Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Metrovacesa SA (BME:MVC) presented its first half 2025 results on July 23, highlighting a temporary slowdown in deliveries while maintaining a positive outlook for the full year. The Spanish residential developer reported lower revenue and profitability figures compared to the same period last year, but emphasized strong presales and an expanding backlog that provide visibility for future growth.

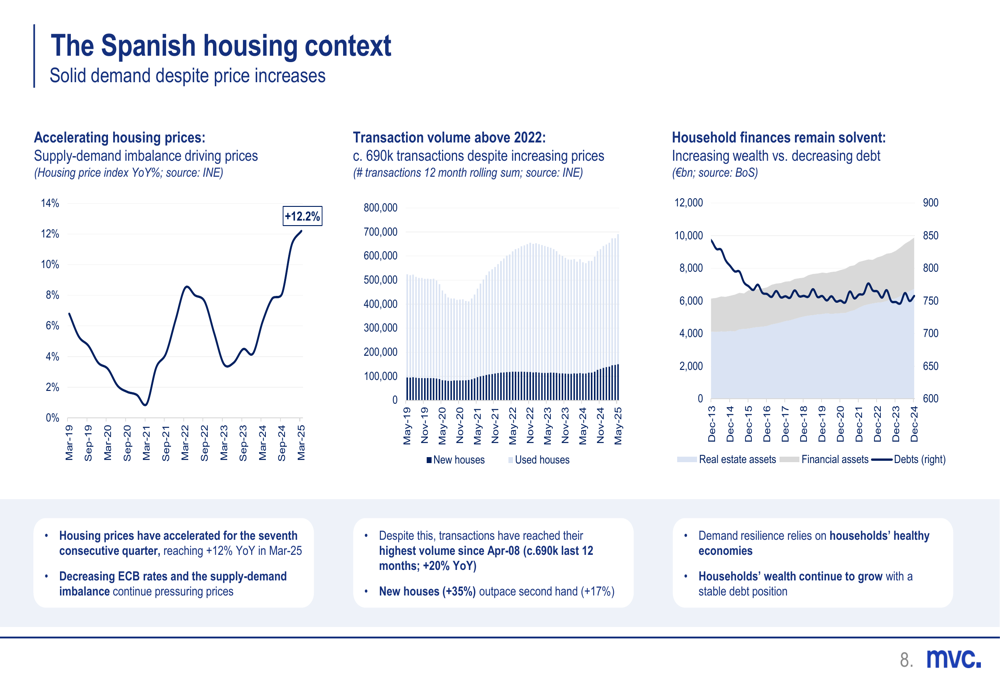

The presentation took place against a backdrop of robust housing market conditions in Spain, with prices accelerating for the seventh consecutive quarter to reach +12.2% year-over-year in March 2025. Transaction (JO:NTUJ) volumes increased 15% year-over-year as of April 2025, despite the price acceleration, indicating sustained demand in the market.

As shown in the following chart illustrating the Spanish housing context, solid demand persists despite price increases, with household finances remaining solvent as wealth increases while debt decreases:

