ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Mitsui High-tec Inc (TYO:6966) presented its second quarter fiscal year 2026 financial results on September 9, 2025, revealing a mixed performance with increased sales but declining profits. The company, which specializes in motor cores for electric vehicles and electronic components, saw continued demand for its EV-related products but faced challenges from rising costs and shifting customer demand patterns.

The stock closed at 868 yen on the day of the announcement, down 16 yen or 1.84% from the previous close, suggesting investors responded cautiously to the mixed results and downward revision of full-year forecasts.

Quarterly Performance Highlights

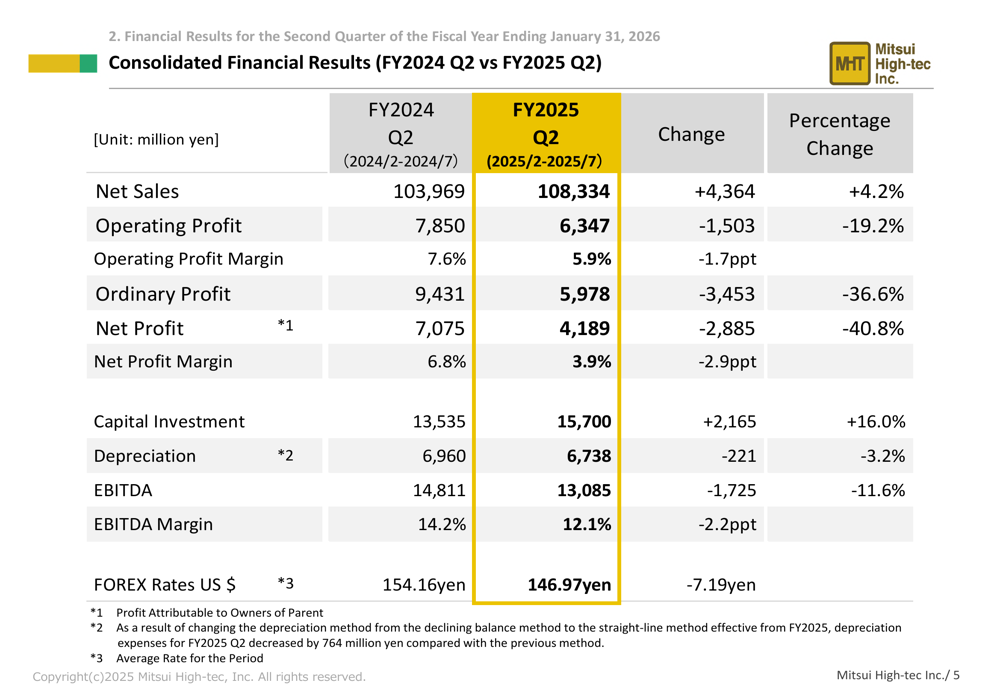

Mitsui High-tec reported a 4.2% year-on-year increase in net sales to 108,334 million yen for Q2 FY2026, primarily driven by demand for electric vehicle motor cores. However, operating profit decreased by 19.2% to 6,347 million yen, with the company citing upfront costs and higher management expenses as key factors.

As shown in the following consolidated financial results summary:

The decline in profitability was even more pronounced in other metrics, with ordinary profit falling 36.6% to 5,978 million yen and net profit attributable to owners of the parent dropping 40.8% to 4,189 million yen. The company noted that performance was generally in line with expectations despite external uncertainties.

