Trump meets Zelenskiy, says Putin wants war to end, mulls trilateral talks

Introduction & Market Context

Montrose Environmental Group (NYSE:MEG) presented its Q1 2025 earnings results on May 8, 2025, reporting record-breaking performance across key financial metrics. The environmental services provider’s stock jumped 10.3% in premarket trading to $16.60, reflecting investor optimism about the company’s performance and improved outlook.

The strong quarterly results come after a challenging period for the company, which had seen its stock decline significantly from its 52-week high of $49.97. The current performance suggests a potential turnaround as Montrose continues to execute its growth strategy in the environmental services sector.

Quarterly Performance Highlights

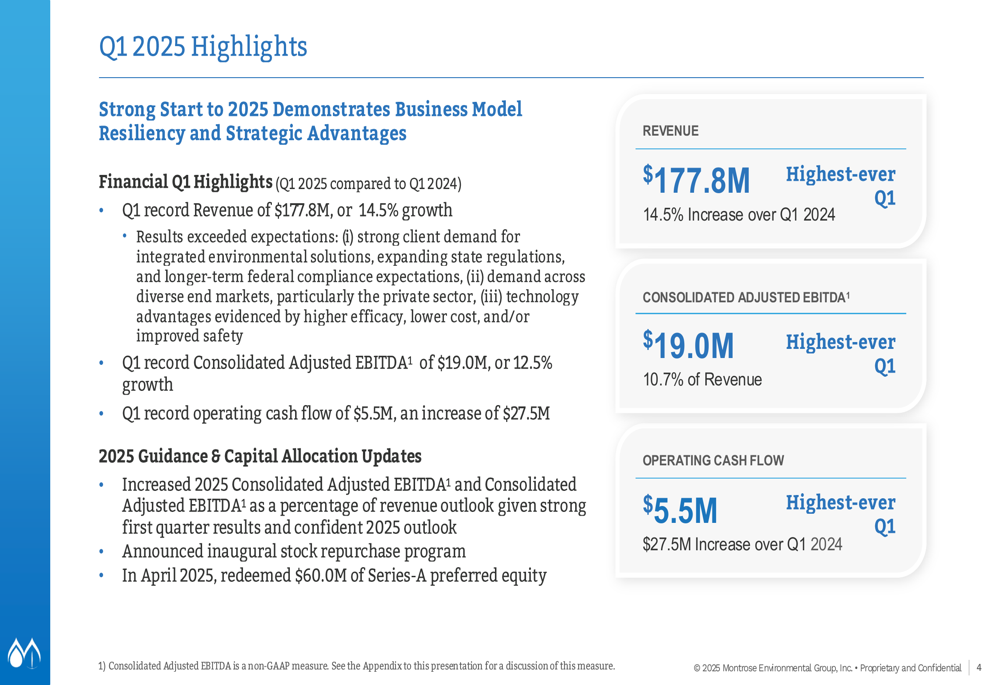

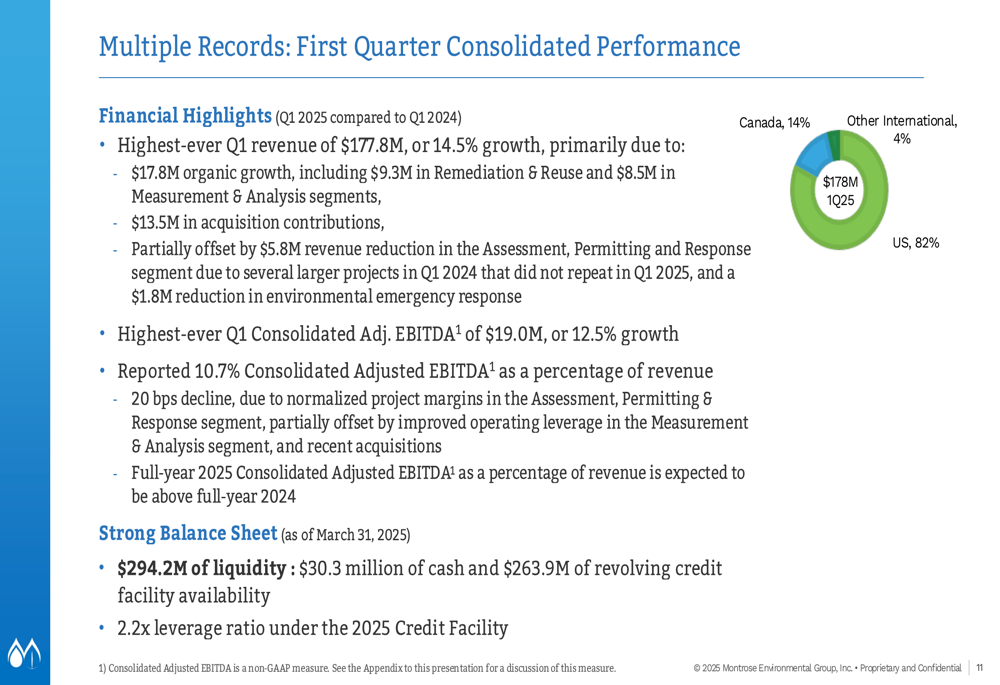

Montrose reported record Q1 2025 revenue of $177.8 million, representing a 14.5% increase compared to the same period last year. This growth was primarily driven by $17.8 million in organic growth and $13.5 million from acquisitions. The company also achieved record consolidated adjusted EBITDA of $19.0 million, up 12.5% year-over-year, with a 10.7% margin.