Quarterly Performance Highlights

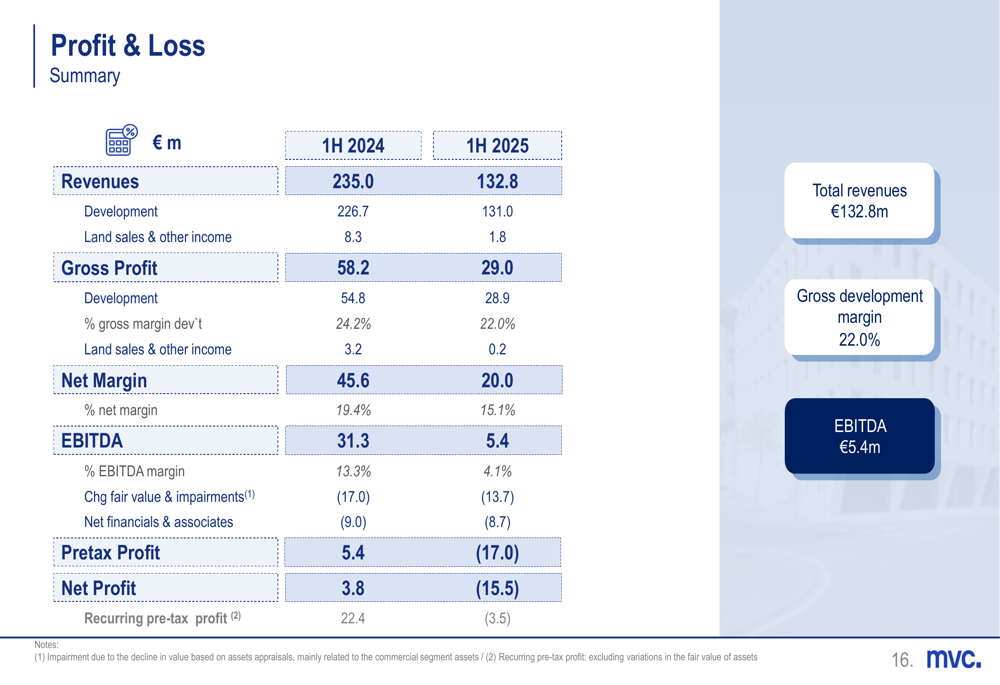

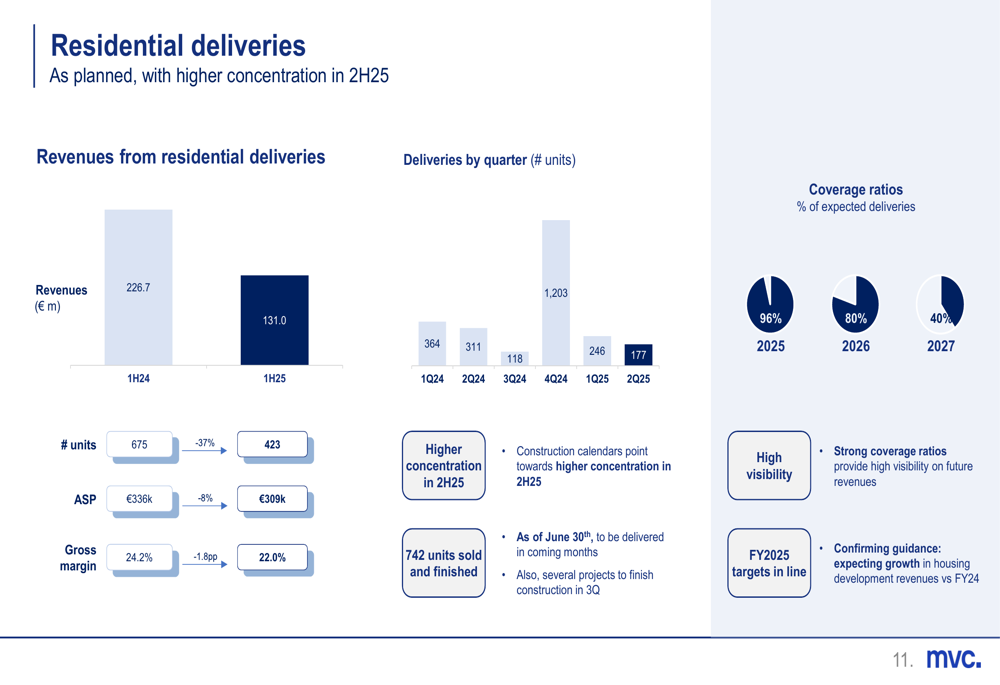

Metrovacesa reported total revenues of €132.8 million in the first half of 2025, a significant decrease from €235.0 million in the same period of 2024. The company delivered 423 residential units during the period, down from 675 units in 1H2024, with an average selling price (ASP) of €309,000 per unit. The gross development margin stood at 22.0%, compared to 24.2% in the prior year.

