US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

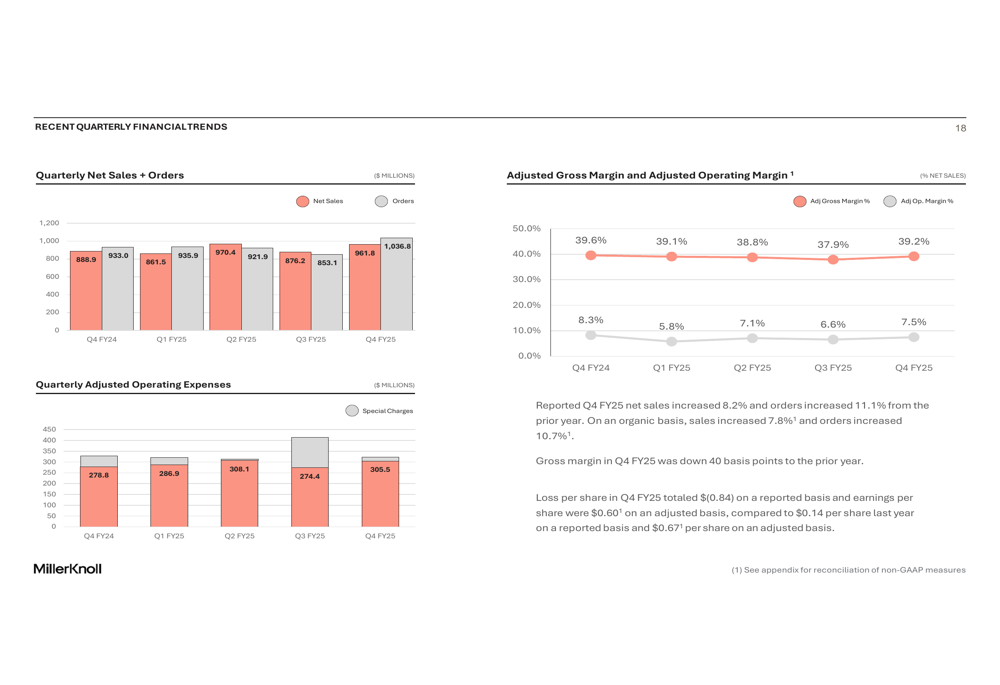

MillerKnoll Inc. (NASDAQ:MLKN) reported fourth-quarter fiscal 2025 results that exceeded analyst expectations, with net sales increasing 8.2% year-over-year to $961.8 million, outpacing the anticipated $913.8 million. The company’s adjusted earnings per share came in at $0.60, significantly above the forecasted $0.44, representing a 36.36% positive surprise. Following the announcement, MillerKnoll’s stock rose 1.58% in aftermarket trading, reflecting investor optimism despite ongoing challenges in the office furniture market.

The company’s performance comes amid mixed macroeconomic indicators, with improving CEO confidence and architect billing indexes suggesting potential tailwinds for the contract furniture business, while consumer sentiment metrics remain volatile.

Quarterly Performance Highlights

MillerKnoll’s fourth quarter showed notable improvement in sales momentum, with orders increasing 11.1% compared to the prior year. On an organic basis, sales increased 7.8% and orders grew 10.7%. The company maintained a solid gross margin of 39.2% in Q4, though this represented a 40 basis point decline from the same period last year.

As shown in the following quarterly financial trends chart, the company has demonstrated sequential improvement in sales while managing operating expenses:

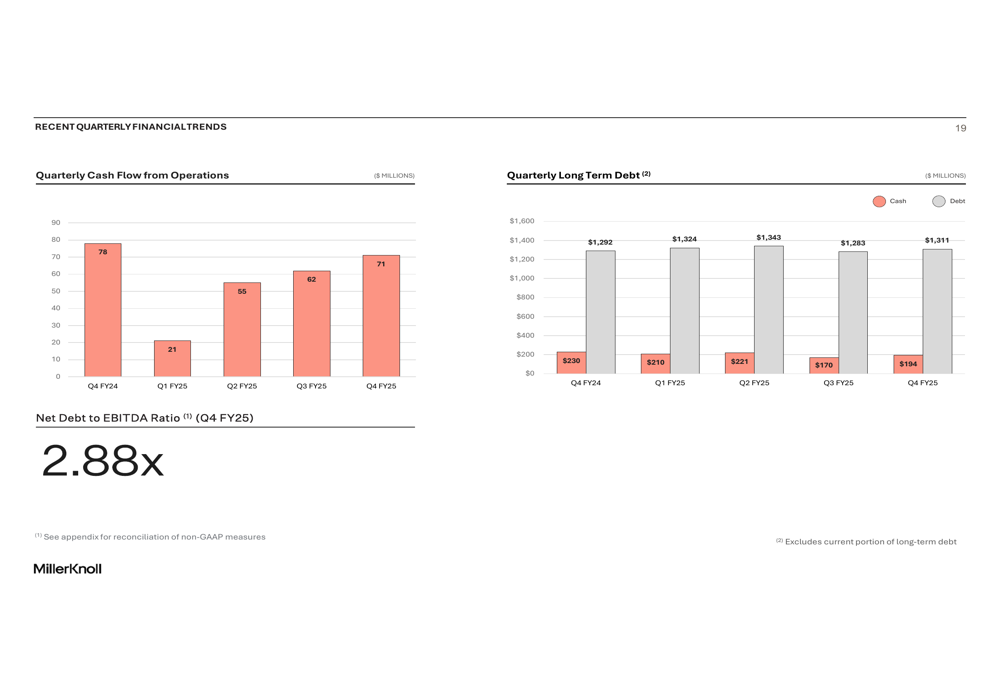

Cash flow from operations remained strong at $71 million for Q4 FY25, contributing to the company’s full-year operating cash flow of $209 million. This represents a decline from the $352 million generated in FY24 but remains substantially positive compared to pandemic-affected periods.

The company’s debt position remained relatively stable, with long-term debt at $1,311 million and cash of $194 million at quarter-end, resulting in a net debt to EBITDA ratio of 2.88x.

Full-Year Financial Analysis

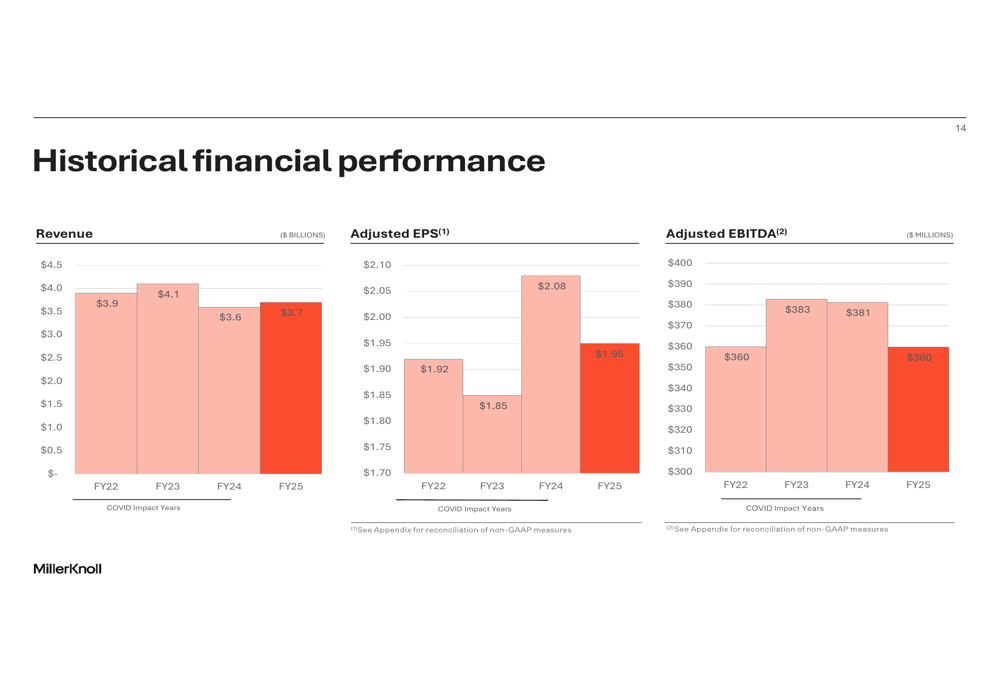

For the full fiscal year 2025, MillerKnoll reported revenue of $3.7 billion, showing modest improvement from the $3.6 billion reported in FY24 but still below pre-pandemic levels. Adjusted earnings per share for FY25 came in at $1.95, down from $2.08 in FY24, reflecting ongoing margin pressures and challenging market conditions.

