Fannie Mae, Freddie Mac shares tumble after conservatorship comments

Introduction & Market Context

Monro Inc. (NASDAQ:MNRO) presented its fourth quarter fiscal 2025 earnings results on May 28, 2025, announcing a significant restructuring plan that includes closing 145 underperforming stores. The automotive service provider continues to face headwinds from consumer trade-down behavior and rising costs, with shares trading near 52-week lows at $12.77, down significantly from the 52-week high of $31.49.

The company’s presentation revealed a comprehensive strategy to address ongoing challenges, with early signs of sales momentum emerging despite continued margin pressure. Monro’s stock gained slightly in aftermarket trading, up 0.94% to $12.89, as investors digested the restructuring plans.

Quarterly Performance Highlights

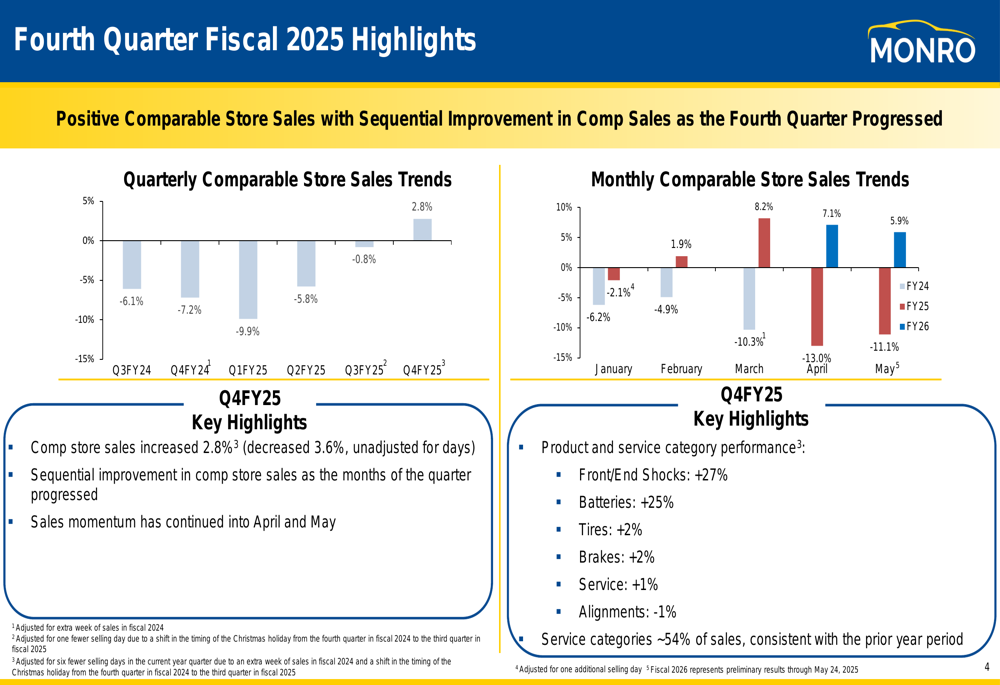

Monro reported fourth quarter sales of $295.0 million, down 4.9% compared to $310.1 million in the same period last year. Comparable store sales increased 2.8% when adjusted for days, but decreased 3.6% on an unadjusted basis. The company noted sequential improvement in comparable store sales as the quarter progressed.

As shown in the following chart of monthly comparable store sales trends, Monro experienced negative growth throughout the period, though with some signs of improvement:

