Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Middleby Corporation (NASDAQ:MIDD) presented its second quarter 2025 earnings results on August 6, showing modest revenue declines amid tariff headwinds but unveiling significant strategic initiatives including a planned spin-off of its Food Processing segment. The company’s stock traded up 0.95% in premarket at $146.09, building on yesterday’s 2.04% gain, as investors digested the mixed results alongside ambitious restructuring plans.

The foodservice equipment manufacturer reported a 1.4% year-over-year revenue decline to $977.9 million, continuing the challenging trend seen in Q1 when the company beat earnings estimates despite revenue shortfalls. The latest results show Middleby navigating a complex operating environment characterized by tariff impacts and varying segment performance.

Quarterly Performance Highlights

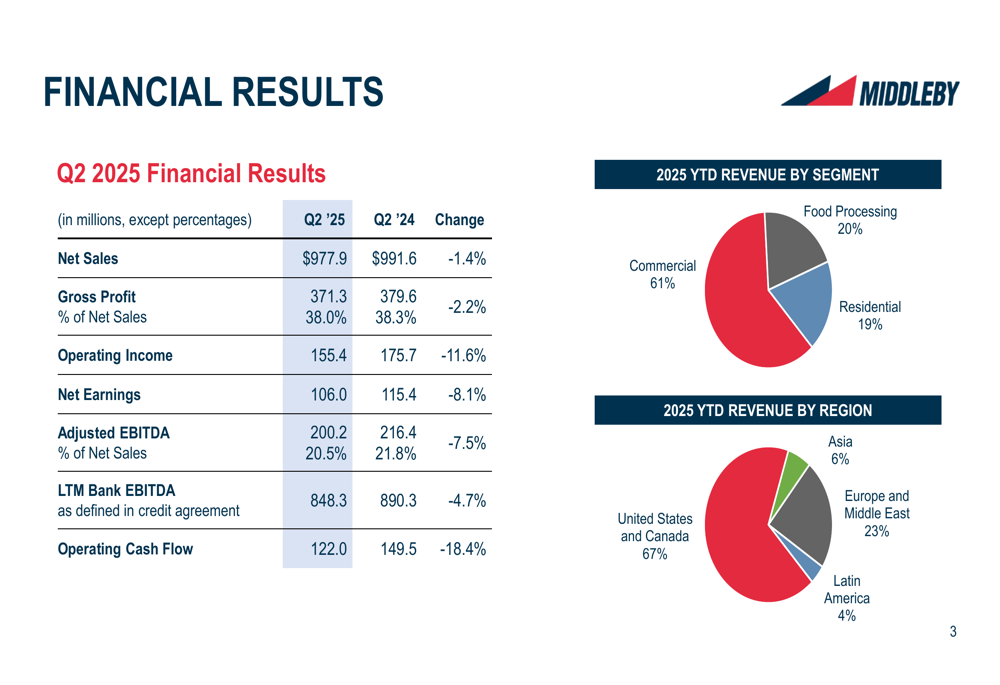

Middleby reported Q2 2025 net sales of $977.9 million, down 1.4% from $991.6 million in Q2 2024. Net earnings decreased 8.1% to $106.0 million, while adjusted EBITDA fell 7.5% to $200.2 million with margins contracting from 21.8% to 20.5%. Operating cash flow declined 18.4% to $122.0 million compared to the prior year.

The company’s revenue mix remains heavily weighted toward North America, with the United States and Canada accounting for 67% of year-to-date revenue. By segment, Commercial Foodservice continues to dominate at 61% of revenue, followed by Food Processing at 20% and Residential Kitchen at 19%.

