Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

Mowi ASA (OSE:MOWI), the world’s leading salmon producer, reported solid first-quarter 2025 results on May 14, highlighting strong operational performance despite challenging market conditions. The company achieved significant volume growth while navigating price pressures from seasonally high industry supply.

The Norwegian salmon giant reported an Operational EBIT of EUR 214 million for Q1 2025, representing a 7% increase year-over-year, driven primarily by a 12% jump in harvest volumes. This performance demonstrates Mowi’s continued execution of its volume-driven growth strategy in a competitive market environment.

Quarterly Performance Highlights

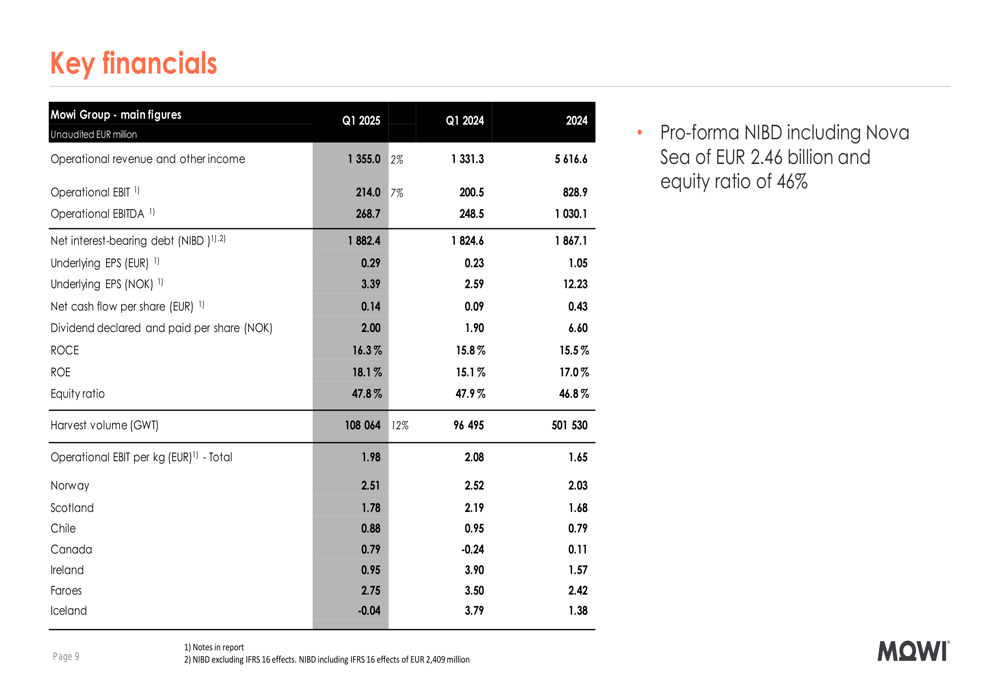

Mowi reported turnover of EUR 1.36 billion in Q1 2025, translating to an Operational EBIT of EUR 214 million. The company harvested 108,064 GWT of salmon during the quarter, marking a substantial 12% increase from the same period last year. This growth was supported by what the company described as "seasonally all-time high seawater production on strong biological KPIs."

As shown in the comprehensive financial summary below, Mowi improved several key metrics compared to Q1 2024, including Operational EBITDA, underlying EPS, and return ratios:

The company’s return on capital employed (ROCE) improved to 16.3% from 15.8% in Q1 2024, while return on equity (ROE) saw a more significant jump to 18.1% from 15.1%. These improvements came despite a slight increase in net interest-bearing debt to EUR 1,882.4 million.

Mowi declared a quarterly dividend of NOK 1.70 per share, continuing its commitment to shareholder returns amid its growth initiatives.