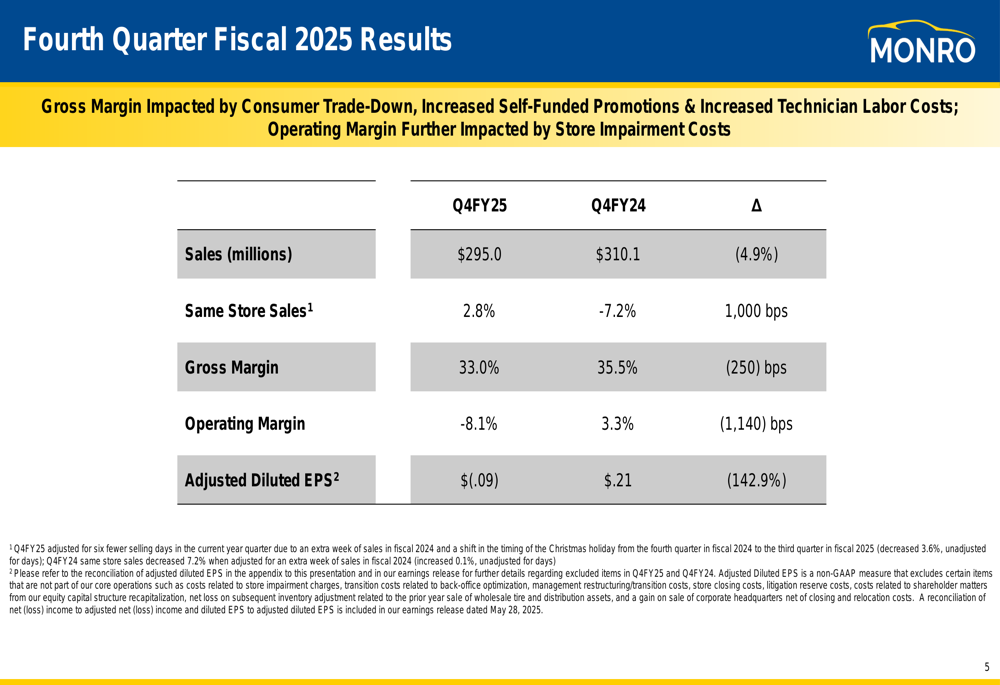

Profitability metrics showed significant pressure, with gross margin declining 250 basis points year-over-year to 33.0%, while operating margin plummeted 1,140 basis points to -8.1%. Adjusted diluted earnings per share came in at -$0.09, compared to $0.21 in the prior year period, representing a 142.9% decrease.

The financial results summary highlights these challenges:

Product category performance was mixed, with front-end/shocks (+27%) and batteries (+25%) showing strong growth, while tires and brakes (+2% each) and service (+1%) delivered modest gains. Alignments declined 1% during the quarter. Service categories represented approximately 54% of total sales.

Strategic Initiatives

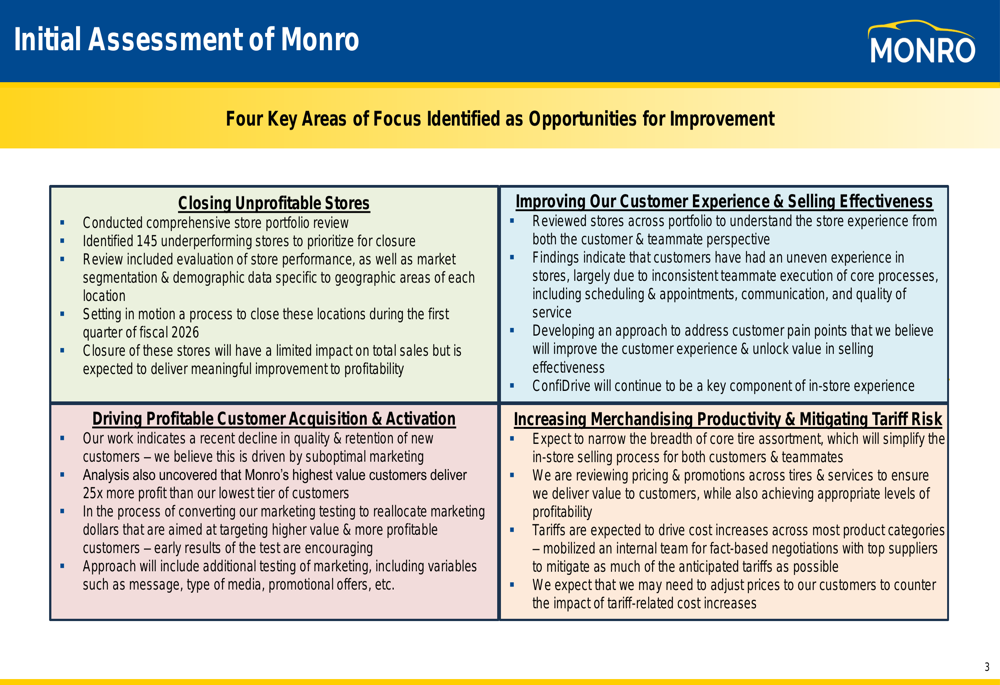

The centerpiece of Monro’s presentation was its strategic plan focused on four key areas for improvement. Following a comprehensive portfolio review, the company identified 145 underperforming stores for closure in the first quarter of fiscal 2026, representing a significant operational restructuring.

