US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

MPLX LP (NYSE:MPLX) reported its second quarter 2025 results on August 5, revealing a strategic focus on Permian Basin expansion despite missing analyst expectations. The midstream operator’s stock declined 2.87% to close at $52.71 following the announcement, with pre-market trading showing an additional 0.42% drop to $52.49.

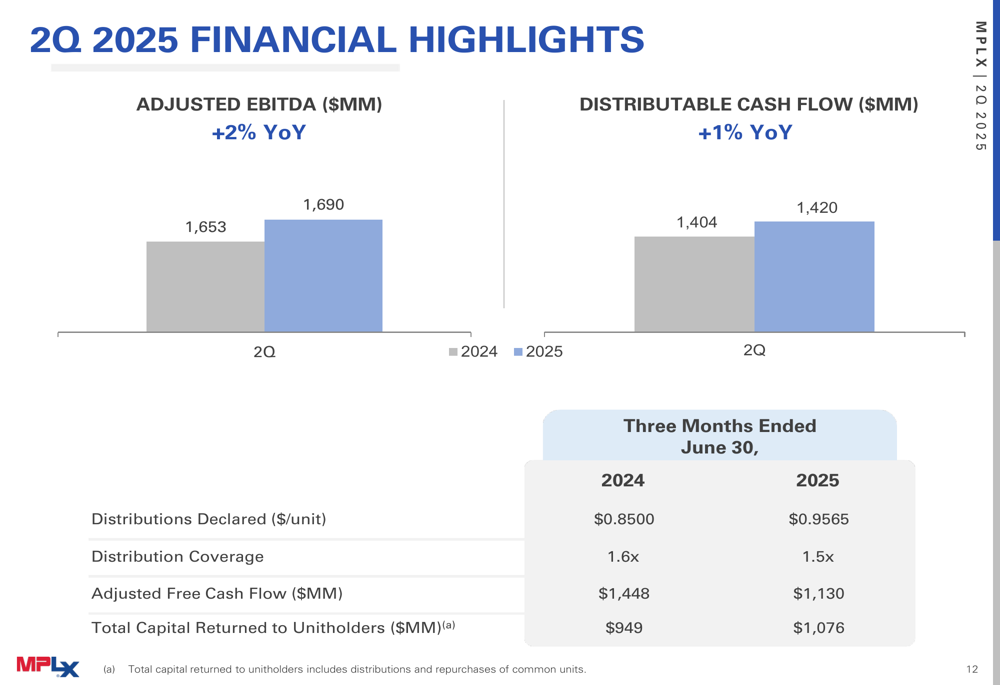

The company reported adjusted EBITDA of $1.7 billion, representing a modest 2% year-over-year increase, while distributable cash flow grew 1% to $1.4 billion. However, these results fell short of analyst expectations, with earnings per share of $1.03 missing forecasts by 2.83% and revenue of $3 billion coming in 5.66% below projections.