The company’s net result swung to a loss of €15.5 million, compared to a profit of €3.8 million in 1H2024. EBITDA decreased to €5.4 million from €31.3 million in the comparable period. The decline in profitability was partly attributed to impairments of €13.7 million, primarily in the commercial segment.

The following slide summarizes the key financial results for the first half of 2025:

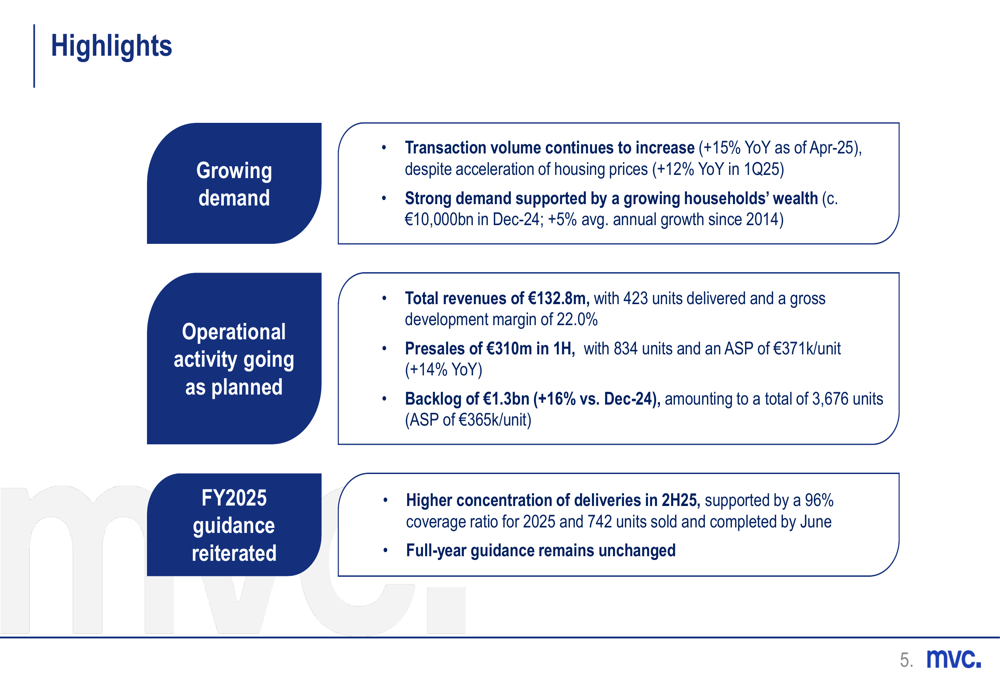

Despite the weaker first-half performance, Metrovacesa highlighted several positive indicators:

- Presales reached €310 million in 1H2025, comprising 834 units with an average selling price of €371,000 per unit, representing a 14% year-over-year increase in ASP

- Sales backlog grew to €1.3 billion, up 16% compared to December 2024, with 3,676 units at an average price of €365,000

- The company maintained a strong coverage ratio of 96% for expected 2025 deliveries

The key operational highlights are summarized in the following slide:

