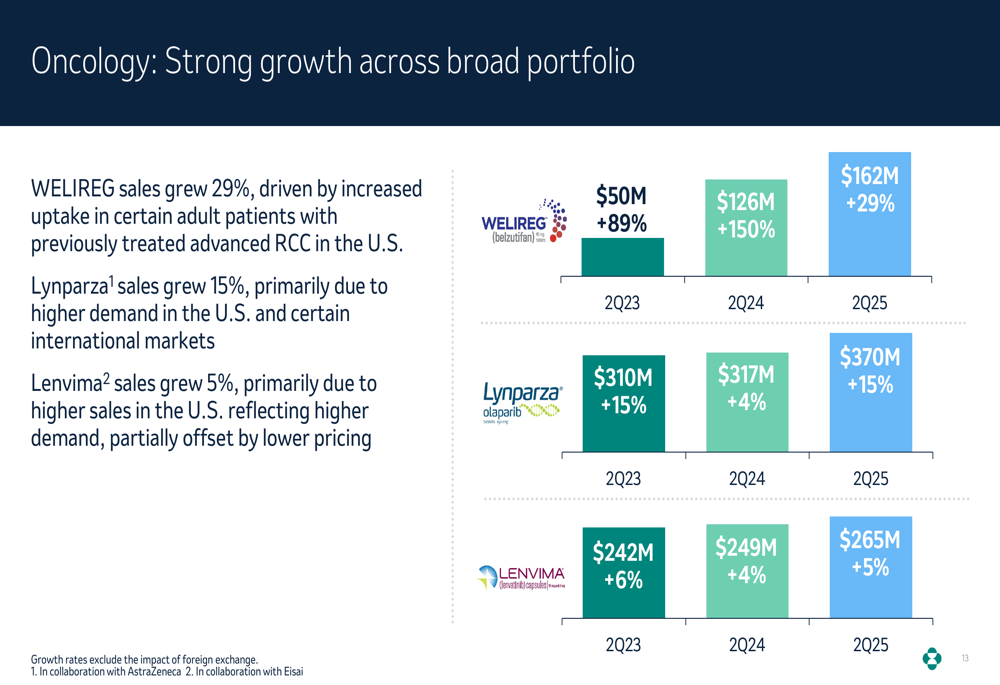

Merck’s broader oncology portfolio showed positive momentum, with WELIREG sales growing 29% to $162 million, Lynparza up 15% to $370 million, and Lenvima increasing 5% to $265 million:

