Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

Meritage Corporation (NYSE:MTH) presented its second quarter 2025 results on July 24, 2025, revealing mixed performance as the homebuilder navigated a challenging market environment. The company’s stock fell 4.91% to $71.11 following the release, reflecting investor concerns about margin compression despite sales growth.

As one of the top five U.S. public homebuilders with a 40-year history, Meritage has positioned itself as a specialist in affordable entry-level and first move-up homes across 25 markets in 12 states. The company’s presentation highlighted its strategy of building spec homes (started before selling) and offering 60-day closing commitments as key competitive advantages in the current market.

Quarterly Performance Highlights

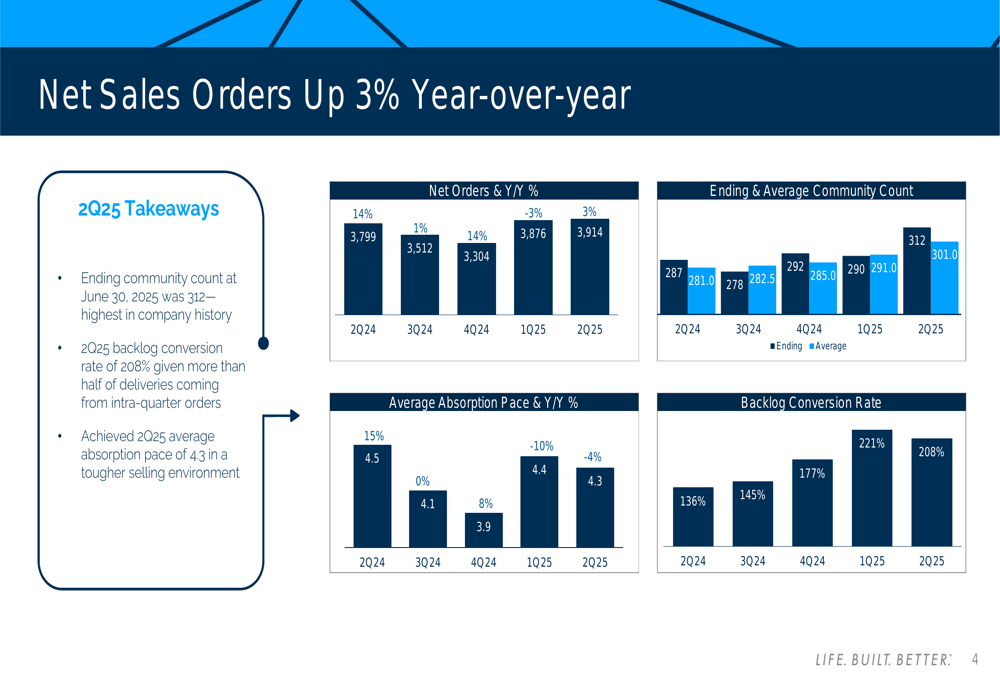

Meritage reported a 3% year-over-year increase in net sales orders to 3,914 units for Q2 2025, supported by a record-high community count of 312 communities. However, the company’s average absorption pace declined slightly to 4.3 homes per community per month compared to 4.5 in the same period last year.

As shown in the following chart of quarterly sales metrics:

The company’s backlog conversion rate remained elevated at 208%, indicating that more than half of the quarter’s deliveries came from intra-quarter orders rather than pre-existing backlog. This reflects Meritage’s continued emphasis on quick-turning, move-in ready homes as a competitive advantage in the current market.

Home closings increased marginally to 4,170 units in Q2 2025 from 4,118 in Q2 2024, but home closing revenue declined 5% to $1.62 billion due to a lower average selling price (ASP) of $387,000, down from $411,000 a year earlier.