Operational Updates

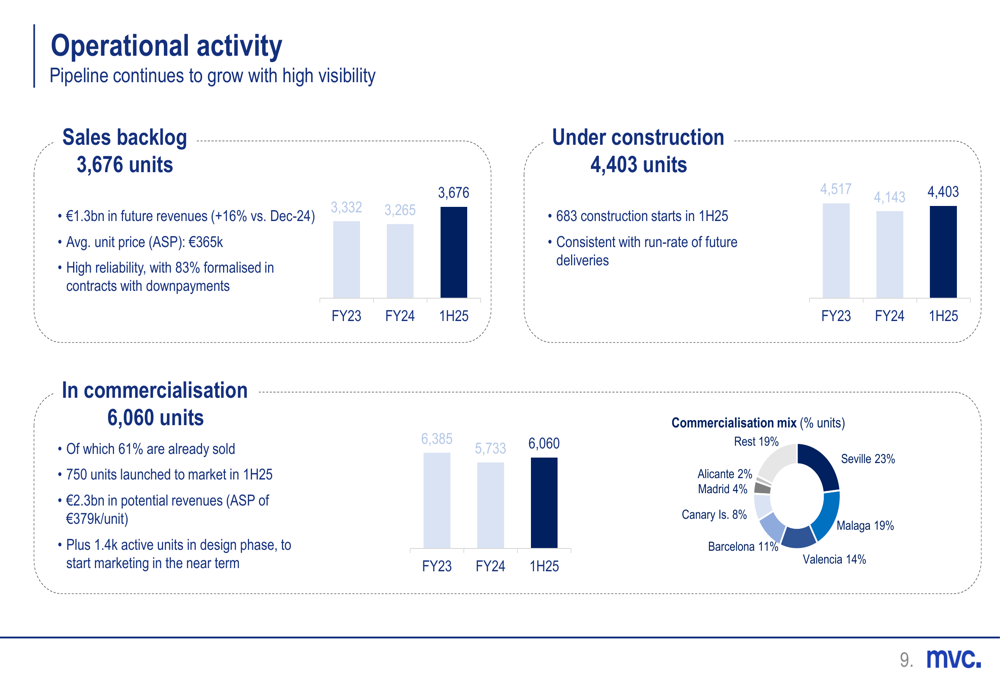

Metrovacesa’s operational activity showed a growing pipeline with high visibility for future deliveries. The company had 4,403 units under construction as of June 2025, with 683 construction starts in the first half of the year. Additionally, 6,060 units were under commercialization, of which 61% were already sold, representing €2.3 billion in potential future revenues.

The following chart details the company’s operational activity, including sales backlog, construction progress, and commercialization mix by region:

In terms of residential deliveries, Metrovacesa noted a higher concentration expected in the second half of 2025. The company had 742 units sold and completed by June, ready to be delivered in the coming months, with several projects scheduled to finish construction in the third quarter.

As illustrated in the following slide on residential deliveries, the company maintains strong coverage ratios that provide high visibility on future revenues:

Regarding land activity, Metrovacesa reported €1.8 million in land sales revenue for 1H2025, with a backlog of binding contracts worth €98.7 million as of June 2025, mostly to be formalized and recognized between 2025 and 2026. The company also made land acquisitions of approximately €38 million in the first half, including plots in Valdecarros (Madrid) and Valencia.