Growth Strategy and Volume Targets

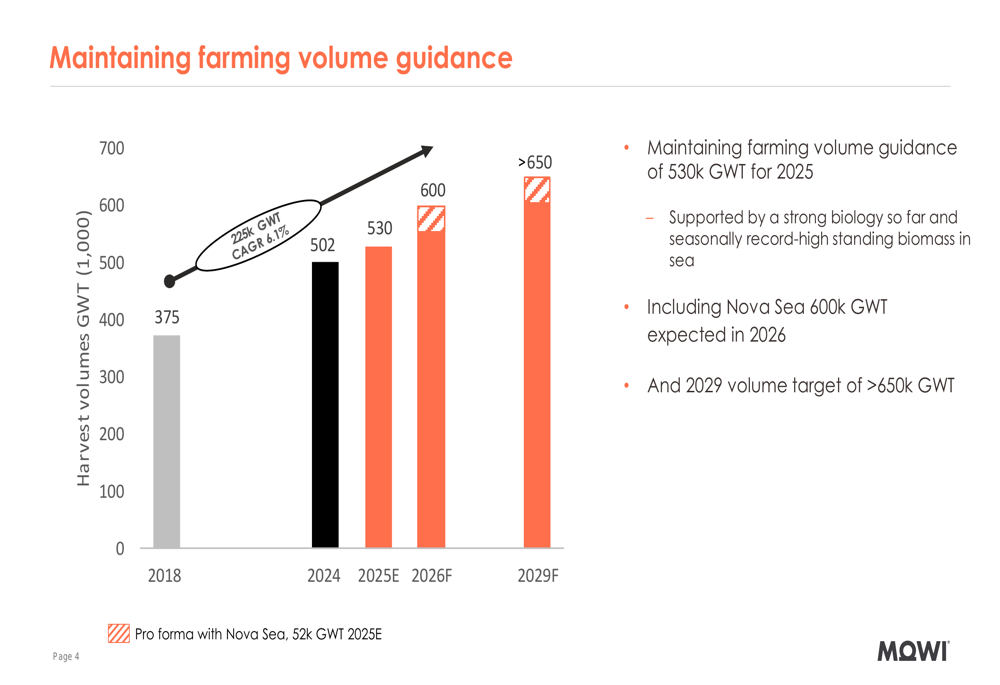

Mowi maintained its farming volume guidance of 530,000 GWT for 2025, supported by strong biological performance and seasonally record-high standing biomass in sea. The company’s long-term growth trajectory remains ambitious, with targets of 600,000 GWT in 2026 (including Nova Sea’s contribution of 52,000 GWT) and over 650,000 GWT by 2029.

This growth plan represents a compound annual growth rate (CAGR) of 6.1% from 2018 to 2029, significantly outpacing the company’s historical growth rate. The following chart illustrates Mowi’s harvest volume progression and targets:

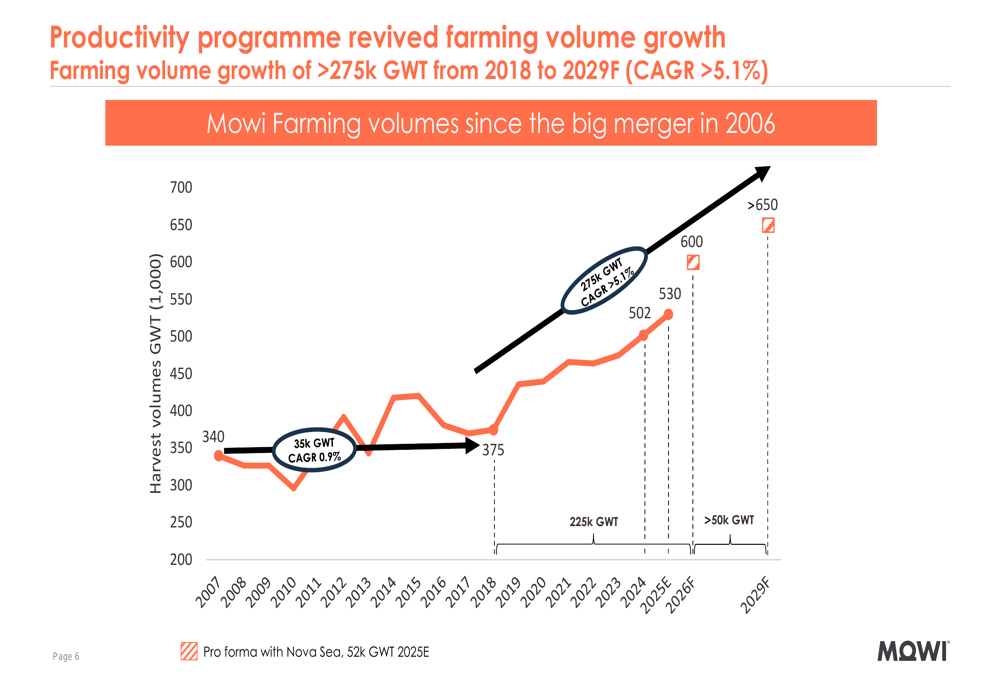

The company’s growth strategy relies heavily on increased smolt stocking and postsmolt utilization, with plans for approximately 40 million postsmolt in 2025, representing 25% coverage globally and 50% in Norway (excluding Region North). This approach has revitalized Mowi’s volume growth after a period of stagnation:

Regional Performance Analysis

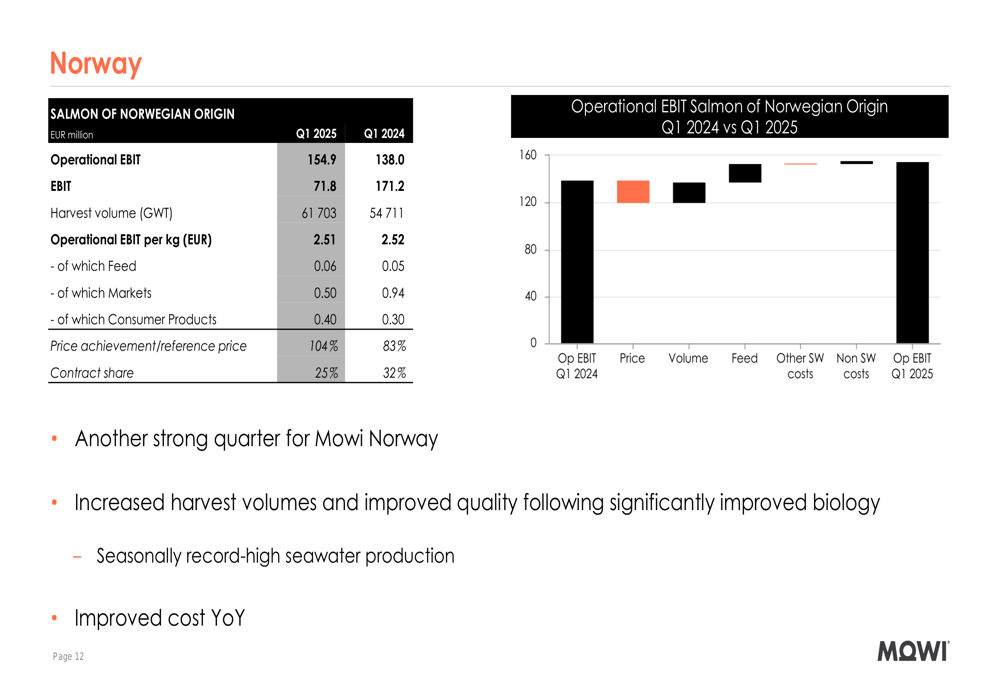

Mowi Norway delivered another strong quarter with Operational EBIT of EUR 154.9 million, up from EUR 138.0 million in Q1 2024. The region harvested 61,703 GWT, a significant increase from 54,711 GWT in the same period last year. Operational EBIT per kg remained stable at EUR 2.51 despite market pressures, supported by improved quality and cost reductions.

The detailed breakdown of Norway’s performance shows the contribution from different parts of the value chain:

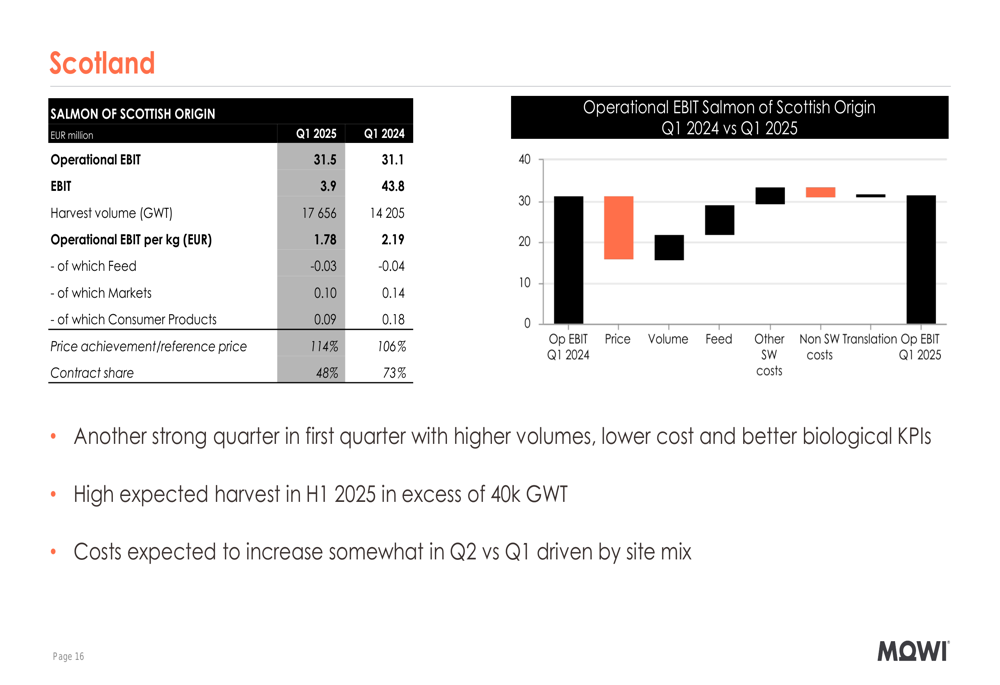

Scotland also performed well, with Operational EBIT of EUR 31.5 million on harvest volumes of 17,656 GWT, compared to EUR 31.1 million on 14,205 GWT in Q1 2024. While Operational EBIT per kg decreased to EUR 1.78 from EUR 2.19, the region benefited from higher volumes, lower costs, and improved biological KPIs.

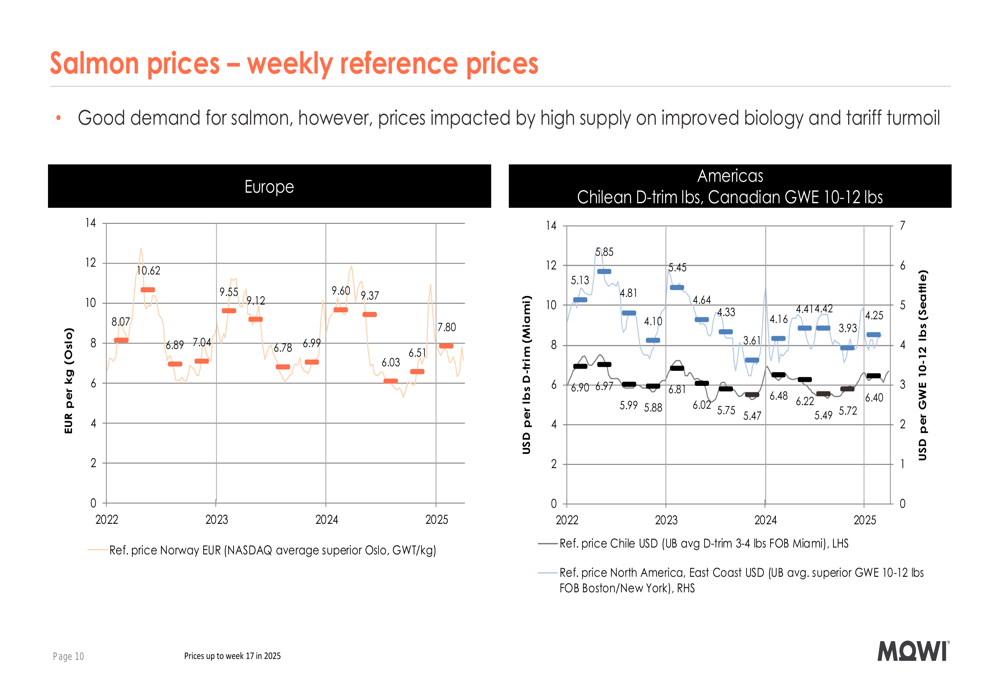

Despite good demand for salmon globally, market prices faced pressure from seasonally record-high industry supply. Mowi’s price achievement was 4% above reference price, positively impacted by contracts and good spot performance. The following chart illustrates weekly reference prices in key markets:

Forward-Looking Statements

Looking ahead, Mowi expects farming costs to decrease further in 2025, building on the reductions already achieved year-over-year. The company anticipates particularly strong harvests in Scotland during the first half of 2025, with volumes expected to exceed 40,000 GWT.

The strategic review of Mowi’s Feed division is "well under way," potentially signaling organizational changes in the future. Meanwhile, the integration of Nova Sea remains on track, with the acquisition expected to contribute significantly to Mowi’s volume growth in 2026.

Mowi continues to position itself as the leader in what it calls the "Blue Revolution," maintaining its status as the largest producer in an industry with global volumes of 2.5 million GWT. The company’s focus on biological performance, cost efficiency, and strategic growth initiatives appears to be yielding results despite challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.