Can anything shut down the Gold rally?

Introduction & Market Context

MidWestOne Financial Group (NASDAQ:MOFG) presented its second quarter 2025 earnings results on July 25, revealing a mixed performance characterized by improved interest margins but declining profitability and emerging credit quality concerns. The regional bank, which closed at $29.86 before the presentation, has seen its stock decline by 2.28% to $28.46 amid investor concerns about deteriorating asset quality metrics.

The Q2 results follow a challenging first quarter where the bank met EPS expectations but missed on revenue targets. The latest presentation shows further pressure on earnings despite progress on strategic initiatives and continued loan growth.

Quarterly Performance Highlights

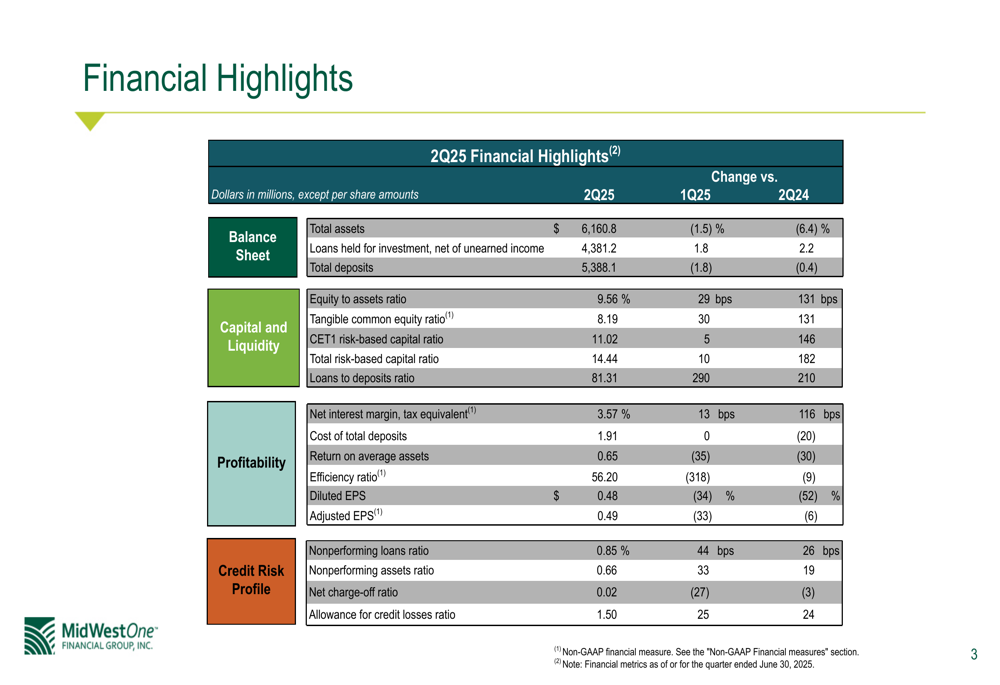

MidWestOne reported diluted earnings per share of $0.48 for the second quarter, representing a significant 34% decline from the previous quarter’s $0.73 and a 52% drop year-over-year. Adjusted EPS came in slightly higher at $0.49, still down 33% quarter-over-quarter and 6% year-over-year.

Despite these earnings challenges, the bank’s net interest margin improved to 3.57%, up 13 basis points from the previous quarter and 116 basis points year-over-year, reflecting better loan yields in the rising rate environment.

As shown in the following financial highlights table, the bank maintained growth in loans while deposits declined slightly:

