Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

Munters Group AB (STO:MTRS) presented its Q3 2025 financial results on October 24, 2025, showcasing strong overall growth despite challenges in certain segments. The company’s stock responded positively to the earnings report, surging 18.95% to close at 154.2 SEK, reflecting investor confidence in the company’s performance and strategic direction.

The climate control solutions provider demonstrated robust growth in order intake and net sales, with particularly strong performance in its Data Center Technologies (DCT) segment, while navigating headwinds in its AirTech business. The presentation highlighted Munters’ continued focus on innovation, strategic investments, and cost optimization measures.

Quarterly Performance Highlights

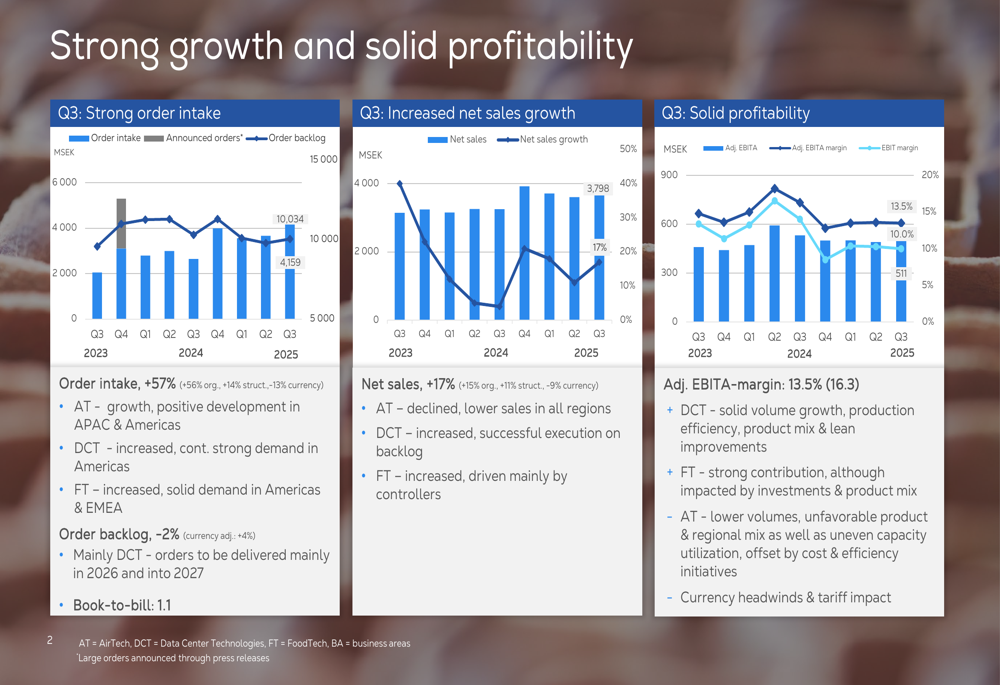

Munters reported exceptional growth in order intake for Q3 2025, reaching 4,159 MSEK, a 57% increase compared to the same period last year. This growth was primarily driven by organic growth (56%), with additional contribution from structural changes (14%), partially offset by negative currency effects (-13%). The company’s order backlog stood at an impressive 10,034 MSEK, providing strong visibility for future revenues.

As shown in the following chart of quarterly financial performance:

Net sales also showed healthy growth of 17%, reaching 3,798 MSEK, with organic growth contributing 15%, structural changes adding 11%, and currency effects reducing the figure by 9%. The adjusted EBITA margin was 13.5%, down from 16.3% in Q3 2024, primarily impacted by challenges in the AirTech segment and currency headwinds.