Detailed Financial Analysis

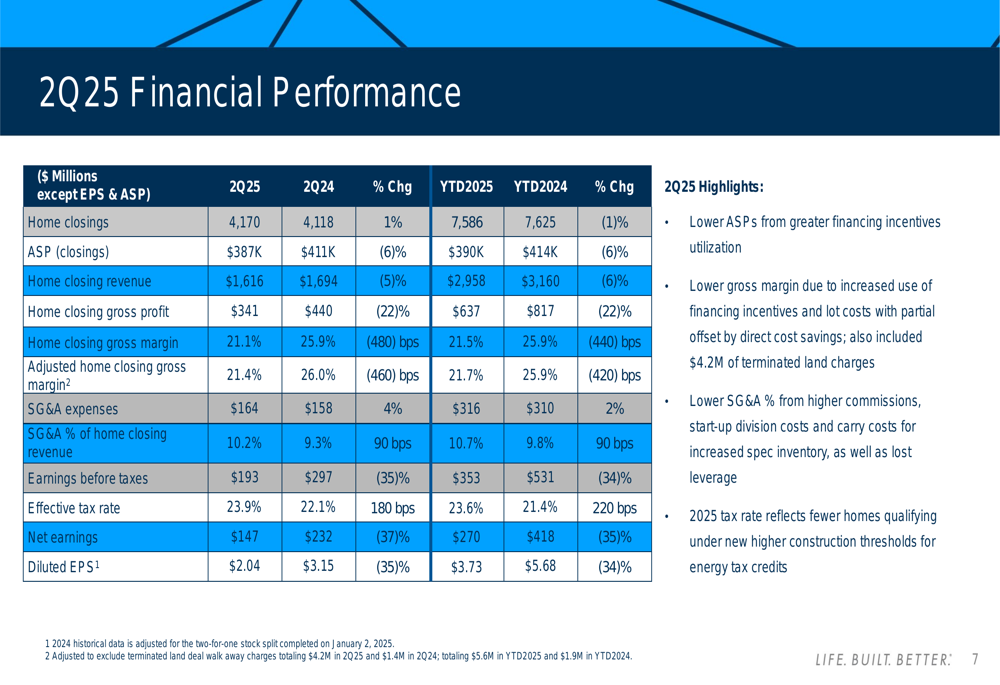

The financial results revealed significant margin pressure, with home closing gross margin falling to 21.1% from 25.9% in Q2 2024. This 480 basis point decline was primarily attributed to increased financing incentives and higher lot costs, partially offset by direct cost savings.

The comprehensive financial performance is illustrated in this table:

Selling, general and administrative (SG&A) expenses increased both in absolute terms ($164 million vs. $158 million) and as a percentage of home closing revenue (10.2% vs. 9.3%) compared to Q2 2024. The company cited higher commissions, start-up division costs, and carrying costs for increased spec inventory as factors contributing to the rise in SG&A expenses.

Net earnings declined 37% to $147 million, resulting in diluted earnings per share of $2.04, compared to $3.15 in the same quarter last year. The effective tax rate increased to 23.9% from 22.1%, reflecting fewer homes qualifying under new higher construction thresholds for energy tax credits.

Regional Performance Variations

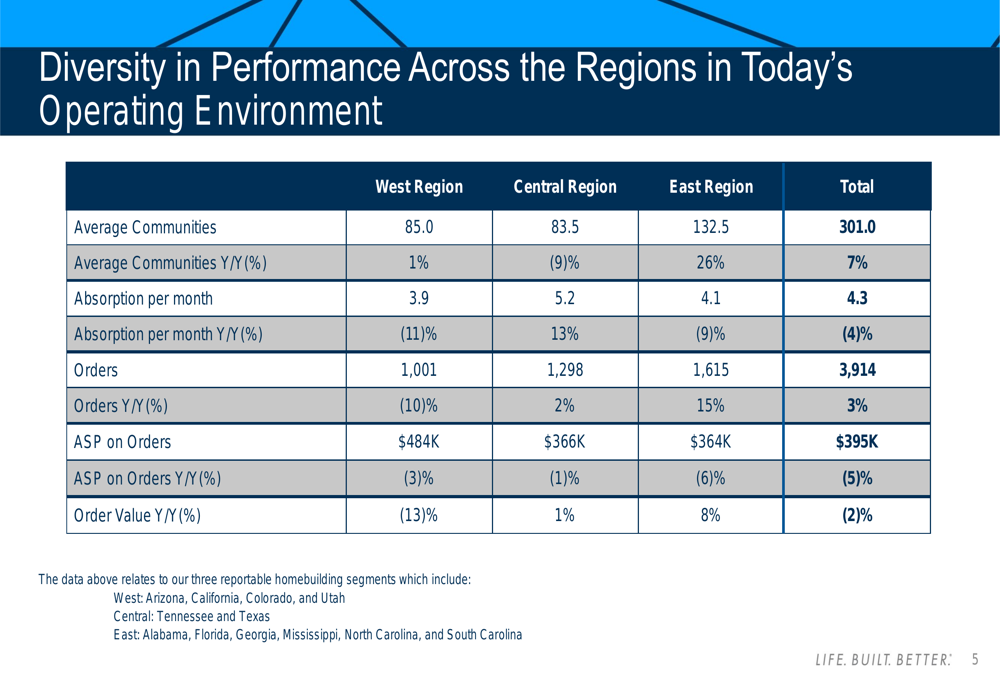

Meritage’s performance varied significantly across its three operating regions, with the East region showing the strongest growth while the West region faced challenges. The East region, which includes markets in Florida, Georgia, and the Carolinas, posted a 15% increase in orders despite a 9% decline in absorption rate, benefiting from a 26% increase in community count.