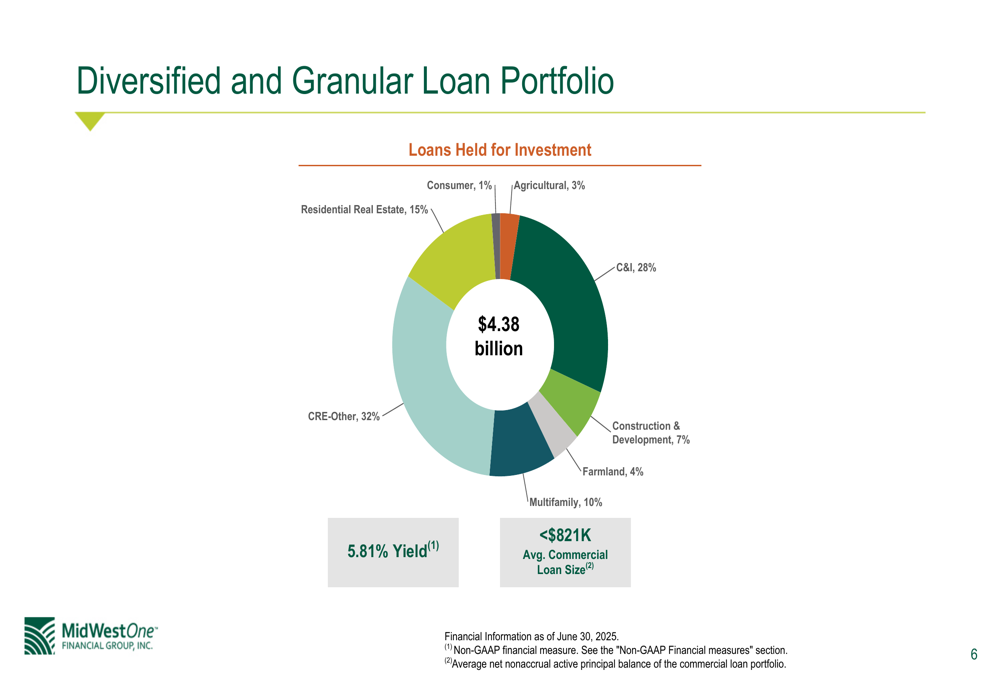

Total (EPA:TTEF) assets decreased to $6.16 billion, down 1.5% from the previous quarter and 6.4% year-over-year. Loans held for investment grew to $4.38 billion, up 1.8% quarter-over-quarter and 2.2% year-over-year, while deposits declined to $5.39 billion, down 1.8% from the previous quarter.

The efficiency ratio improved to 56.20%, down 318 basis points from the previous quarter, indicating better cost control. However, return on average assets declined to 0.65%, down from 1.0% in the first quarter, reflecting pressure on overall profitability.

Credit Quality and Risk Profile

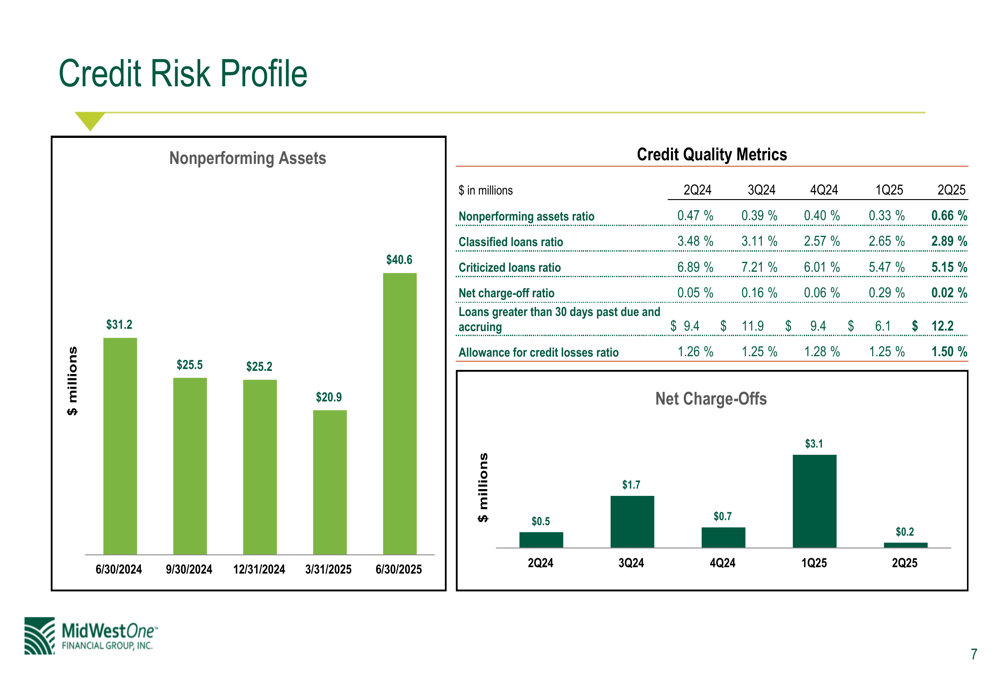

A concerning trend in MidWestOne’s Q2 results is the deterioration in credit quality metrics. The nonperforming loans ratio increased to 0.85%, up 44 basis points quarter-over-quarter and 26 basis points year-over-year. Similarly, the nonperforming assets ratio rose to 0.66%, up 33 basis points from the previous quarter.