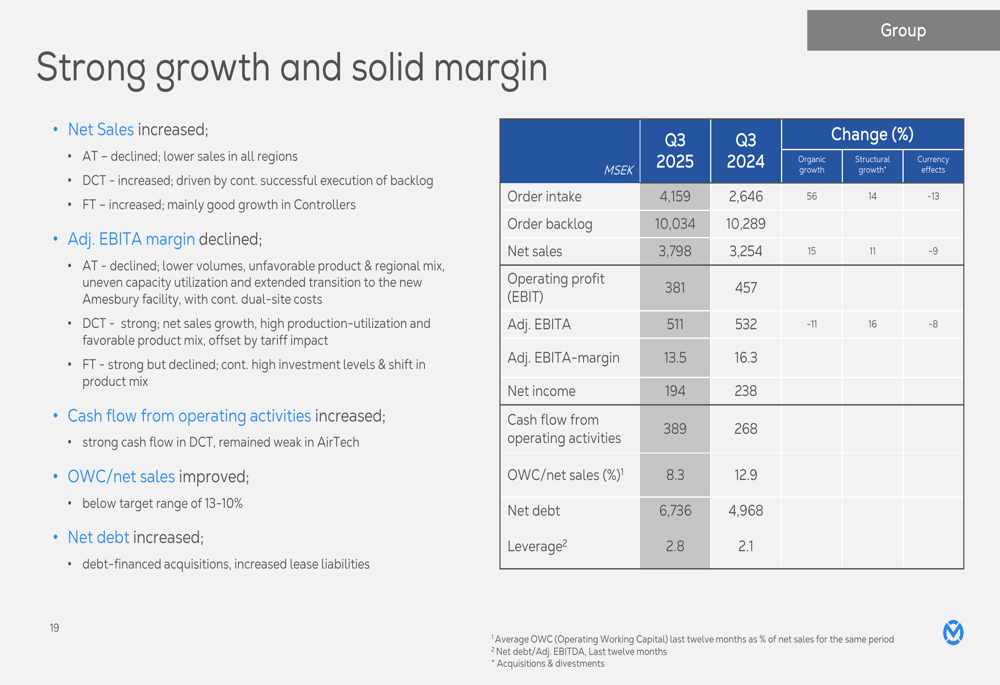

The company’s overall financial health remained solid, as demonstrated in the group financial summary:

Business Segment Analysis

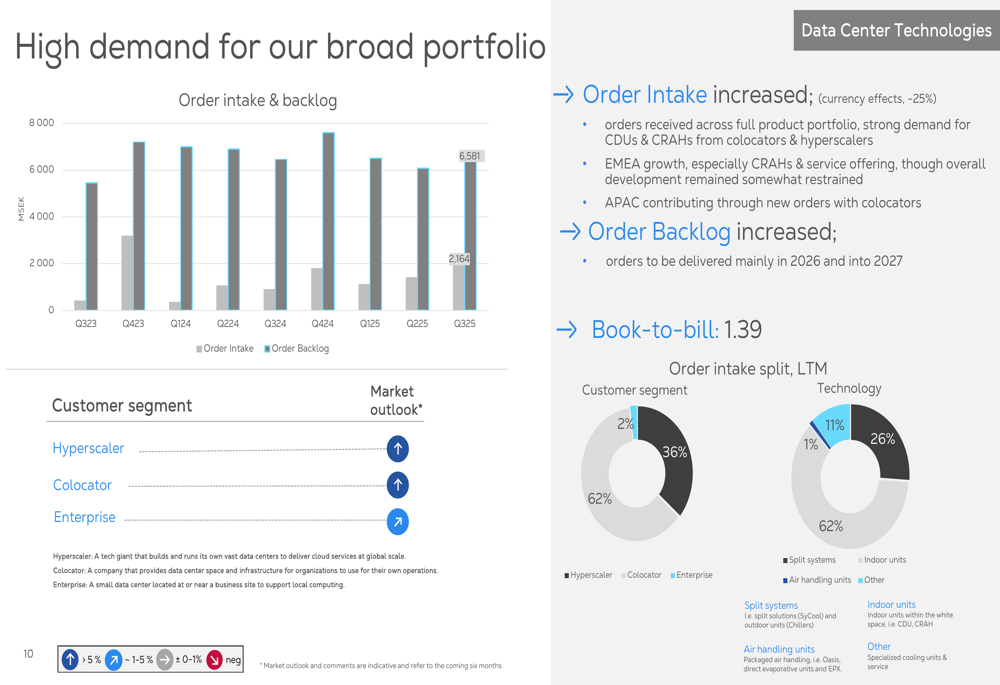

Data Center Technologies: Driving Growth

The DCT segment emerged as the primary growth driver for Munters in Q3 2025, with order intake increasing significantly to 2,164 MSEK. The segment maintained a strong book-to-bill ratio of 1.39, indicating continued growth momentum. Customer demand was particularly strong from colocators (62% of order intake) and hyperscalers (36%), with a positive market outlook for both segments.

The following chart illustrates DCT’s order intake and backlog:

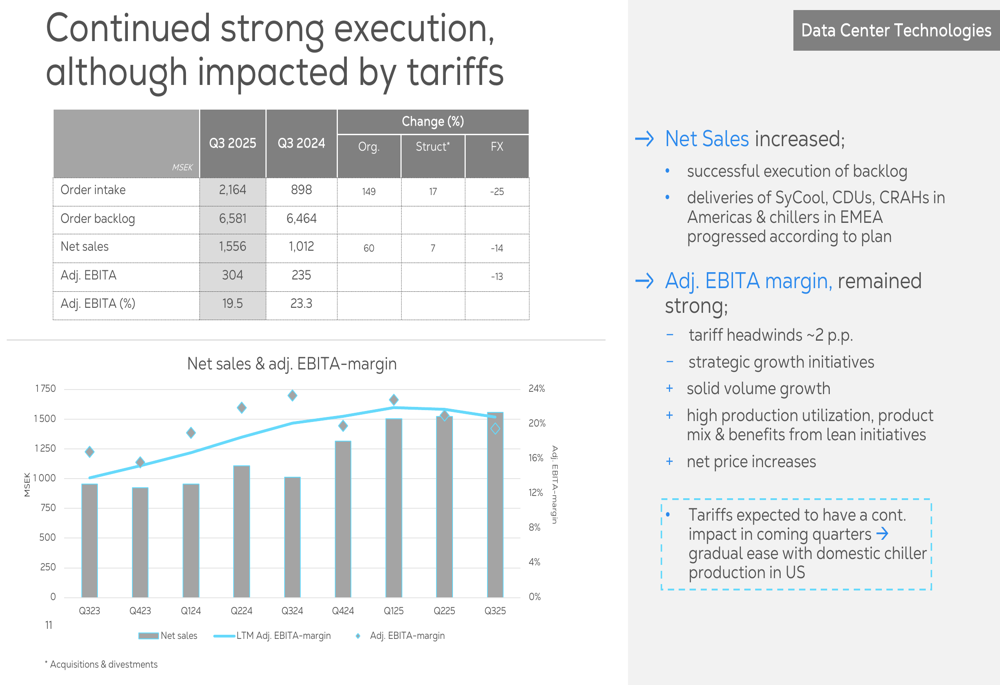

Despite the strong execution, DCT’s profitability was impacted by tariffs, though it maintained a robust adjusted EBITA margin of 19.5%. Net sales increased to 1,556 MSEK, reflecting successful execution on the backlog.

The segment’s strong order backlog extends well into 2026 and 2027, with several significant projects in the pipeline. Munters is positioning itself strategically in the growing market for AI infrastructure cooling solutions, emphasizing modularity to accelerate scalable growth.

