FINAL HOURS: Lock in your InvestingPro subscription for 50% off before sale ends

Introduction & Market Context

MGM Resorts International (NYSE:MGM) presented its second quarter 2025 results on July 30, revealing a mixed performance across its business segments. The company’s stock closed at $37.41, up 1.34% on the day of the presentation, reflecting investor confidence despite some challenges in its Las Vegas operations.

The global gaming and hospitality giant reported record consolidated net revenues for the quarter, driven by strong performances in its regional operations and MGM China (OTC:MCHVY) segments, while its digital business continued to show promising growth. These positive developments helped offset a year-over-year decline in Las Vegas Strip revenue.

Quarterly Performance Highlights

MGM Resorts reported Q2 net income of $49 million, with several business segments achieving record results. The company highlighted its EBITDA enhancement initiatives, which are on pace to reach $200 million, with over $150 million expected to be implemented in 2025.

Market expansion remains a key focus, with New York awarding gaming licenses in December, the Dubai project on track for the second half of 2028, and MGM Osaka construction proceeding as planned for a 2030 opening.

As shown in the following summary of key quarterly highlights:

Segment Performance Analysis

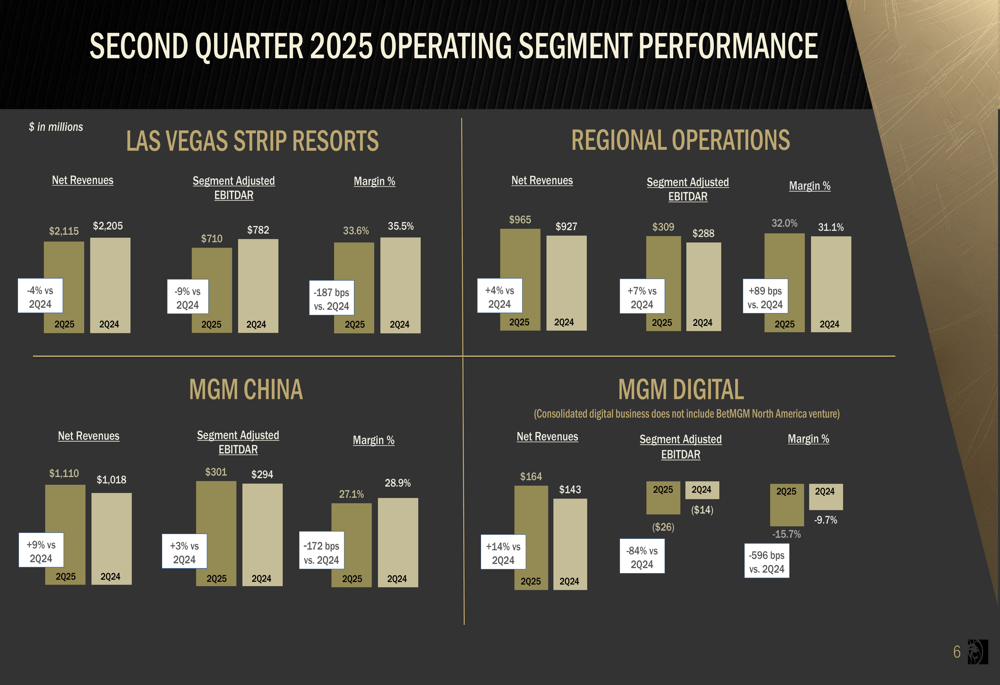

MGM’s Q2 2025 results revealed divergent performance across its operating segments. Las Vegas Strip Resorts experienced a 4% year-over-year decline in net revenues to $2,115 million, with Segment Adjusted EBITDAR falling 9% to $710 million. This resulted in a margin contraction of 187 basis points to 33.6%.

In contrast, Regional Operations delivered record net revenues of $965 million, up 4% compared to Q2 2024, with Segment Adjusted EBITDAR increasing 7% to $309 million. The segment’s margin improved by 89 basis points to 32.0%.

MGM China continued its strong recovery, with net revenues rising 9% to $1,110 million and Segment Adjusted EBITDAR increasing 3% to $301 million, representing an all-time record. However, margin decreased by 172 basis points to 27.1%.