The following chart illustrates the upward trend in nonperforming assets, which increased to $40.6 million in June 2025 from $20.9 million in March 2025:

In response to these credit quality concerns, the bank increased its allowance for credit losses ratio to 1.50%, up 25 basis points from the previous quarter. Net charge-offs, however, decreased significantly to 0.02% from 0.29% in the first quarter.

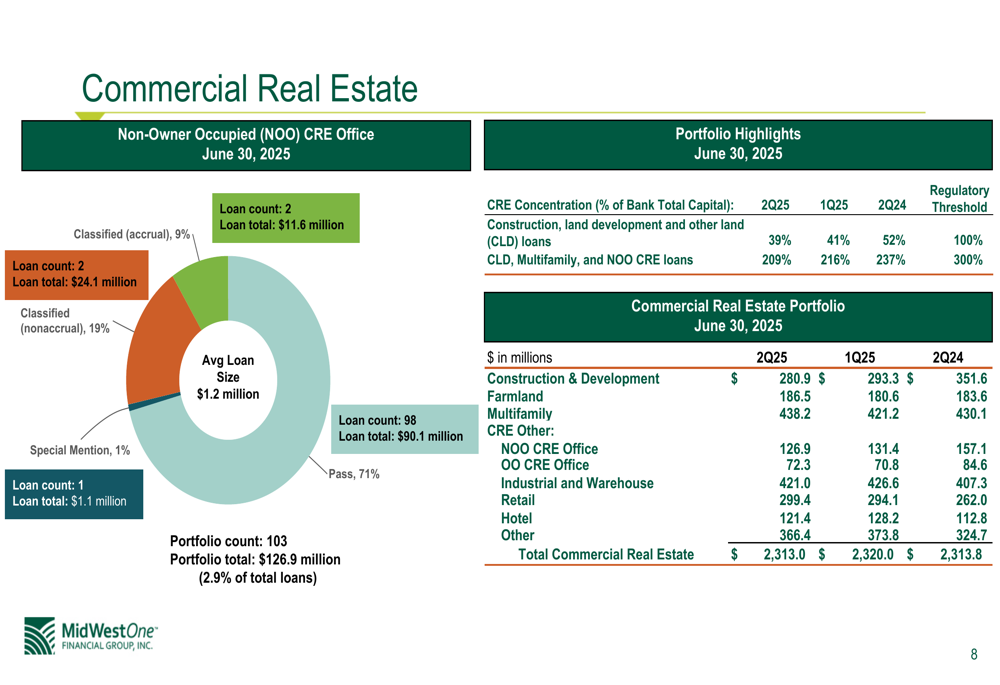

The commercial real estate portfolio, particularly non-owner-occupied office properties, shows signs of stress. Of the 103 loans in this category totaling $126.9 million, 28% are classified as either nonaccrual (19%) or classified accrual (9%), representing a potential risk area for the bank.