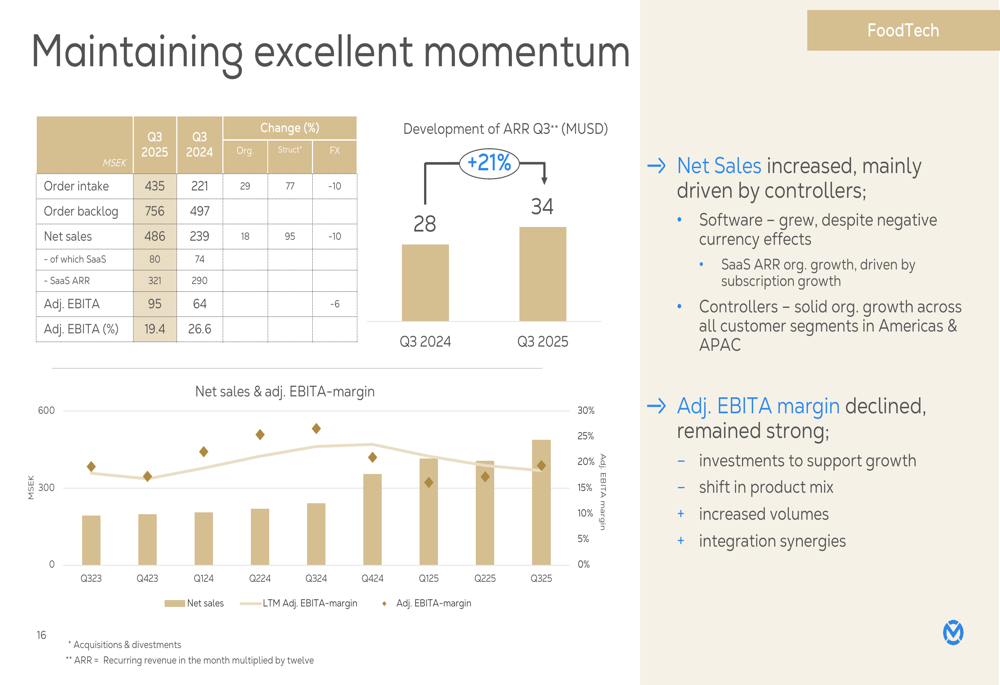

FoodTech: Maintaining Momentum

The FoodTech segment continued its excellent performance, with order intake increasing to 435 MSEK and net sales rising to 486 MSEK. The segment achieved an impressive adjusted EBITA margin of 19.4%, demonstrating the success of its digital transformation strategy.

FoodTech’s strong performance was driven primarily by demand in the Americas, with controllers accounting for 74% of order intake and software for 26%. The segment is increasingly leveraging AI technologies to enhance efficiency and customer relationships, including the Calvin suite of AI-powered agents and the Clarity AI virtual assistant.