The following chart details the performance of each operating segment:

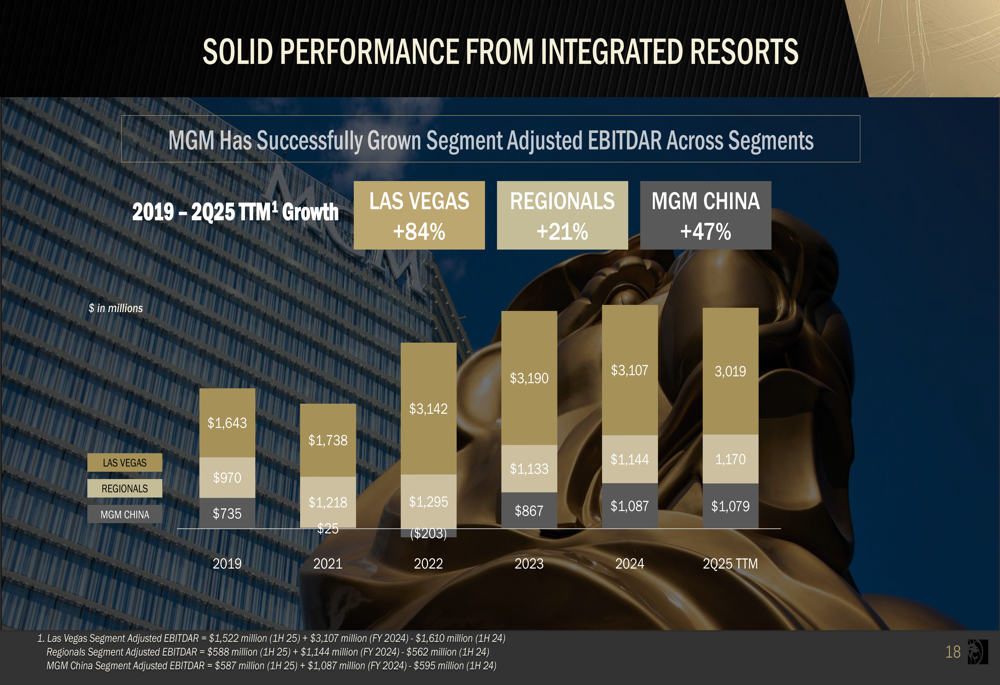

Looking at longer-term trends, MGM’s integrated resorts have shown remarkable growth since 2019, with Las Vegas Adjusted EBITDAR up 84%, Regional operations up 21%, and MGM China up 47%, demonstrating the company’s resilience and recovery from the pandemic:

Digital Operations & Growth Strategy

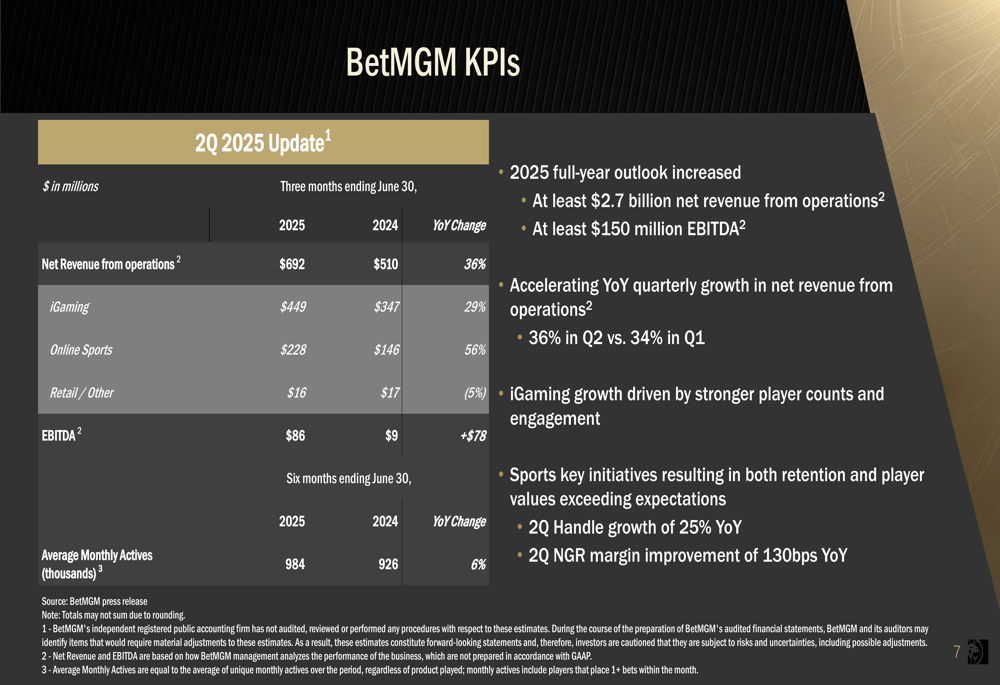

BetMGM, MGM’s joint venture with Entain, delivered exceptional results in Q2 2025, with net revenue from operations reaching $692 million, a 36% increase year-over-year. The digital platform showed particularly strong growth in online sports betting, which increased 56% to $228 million, while iGaming revenue grew 29% to $449 million.