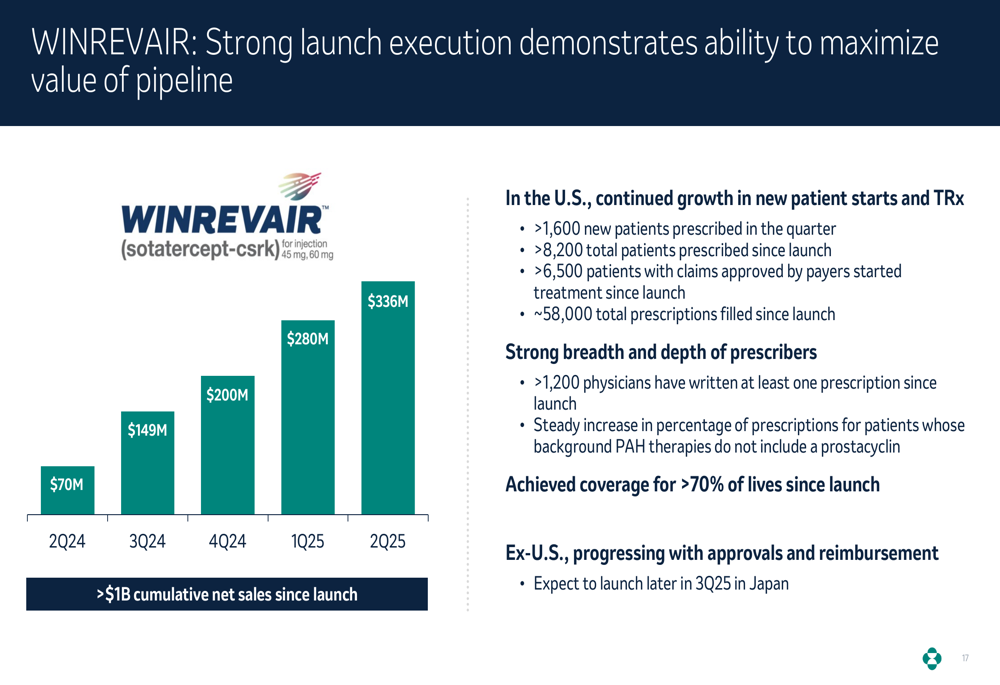

A notable bright spot was WINREVAIR, which continued its strong launch trajectory with Q2 sales of $336 million and cumulative sales exceeding $1 billion since launch. The company reported that over 8,200 patients have been prescribed the medication since its introduction:

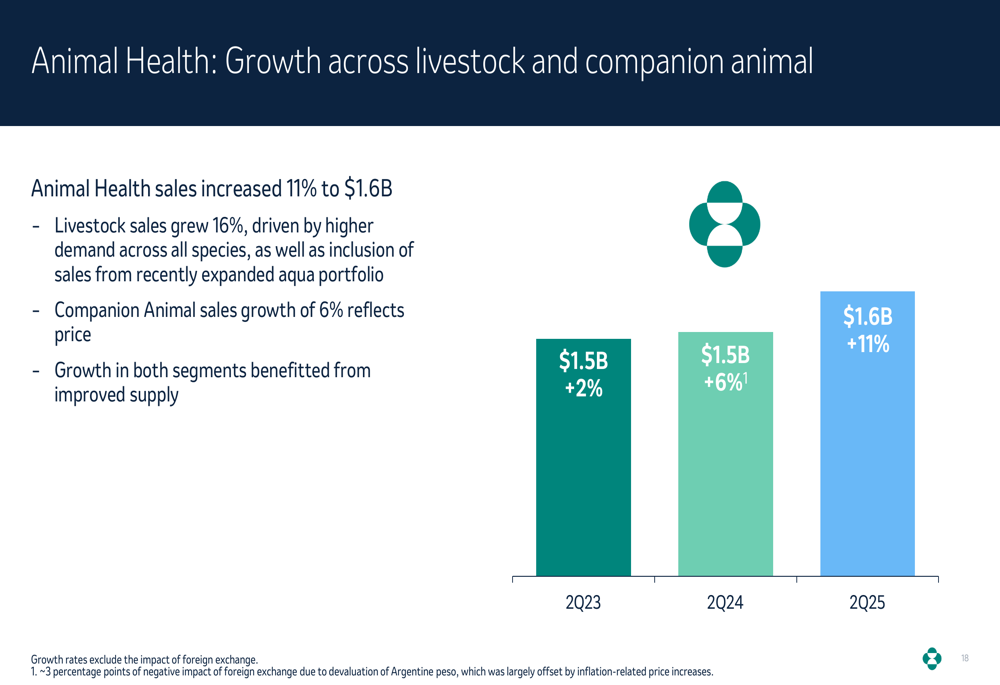

The Animal Health segment delivered robust performance with 11% growth to $1.6 billion, driven by higher demand across all species and benefits from an expanded aqua portfolio:

Strategic Initiatives & Pipeline

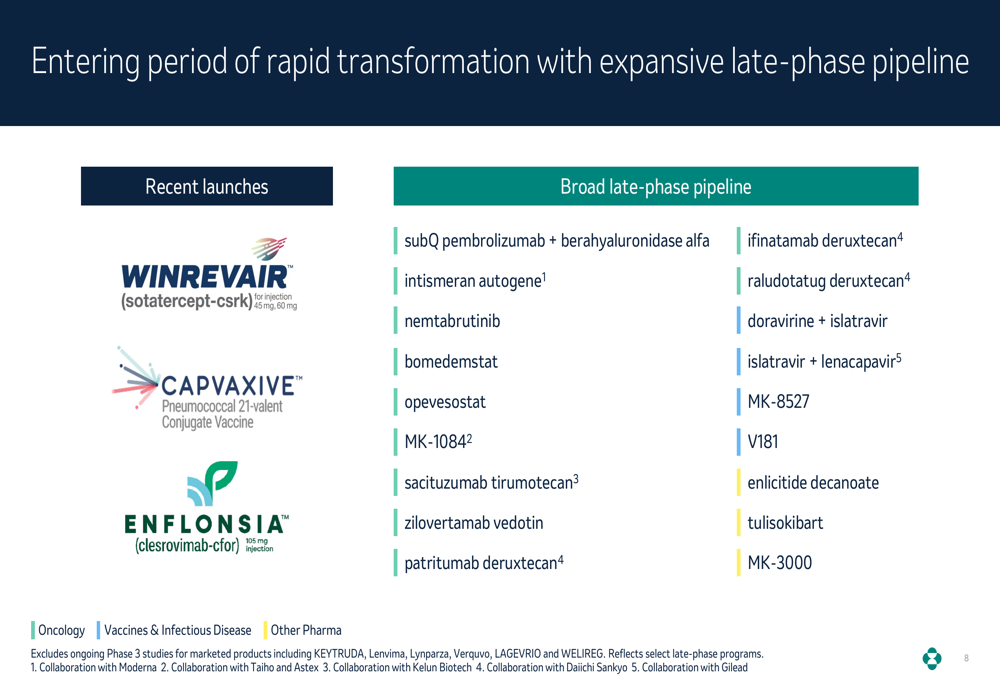

Merck is actively preparing for the eventual loss of exclusivity for KEYTRUDA by expanding its pipeline and pursuing strategic acquisitions. The company highlighted its pending acquisition of Verona Pharma (NASDAQ:VRNA), expected to close in Q4 2025, which will strengthen its cardiopulmonary portfolio with Ohtuvayre, the first novel inhaled COPD maintenance treatment in more than 20 years.

The company’s late-phase pipeline has tripled since 2021, with potential new growth drivers representing a commercial opportunity exceeding $50 billion by the mid-2030s:

Recent pipeline progress includes positive topline results for enlicitide in cardiovascular disease, FDA approval of ENFLONSIA for RSV prevention in infants, and continued expansion of KEYTRUDA’s indications with its 10th approval in earlier-stage cancers.