Balance Sheet and Investment Portfolio

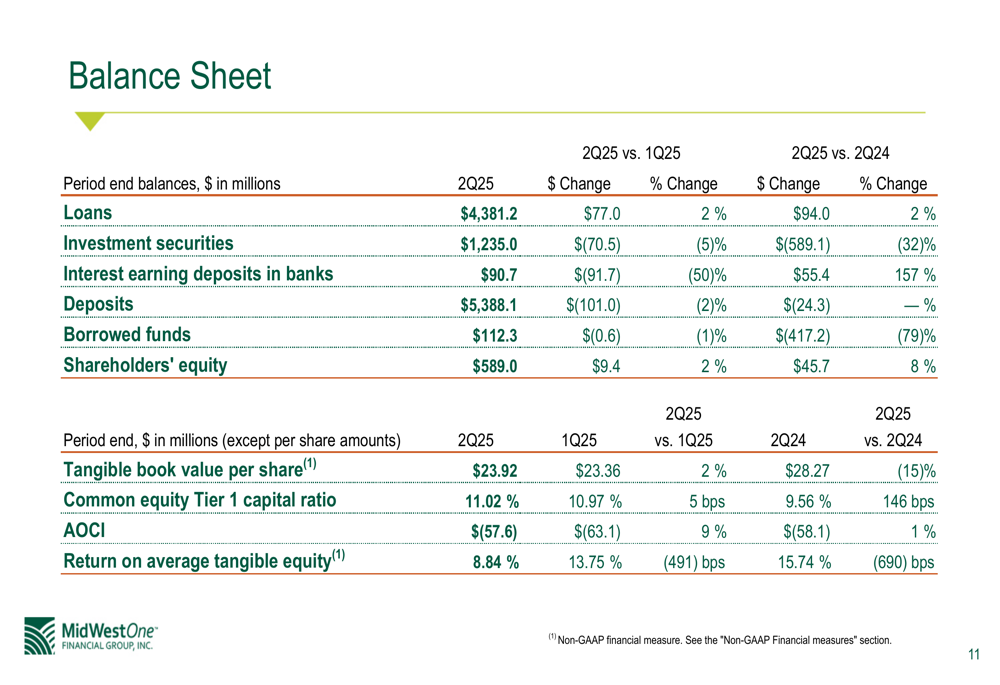

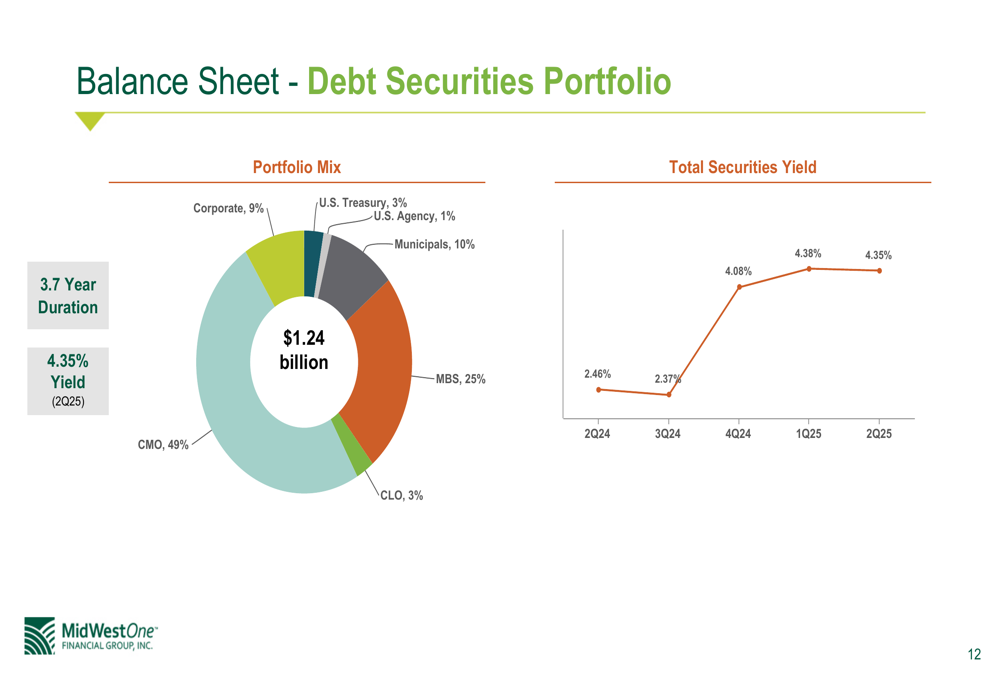

MidWestOne’s balance sheet shows a shift toward higher-yielding loans and away from investment securities. The loan portfolio grew by $77 million quarter-over-quarter while investment securities decreased by $70.5 million.

The bank’s investment securities portfolio, totaling $1.24 billion, has a duration of 3.7 years and a yield of 4.35%, up significantly from 2.46% a year earlier. The portfolio is primarily composed of CMOs (49%) and MBS (25%), with smaller allocations to municipals, corporates, and other securities.

