S&P, Nasdaq edge higher with gold spike, FOMC minutes in focus

Introduction & Market Context

Metsä Board Oyj (HEL:METSB) presented its Q2 2025 investor presentation on July 31, 2025, revealing significant operational challenges despite the company’s leading position in the European paperboard market. The stock closed at 3.204 EUR, up 0.82% on the day, but remains significantly below its 52-week high of 7.185 EUR, reflecting ongoing investor concerns about the company’s performance trajectory.

As a key player in the sustainable packaging sector, Metsä Board continues to emphasize its strategic focus on premium fresh fiber paperboards, which are positioned to benefit from global megatrends favoring recyclable packaging materials. However, the company’s current financial results demonstrate considerable headwinds in translating this market potential into financial performance.

Quarterly Performance Highlights

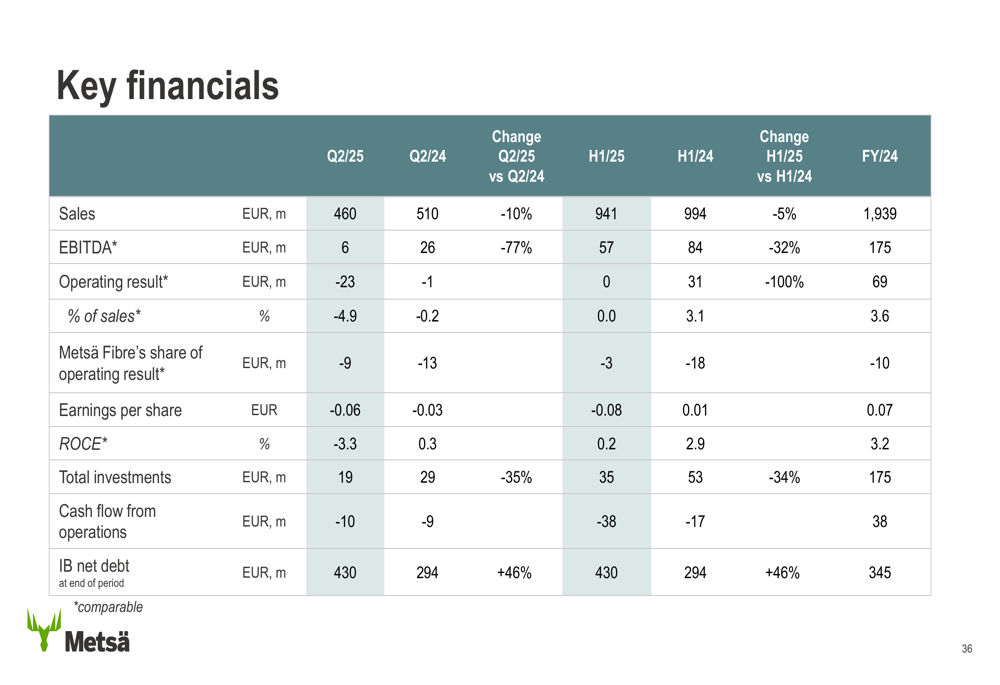

Metsä Board’s Q2 2025 results showed a marked deterioration compared to both the previous quarter and the same period last year. Sales reached EUR 460 million, while the operating result turned negative at -23 EUR million, significantly worse than the -1 EUR million reported in Q2 2024.

As shown in the following comprehensive financial overview from the presentation:

The company’s earnings per share declined to -0.06 EUR in Q2 2025 from -0.03 EUR in Q2 2024, while return on capital employed (ROCE) fell to -3.3%, far below the company’s target of over 12%. Cash flow from operations remained negative at -10 EUR million, and interest-bearing net debt increased to 430 EUR million, up from 294 EUR million a year earlier.