Quarterly Performance Highlights

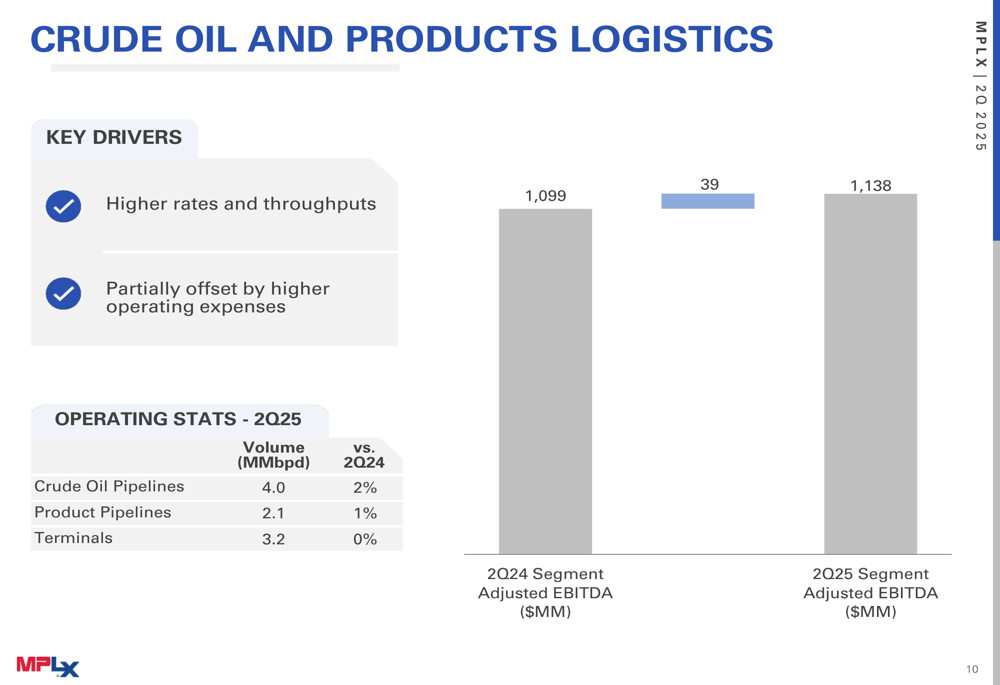

MPLX’s performance showed mixed results across its two primary business segments. The Crude Oil and Products Logistics segment delivered adjusted EBITDA of $1,138 million, up from $1,099 million in Q2 2024, driven by higher rates and throughputs despite increased operating expenses.

As shown in the following segment performance breakdown:

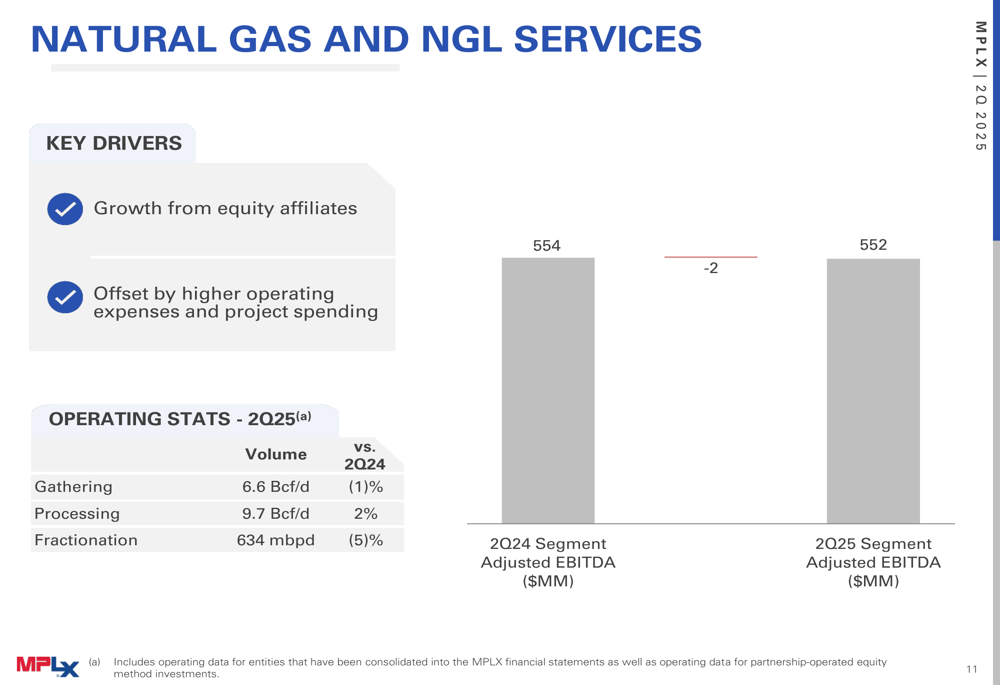

Meanwhile, the Natural Gas and NGL Services segment reported a slight decline in adjusted EBITDA to $552 million from $554 million in the prior year period, with growth from equity affiliates offset by higher operating expenses and project spending.

The company’s overall financial position remains solid, with year-to-date adjusted EBITDA increasing 5% compared to the same period in 2024. MPLX maintained its distribution coverage at 1.5x while returning $1,076 million to unitholders through distributions and unit repurchases.

