Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

Minerals Technologies Inc. (NYSE:MTX) presented its third quarter 2025 earnings results on October 24, showing stable performance despite varied market conditions across its business segments. The company’s stock declined 2.58% following the presentation, closing at $61.50, as investors reacted to the company’s cautious outlook for the fourth quarter.

The materials company reported record third-quarter earnings per share while maintaining consistent performance compared to the previous quarter, but signaled a seasonal slowdown ahead. Market conditions remained mixed across MTX’s diverse portfolio, with particular weakness in construction-related markets and renewed uncertainty around tariff policies.

"We delivered record third-quarter earnings per share with strong execution amid mixed market conditions," said Douglas T. Dietrich, Chairman and CEO, highlighting the company’s performance in the challenging environment.

Quarterly Performance Highlights

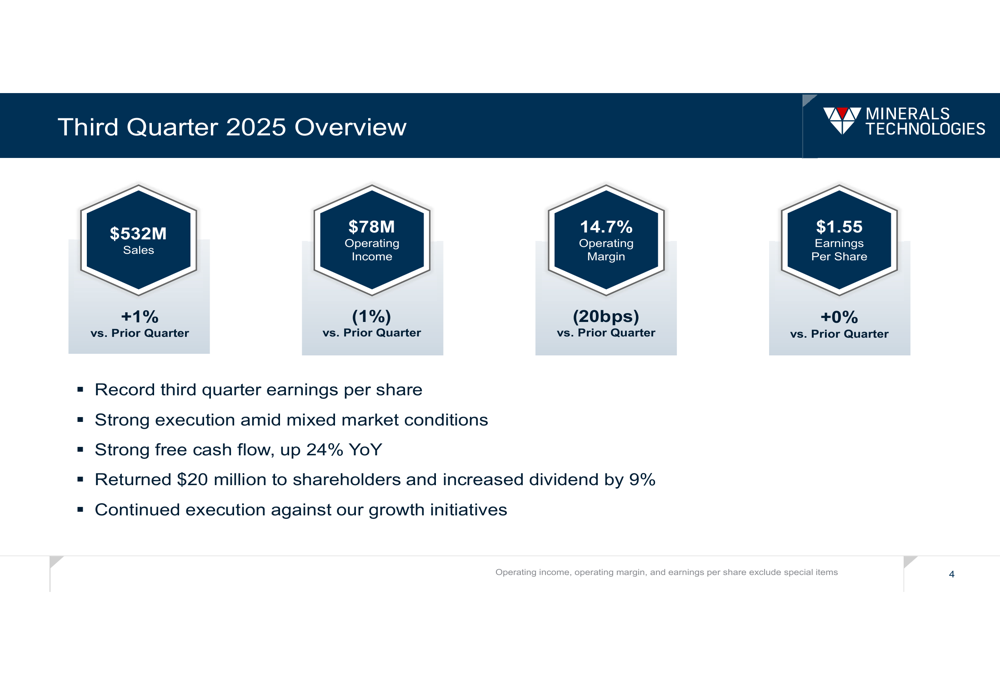

Minerals Technologies reported Q3 2025 sales of $532 million, representing a modest 1% increase both sequentially and year-over-year. Operating income was $78 million, down 1% from both the prior quarter and the same period last year. The company maintained earnings per share of $1.55, flat compared to Q2 but up 3% year-over-year.

As shown in the following financial overview:

Operating margin contracted slightly to 14.7%, representing a 20 basis point decline from the previous quarter and a 40 basis point reduction year-over-year. Despite these margin pressures, the company generated strong free cash flow of $44 million in the quarter, a 24% improvement from the same period in 2024.

The company returned $20 million to shareholders during the quarter and announced a 9% increase to its quarterly dividend, demonstrating confidence in its financial position despite the mixed operating environment.

Segment Performance Analysis

Minerals Technologies operates through two main segments: Consumer & Specialties and Engineered Solutions, each showing different performance trajectories during the quarter.