Financial Analysis

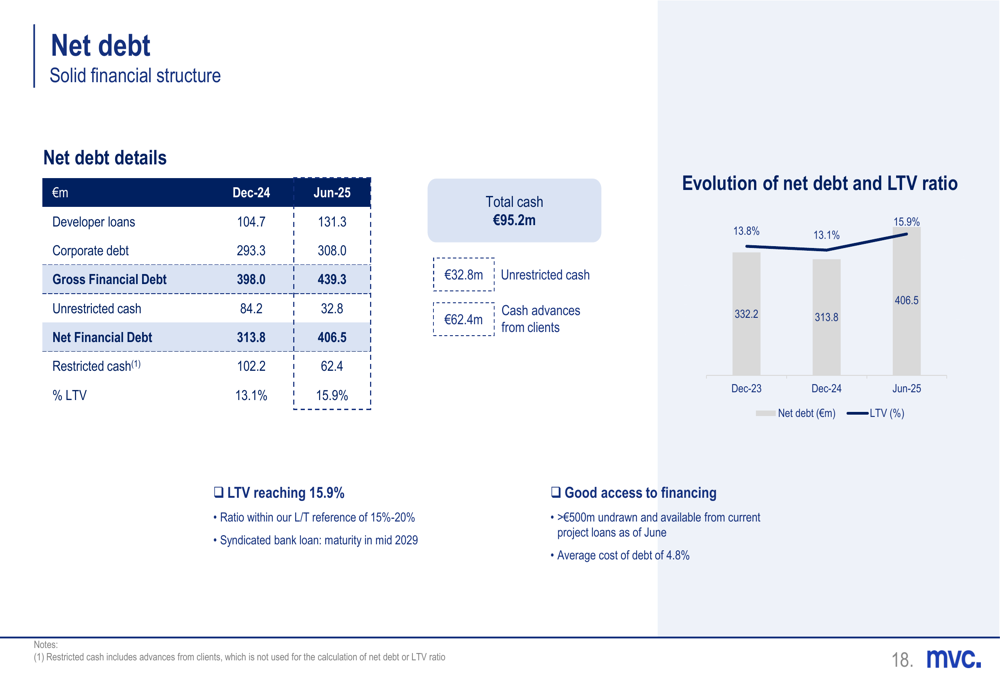

Metrovacesa’s net debt increased to €406.5 million as of June 2025, compared to €313.8 million at the end of 2024. The company maintained a loan-to-value (LTV) ratio of 15.9%, indicating a conservative financial position. Total (EPA:TTEF) cash stood at €95.2 million.

The following slide details the company’s net debt position:

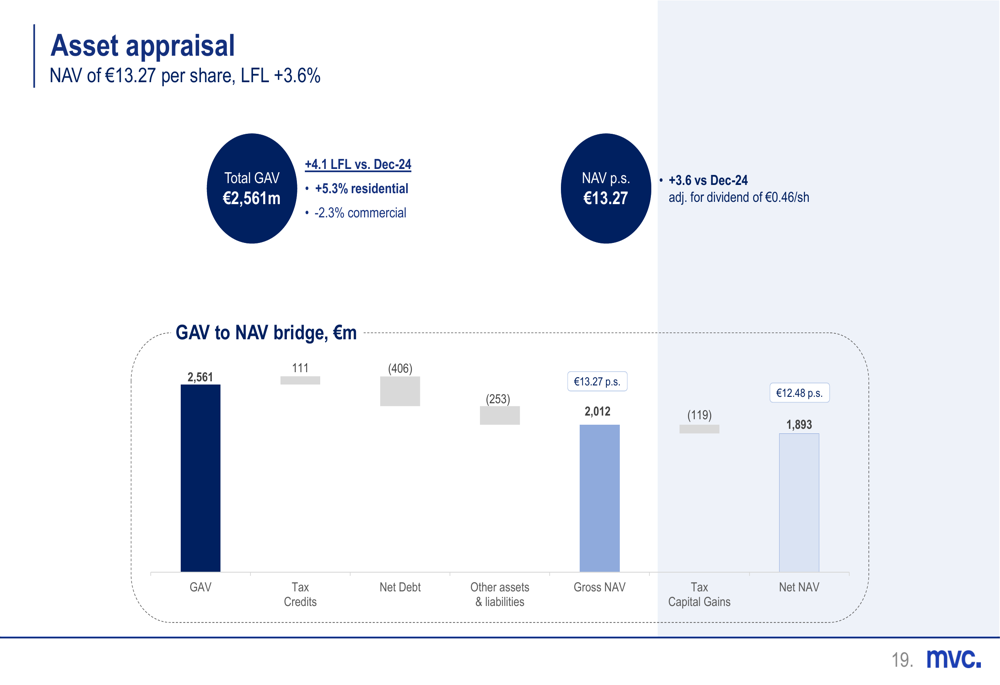

In terms of asset valuation, Metrovacesa reported a total Gross Asset Value (GAV) of €2,561 million and a Net Asset Value (NAV) per share of €13.27 as of June 2025, a slight increase from €13.25 at the end of 2024.