The following chart illustrates key financial metrics for the quarter:

Strategic Initiatives

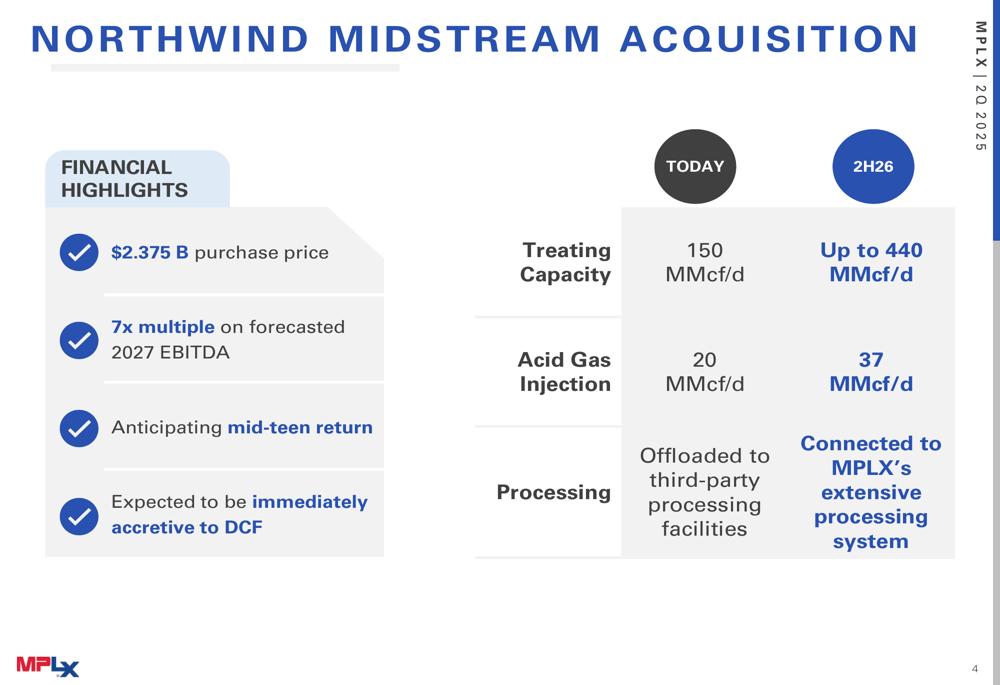

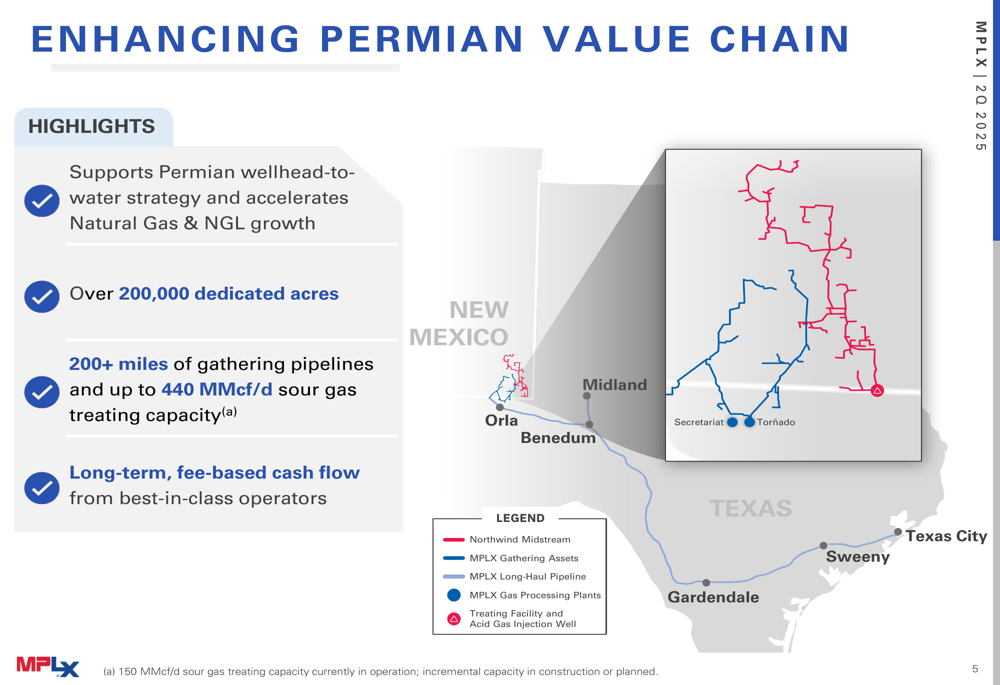

The centerpiece of MPLX’s strategic initiatives is the $2.375 billion acquisition of Northwind Midstream, which the company expects to be immediately accretive to distributable cash flow. This acquisition significantly expands MPLX’s presence in the Delaware Basin with 200,000 dedicated acres and enhances its sour gas treating capacity.

The following details highlight the Northwind Midstream acquisition terms and operational metrics:

This acquisition strengthens MPLX’s integrated Permian Basin value chain, supporting its "wellhead-to-water" strategy and accelerating natural gas and NGL growth. The assets include over 200 miles of gathering pipelines and up to 440 MMcf/d of sour gas treating capacity, providing long-term, fee-based cash flow from established operators.

The strategic positioning of these assets is illustrated in this regional map:

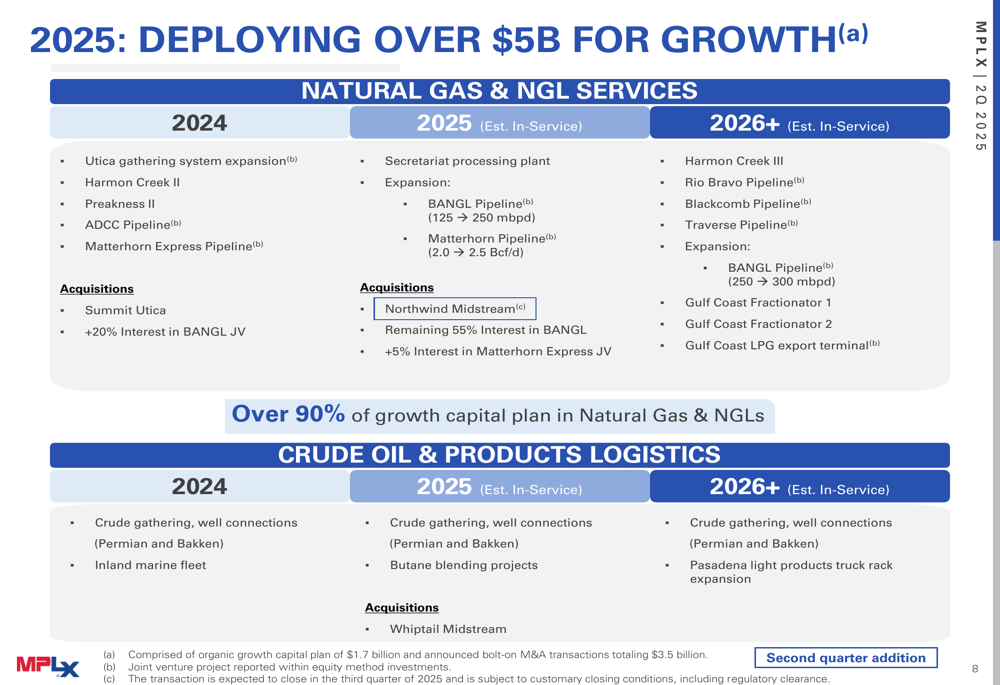

MPLX is deploying over $5 billion for growth initiatives across its natural gas, NGL, crude oil, and products logistics segments. The company’s investment strategy includes multiple projects with in-service dates spanning from 2025 through 2029.

