Europe’s Stoxx 600 inches lower amid French political crisis

Introduction & Market Context

MGIC Investment Corp (NYSE:MTG), a leading provider of private mortgage insurance, released its Q2 2025 quarterly supplement on July 31, 2025, revealing continued strength in its mortgage insurance portfolio. The presentation follows a strong Q1 where the company reported earnings per share of $0.75, exceeding analyst expectations of $0.69, and demonstrates MGIC’s continued focus on maintaining high credit quality while effectively managing risk.

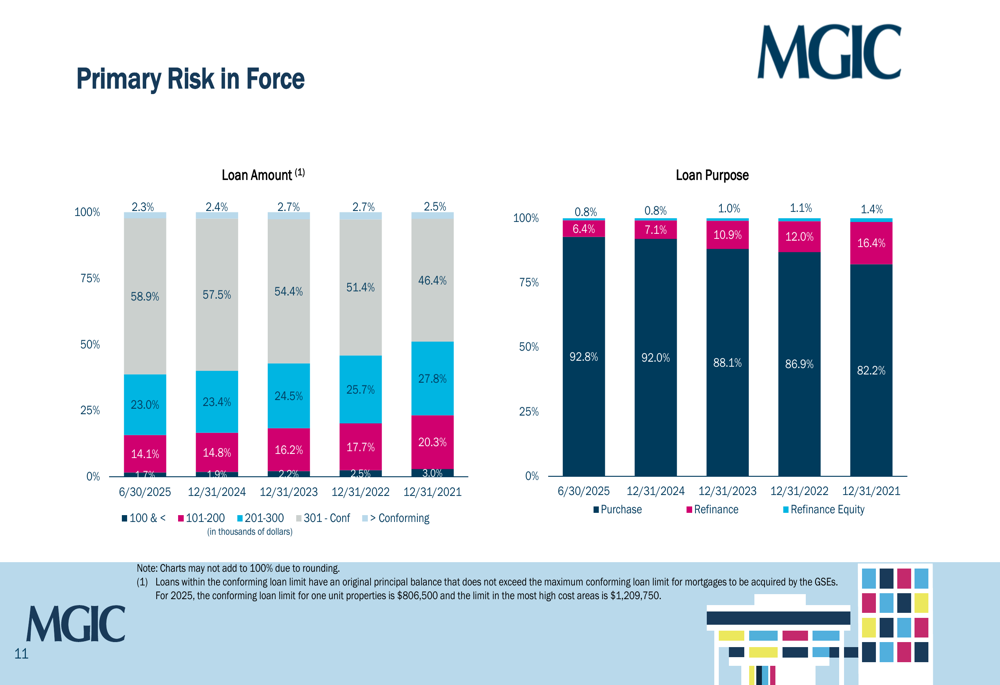

The company’s stock closed at $25.68 on July 30, 2025, down 1.13% for the day, but has shown resilience with its current price well above its 52-week low of $21.94. MGIC continues to benefit from a housing market that favors purchase loans over refinancing, with 92.8% of its portfolio consisting of purchase mortgages.