As shown in the following financial highlights slide, Montrose demonstrated strong performance across key metrics:

Operating cash flow showed particularly impressive improvement, reaching a record $5.5 million for the quarter, a substantial $27.5 million increase from the prior year. This cash flow enhancement aligns with management’s stated goal of improving cash generation capabilities.

The company maintains a strong balance sheet with $294.2 million of liquidity and a 2.2x leverage ratio under its 2025 Credit Facility. Geographically, Montrose generates 82% of its revenue from the United States, 14% from Canada, and 4% from other international markets, as illustrated in the following quarterly performance overview:

Segment Performance Analysis

Montrose’s performance varied significantly across its three business segments, with two showing strong growth while one experienced a decline:

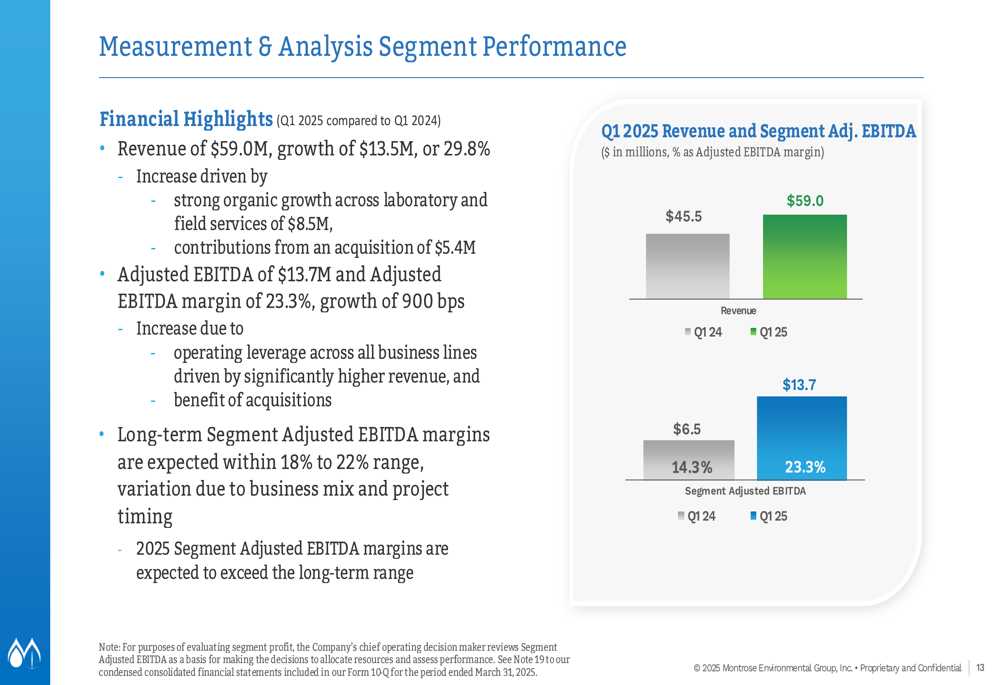

The Measurement & Analysis segment delivered the strongest performance, with revenue increasing 29.8% to $59.0 million and adjusted EBITDA margin expanding significantly from 14.3% to 23.3%. This 900 basis point improvement in profitability demonstrates the segment’s growing operational efficiency.