Forward-Looking Statements

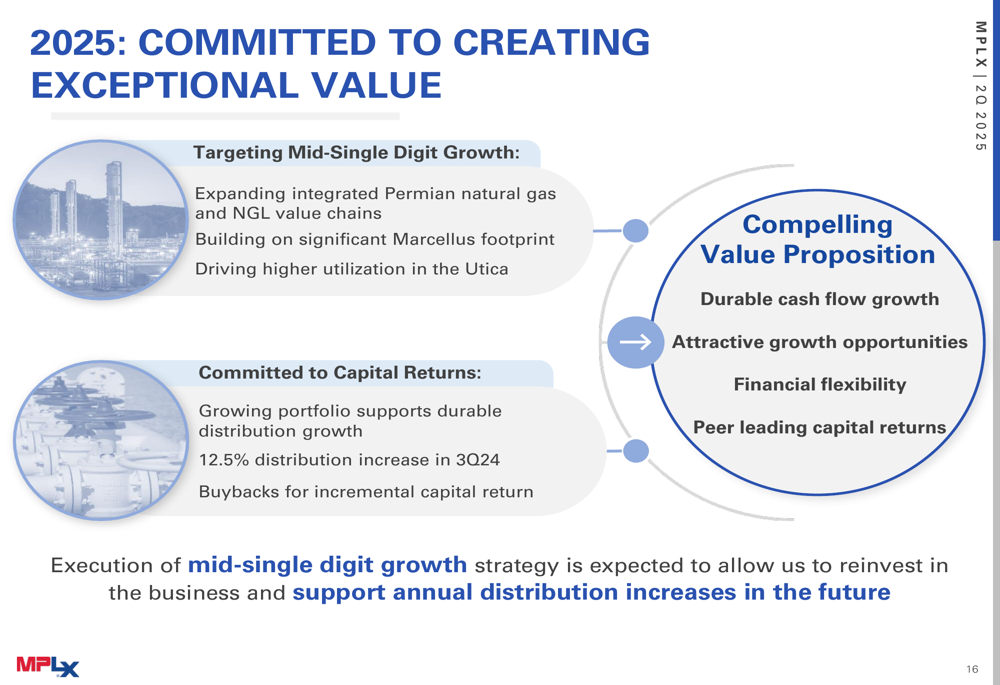

Despite the earnings miss, MPLX maintains an optimistic outlook, targeting mid-single-digit adjusted EBITDA growth while continuing to return capital to unitholders. The company announced a 12.5% distribution increase to $0.9565 per unit in Q3 2024, reflecting confidence in sustainable cash flow generation.

MPLX’s financial priorities remain focused on maintaining asset safety and reliability, growing distributions as its primary return of capital tool, pursuing disciplined growth opportunities, and providing incremental returns to unitholders when appropriate.

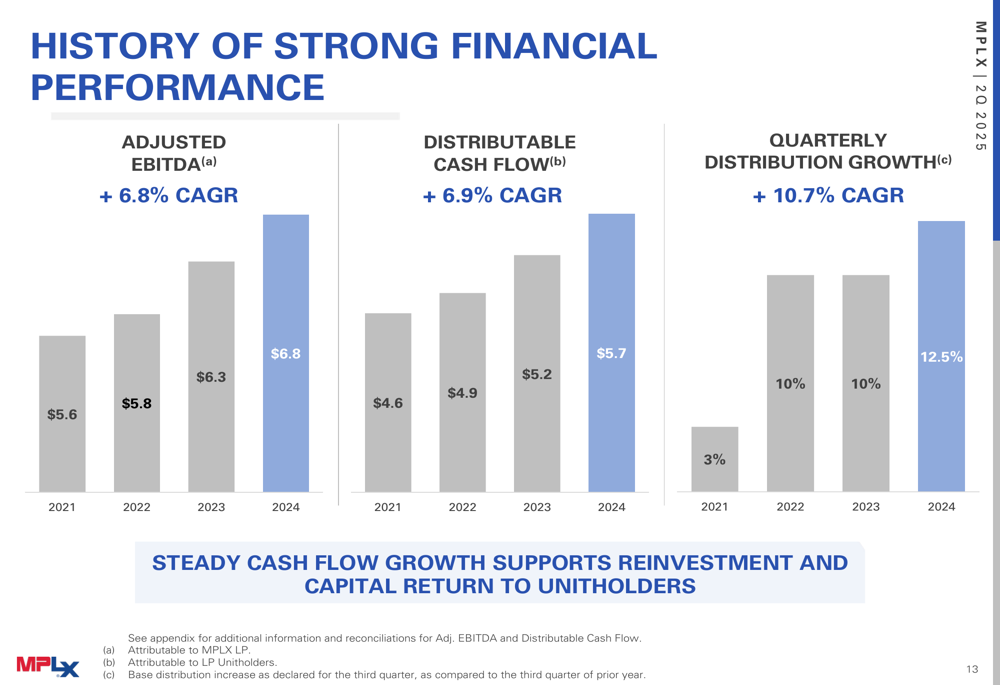

The company’s long-term performance demonstrates consistent growth across key financial metrics:

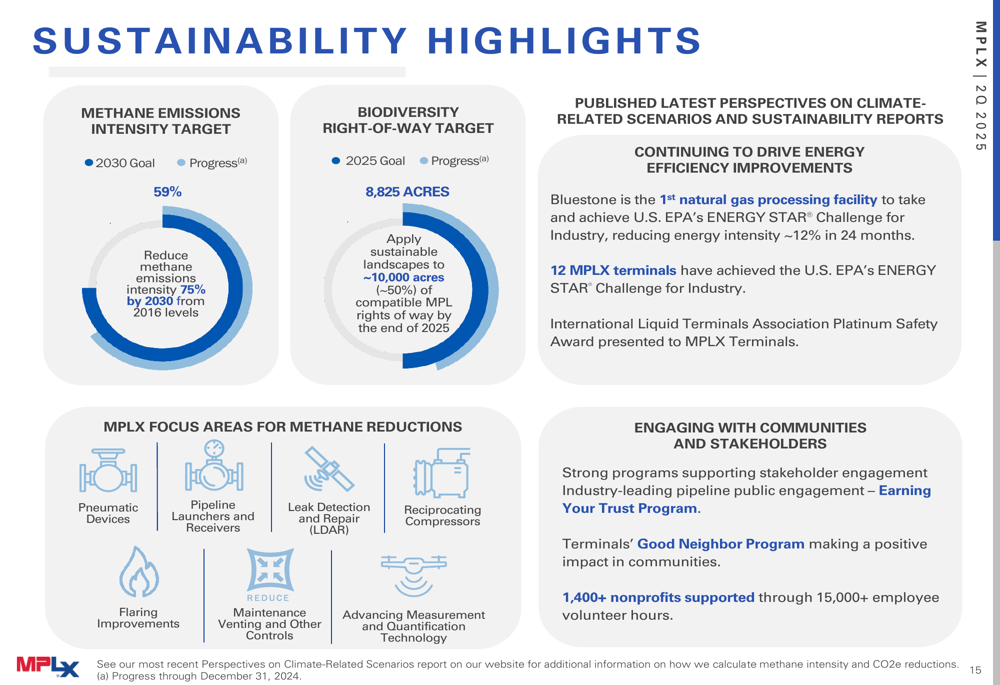

MPLX also highlighted its sustainability initiatives, including targets to reduce methane emissions intensity by 75% by 2030 from 2016 levels and apply sustainable landscapes to approximately 10,000 acres of rights-of-way by the end of 2025.

Analyst Perspectives

Despite management’s optimistic outlook, market reaction to MPLX’s quarterly results was negative, with shares declining nearly 3% following the announcement. Analysts expressed concerns about the earnings and revenue misses, though many acknowledged the strategic value of the Northwind acquisition.

During the earnings call, CEO Mary Anne Mannen emphasized the compelling economics of the Northwind transaction and highlighted the company’s competitive advantages in the Permian Basin and LPG export market. However, questions remain about integration challenges with recent acquisitions and the company’s dependence on the Permian Basin for growth.

MPLX’s commitment to creating exceptional value centers on expanding its integrated Permian natural gas and NGL value chains, building on its significant Marcellus footprint, and driving higher utilization in the Utica. The company believes these initiatives, combined with its financial flexibility and peer-leading capital returns, create a compelling value proposition for investors.

With a strong balance sheet showing a consolidated total debt to LTM adjusted EBITDA ratio of 3.1x, MPLX appears well-positioned to execute its growth strategy while maintaining its commitment to returning capital to unitholders, despite the near-term headwinds reflected in its Q2 2025 performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.