As shown in the following financial overview:

Segment Performance Analysis

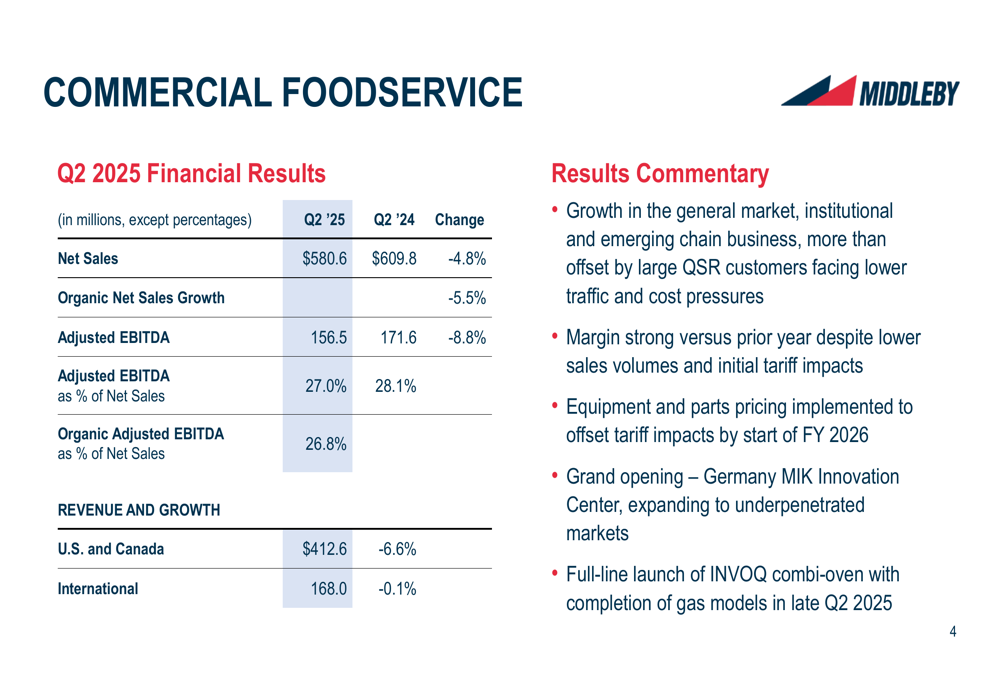

The Commercial Foodservice segment, Middleby’s largest business unit, posted net sales of $580.6 million, down 4.8% year-over-year with organic sales declining 5.5%. Despite volume challenges and initial tariff impacts, the segment maintained strong margins at 27.0% adjusted EBITDA. Management noted growth in general market, institutional and emerging chains, offset by challenges with large quick-service restaurant customers.