Financial Outlook & Guidance

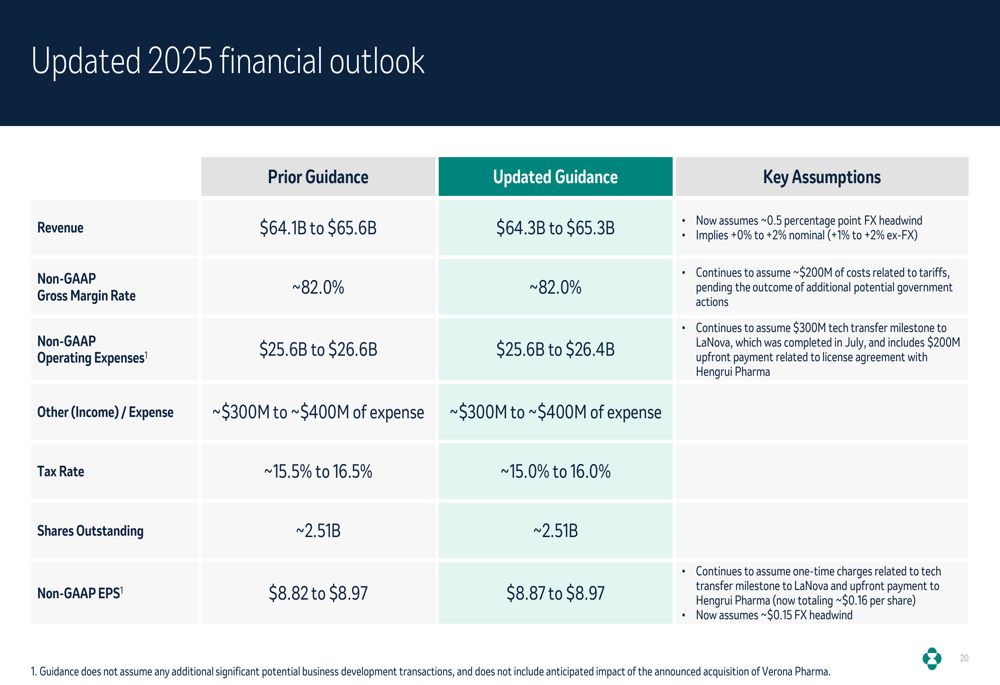

Despite the challenges with GARDASIL in China, Merck slightly narrowed and raised its 2025 financial guidance. The company now projects full-year revenue between $64.3 billion and $65.3 billion, compared to the previous range of $64.1 billion to $65.6 billion. Non-GAAP EPS guidance was adjusted to $8.87-$8.97 from the previous $8.82-$8.97, reflecting confidence in the underlying business strength:

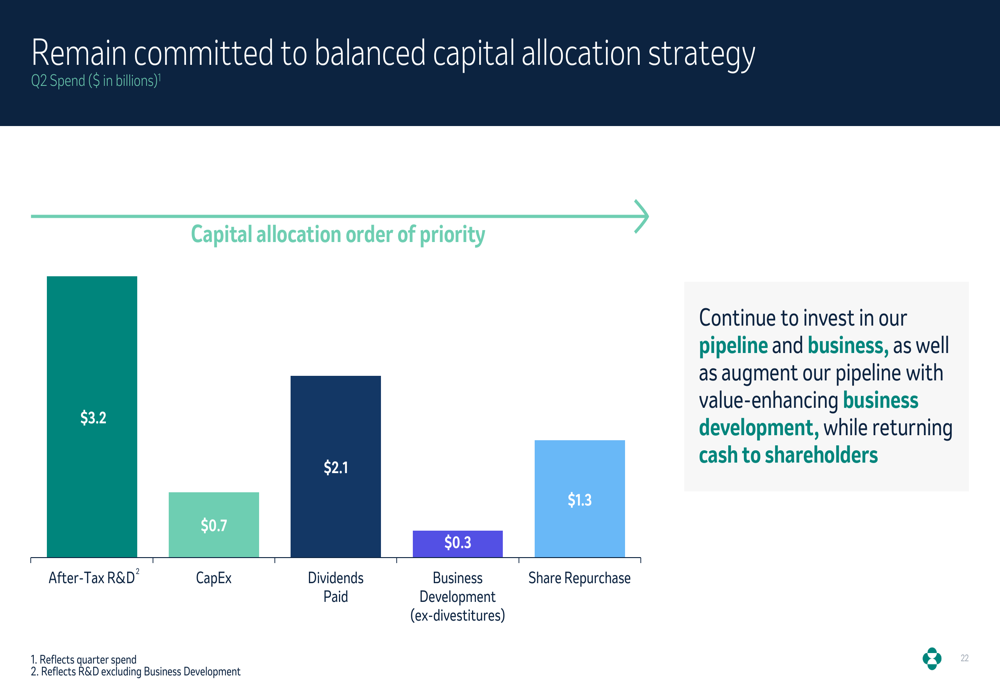

The company’s capital allocation strategy continues to prioritize R&D investments ($3.2 billion), followed by dividends ($2.1 billion), share repurchases ($1.3 billion), and business development activities ($0.3 billion):

Looking ahead, Merck highlighted several key milestones for the second half of 2025, including regulatory decisions for subcutaneous pembrolizumab (PDUFA date September 23) and WINREVAIR label update (PDUFA date October 25), as well as the expected closing of the Verona Pharma acquisition in Q4.

The company cautioned that GARDASIL headwinds will persist through at least the end of 2025 in China, while Japan will face additional pressure in the second half as the company laps increased vaccinations from a catch-up cohort. Despite these challenges, Merck’s diverse portfolio and expanding pipeline position it to navigate near-term headwinds while building foundations for future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.