Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

Mowi ASA (OB:MOWI), the world’s largest salmon producer, presented its second quarter 2025 results on August 20, showing strong volume growth despite challenging market conditions. The company achieved record Q2 harvest volumes while facing pressure on salmon prices due to high industry-wide supply.

The quarter was characterized by a significant 18% year-over-year increase in industry volumes, which put downward pressure on prices. Despite this challenging price environment, Mowi reported underlying demand growth of approximately 5% year-over-year, indicating healthy market fundamentals.

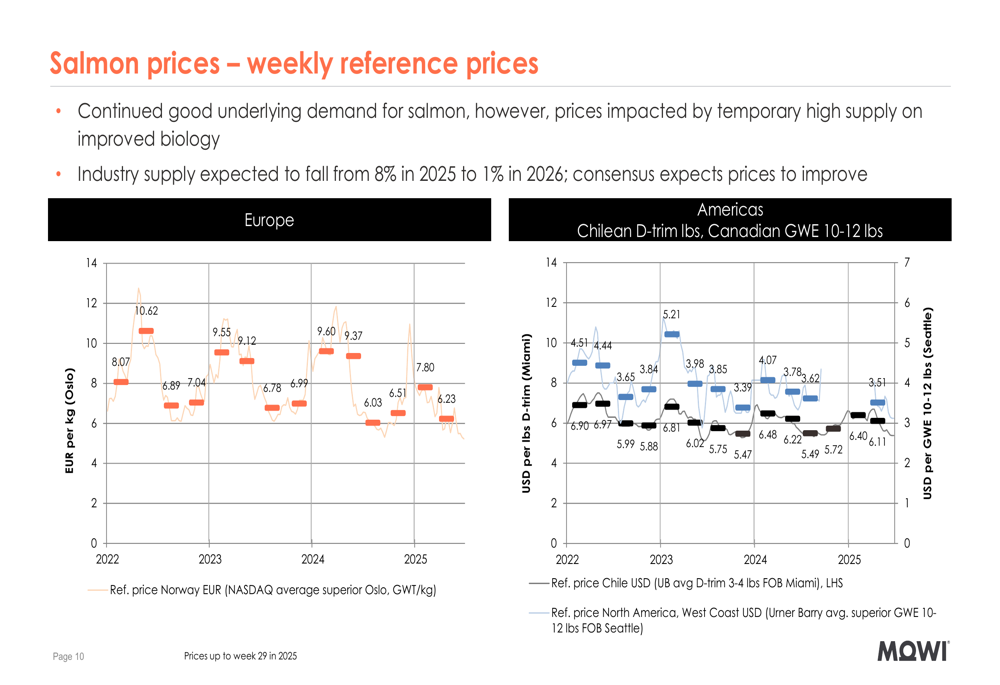

As shown in the following chart of salmon price trends, market prices have been under pressure compared to previous years:

Quarterly Performance Highlights

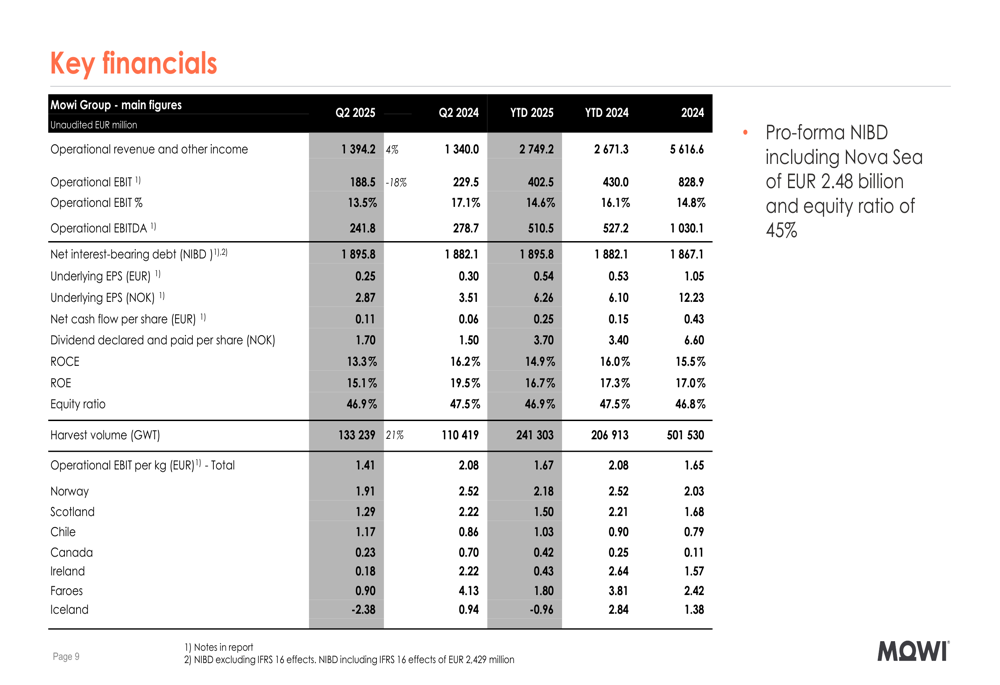

Mowi reported seasonally record-high harvest volumes of 133,239 GWT in Q2 2025, representing a substantial 21% growth compared to the same period last year. This volume increase helped the company achieve record quarterly revenue of EUR 1.39 billion, up 4% year-over-year.