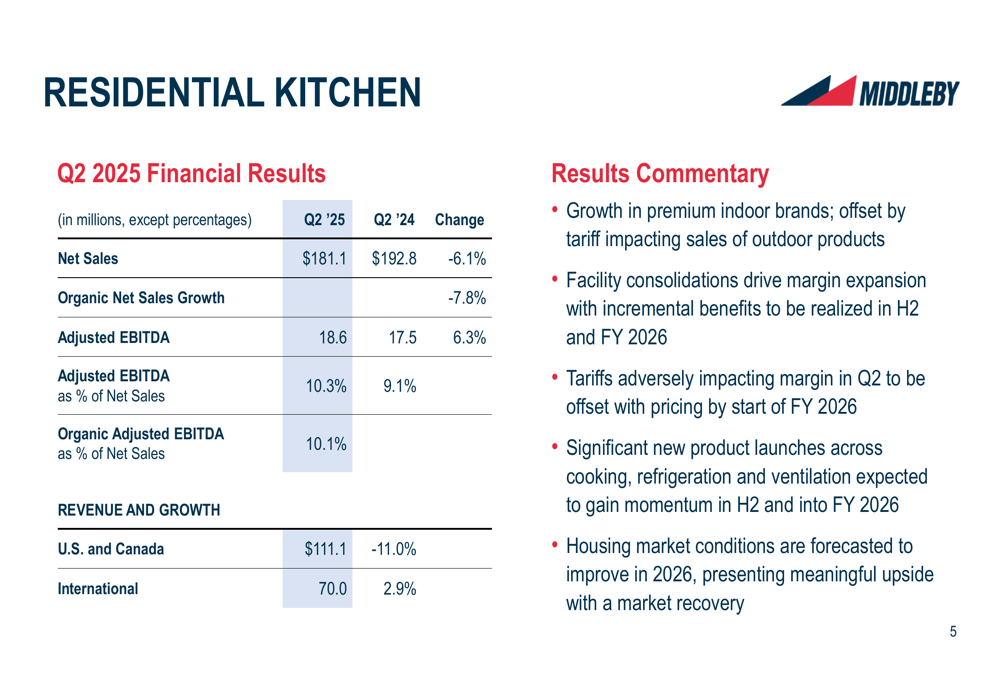

The Residential Kitchen segment reported net sales of $181.1 million, a 6.1% decrease from Q2 2024. Despite the revenue decline, adjusted EBITDA increased 6.3% to $18.6 million, with margins expanding from 9.1% to 10.3%. The company highlighted growth in premium indoor brands and margin improvements from facility consolidations, partially offset by tariff impacts.

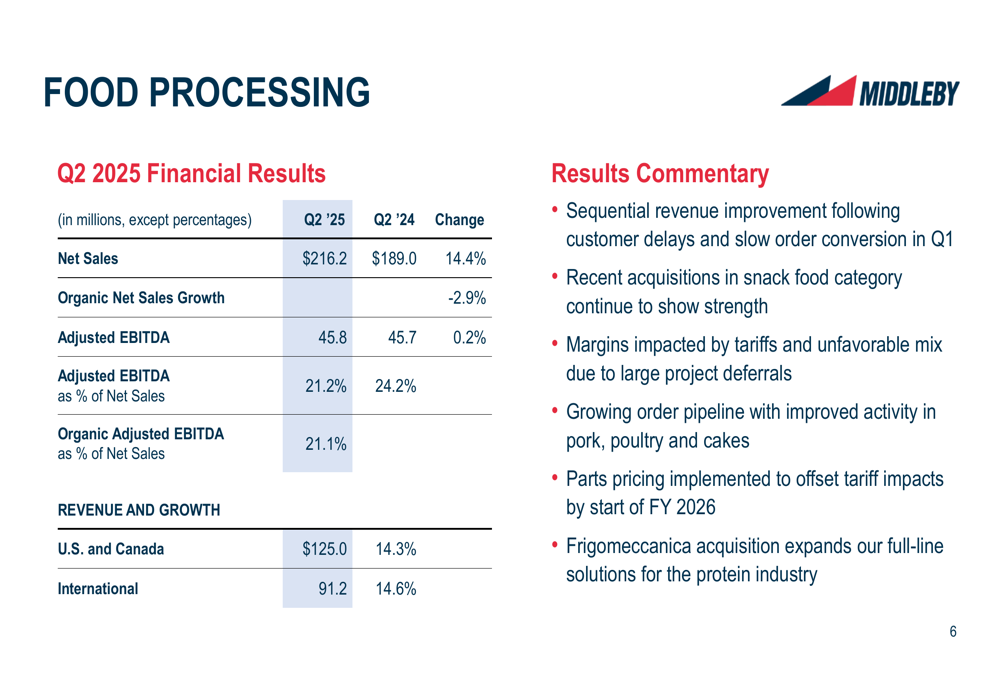

The Food Processing segment was the standout performer with net sales of $216.2 million, up 14.4% year-over-year, though organic sales declined 2.9%. Adjusted EBITDA remained essentially flat at $45.8 million, with margins contracting from 24.2% to 21.2% due to tariff impacts and unfavorable mix. Management noted a growing order pipeline and the strategic acquisition of Frigomeccanica.

The following segment details illustrate the varying performance:

Tariff Impact and Mitigation Strategies

Tariffs emerged as a significant headwind for Middleby in Q2, with the company now projecting a $150 million annual impact. The company experienced approximately $10 million in tariff-related costs during Q2 and expects $10-15 million in Q3 and $5-10 million in Q4, net of pricing actions.