Detailed Financial Analysis

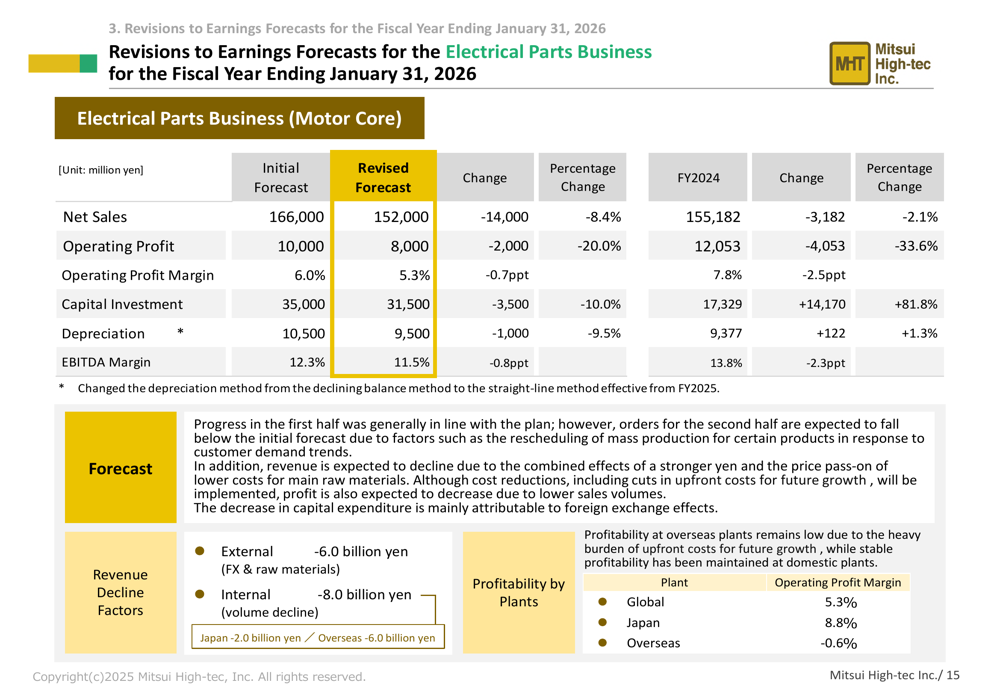

Breaking down performance by business segment, the Electrical Parts Business (Motor Core) remained the primary growth driver, with sales increasing to 77,406 million yen from 73,781 million yen in the previous year. The Electronic Parts Business (Leadframe) also saw modest growth, with sales rising to 28,753 million yen from 28,107 million yen.

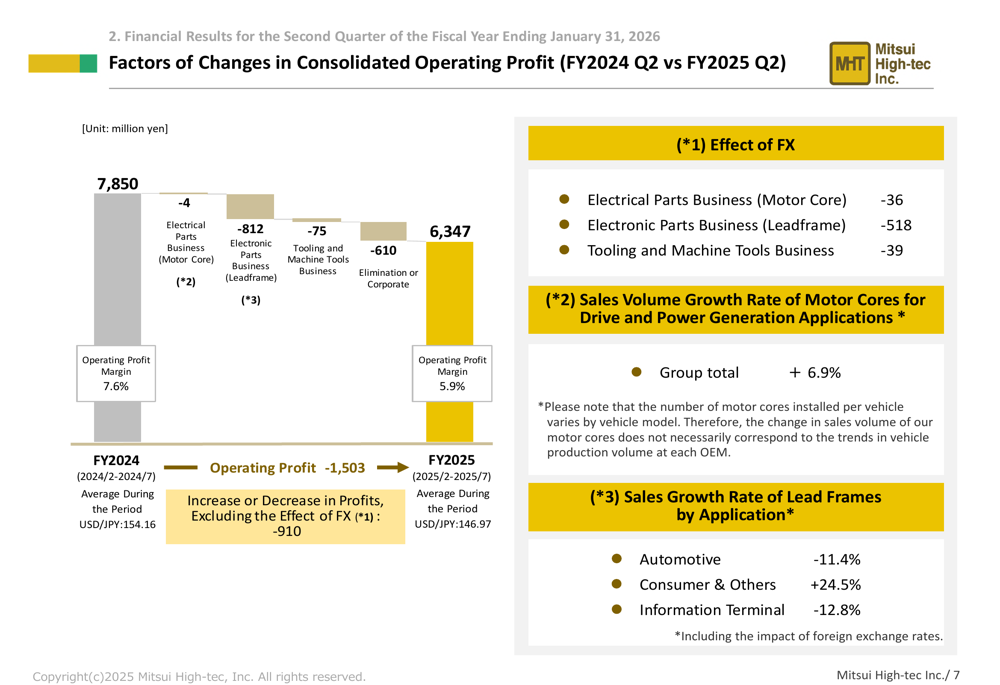

The company provided a detailed analysis of factors affecting the operating profit decline:

Foreign exchange effects negatively impacted all business segments, with the US dollar rate decreasing from 154.16 yen to 146.97 yen year-on-year. While motor cores for drive and power generation applications showed a healthy 6.9% sales volume growth rate, leadframes for automotive applications declined by 11.4%, partially offset by 24.5% growth in consumer and other applications.