Portfolio Quality Highlights

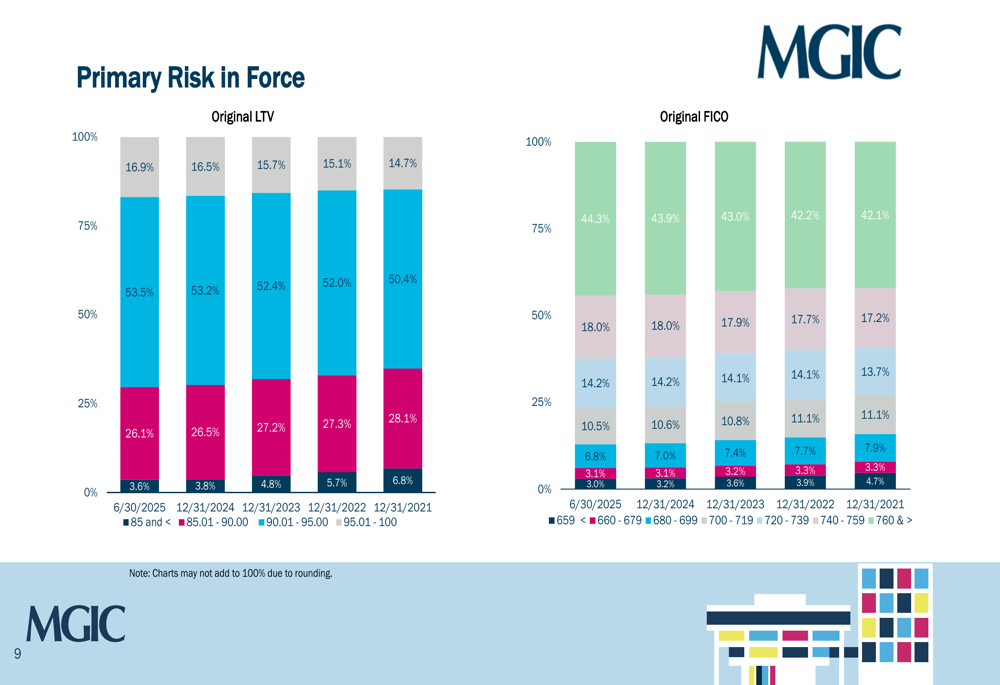

MGIC’s primary risk in force as of June 30, 2025, demonstrates strong credit quality with a weighted average FICO score of 747. The portfolio shows a healthy distribution across credit bands, with 44.3% of risk having FICO scores of 760 or higher, indicating a focus on high-quality borrowers.

As shown in the following chart breaking down the portfolio by FICO scores and loan-to-value (LTV) ratios:

The company’s loan-to-value distribution shows that 53.5% of the portfolio has original LTVs between 90.01-95.00%, with only 16.9% having LTVs above 95%. This balanced approach to risk is further supported by the portfolio’s weighted average LTV of 93.3%.

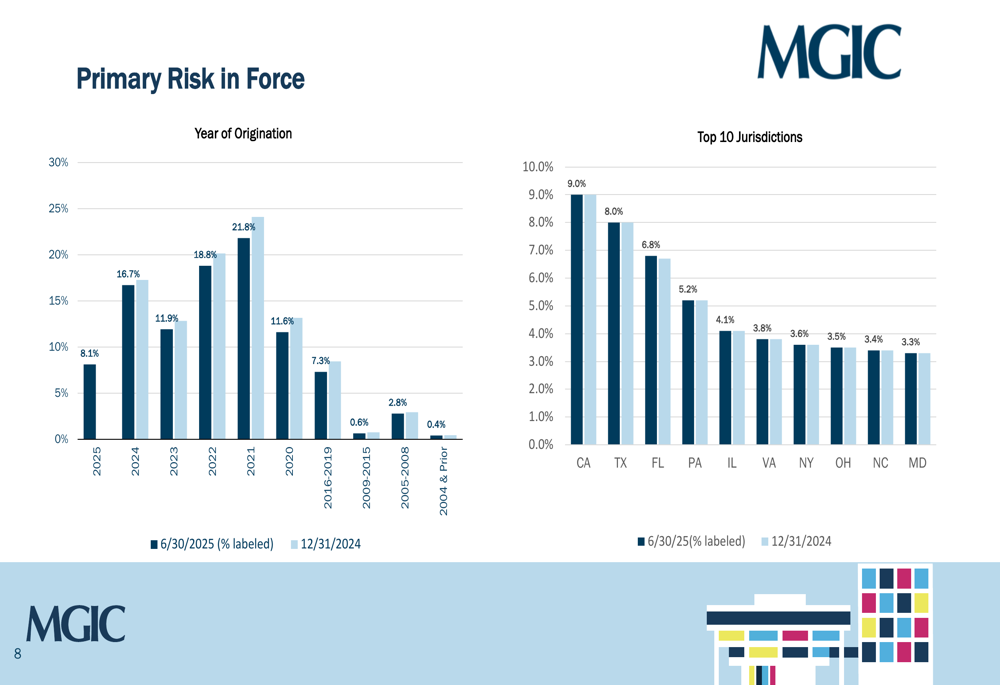

MGIC’s portfolio is well-diversified geographically, reducing concentration risk. California represents the largest state exposure at 9.0%, followed by Texas at 8.0% and Florida at 6.8%. This geographic distribution helps mitigate regional economic risks.