Most notably, BetMGM’s EBITDA improved dramatically to $86 million, compared to just $9 million in Q2 2024. Based on this strong performance, the company increased its full-year outlook, now expecting at least $2.7 billion in net revenue from operations and at least $150 million in EBITDA.

The detailed BetMGM performance metrics are illustrated below:

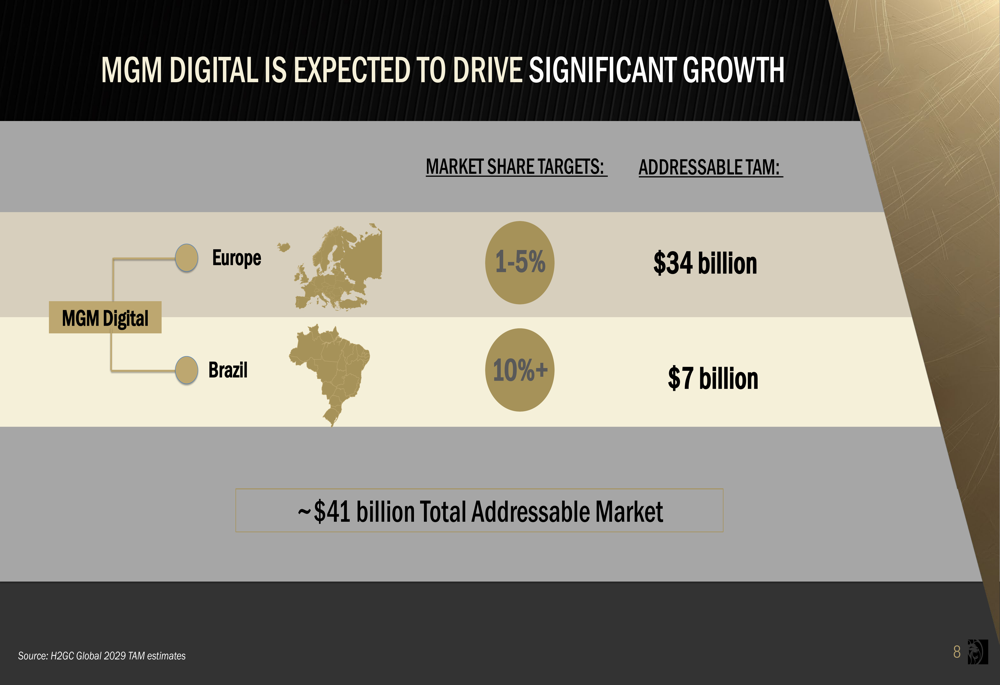

Meanwhile, MGM Digital is pursuing ambitious international expansion, targeting market share of 1-5% in Europe’s $34 billion TAM and over 10% in Brazil’s $7 billion TAM. The company is making progress in Brazil and continues to invest in its digital infrastructure, including the MGM Live Studio at MGM Grand, which streams 24/7 to fully regulated markets.