The regional breakdown reveals these contrasting performances:

The Central region, comprising Texas, Colorado, and Arizona, maintained relatively stable performance with a 2% increase in orders and a 13% improvement in absorption pace, despite having 9% fewer communities. Meanwhile, the West region (California and Utah) experienced a 10% decline in orders and an 11% drop in absorption rate.

Average selling prices on orders declined across all regions, with the East region seeing the largest decrease at 6%, contributing to an overall 5% decline in ASP on orders to $395,000.

Land Strategy and Capital Allocation

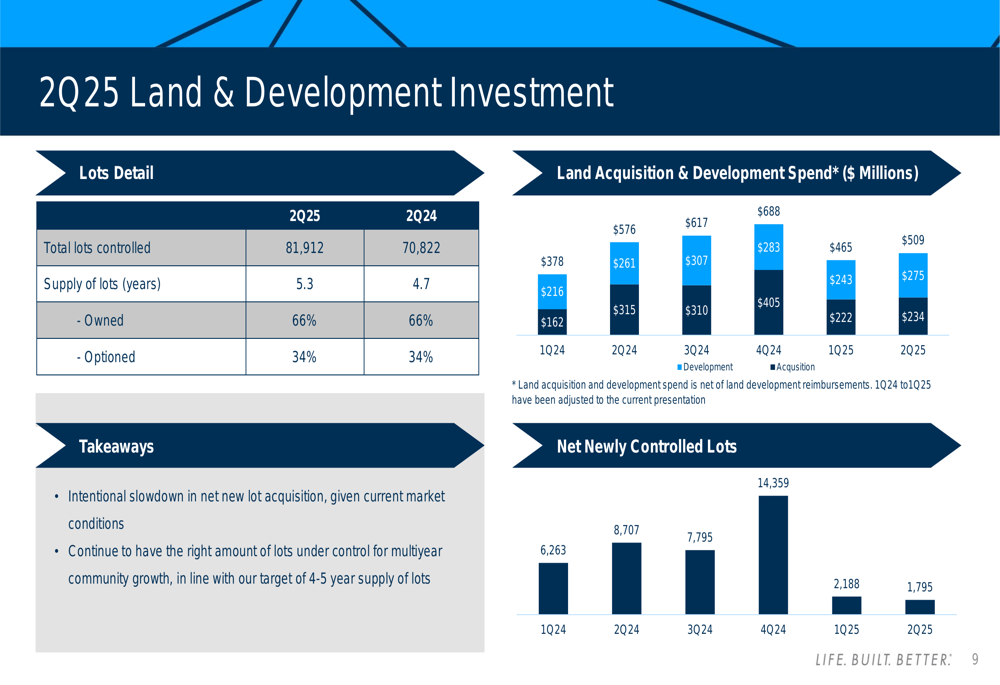

Meritage reported controlling 81,912 lots as of Q2 2025, representing a 5.3-year supply based on trailing twelve months closings, up from 4.7 years in Q2 2024. The company maintained its 66% owned and 34% optioned lot ratio.

The following chart illustrates the company’s land acquisition strategy:

The company intentionally slowed its net new lot acquisition given current market conditions, while maintaining sufficient inventory for multi-year community growth. Land and development spending totaled $509 million in Q2 2025, with $465 million allocated to land acquisition and $234 million to development.