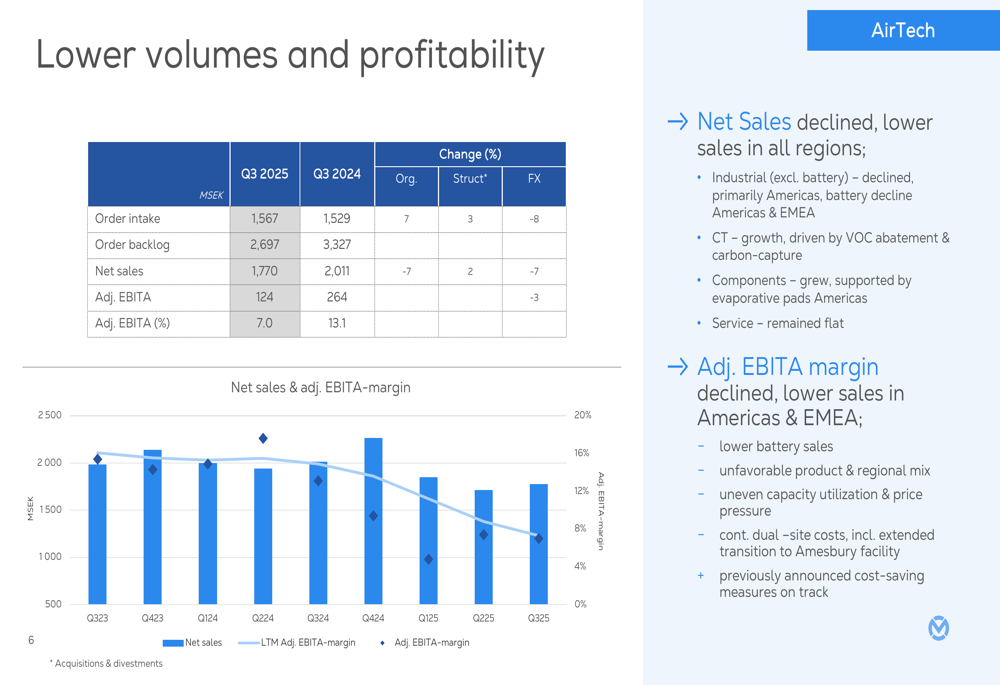

AirTech: Navigating Challenges

In contrast to the strong performance in other segments, AirTech faced challenges in Q3 2025, with lower volumes and profitability. Order intake was 1,567 MSEK, while net sales decreased to 1,770 MSEK. The adjusted EBITA margin declined significantly to 7.0% from 13.1% in Q3 2024.

To address these challenges, Munters is implementing cost-saving measures expected to yield annual net savings of 250-300 MSEK, with full effect by the end of 2026. The restructuring charge of approximately 150 MSEK will be recognized across Q4 2025 and Q1 2026.

Despite the current challenges, AirTech secured a significant new order from a leading US battery cell manufacturer in Q4 2025, valued at approximately 30 MUSD, demonstrating the segment’s technological leadership despite the continued weak battery market.

Strategic Initiatives & Outlook

Munters is pursuing several strategic initiatives to drive future growth and improve profitability. The company is making continuous investments to support its next growth wave, with a focus on expanding capacity and enhancing product offerings.

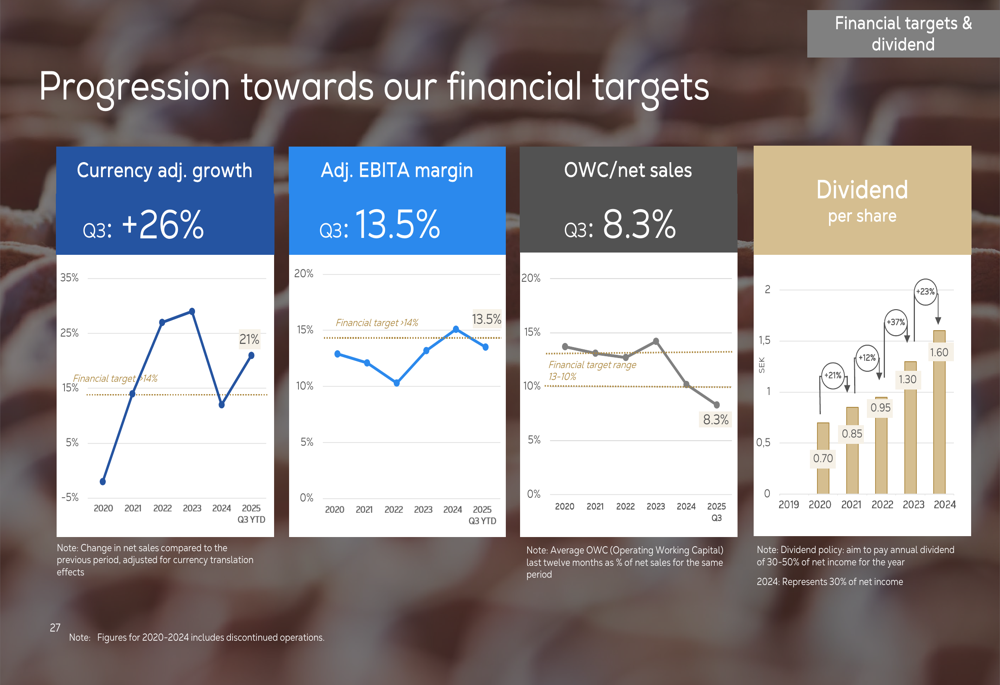

The company’s progress toward its long-term financial targets shows mixed results, with strong performance in currency-adjusted growth (26% in Q3) and operating working capital (8.3% of net sales), while the adjusted EBITA margin (13.5%) remains within the target range of 13-16%.