Management emphasized that Middleby’s large U.S. manufacturing footprint and global scale position the company to navigate tariffs better than competitors. China and India represent roughly 50% of the identified cost exposure. The company has implemented price increases in Q3 2025 and expects to fully offset tariff impacts by the start of fiscal year 2026 through a combination of pricing and operational initiatives.

This represents a refinement of previous guidance, as the Q1 earnings report had estimated tariff impacts at $150-200 million annually. The more precise $150 million figure and detailed quarterly impact projections suggest the company has gained better visibility into the challenges ahead.

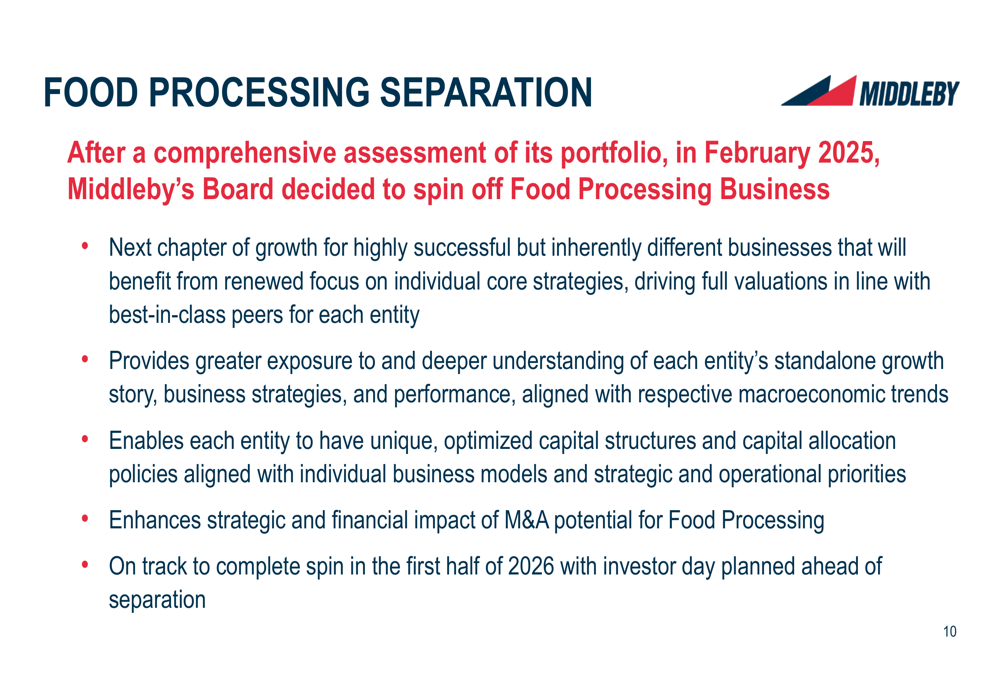

Strategic Initiatives: Food Processing Spin-off

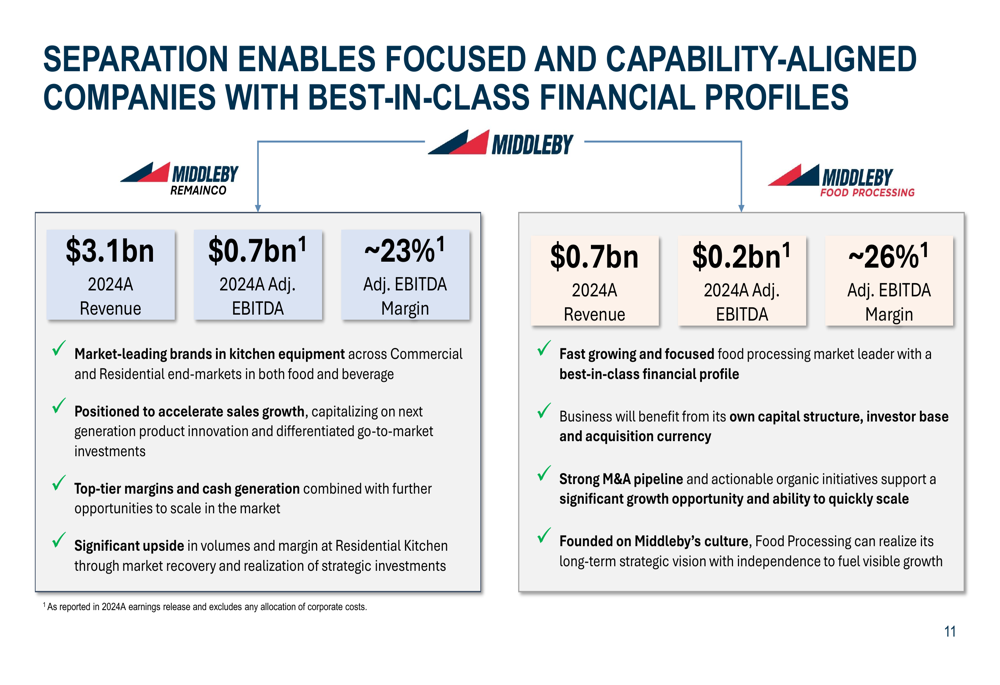

In a major strategic development, Middleby announced plans to spin off its Food Processing business in the first half of 2026, following a comprehensive assessment that began in February 2025. The separation aims to create two focused, capability-aligned companies with distinct growth strategies and capital structures.