The loan portfolio remains well-diversified across various sectors, with commercial real estate (excluding multifamily) representing the largest concentration at 32%, followed by commercial and industrial loans at 28%. The weighted average yield on the loan portfolio stands at 5.81%.

Strategic Initiatives

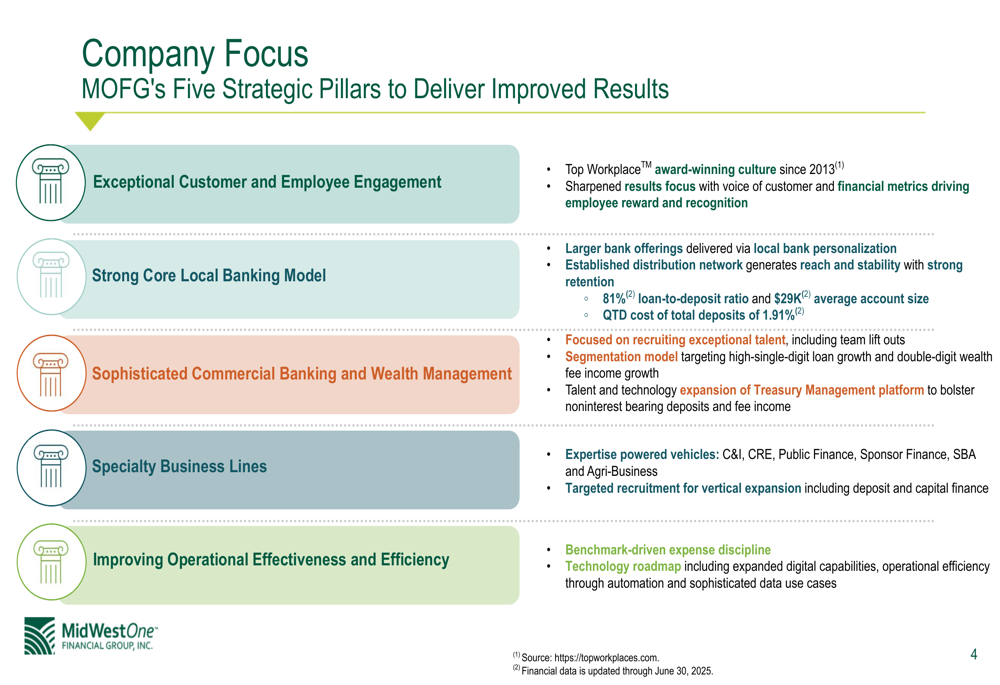

Despite the challenging quarter, MidWestOne continues to execute on its strategic plan, focusing on five key pillars: customer and employee engagement, core local banking, commercial banking and wealth management, specialty business lines, and operational efficiency.