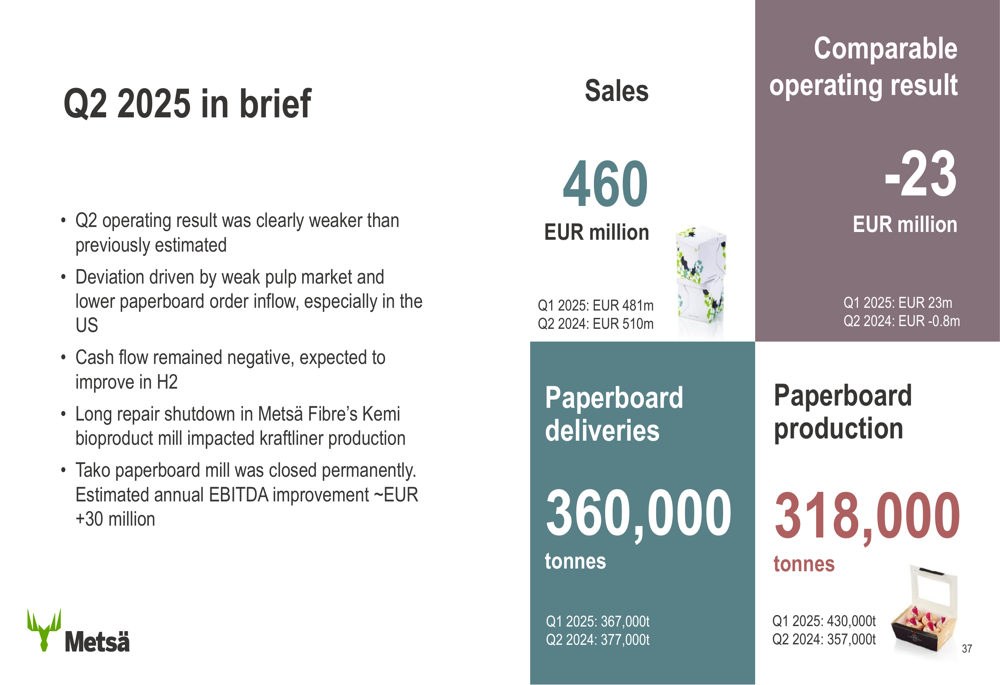

The Q2 results were summarized as "clearly weaker than previously estimated," with the company citing a weak pulp market and lower paperboard order inflow as key factors:

This performance continues a concerning trend that was evident in Q1 2025, when the company reported stable sales of €481 million but saw its operating result decline by nearly 30% to €23 million. The Q2 results represent a further deterioration from that already challenging position.

Strategic Initiatives

In response to these challenges, Metsä Board has implemented several strategic measures aimed at improving profitability and cash flow. Most notably, the company permanently closed its Tako paperboard mill, a decision expected to yield an annual EBITDA improvement of approximately EUR 30 million.

The company continues to invest in sustainable growth and improved competitiveness, with ongoing and planned investments including:

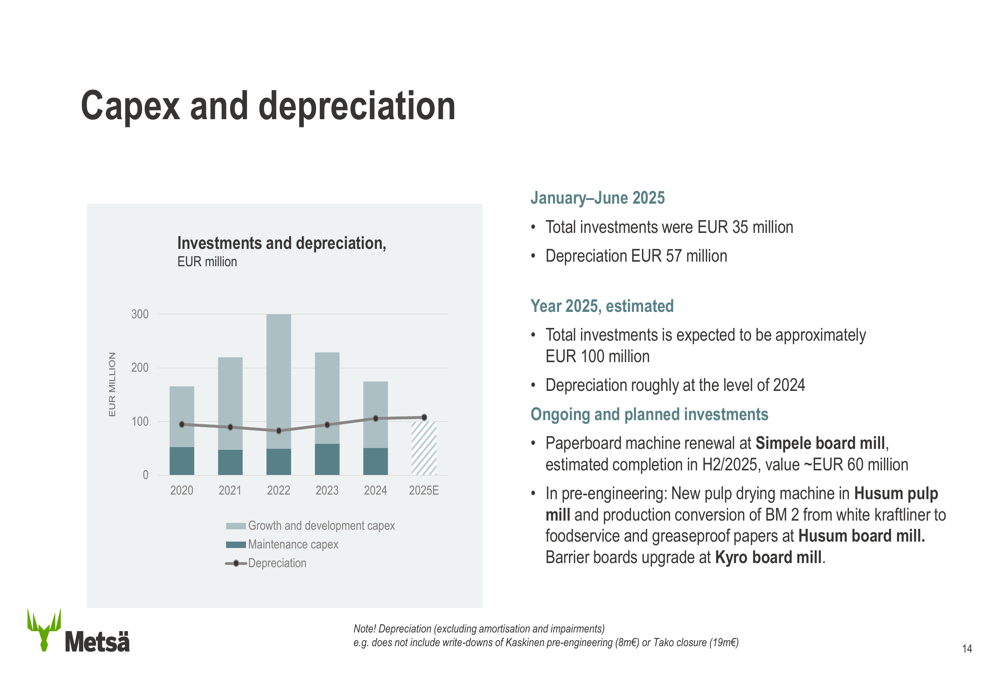

For 2025, total investments are expected to be approximately EUR 100 million, with a focus on the paperboard machine renewal at Simpele board mill. The company is also conducting pre-engineering for a new pulp drying machine at Husum pulp mill and barrier boards upgrade at Kyro board mill.

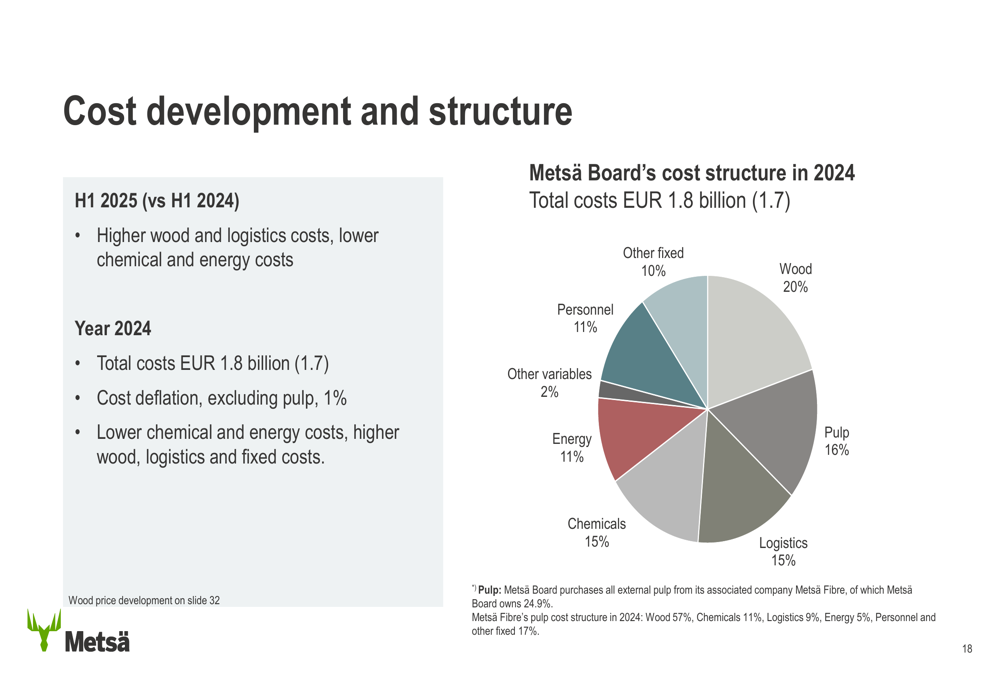

Metsä Board’s cost structure reveals areas where the company might find additional efficiencies:

With wood (20%), pulp (16%), logistics (15%), and chemicals (15%) representing the largest cost components, the company’s profitability is highly sensitive to fluctuations in these input prices. In H1 2025, the company faced higher wood and logistics costs, though this was partially offset by lower chemical and energy costs.