The company’s historical financial performance reveals the impact of post-pandemic adjustments and integration efforts following the Knoll acquisition:

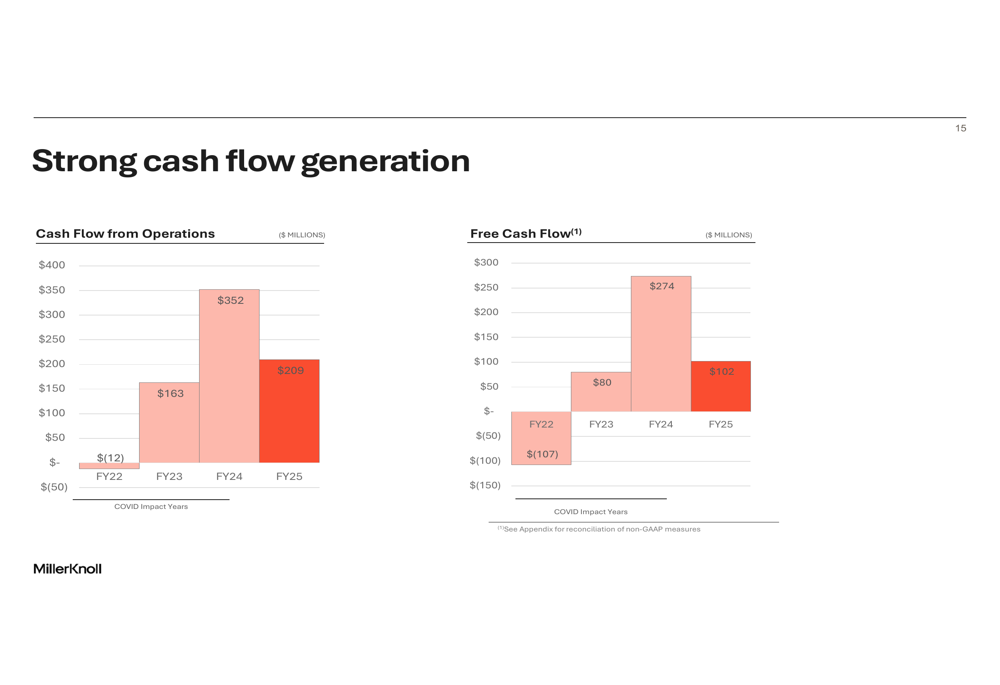

Cash flow generation has shown significant volatility over recent years, with FY25 free cash flow of $102 million representing a substantial decline from the $274 million generated in FY24:

Strategic Positioning

MillerKnoll maintains a strong competitive position through its portfolio of 15 design brands spanning both commercial and residential markets. The company operates through three primary segments: North America Contract (54% of revenue), Global Retail (28%), and International Contract (18%).

As illustrated in the following brand portfolio overview, MillerKnoll owns many of the industry’s most recognized design brands:

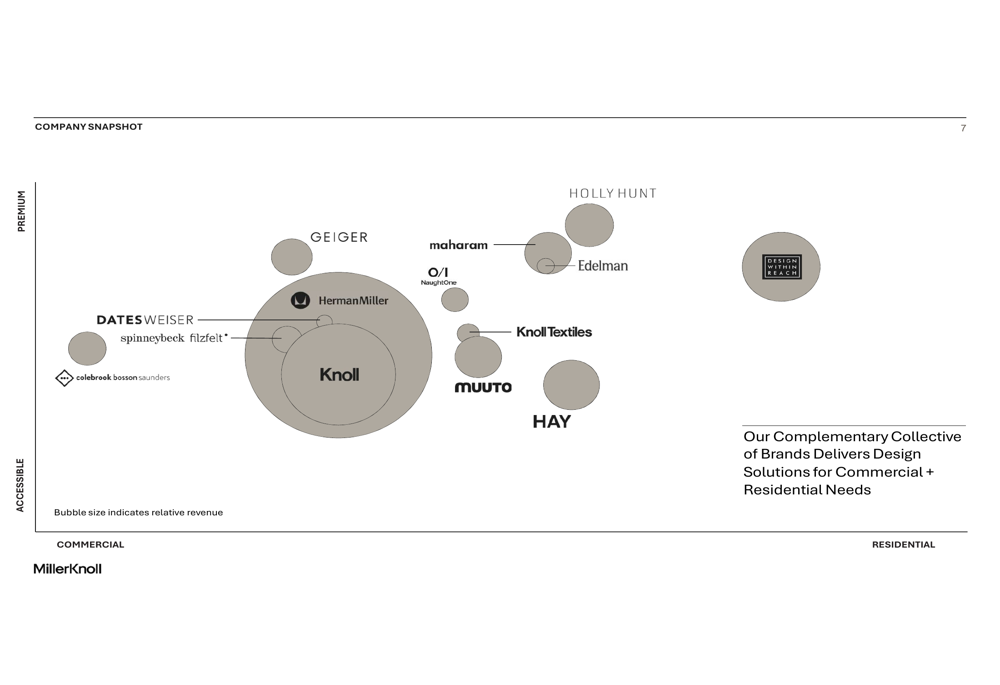

The company strategically positions these brands across different market segments, from premium to accessible price points and from commercial to residential applications:

MillerKnoll’s competitive advantages stem from its design leadership, diversified business model, global scale, brand portfolio, and talent. The company’s global manufacturing footprint includes facilities across North America, Europe, Asia, and Latin America, employing a hub-and-spoke model that emphasizes localized production closer to customers.