Capital Allocation & Shareholder Returns

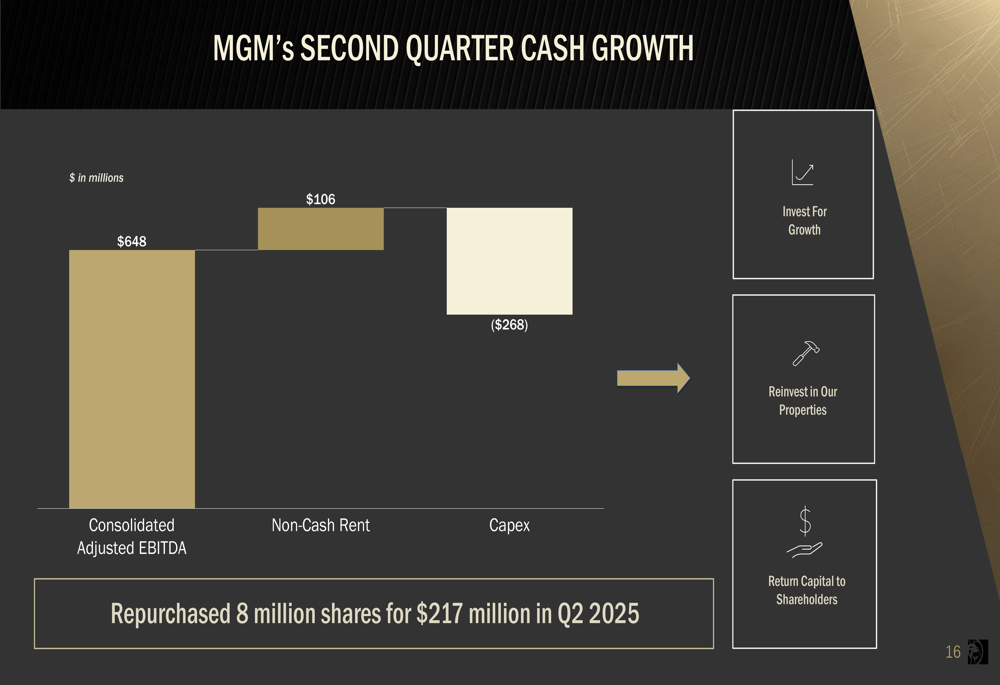

MGM Resorts continues to generate strong cash flow while balancing investments in growth projects and returning capital to shareholders. In Q2 2025, the company reported Consolidated Adjusted EBITDA of $648 million and repurchased 8 million shares for $217 million.

The following chart illustrates MGM’s cash flow generation and allocation during the quarter:

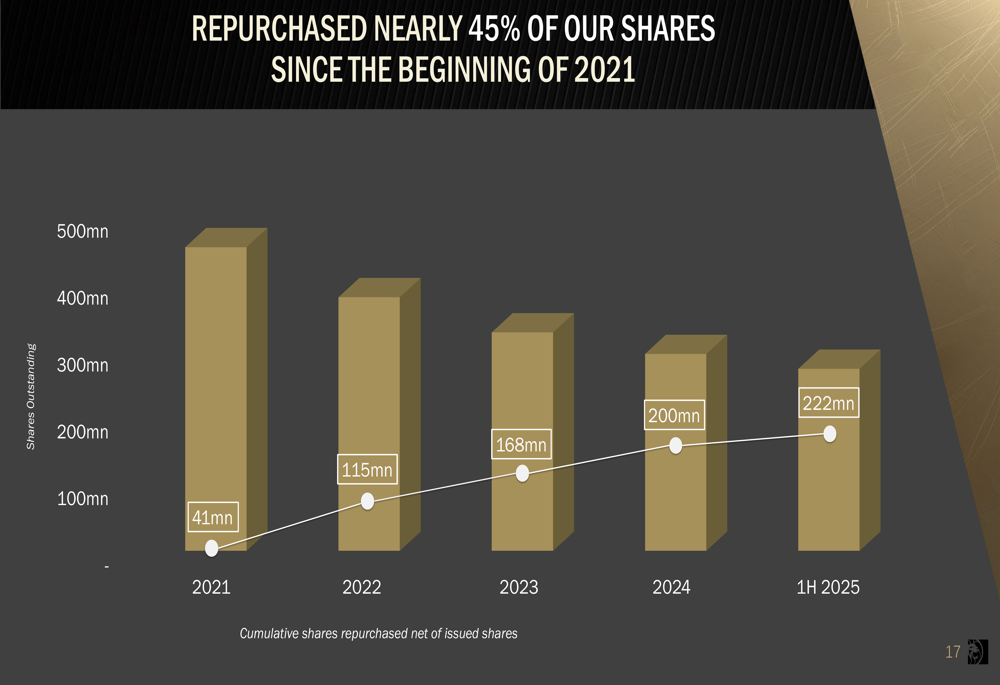

The company has maintained an aggressive share repurchase program, buying back nearly 45% of its outstanding shares since the beginning of 2021. In the first half of 2025 alone, MGM repurchased 22 million shares, continuing the trend of significant capital returns to shareholders:

As of June 30, 2025, MGM maintained a strong liquidity position with $2.16 billion in consolidated cash and cash equivalents, plus $4.43 billion in revolver availability, bringing total liquidity to $6.59 billion.

Forward-Looking Statements & Outlook

Looking ahead, MGM Resorts provided key financial forecasts for 2025, including corporate expense projections of $440-475 million and capital expenditures of approximately $750-800 million domestically. The company expects to receive a domestic net cash tax refund of at least $100 million.

MGM’s global expansion strategy continues to progress, with development underway for integrated resorts in Japan and Dubai. The company aims to strengthen its position as the world’s premier gaming entertainment company by capitalizing on opportunities in Las Vegas, U.S. regional markets, international locations, and online platforms.

The Las Vegas Strip has demonstrated remarkable resilience over the past three decades, with a 4% CAGR in gross gaming revenue since 1990, reaching new all-time highs in 16 of the past 34 years despite major disruptions like 9/11, the Great Financial Crisis, and the COVID-19 pandemic. This long-term growth trend supports MGM’s continued investment in its flagship market.

MGM Resorts’ Q2 2025 presentation reveals a company successfully navigating the evolving gaming landscape through geographic diversification, digital expansion, and strategic capital allocation. While Las Vegas operations showed some softness compared to the prior year, the strong performance in regional markets, China, and digital platforms demonstrates the benefits of the company’s balanced portfolio approach.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.