The company provided the following rationale for the spin-off:

Post-separation, Middleby RemainCo is expected to generate approximately $3.1 billion in revenue with $0.7 billion in adjusted EBITDA at approximately 23% margin. The spun-off Middleby Food Processing business is projected to have $0.7 billion in revenue with $0.2 billion in adjusted EBITDA at approximately 26% margin.

The following slide illustrates the expected financial profiles of both companies:

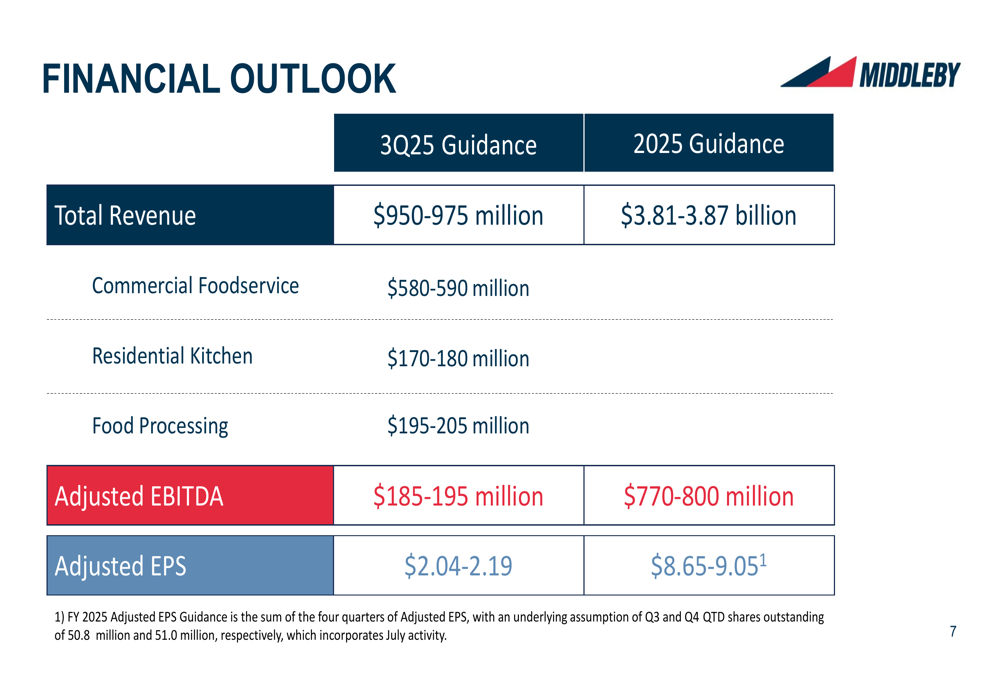

Financial Outlook

Looking ahead, Middleby provided guidance for both Q3 2025 and the full year. For Q3, the company projects total revenue of $950-975 million, with the Commercial Foodservice segment contributing $580-590 million, Residential Kitchen $170-180 million, and Food Processing $195-205 million. Adjusted EBITDA is expected to be $185-195 million with adjusted EPS of $2.04-2.19.

