Progressive shares fall as Q3 earnings, revenue miss expectations

Introduction & Market Context

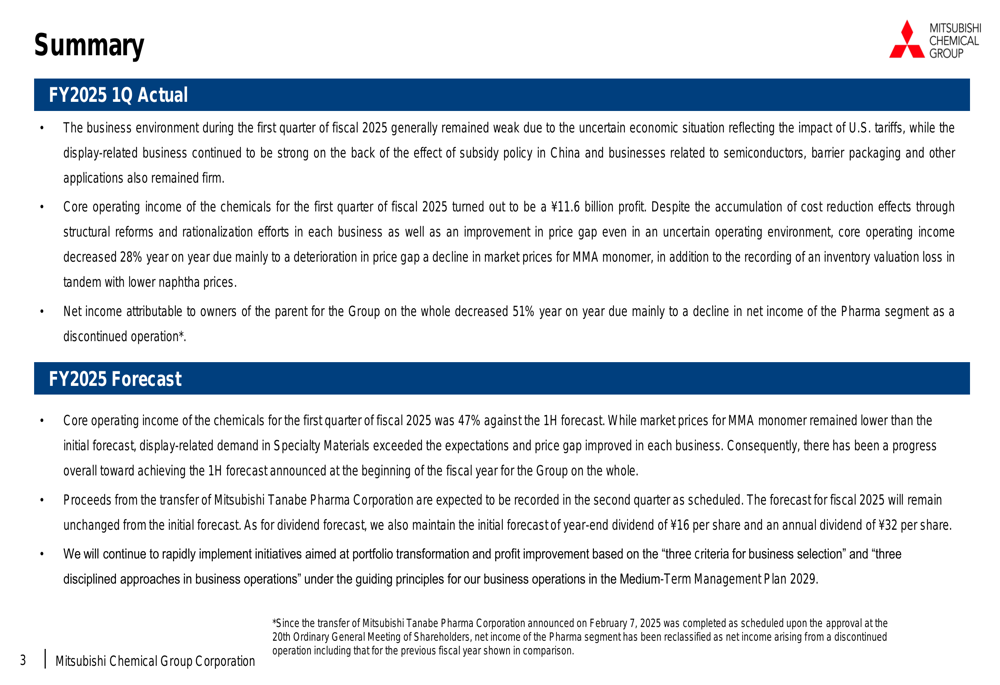

Mitsubishi Chemical Group Corporation (TYO:4188) presented its Q1 FY2025 operational summary on August 1, 2025, revealing significant revenue and profit declines amid challenging market conditions. Despite the disappointing financial results, the company’s stock has surged by 31.62% to ¥843, approaching its 52-week high of ¥852.6, suggesting investors are responding positively to the company’s strategic initiatives and cost-cutting measures.

The company reported that the business environment remained weak due to uncertain economic conditions and U.S. tariffs, which impacted performance across multiple segments. However, management maintained its full-year forecast, signaling confidence in recovery through ongoing portfolio transformation and profit improvement initiatives.

As shown in the following summary of Q1 results:

Quarterly Performance Highlights

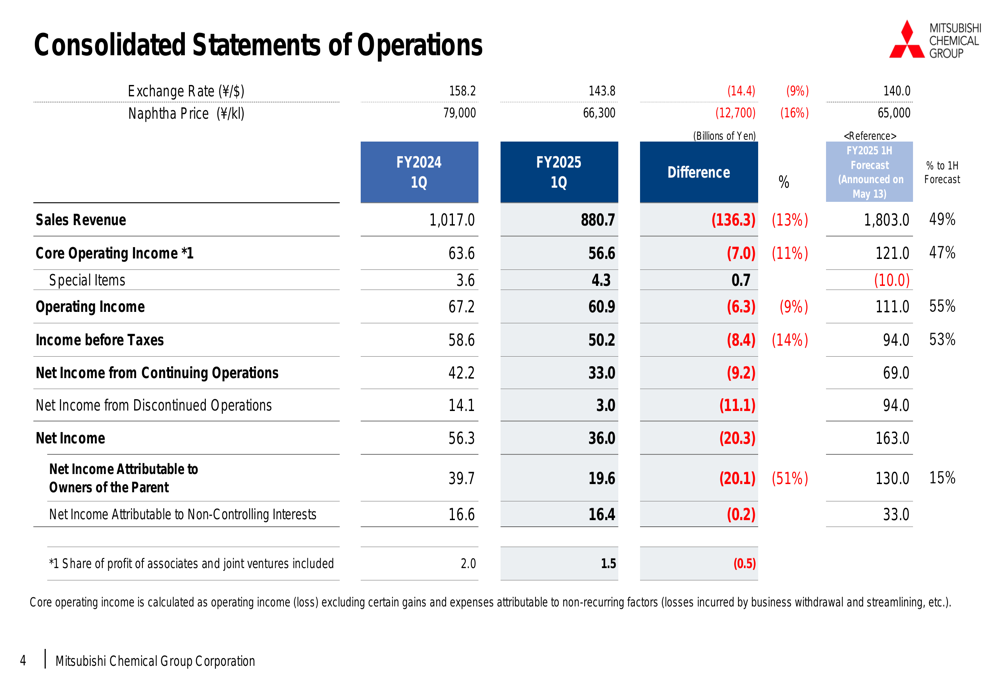

Mitsubishi Chemical reported sales revenue of ¥880.7 billion for Q1 FY2025, representing a 13% decrease from the same period last year. Core operating income fell by 11% year-on-year to ¥56.6 billion, while net income attributable to owners of the parent decreased significantly by 51% to ¥19.6 billion.

The consolidated financial statements reveal the extent of the declines across key metrics, with operating income decreasing by 9% and income before taxes falling by 14% compared to Q1 FY2024:

Despite these challenges, the company achieved a positive free cash flow of ¥24.4 billion in Q1 FY2025, a substantial improvement from the negative ¥6.6 billion reported in the same period last year. This improvement reflects the company’s efforts to enhance cash generation amid difficult market conditions.

Segment Analysis

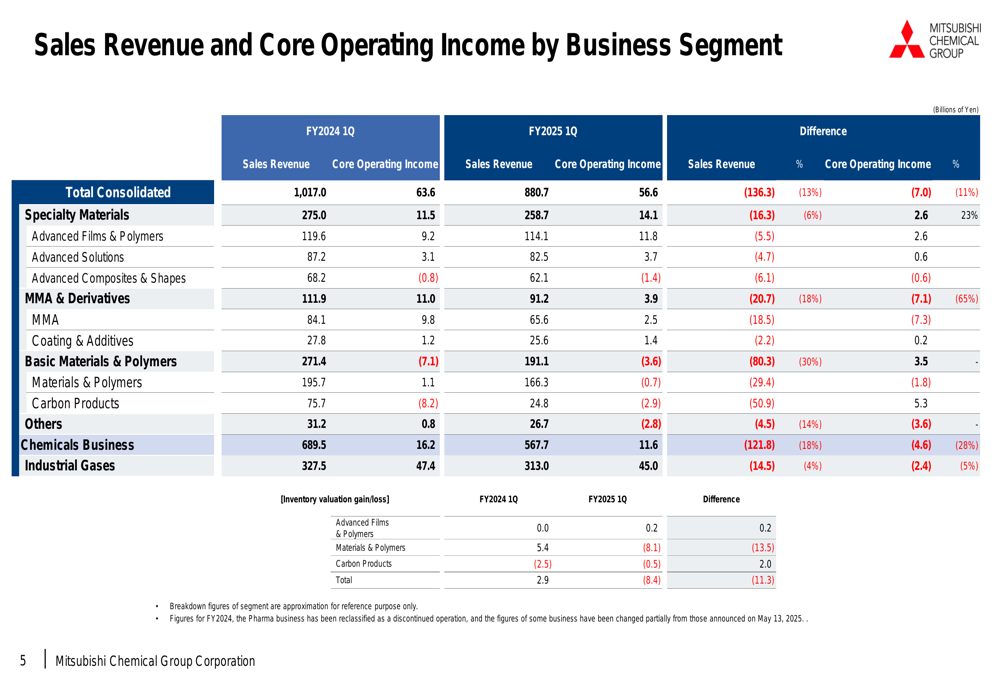

The company’s performance varied significantly across business segments. The detailed breakdown shows that Industrial Gases remained the strongest contributor to core operating income at ¥45.0 billion, while the Chemicals Business reported a profit of ¥11.6 billion, down 28% year-on-year:

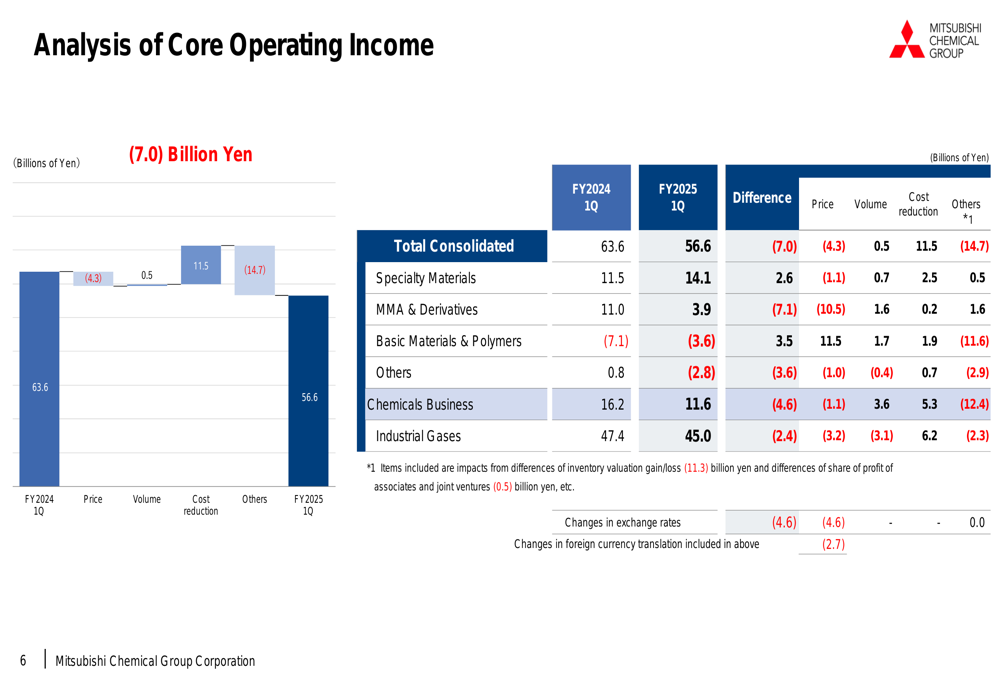

A waterfall analysis of the changes in core operating income reveals that cost reduction efforts contributed positively with ¥11.5 billion in savings, but this was offset by negative price impacts of ¥4.3 billion and other factors amounting to ¥14.7 billion:

Within individual segments, Specialty Materials showed resilience with a ¥2.6 billion improvement in core operating income, driven primarily by the Advanced Films & Polymers business, which saw increased production and sales due to rising demand for barrier packaging. However, the MMA & Derivatives segment suffered a ¥7.1 billion decline, primarily due to deteriorating price gaps from falling market prices for MMA monomer.

The Basic Materials & Polymers segment showed a ¥3.5 billion improvement, largely due to structural reforms in the coke business, while the Industrial Gases segment experienced a ¥2.4 billion decline, affected by foreign exchange impacts and reduced sales volumes across regions.

Strategic Initiatives & Cost Reduction

Mitsubishi Chemical’s presentation emphasized its ongoing initiatives for portfolio transformation and profit improvement. The company has implemented significant cost reductions through rationalization of production sites and optimization of plant operations, contributing to the ¥11.5 billion in cost savings reported for the quarter.