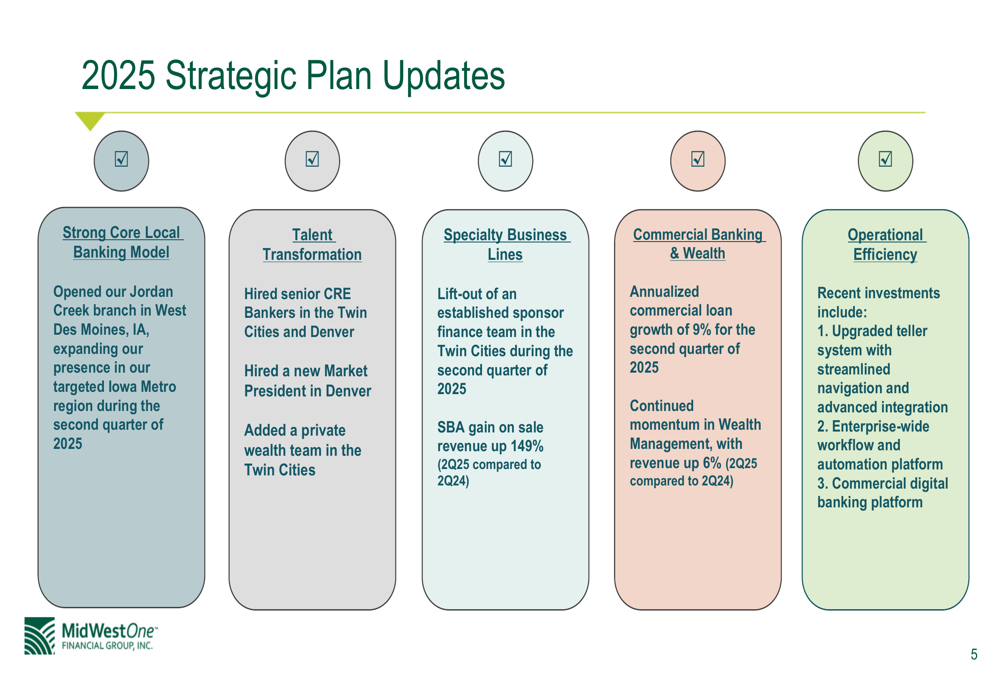

The bank reported progress on several strategic initiatives, including opening a new Jordan Creek branch, hiring senior CRE bankers, establishing a sponsor finance team, and upgrading its teller system. Commercial loan growth reached an annualized rate of 9%, exceeding the overall loan growth rate.

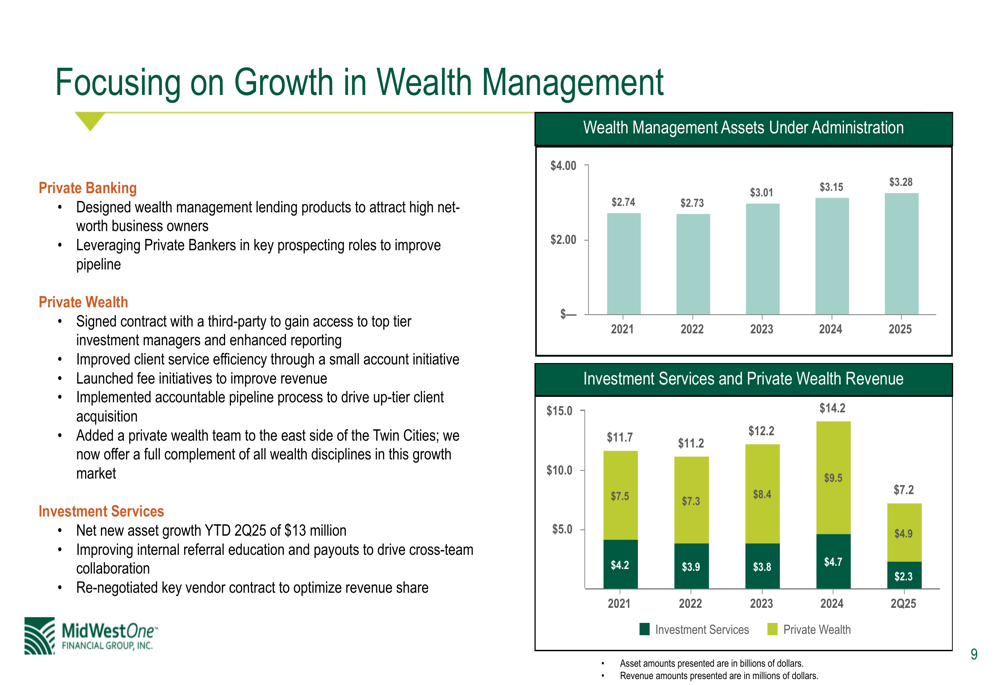

Wealth management remains a bright spot in MidWestOne’s business, with assets under administration growing to $3.28 billion in 2025 from $2.74 billion in 2021. Investment services and private wealth revenue has also shown strong growth, increasing from $4.2 million in 2021 to $7.2 million in 2025.

Forward-Looking Statements

Looking ahead, MidWestOne faces several challenges, including managing credit quality in its commercial real estate portfolio and reversing the trend of declining profitability. The bank’s improved net interest margin provides some cushion, but continued pressure on noninterest income and rising credit costs could impact future earnings.

The bank’s capital position remains strong, with the CET1 risk-based capital ratio at 11.02%, up 5 basis points from the previous quarter and 146 basis points year-over-year. This provides flexibility to manage through potential credit challenges while continuing to invest in strategic initiatives.

While MidWestOne had previously projected mid-single-digit loan growth for Q2 2025, the actual 1.8% growth fell short of this target. Investors will be watching closely to see if the bank can maintain its loan growth momentum while addressing the emerging credit quality concerns in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.