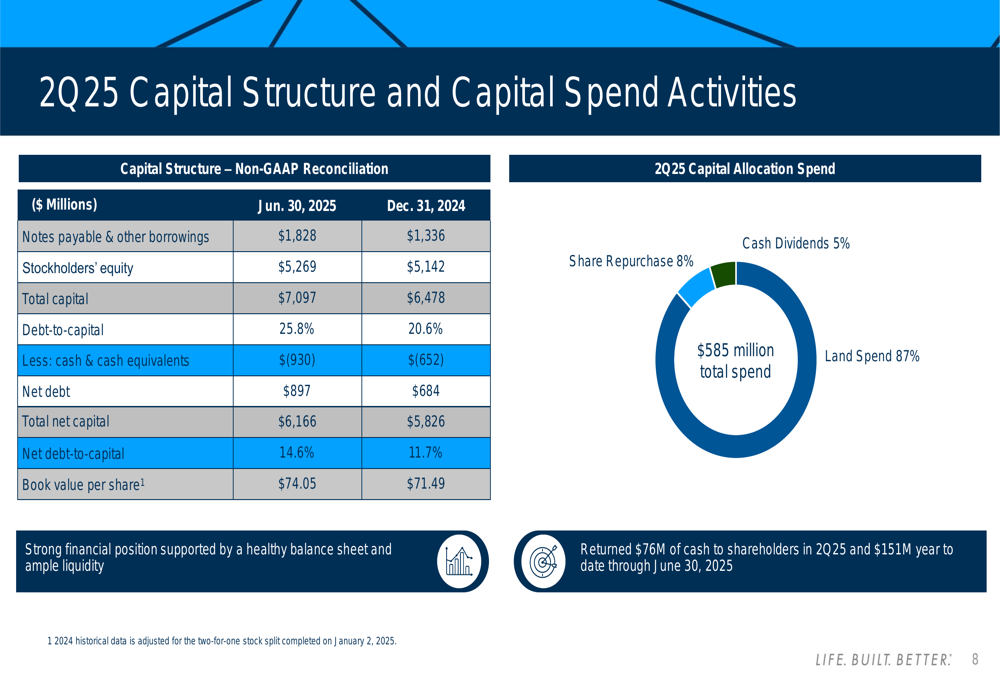

Meritage’s capital structure showed an increase in debt levels, with debt-to-capital ratio rising to 25.8% from 20.6% at year-end 2024. However, the net debt-to-capital ratio remained conservative at 14.6% due to $930 million in cash and cash equivalents.

The company’s capital allocation is detailed in this breakdown:

Meritage returned $76 million to shareholders in Q2 2025 and $151 million year-to-date through June 30, 2025, representing 13% of its total capital spend, with the remainder primarily allocated to land investment.

Forward Guidance and Outlook

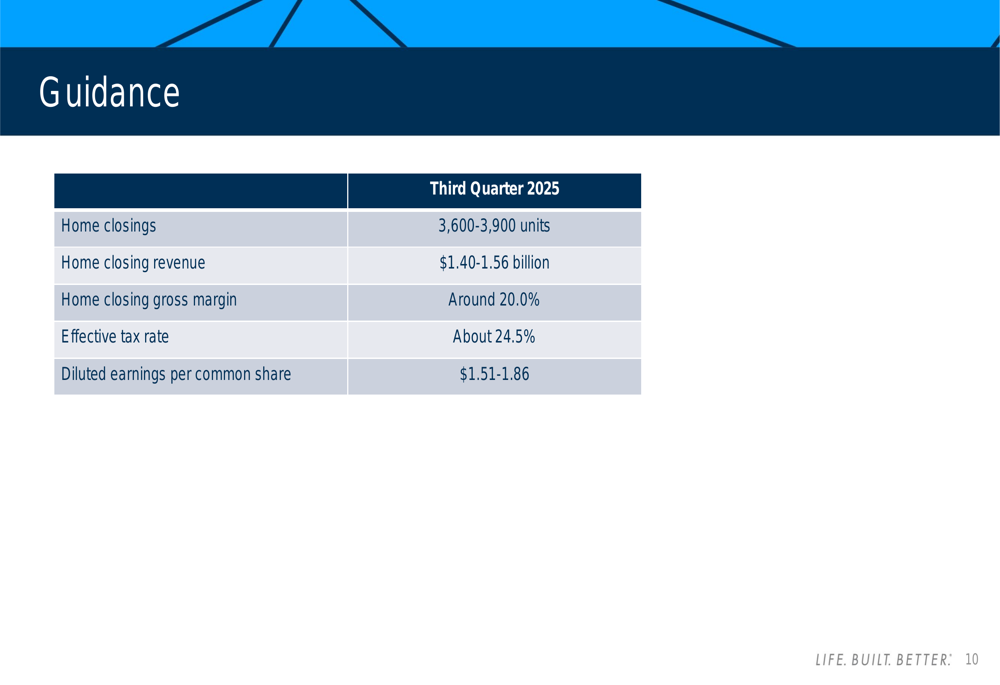

For the third quarter of 2025, Meritage provided the following guidance:

The company expects 3,600-3,900 home closings and $1.40-1.56 billion in home closing revenue for Q3 2025. Gross margins are projected to decline further to around 20.0%, reflecting continued pressure from financing incentives and competitive pricing. Diluted earnings per share are forecast between $1.51 and $1.86.

Management emphasized its flexible operations and capital allocation strategy aimed at maximizing returns during economic transitions. The company highlighted its community count expansion and improved cycle times as preparing it for future growth opportunities, while maintaining a balanced approach to land spending and shareholder returns.

This guidance suggests continued challenges in maintaining profitability despite sales growth, as Meritage navigates a housing market characterized by affordability concerns and interest rate sensitivity. The company’s focus on move-in ready homes and financing incentives appears to be supporting sales volume at the expense of margins, a trend that may persist in the near term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.