However, operational EBIT declined 18% to EUR 189 million, with margins contracting from 17.1% to 13.5%, reflecting the impact of lower salmon prices. The company declared a quarterly dividend of NOK 1.45 per share.

The comprehensive financial performance is illustrated in the following table:

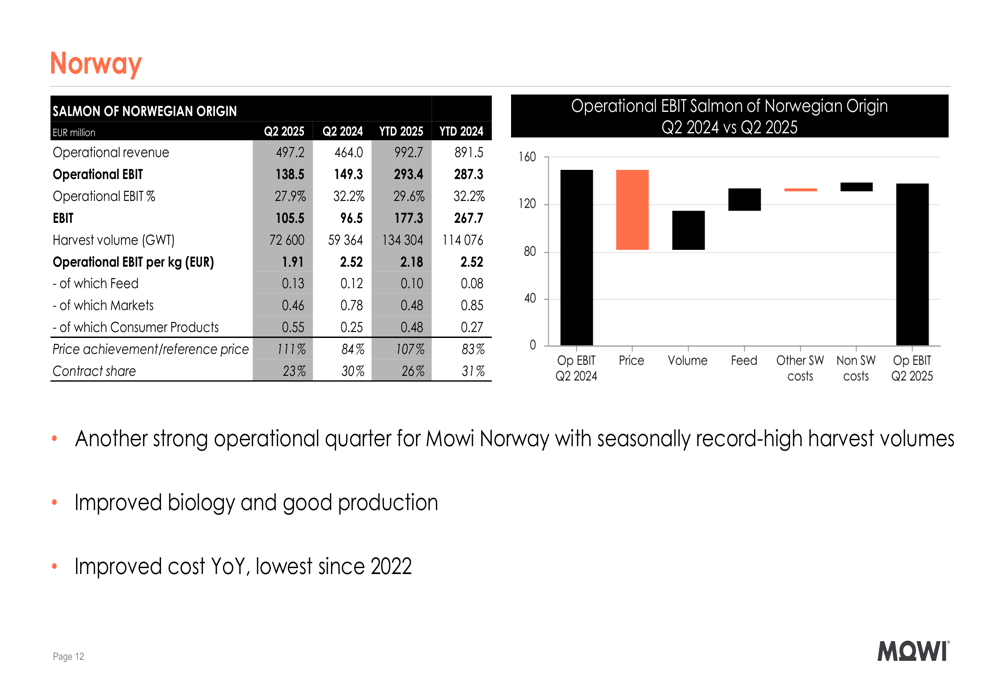

Mowi’s Norwegian operations, which represent its largest segment, delivered strong operational results despite the challenging price environment. The company highlighted improved biology and production efficiency as key drivers:

Cost Reduction Initiatives

A significant bright spot in Mowi’s Q2 results was the company’s success in reducing production costs, which helped partially offset the impact of lower salmon prices. The company achieved cost reductions of EUR 49 million in the quarter and EUR 67 million year-to-date compared to 2024.

Blended farming costs across Mowi’s seven production origins decreased to EUR 5.39 per kg, down EUR 0.45 per kg year-over-year and EUR 0.50 per kg quarter-over-quarter. This represents the lowest cost level since 2022, a notable achievement in the current inflationary environment.

Management expects this cost performance to continue in the second half of 2025, with costs projected to remain approximately stable compared to Q2 levels. This outlook aligns with the company’s Q1 2025 earnings call, where executives had expressed confidence in further reducing production costs.