Munters is also advancing its sustainability agenda, having issued a 1 BSEK green bond in September 2025 under its MTN program launched in May 2025. The company is focusing on expanding circularity in its operations and products.

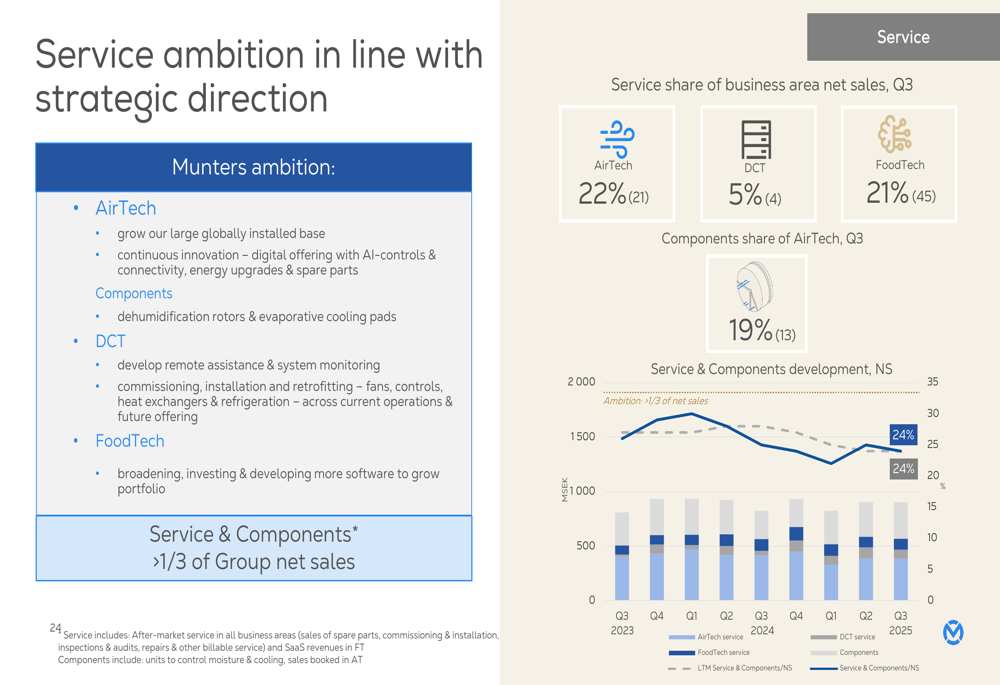

Service growth remains a strategic priority, with the ambition to increase service share to more than one-third of net sales. Currently, service accounts for 22% of AirTech’s net sales, 5% of DCT’s, and 21% of FoodTech’s.

Market Reaction & Conclusion

The market responded positively to Munters’ Q3 2025 results, with the stock price increasing by 18.95% following the earnings release. This surge reflects investor confidence in the company’s growth trajectory and strategic initiatives, despite challenges in the AirTech segment.

According to the earnings article, analysts maintain a strong buy consensus on Munters stock, with price targets between $14.32 and $21.22. The company’s financial health is rated as "GOOD," with last twelve months EBITDA reaching $224.52 million.

Looking ahead, Munters remains optimistic about its future prospects, particularly in the data center and food technology sectors. The company’s diversified business model, as highlighted by CEO Klas Forsström, positions it well to navigate ongoing challenges such as tariffs, geopolitical tensions, and market unpredictability. While the battery market remains subdued, the company’s strategic cost-saving measures and continued innovation efforts should help mitigate near-term headwinds and support long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.