The following chart illustrates the company’s risk distribution by origination year and geographic jurisdiction:

The portfolio is predominantly composed of recent vintages, with loans originated between 2021-2025 accounting for 77.3% of risk in force. This concentration in newer vintages is positive as these loans were underwritten during a period of stricter credit standards and rising home values.

Risk Management Strategy

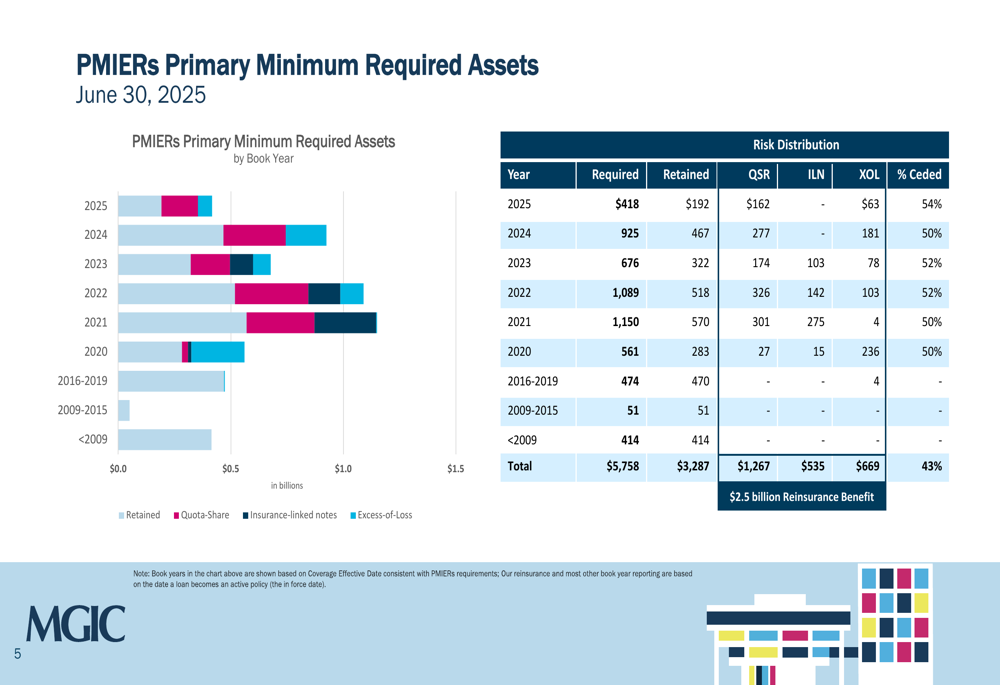

MGIC’s approach to risk management is highlighted in its PMIERs (Private Mortgage Insurer Eligibility Requirements) compliance strategy. The company maintains $5,758 million in required assets, with 43% of this risk ceded through various reinsurance structures including quota share, insurance-linked notes, and excess-of-loss coverage.

The following chart details how MGIC distributes its risk across different reinsurance structures by origination year:

This risk transfer strategy provides a $2.5 billion reinsurance benefit, enhancing the company’s capital efficiency and reducing volatility. The approach varies by vintage, with newer books having higher cession percentages – 54% for 2025 originations and 50% for 2024 originations – reflecting a strategic approach to managing capital requirements on new business.