Strategic Growth Plans

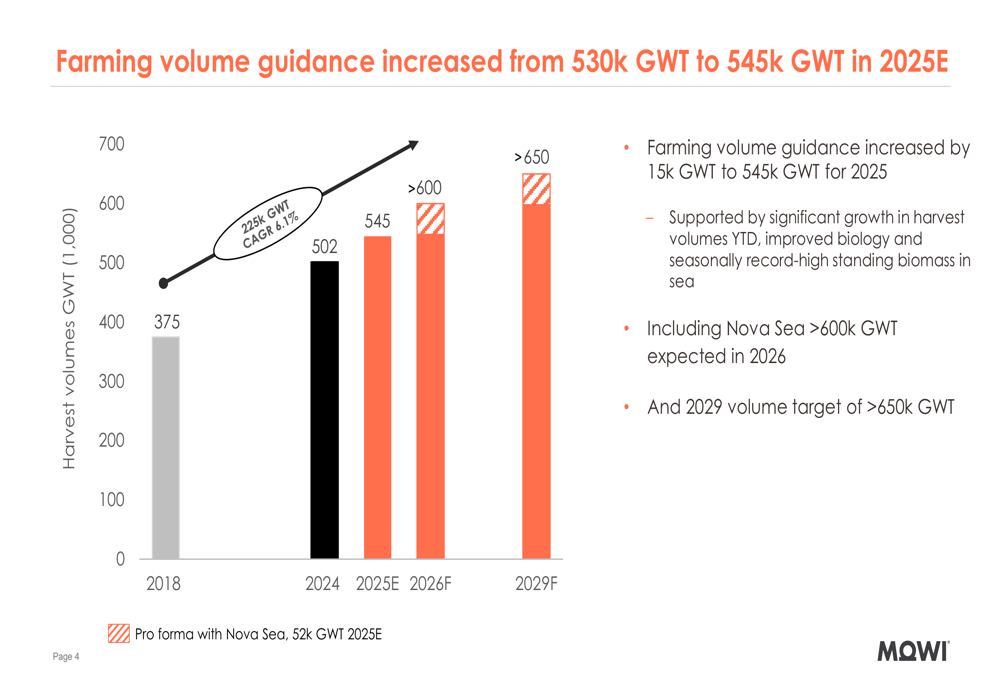

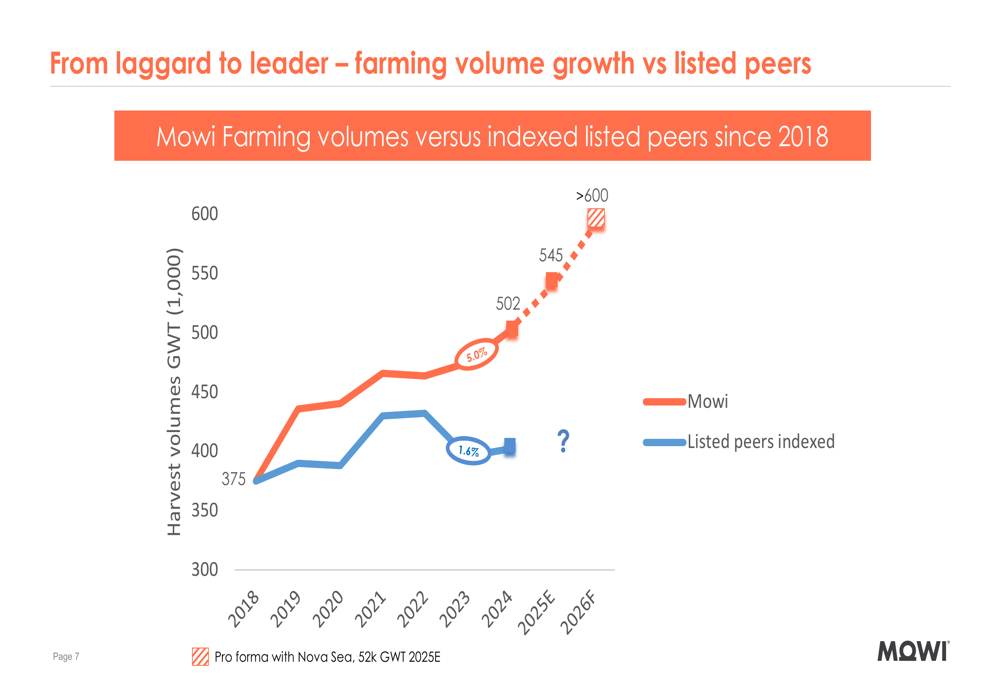

Mowi raised its 2025 farming volume guidance from 530,000 GWT (as stated in the Q1 2025 earnings call) to 545,000 GWT, citing significant growth in harvest volumes year-to-date, improved biology, and seasonally record-high standing biomass in sea.

The company’s long-term growth trajectory remains ambitious, with targets of over 600,000 GWT in 2026 (including the Nova Sea acquisition) and over 650,000 GWT by 2029. This represents a compound annual growth rate (CAGR) of over 5.1% from 2018 to 2029.

The following chart illustrates Mowi’s harvest volume growth trajectory:

This growth strategy is supported by increased smolt stocking on unutilized licenses and improved productivity through postsmolt production on utilized licenses. The company plans to produce approximately 40 million postsmolt in 2025, representing 25% coverage globally and 50% in Norway (excluding Region North).

Mowi’s farming volume growth has outpaced that of its listed peers, as shown in the following comparison:

Forward-Looking Statements

Looking ahead, Mowi expects industry supply growth to decrease from 8% in 2025 to just 1% in 2026, which should support price recovery according to market consensus. The company noted that underlying demand remains good, with approximately 5% growth year-over-year.

The Consumer Products and Feed segments both achieved seasonally record-high earnings and volumes in Q2. Management mentioned that a strategic review of the Feed division is progressing, potentially signaling future changes in this business unit.

While the presentation highlighted numerous positive developments, investors should note that operational EBIT declined by 18% year-over-year in Q2, contrasting with the 14 million euro increase reported in Q1 2025. This suggests that market conditions have become more challenging as 2025 has progressed, despite the company’s success in volume growth and cost reduction.

With continued focus on operational efficiency, biological improvements, and strategic growth initiatives, Mowi appears well-positioned to navigate the current market challenges while building capacity for long-term growth in the global salmon industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.