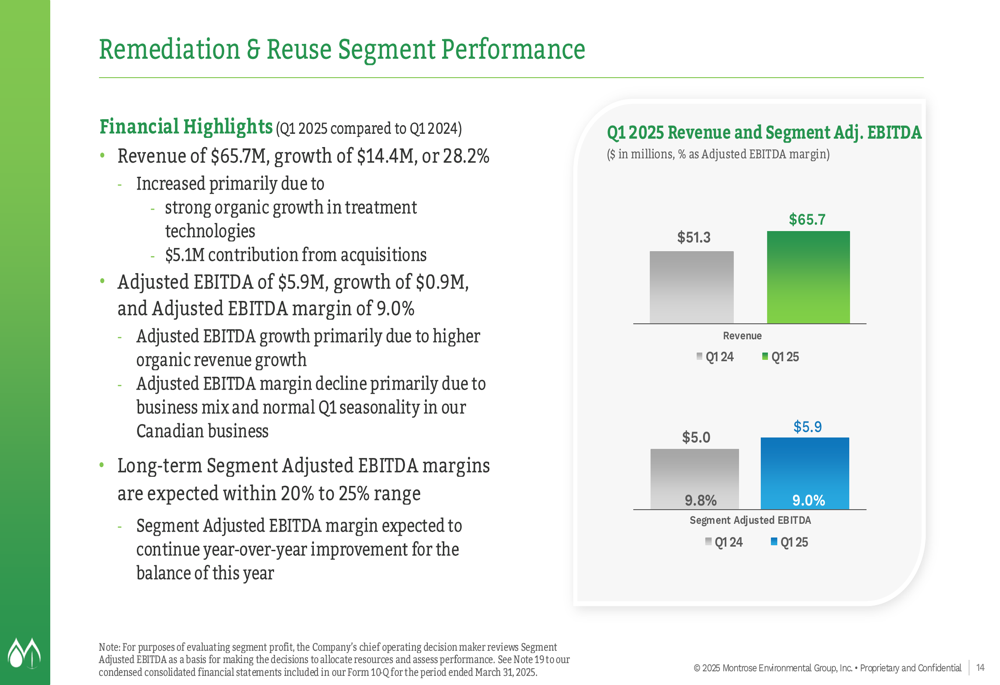

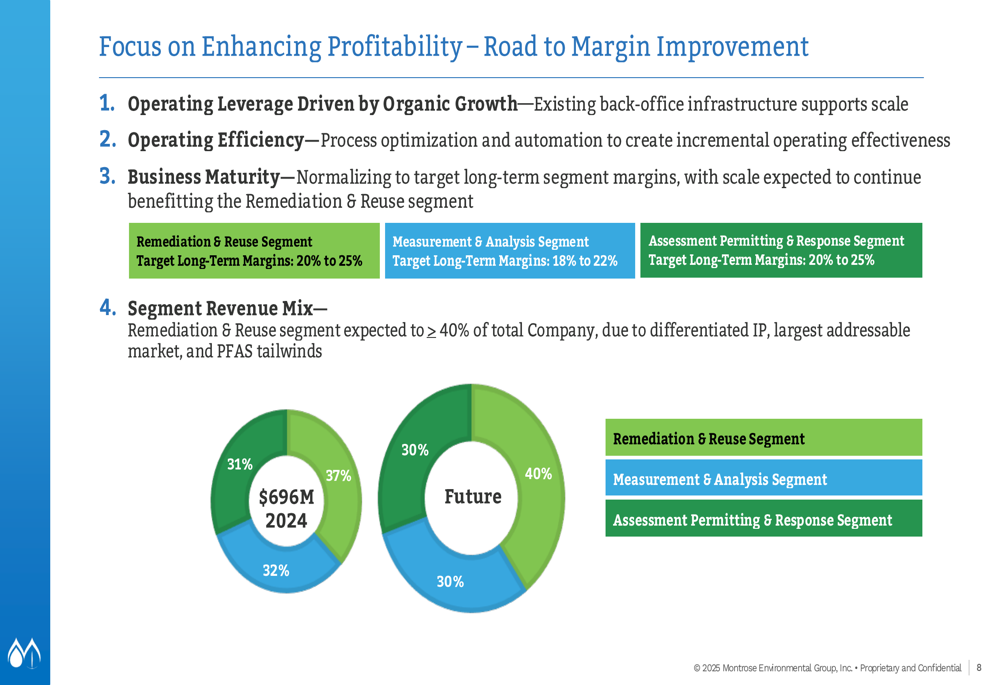

The Remediation & Reuse segment also showed robust growth, with revenue increasing 28.2% to $65.7 million. However, adjusted EBITDA margin slightly declined from 9.8% to 9.0%. Management has identified this segment as a strategic growth priority, expecting it to eventually represent more than 40% of total company revenue.

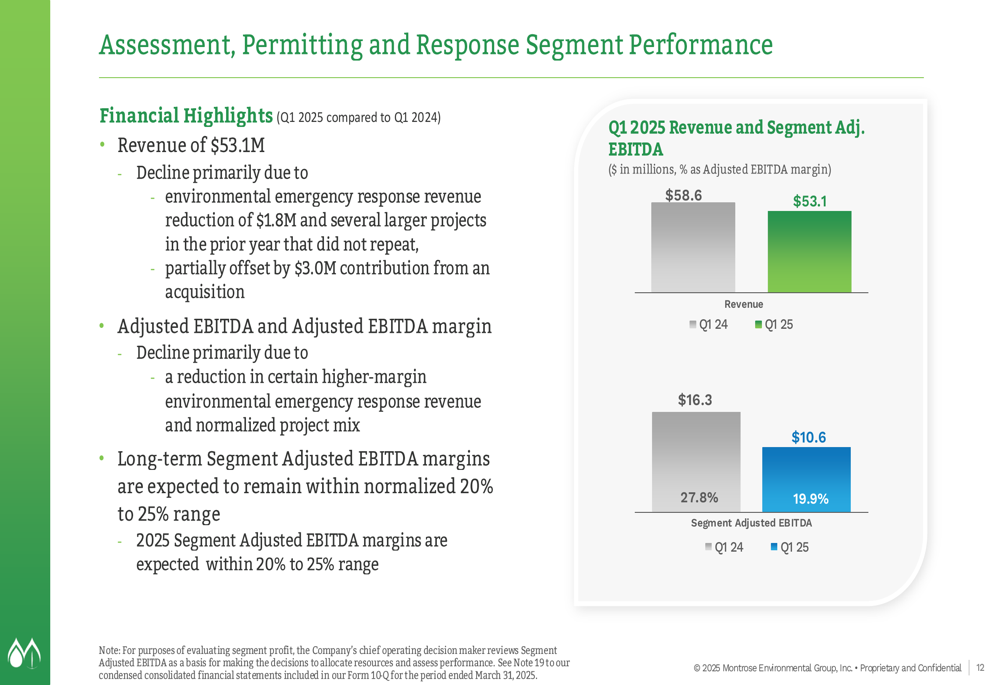

In contrast, the Assessment, Permitting & Response segment experienced a decline, with revenue falling to $53.1 million from $58.6 million in Q1 2024. The segment’s adjusted EBITDA margin also contracted significantly from 27.8% to 19.9%. Despite this setback, management expects segment margins to stabilize within the 20-25% range for 2025.

Strategic Initiatives

Montrose outlined several strategic capital allocation priorities during the presentation. The company redeemed $60.0 million of Series A-2 Preferred Equity in April 2025 and committed to redeeming the remaining $62.0 million by the end of the year. Additionally, Montrose announced its inaugural stock repurchase program of up to $40 million.