Quarter-to-quarter comparison revealed additional challenges, with net sales decreasing 1.9% from Q1 to Q2 FY2025, and operating profit declining 17.0%. However, ordinary profit and net profit showed significant increases of 203.8% and 232.5% respectively, suggesting some non-operational factors positively affected the bottom line.

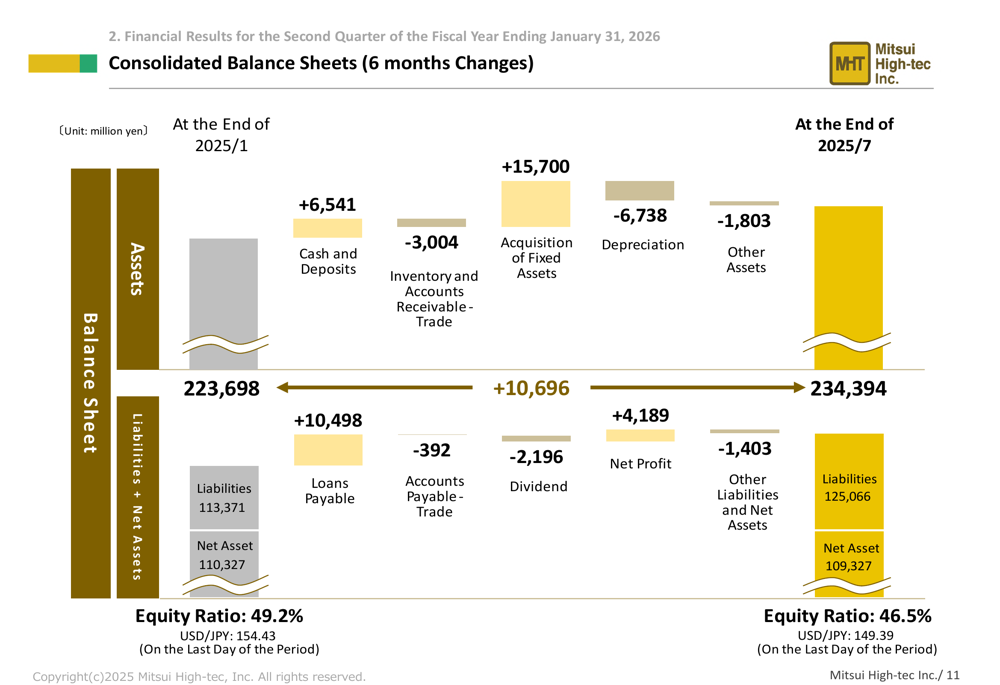

The company's balance sheet showed an increase in total assets to 234,394 million yen, with cash and deposits increasing by 6,541 million yen. However, the equity ratio decreased from 49.2% to 46.5%, partly due to increased loans payable of 10,498 million yen, likely related to the ongoing capital investment program.

Cash flow from operating activities improved year-on-year from 13,207 million yen to 15,361 million yen, while investment activities remained stable around -14,700 million yen. The closing balance of cash and cash equivalents increased substantially to 56,161 million yen from 46,372 million yen in the previous year.