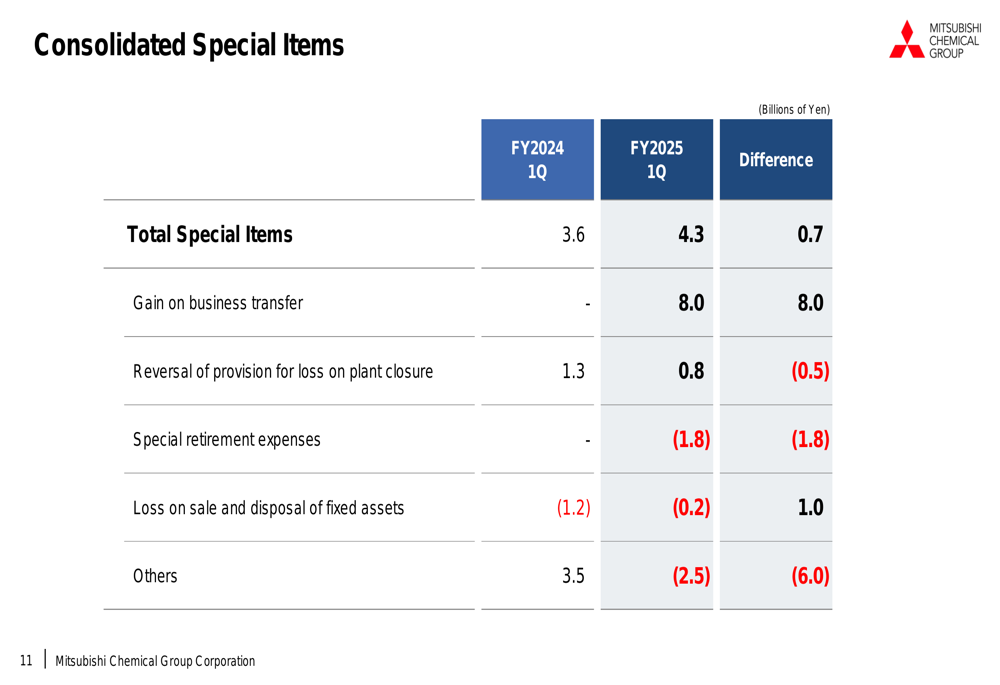

Special items for the quarter included an ¥8.0 billion gain on business transfer, reflecting the company’s strategic realignment efforts:

The company also noted that it has reclassified the net income of the Pharma segment as net income arising from a discontinued operation, further indicating its focus on portfolio optimization.

Balance Sheet and Cash Flow

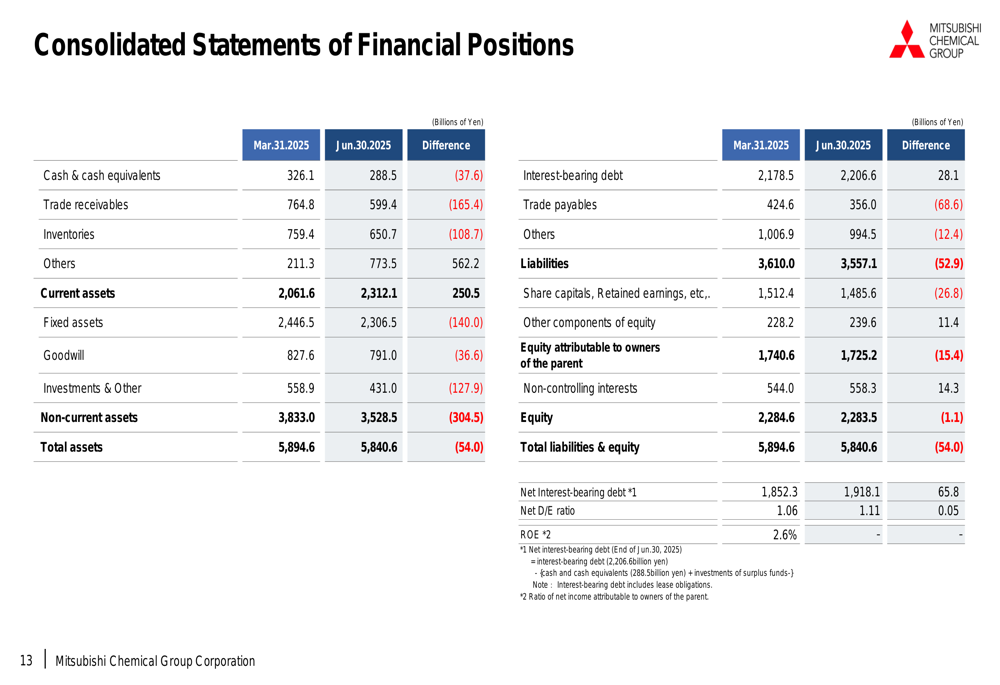

The consolidated statements of financial positions show a slight decrease in total assets from ¥5,894.6 billion as of March 31, 2025, to ¥5,840.6 billion as of June 30, 2025. Notable changes include reductions in trade receivables and inventories, which may reflect improved working capital management:

The company’s net debt-to-equity ratio increased slightly from 1.06 to 1.11, while interest-bearing debt rose marginally from ¥2,178.5 billion to ¥2,206.6 billion. Cash flow from operating activities remained positive at ¥60.2 billion, though lower than the ¥73.9 billion reported in Q1 FY2024.

Market Trends & Outlook

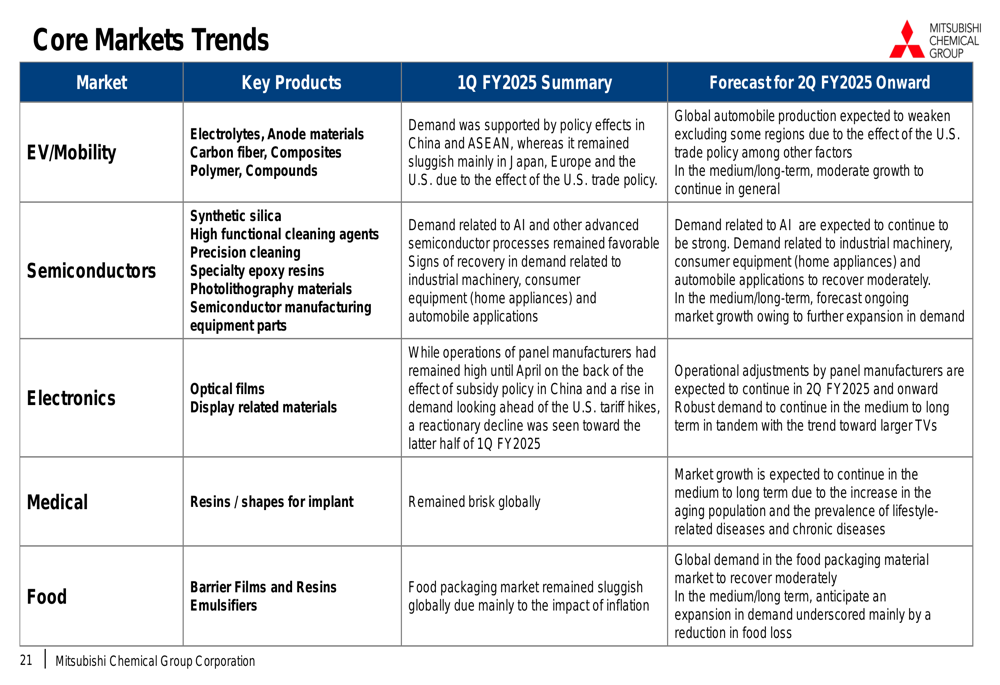

Mitsubishi Chemical provided insights into trends across its core markets, which offer context for both current performance and future prospects. The company noted varying conditions across key sectors, with AI-related semiconductor demand showing strength while other areas face challenges:

Despite the weak Q1 performance, management maintained its full-year forecast, with a projected year-end dividend of ¥16 per share and an annual dividend of ¥32 per share. The company expects core operating income for FY2025 to reach ¥121.0 billion, with Q1 results representing 47% of the first-half forecast.

During the earnings call, management emphasized that "the effects of the structural reform that we have been promoting since last year are gradually emerging," suggesting that the company’s strategic initiatives are beginning to yield results despite the challenging business environment. The company also highlighted the importance of thinking about "the global market and see where we should do our operations," indicating a continued focus on optimizing its global footprint.

With its strategic focus on high-value segments, ongoing cost reduction initiatives, and portfolio optimization efforts, Mitsubishi Chemical appears positioned to navigate the current market challenges while working toward improved performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.