Delinquency and Loss Performance

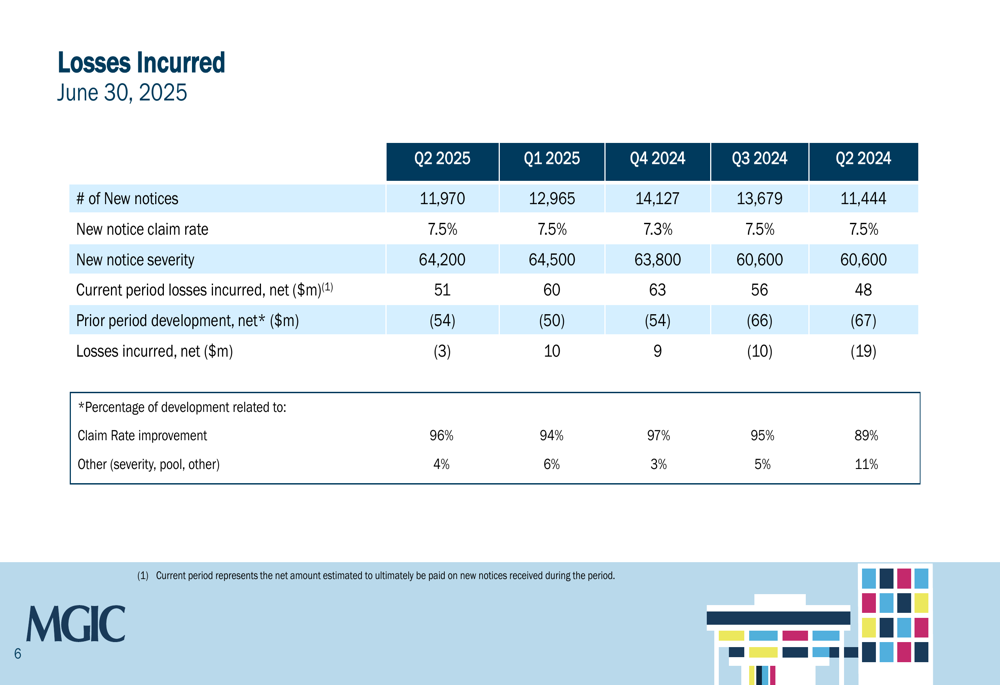

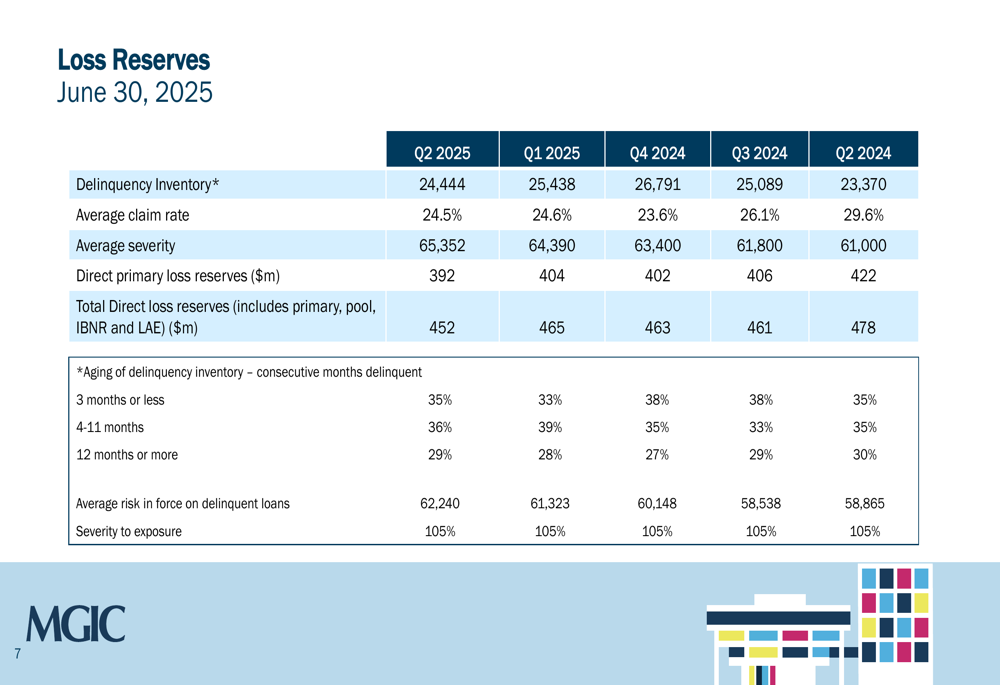

MGIC’s delinquency performance remains strong, with an overall delinquency rate of 2.2% based on loan count (1.9% based on risk in force). The company reported 24,444 delinquent loans as of Q2 2025, down from the peak of 26,791 in Q4 2024.

Loss experience has been favorable, with net losses incurred of $(3) million in Q2 2025, consisting of $51 million in current period losses offset by $(54) million in prior period development. This positive development suggests that previously established reserves have proven to be conservative as actual claim experience has been better than initially anticipated.

The following chart shows the quarterly trend in losses incurred:

The company’s new notice claim rate remained stable at 7.5% in Q2 2025, unchanged from Q2 2024, while new notice severity increased slightly to $64,200 from $60,600 a year earlier.