Revised Outlook

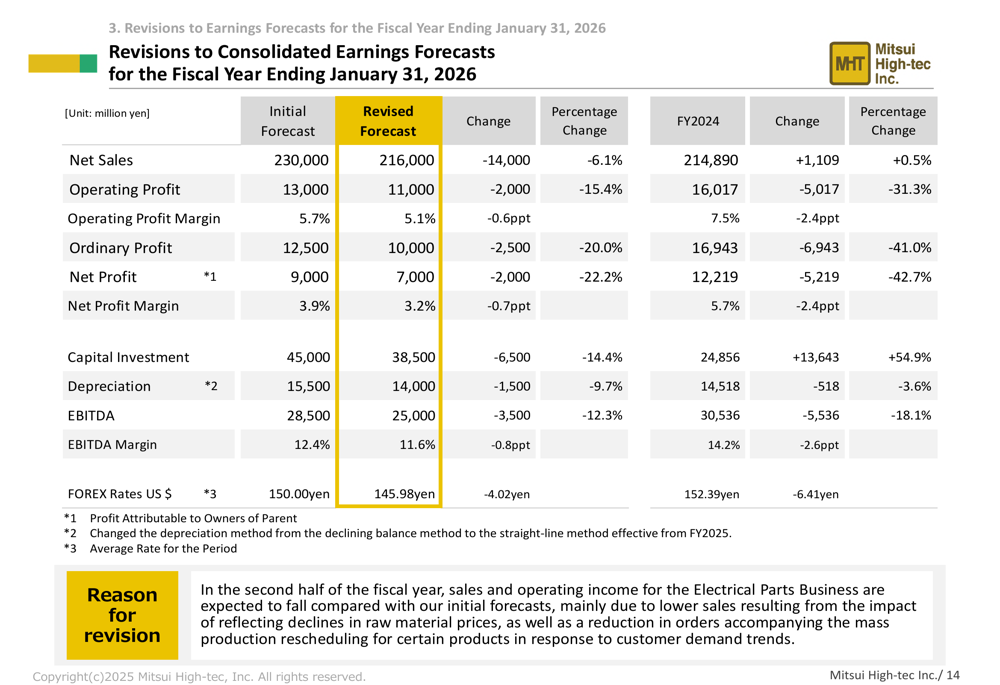

In a significant development, Mitsui High-tec revised its full-year forecasts downward for the fiscal year ending January 31, 2026:

The company reduced its net sales forecast by 6.1% to 216,000 million yen and operating profit forecast by 15.4% to 11,000 million yen. Capital investment plans were also scaled back by 14.4% to 38,500 million yen.

The revision was primarily attributed to expected weakness in the Electrical Parts Business in the second half of the fiscal year:

Management explained that sales and operating income for the Electrical Parts Business are expected to fall compared with initial forecasts, mainly due to lower sales resulting from declining raw material prices and reduced orders following mass production rescheduling for certain products in response to customer demand trends.

The Electronic Parts Business forecasts remained unchanged for sales and operating profit, though capital investment was reduced from 5,500 to 4,500 million yen. The Tooling and Machine Tools Business saw a modest downward revision in operating profit from 1,000 to 800 million yen.