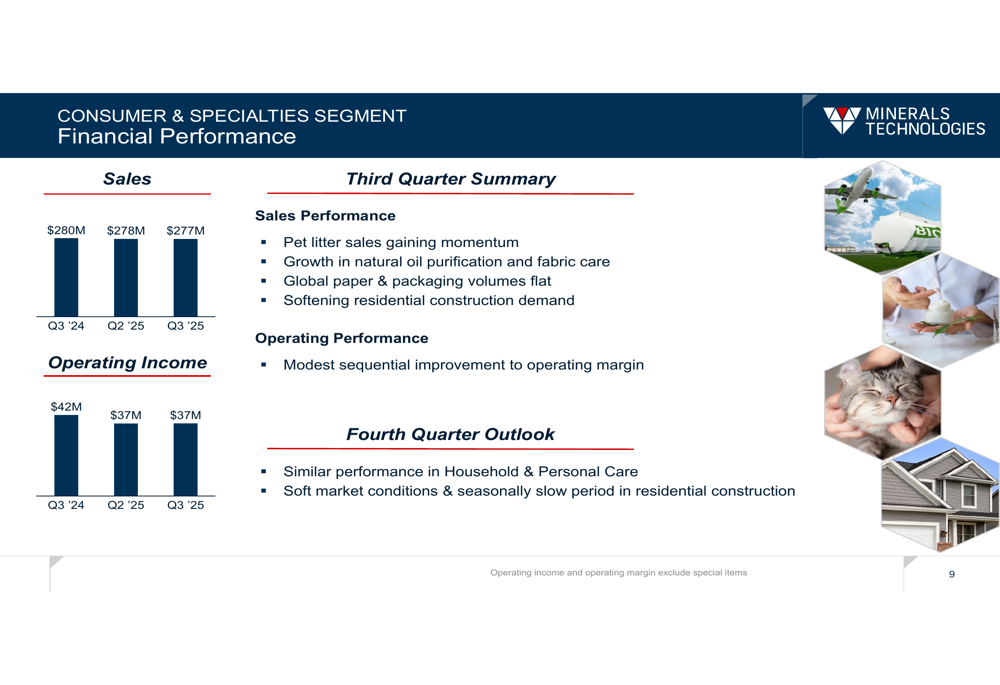

The Consumer & Specialties segment reported sales of $277 million in Q3, relatively flat compared to $278 million in the previous quarter. Operating income for this segment remained stable at $37 million, unchanged from Q2 but down from $42 million in Q3 2024. The company noted that pet litter sales were gaining momentum, while growth continued in natural oil purification and fabric care products.

The segment performance is detailed in the following chart:

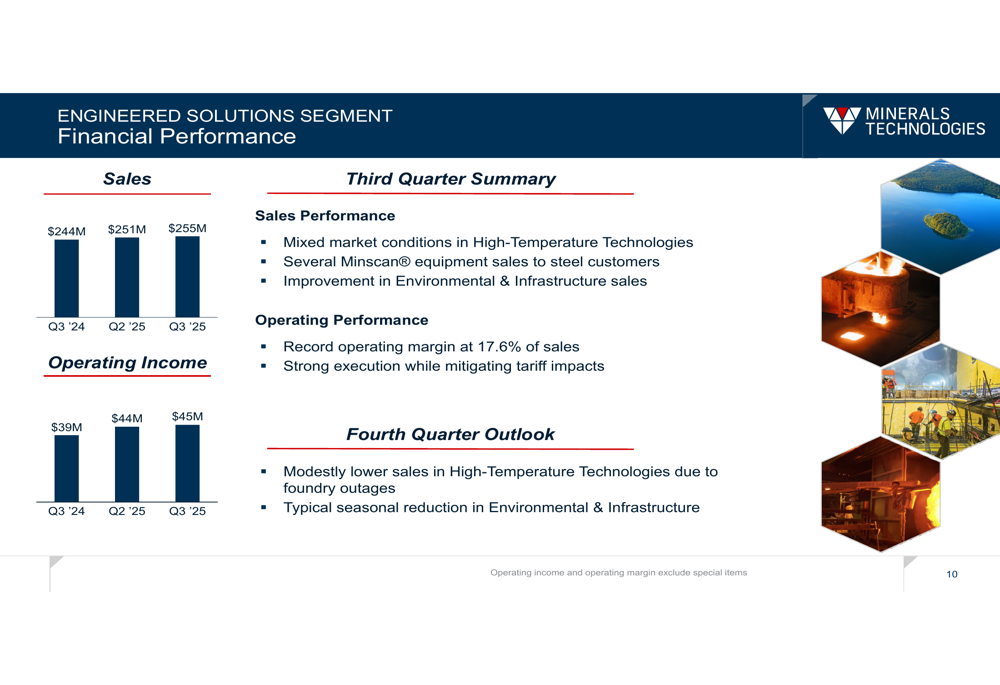

The Engineered Solutions segment showed more positive momentum, with sales increasing to $255 million in Q3 from $251 million in Q2. Operating income improved to $45 million from $44 million in the previous quarter. This segment achieved a record operating margin of 17.6%, demonstrating strong execution despite tariff impacts.

As illustrated in the segment breakdown:

"We achieved record operating margin at 17.6% of sales in our Engineered Solutions segment through strong execution while mitigating tariff impacts," noted Erik C. Aldag, Senior Vice President, Finance and Treasury and Chief Financial Officer during the presentation.

Strategic Growth Initiatives

Despite near-term market challenges, Minerals Technologies continues to invest in organic growth opportunities across its business segments. The company highlighted several key investment areas aligned with high-growth markets, including cat litter, global bleaching earth, and paper and packaging in Asia.

The following chart details the company’s recent organic growth investments:

Notable initiatives include upgrading cat litter production facilities in the US and Canada while expanding capacity in rapidly growing Asian markets. The company is also increasing capacity for sustainable aviation fuel production and other renewable fuels, reflecting its commitment to sustainability-driven growth opportunities.

In the technology space, Minerals Technologies continues to deploy its Minscan® units for steel customers, with 12 units already installed and plans to add six more over the next 12 months. This technology provides significant value to customers while creating a recurring revenue stream for the company.

Balance Sheet and Capital Allocation

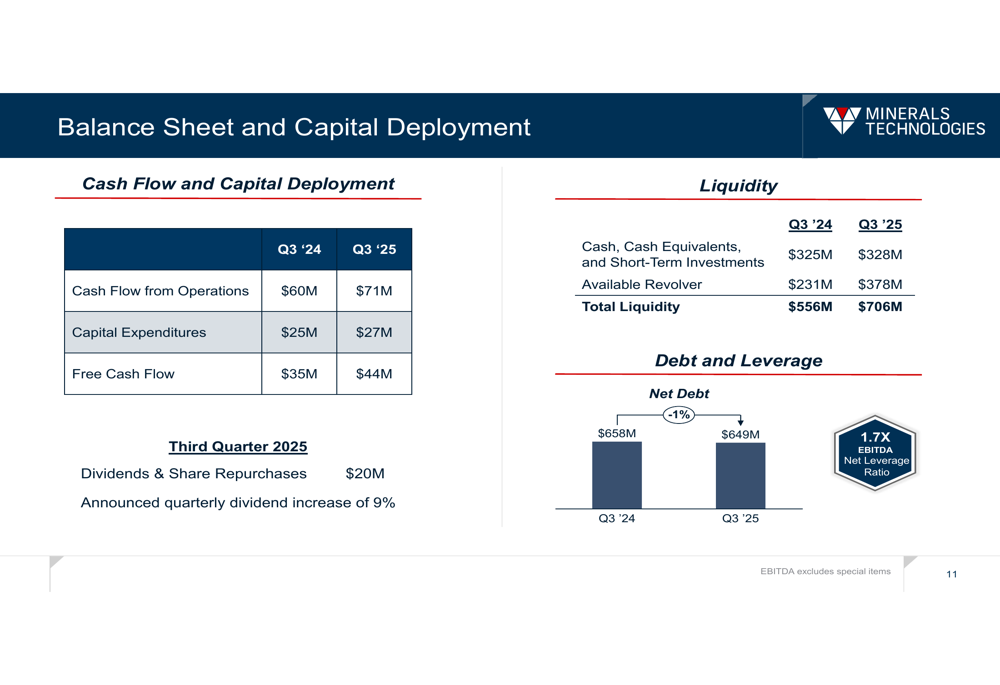

Minerals Technologies maintained a strong financial position, with total liquidity of $706 million as of Q3 2025, a significant improvement from $556 million in the same period last year. The company reduced its net debt slightly to $649 million from $658 million in Q3 2024, resulting in a net leverage ratio of 1.7x EBITDA.