Competitive Industry Position

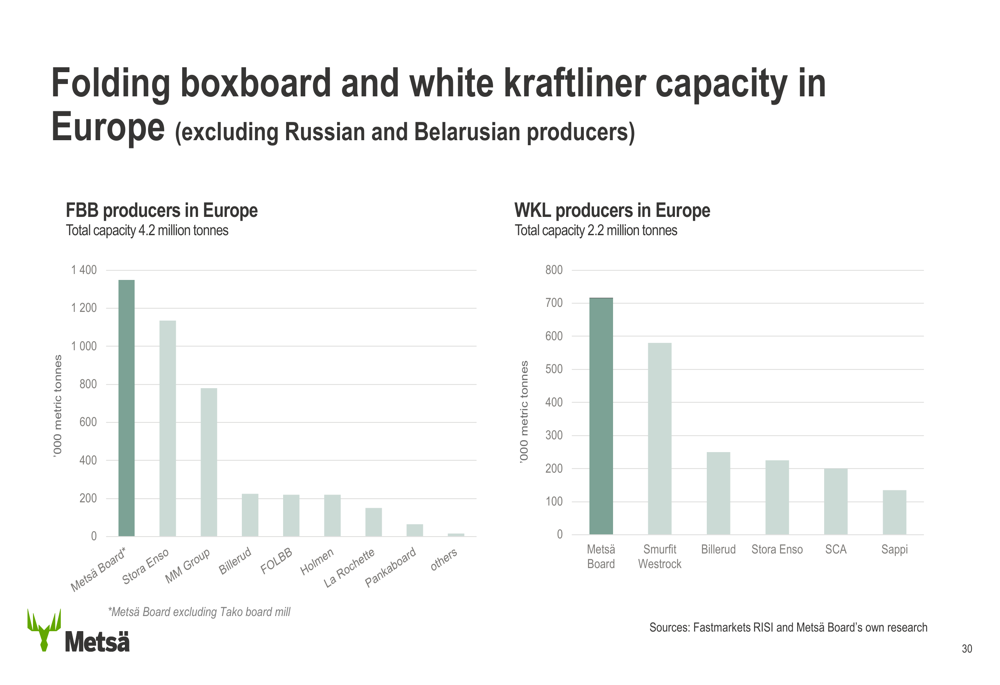

Despite its current financial challenges, Metsä Board maintains a leading position in its core markets. The company is the largest producer of folding boxboard in Europe, with a significant share of the white kraftliner market as well:

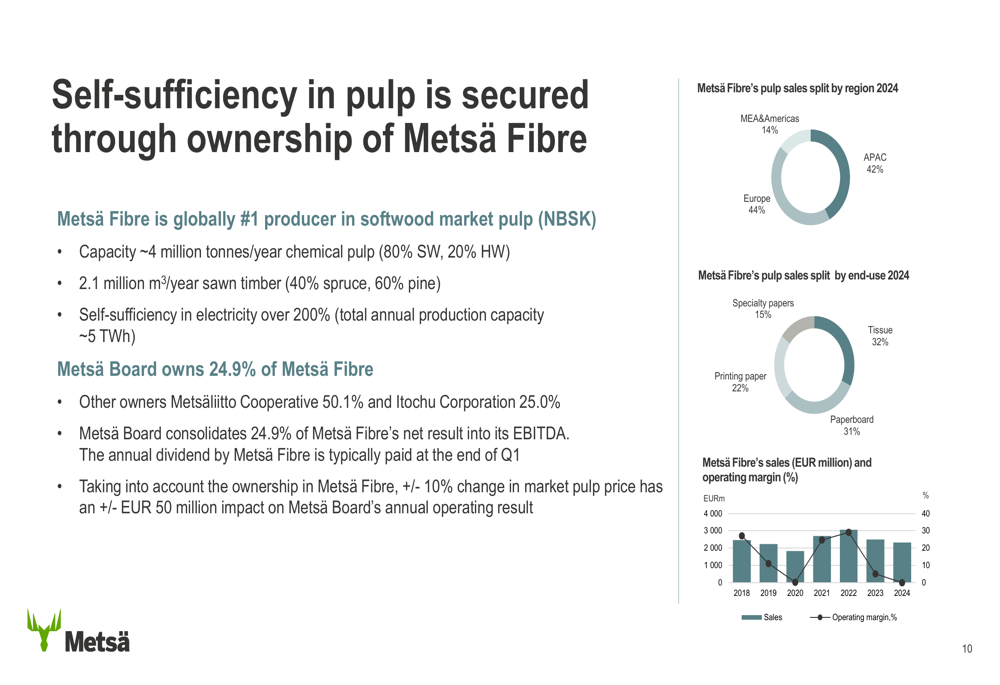

This market leadership provides Metsä Board with scale advantages and customer relationships that could prove valuable as market conditions improve. The company’s self-sufficiency in pulp through its 24.9% ownership in Metsä Fibre represents another strategic advantage, though the weak pulp market is currently negatively impacting results:

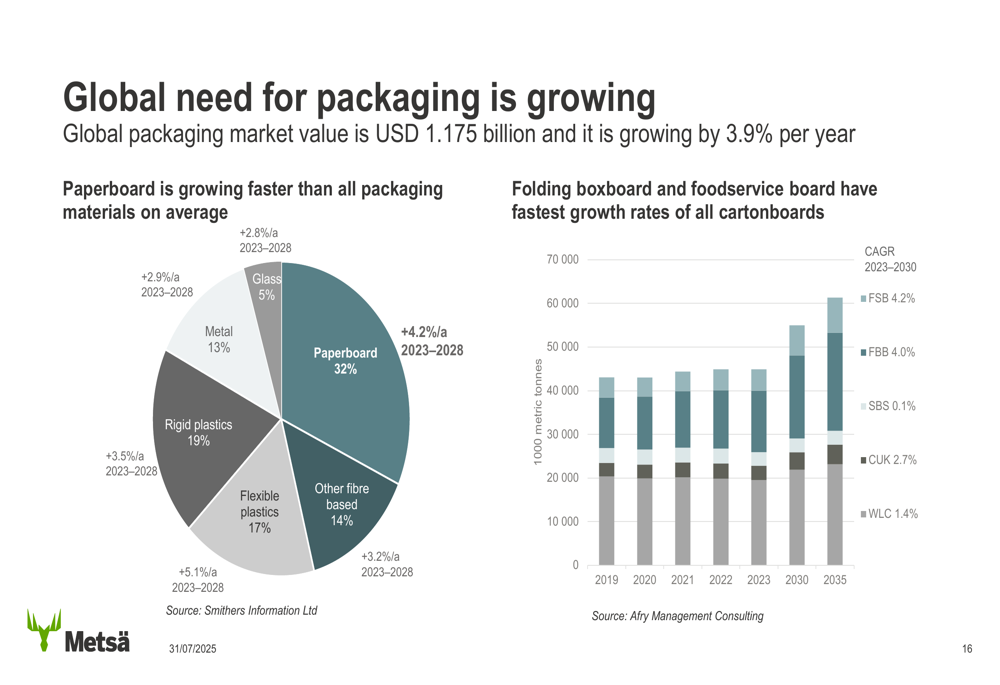

The global packaging market continues to show long-term growth potential, with paperboard growing faster than all packaging materials on average:

This market context suggests that Metsä Board’s current challenges may be more cyclical than structural, though the company will need to address operational inefficiencies to capitalize on market growth when conditions improve.