Capital Allocation and Balance Sheet

MillerKnoll’s capital allocation strategy balances investments in growth, debt management, and shareholder returns. The company expects capital expenditures of $120-130 million in FY26, up from the average of approximately $90 million over the past four years. Research and development spending has averaged 2.5% of sales over the same period.

Despite ongoing investments, the company has maintained its commitment to shareholder returns, with $56 million in dividends and $52 million in share repurchases during FY25. According to the earnings report, MillerKnoll has maintained dividend payments for an impressive 55 consecutive years, demonstrating long-term financial stability.

CEO Andy Owen emphasized the company’s financial position during the earnings call, stating, "We are well positioned with cash flow and balance sheet strength to capitalize on opportunities."

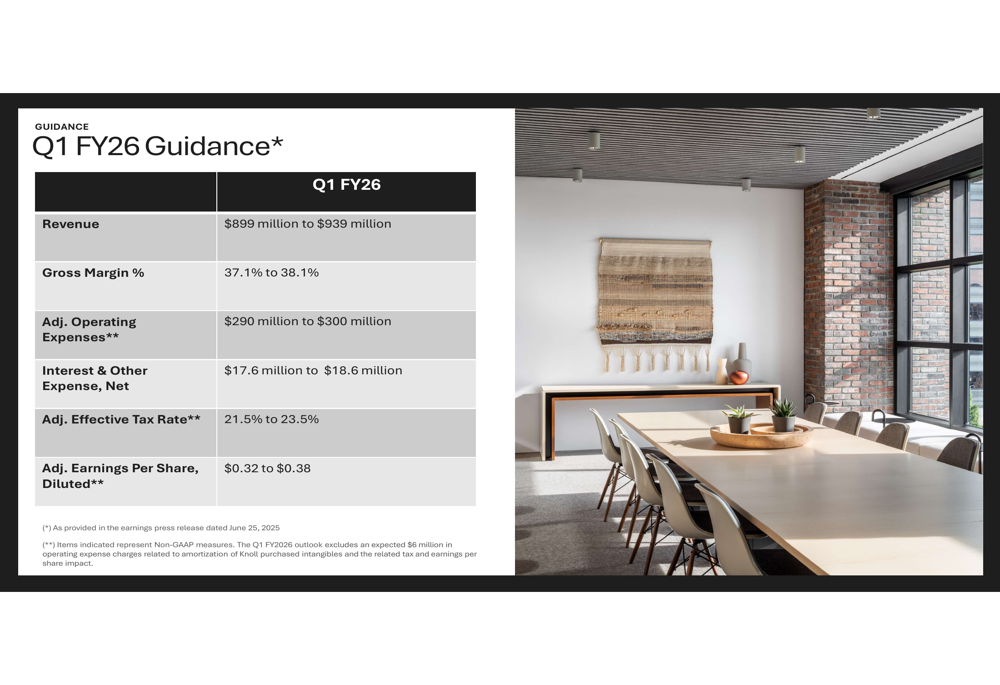

Forward Guidance

Looking ahead to the first quarter of fiscal 2026, MillerKnoll provided guidance that suggests continued growth but with some margin pressure. The company expects Q1 FY26 revenue between $899 million and $939 million, with adjusted earnings per share ranging from $0.32 to $0.38.

The following table details the company’s Q1 FY26 guidance:

Management noted during the earnings call that more companies are returning to office work and focusing on upgrading spaces to attract employees. This trend could provide tailwinds for MillerKnoll’s contract furniture business. However, the company also faces challenges from tariff-related costs, which it expects to mitigate by the third and fourth quarters of fiscal 2026.

Conclusion

MillerKnoll’s fourth-quarter results demonstrate sales momentum and order growth that exceeded market expectations, though profitability metrics show some pressure compared to prior periods. The company’s diversified brand portfolio, global manufacturing footprint, and strategic positioning across market segments provide competitive advantages as it navigates evolving workplace trends.

While the guidance for Q1 FY26 suggests continued growth, the projected earnings range of $0.32-$0.38 per share represents a sequential decline from Q4 FY25’s $0.60, indicating ongoing challenges. Investors will likely focus on the company’s ability to translate sales growth into improved profitability while managing its debt position and continuing to return capital to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.