Dividend Policy

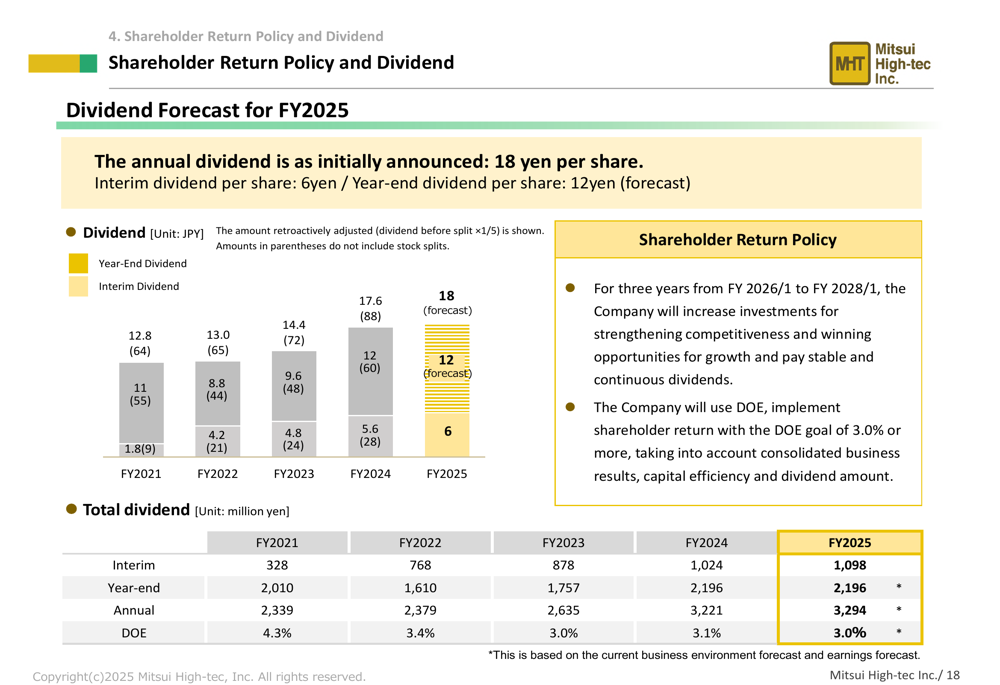

Despite the downward revision in earnings forecasts, Mitsui High-tec maintained its annual dividend at 18 yen per share, consisting of a 6 yen interim dividend and a projected 12 yen year-end dividend.

The company reiterated its shareholder return policy, noting that for the three years from FY2026 to FY2028, it will increase investments to strengthen competitiveness and capture growth opportunities while continuing to pay stable and continuous dividends.

Historical dividend data shows a steady increase from 12 yen in FY2021 to the current 18 yen, reflecting the company's commitment to shareholder returns despite fluctuations in business performance.

Strategic Initiatives

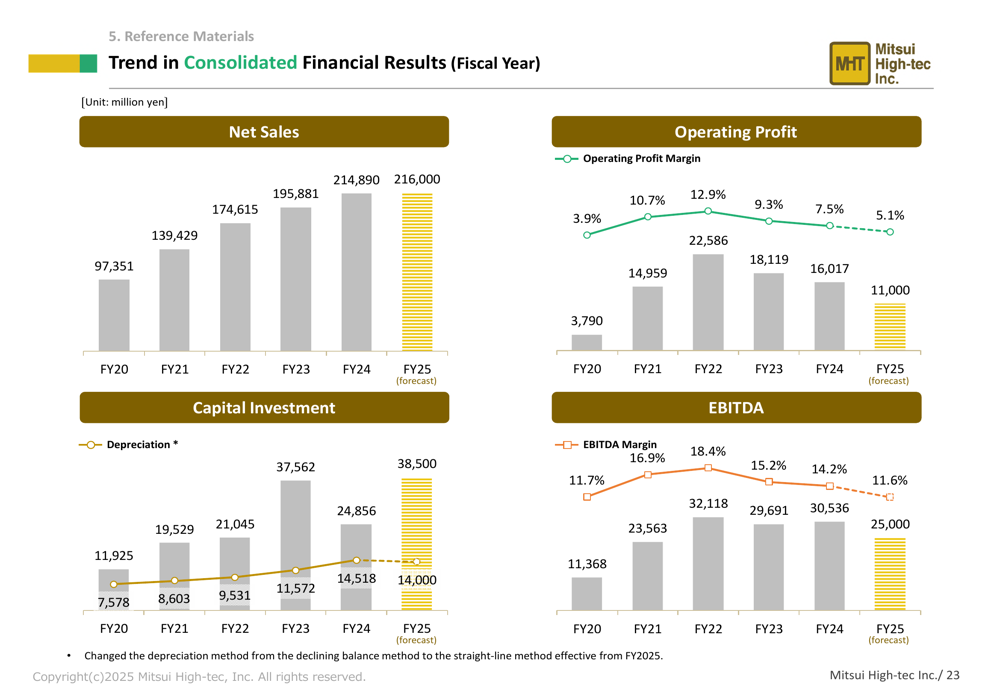

Looking at longer-term trends, Mitsui High-tec has shown significant growth over the past five years, with net sales more than doubling from 97,351 million yen in FY2020 to 214,890 million yen in FY2024. This growth trajectory is illustrated in the company's consolidated financial results trend:

The company continues to invest heavily in capital expenditures, particularly in the Electrical Parts Business, positioning itself to capture future growth in the electric vehicle market despite near-term challenges. The current period of increased investment and margin pressure appears to be part of a strategic expansion plan to strengthen market position in anticipation of continued EV adoption globally.

While the revised outlook suggests some caution is warranted in the near term, Mitsui High-tec's focus on EV motor cores and continued capital investment indicate confidence in the long-term growth potential of its core markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.