Forward-Looking Statements

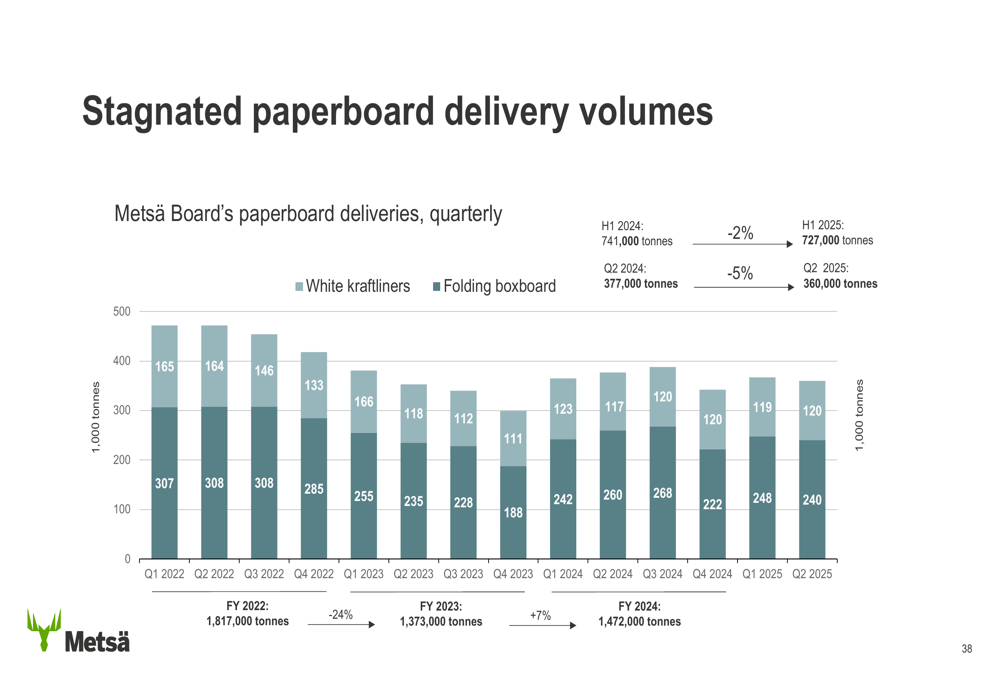

Metsä Board’s paperboard delivery volumes have stagnated in recent quarters, presenting a significant challenge to the company’s growth narrative:

Looking ahead, the company expects cash flow to improve in the second half of 2025, though specific guidance on operating results remains cautious. The anticipated EBITDA improvement from the Tako mill closure should begin to materialize in upcoming quarters.

The company’s financial targets remain ambitious relative to current performance, with goals including a comparable ROCE above 12% (versus current -3.3%), interest-bearing net debt to comparable EBITDA ratio of 2.5x (versus current 2.9x), and a dividend payout ratio of at least 50% (which was 98% in 2024, raising questions about sustainability).

CEO Esa Kaikkonen had previously emphasized the company’s focus on strengthening cash flow amid challenging market conditions, stating, "Our short-term focus is on strengthening our cash flow." This priority appears increasingly critical given the negative cash flow reported in Q2 2025.

Conclusion

Metsä Board’s Q2 2025 presentation reveals a company facing significant operational challenges despite maintaining a strong competitive position in growing markets. The negative operating result and cash flow, combined with stagnating delivery volumes, highlight the urgent need for the strategic measures the company has begun implementing.

While the permanent closure of the Tako mill and focus on cash flow improvement represent positive steps, investors will likely remain cautious until these initiatives translate into improved financial performance. The contrast between the company’s long-term growth narrative based on sustainable packaging trends and its current operational difficulties creates a complex investment case that will require careful monitoring in coming quarters.

For Metsä Board, successfully navigating the current market headwinds while positioning for future growth remains the central challenge, with upcoming quarters likely to prove decisive in determining whether the company can reverse its negative performance trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.