The asset appraisal and NAV calculation are illustrated in the following slide:

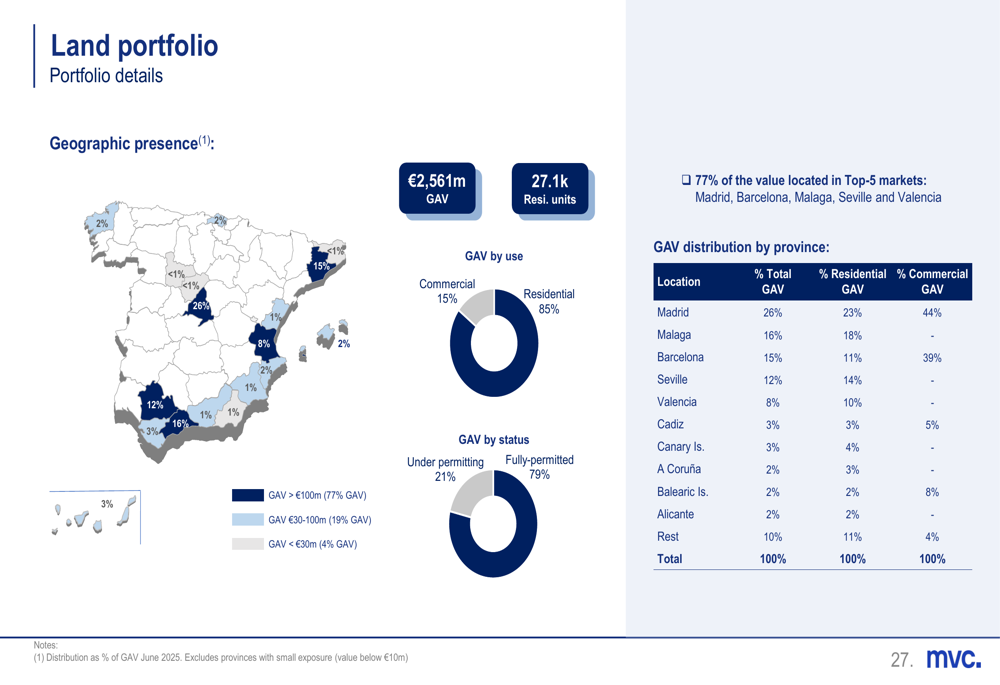

The company’s land portfolio remains well-diversified geographically, with 77% of the value located in Spain’s top five markets: Madrid, Barcelona, Malaga, Seville, and Valencia. Residential assets account for 85% of the GAV, with the remaining 15% in commercial properties. Fully-permitted land represents 79% of the portfolio value.

The geographic distribution of Metrovacesa’s land portfolio is shown in the following slide:

Forward-Looking Statements

Despite the weaker first-half performance, Metrovacesa confirmed its full-year guidance for 2025, expecting growth in housing development revenues compared to 2024. The company anticipates gross operating cash flow of more than €150 million for the full year.

Management emphasized three key factors supporting their positive outlook:

1. Solid foundations for demand in the Spanish housing market

2. Growing pipeline and visibility on future deliveries

3. Strong coverage ratios for upcoming projects

The company’s strategy continues to prioritize price over volume in its sales approach, taking advantage of the strong market conditions and supply-demand imbalance to maintain margins. This approach is reflected in the increasing average selling prices across both delivered units and presales.

Metrovacesa also highlighted its ESG initiatives, noting that it received a 93rd percentile valuation in the S&P Global Sustainability Assessment, underscoring the company’s commitment to sustainable development practices.

With a solid backlog of presales and high coverage ratios for future deliveries, Metrovacesa appears well-positioned to achieve its full-year targets, despite the temporary slowdown in the first half of 2025. Investors will be watching closely to see if the anticipated acceleration in second-half deliveries materializes as expected.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.