The strategic initiatives are detailed in the following slide:

Beyond store closures, Monro is focusing on improving customer experience and selling effectiveness by addressing inconsistencies in service delivery. The company also plans to drive profitable customer acquisition by targeting higher-value customers and increase merchandising productivity while mitigating tariff risks through a narrower tire assortment and strategic pricing adjustments.

"We conducted a comprehensive store portfolio review, identifying 145 underperforming stores for closure," the company stated in its presentation. "These closures are planned for the first quarter of fiscal 2026 and are expected to improve profitability."

Financial Position

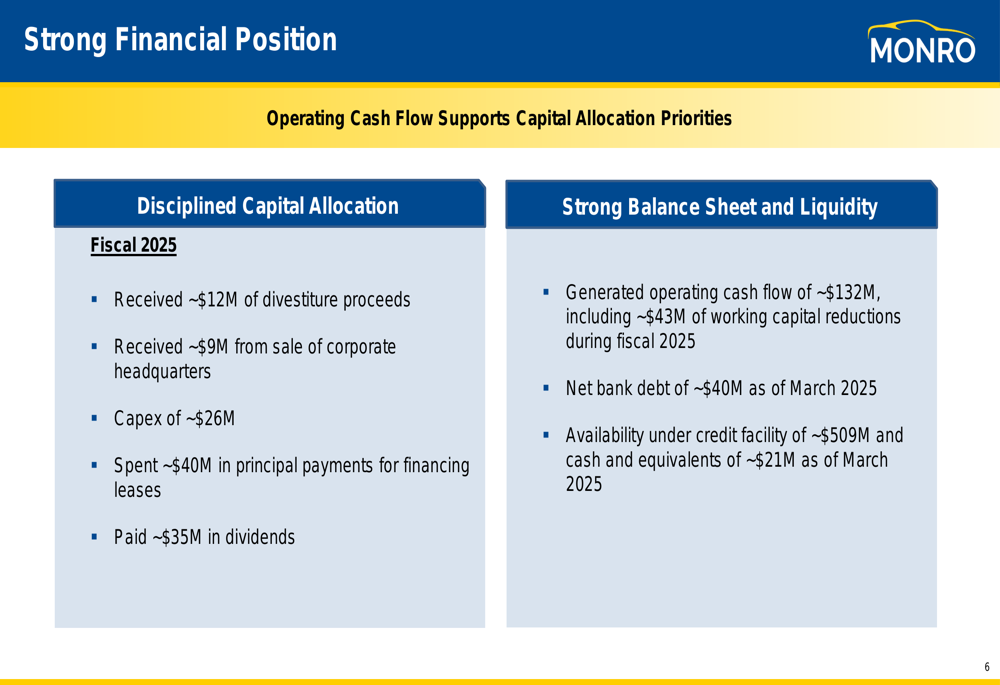

Despite operational challenges, Monro maintained a relatively strong financial position, generating approximately $132 million in operating cash flow during fiscal 2025, including about $43 million from working capital reductions. The company ended March 2025 with net bank debt of approximately $40 million and cash and equivalents of around $21 million.

The following slide details Monro’s capital allocation and balance sheet position:

During fiscal 2025, Monro received approximately $12 million from divestiture proceeds and about $9 million from the sale of its corporate headquarters. The company spent approximately $26 million on capital expenditures, $40 million in principal payments for financing leases, and paid approximately $35 million in dividends, demonstrating its commitment to shareholder returns despite operational challenges.