The following chart illustrates the company’s balance sheet strength and capital deployment:

Free cash flow generation was particularly strong at $44 million for the quarter, representing a 24% increase from $35 million in Q3 2024. This improvement came despite slightly higher capital expenditures of $27 million compared to $25 million in the prior year period.

The company’s balanced approach to capital allocation was evident in its decision to return $20 million to shareholders during the quarter while continuing to invest in growth initiatives and maintaining financial flexibility.

Forward Outlook and Guidance

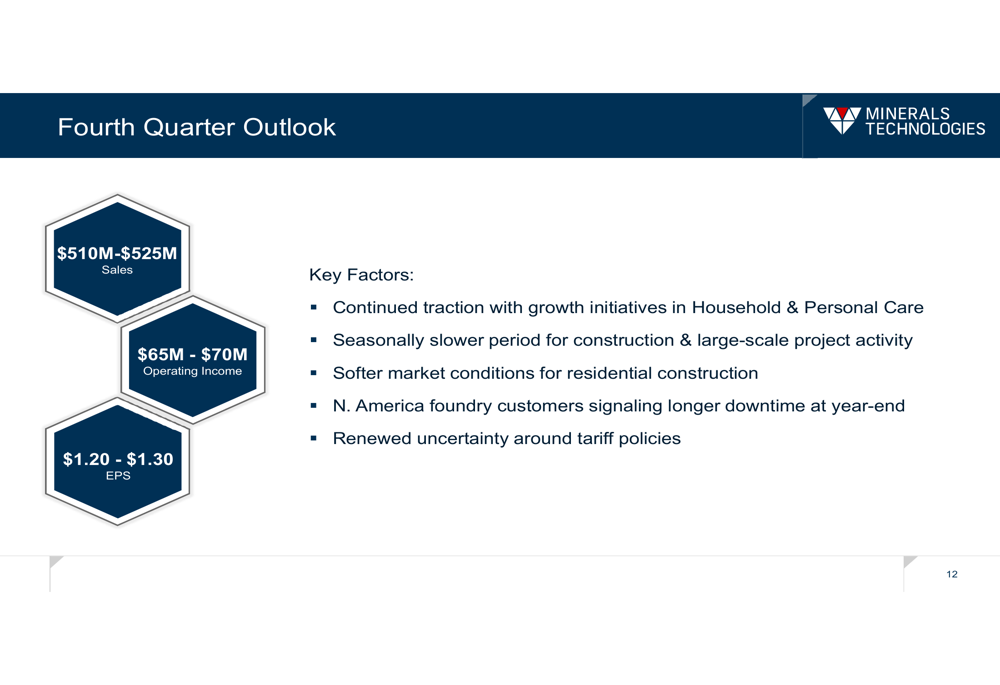

Looking ahead to the fourth quarter, Minerals Technologies provided a more cautious outlook, projecting sales between $510 million and $525 million and operating income between $65 million and $70 million. This guidance implies a sequential decline from Q3 results, with earnings per share expected to range from $1.20 to $1.30.

The company’s Q4 outlook is summarized in the following projection:

Several factors are driving this more conservative outlook, including seasonally slower construction activity, softer residential construction markets, and foundry customers signaling longer downtime at year-end. The company also cited renewed uncertainty around tariff policies as a potential headwind.

For the Consumer & Specialties segment, management expects similar performance in Household & Personal Care products but anticipates soft market conditions and a seasonally slow period in residential construction. The Engineered Solutions segment is projected to see modestly lower sales in High-Temperature Technologies due to foundry outages and a typical seasonal reduction in Environmental & Infrastructure activities.

Despite these near-term challenges, the company remains focused on its long-term growth initiatives, particularly in high-growth markets such as sustainable aviation fuel, pet care products, and specialized technology solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.