MGIC’s loss reserves stood at $452 million as of Q2 2025, with $392 million specifically allocated to primary losses. The average claim rate on delinquent loans was 24.5%, down from 29.6% in Q2 2024, reflecting improved expectations for cure rates.

The following table provides a detailed breakdown of the company’s loss reserves:

The aging of the delinquency inventory shows a balanced distribution, with 35% of delinquencies being 3 months or less, 36% between 4-11 months, and 29% being 12 months or more.

Capital Position

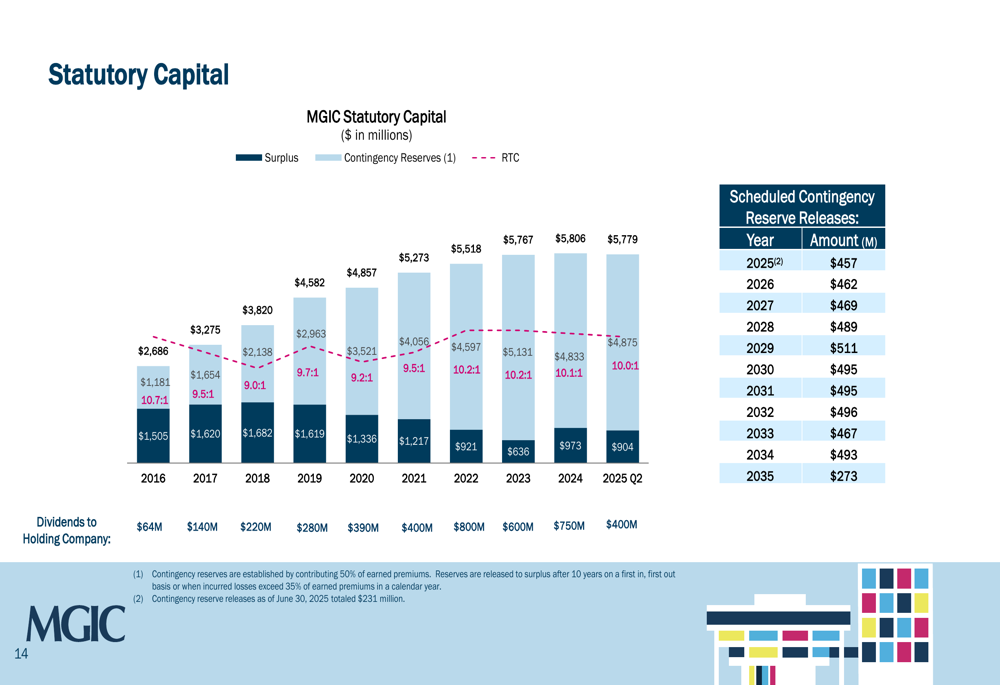

MGIC maintains a strong capital position, with substantial statutory capital including surplus and contingency reserves. The company has scheduled contingency reserve releases of $457 million for 2025, providing additional financial flexibility.

The following chart illustrates the company’s statutory capital position and future contingency reserve releases:

This strong capital position aligns with the company’s shareholder-friendly actions noted in Q1 2025, including share repurchases and dividend increases. MGIC has maintained a 6-year streak of dividend increases, demonstrating confidence in its financial strength and commitment to shareholder returns.

Forward-Looking Statements

Based on the portfolio composition and performance metrics presented, MGIC appears well-positioned to navigate the current housing market environment. The concentration in purchase loans (92.8%) rather than refinances suggests the company is less vulnerable to interest rate fluctuations affecting refinance activity.

The high credit quality of the portfolio, with 44.3% of risk having FICO scores above 760 and 98.4% being owner-occupied properties, provides a buffer against potential economic headwinds. Additionally, the effective risk transfer strategy with 43% of required assets ceded helps mitigate potential losses.

As shown in the following chart detailing loan purpose and amount distribution:

The company’s focus on conventional loan amounts (96% below conforming limits) and purchase loans suggests a conservative approach to risk that should serve it well if economic conditions deteriorate.

During the Q1 2025 earnings call, CEO Tim Mackie emphasized the importance of building relationships with key stakeholders, particularly the new FHFA Director. This regulatory engagement, combined with the strong financial metrics presented in the Q2 2025 supplement, indicates MGIC is well-positioned to maintain its leadership in the private mortgage insurance sector while navigating regulatory and market challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.