Forward-Looking Statements

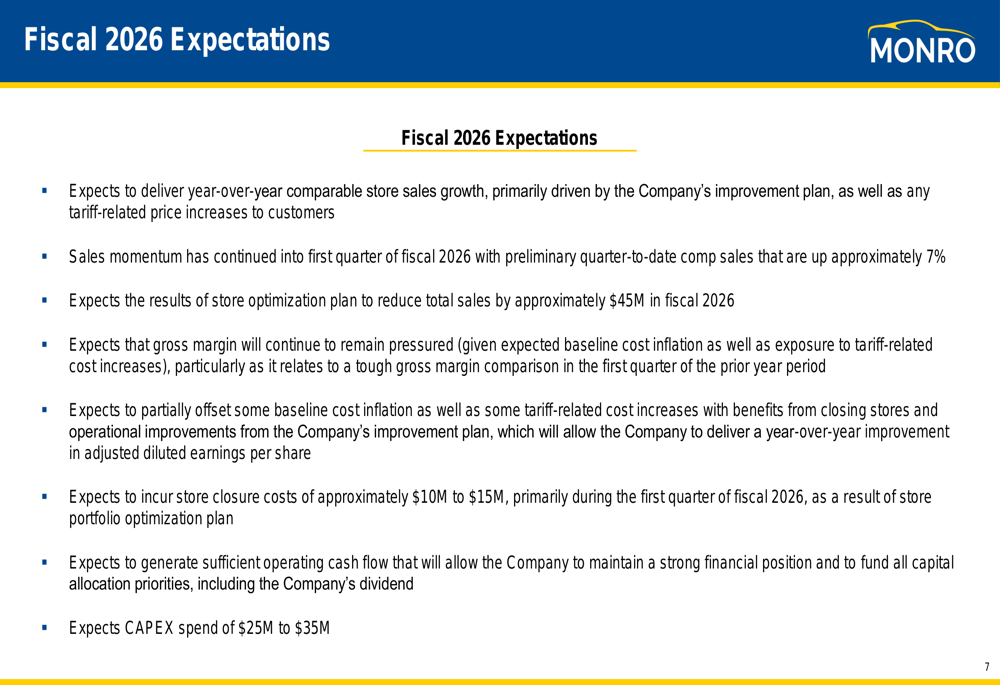

Looking ahead to fiscal 2026, Monro expects to deliver year-over-year comparable store sales growth, with preliminary quarter-to-date comparable sales up approximately 7%. However, the company anticipates that the store optimization plan will reduce total sales by approximately $45 million in fiscal 2026.

The outlook for fiscal 2026 is detailed in this slide:

Monro expects gross margin to remain under pressure but aims to partially offset baseline cost inflation and tariff-related increases through benefits from store closures and operational improvements. The company anticipates store closure costs of approximately $10 million to $15 million but expects to generate sufficient operating cash flow, with capital expenditures projected between $25 million and $35 million.

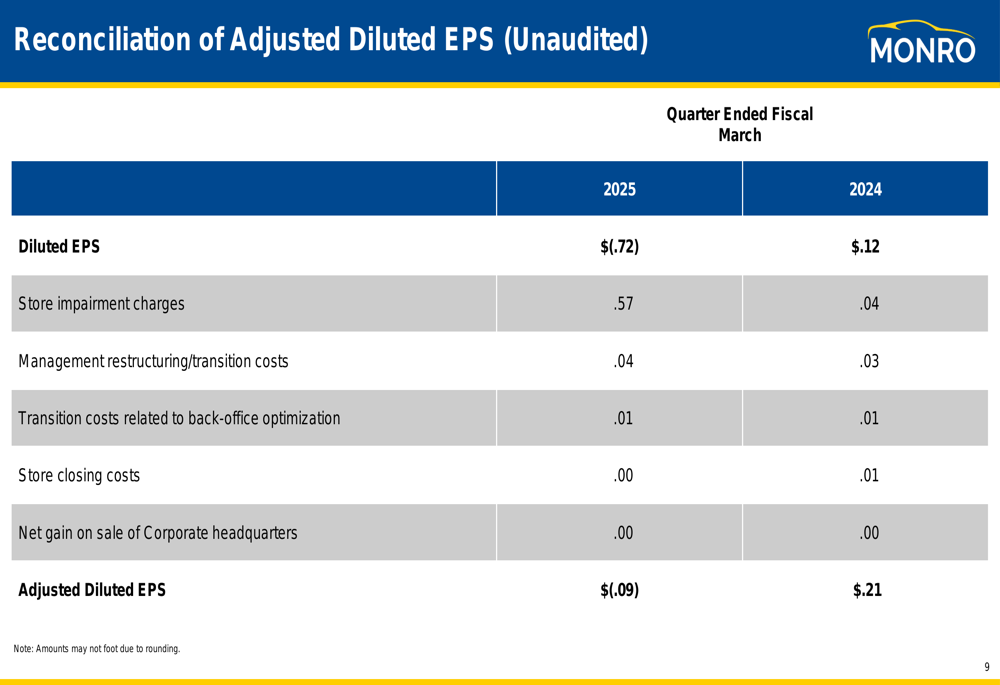

The company also provided a reconciliation of its adjusted diluted EPS, highlighting significant store impairment charges of $0.57 per share in the fourth quarter:

This restructuring marks a significant shift for Monro as it attempts to address persistent challenges that have affected its performance over multiple quarters. The company’s previous earnings report for Q3 FY2024 had already shown signs of strain, with an EPS miss and declining revenues, suggesting that these more dramatic measures were becoming increasingly necessary to stabilize the business.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.