For the full year 2025, Middleby forecasts total revenue of $3.81-3.87 billion, adjusted EBITDA of $770-800 million, and adjusted EPS of $8.65-9.05.

The detailed financial outlook is presented below:

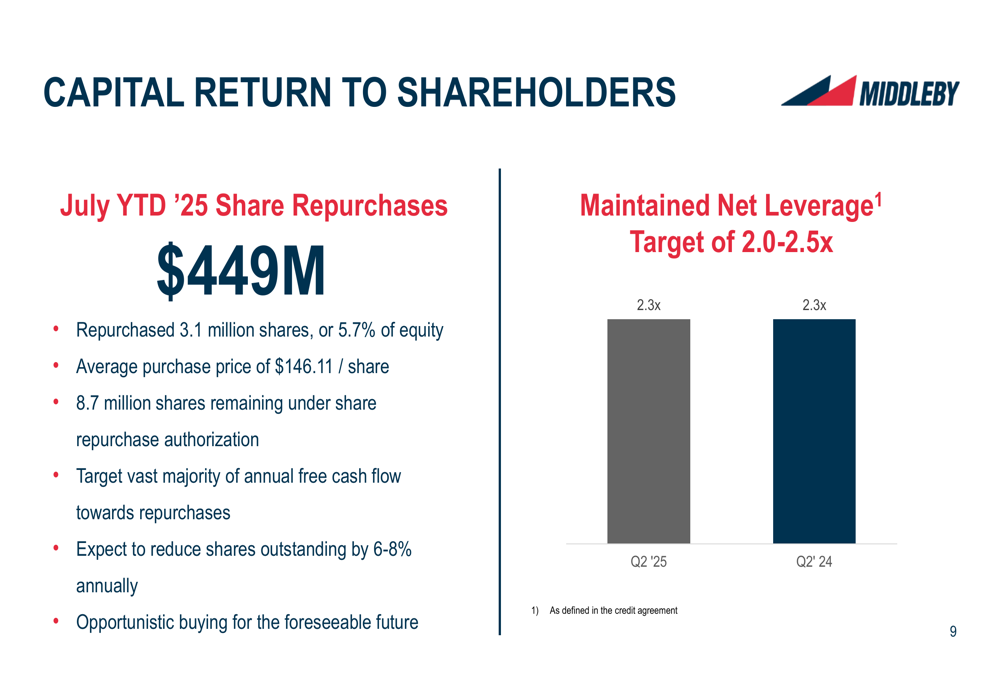

Capital Allocation and Shareholder Returns

Middleby continues to prioritize share repurchases as a key component of its capital allocation strategy. Year-to-date through July 2025, the company has repurchased $449 million worth of shares, representing 3.1 million shares or 5.7% of equity at an average price of $146.11 per share. The company maintains 8.7 million shares remaining under its repurchase authorization.

Management stated its intention to direct the "vast majority" of annual free cash flow toward repurchases, targeting a 6-8% annual reduction in shares outstanding. The company also aims to maintain net leverage between 2.0x and 2.5x, with Q2 2025 leverage at 2.3x, unchanged from the prior year.

The following chart details the company’s capital return to shareholders:

Middleby’s Q2 results and strategic announcements reflect a company navigating near-term challenges while positioning for long-term growth through portfolio optimization and continued investment in innovation. The planned Food Processing spin-off represents a significant strategic shift that could unlock shareholder value by creating two focused entities with distinct growth profiles and market opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.