The company also executed a new credit facility, consisting of a $200 million term loan A and a $300 million revolver, providing enhanced financial flexibility.

Looking forward, Montrose presented a clear roadmap for improving profitability through four key drivers: operating leverage from organic growth, process optimization, business maturity, and favorable segment revenue mix shifts. The company specifically highlighted its expectation for the Remediation & Reuse segment to grow to more than 40% of total company revenue.

Forward-Looking Statements

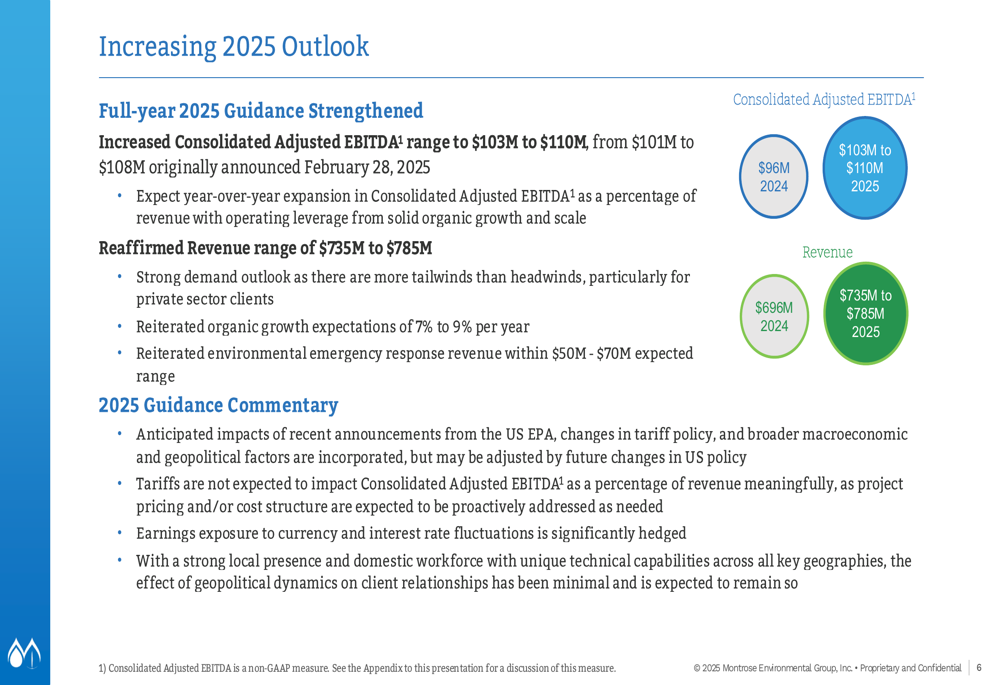

Based on its strong Q1 performance, Montrose increased its full-year 2025 guidance for Consolidated Adjusted EBITDA to a range of $103 million to $110 million, up from the previous guidance of $101 million to $108 million. The company reaffirmed its revenue guidance of $735 million to $785 million.

The updated outlook incorporates potential impacts from EPA announcements, tariff policy changes, and geopolitical factors, though management noted that tariffs are not expected to meaningfully impact Adjusted EBITDA. The company has also hedged against currency and interest rate fluctuations.

Montrose reiterated its long-term growth algorithm of 7% to 9% average annual organic growth, plus additional revenue and adjusted EBITDA from future acquisitions. The company also maintained its target of converting more than 50% of Consolidated Adjusted EBITDA to operating cash flow on an annual basis in 2025 and beyond.

Management emphasized ongoing focus on enhancing profitability through operating leverage, efficiency improvements, business maturity, and favorable segment revenue mix. These initiatives are expected to drive continued margin expansion over time, supporting the company’s long-term financial objectives.

In summary, Montrose Environmental’s Q1 2025 presentation revealed a company with strong momentum, improved financial performance, and a clear strategic direction. The record results and increased guidance suggest that the company is successfully executing its growth strategy despite previous market challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.