Still betting on Nvidia? Our AI picked this stock instead; it’s up 96%+ THIS MONTH

Myers Industries Inc (NYSE:MYE) released its first quarter 2025 results on May 1, showing essentially flat revenue but improved profitability as the company continues its "Focused Transformation" initiative aimed at enhancing operational efficiency and shareholder returns.

Quarterly Performance Highlights

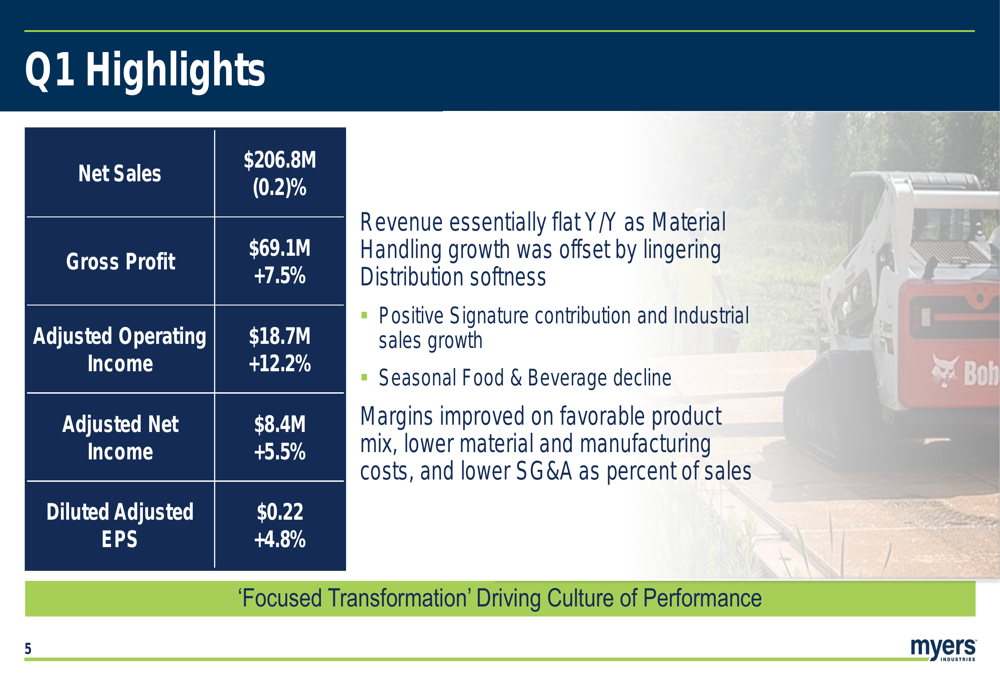

Myers reported Q1 2025 net sales of $206.8 million, a slight decrease of 0.2% compared to the same period last year. Despite the flat revenue, the company achieved notable improvements in profitability metrics, with gross profit increasing 7.5% to $69.1 million and adjusted operating income rising 12.2% to $18.7 million.

Adjusted net income grew 5.5% to $8.4 million, while diluted adjusted earnings per share increased 4.8% to $0.22. The company’s adjusted EBITDA margin expanded by 170 basis points to 13.8%.

"Our first quarter results demonstrate the early progress of our transformation initiatives, with meaningful margin expansion despite flat revenue," said Aaron Schapper, President and CEO of Myers Industries, according to the presentation.

As shown in the following comprehensive financial overview:

The company’s stock closed at $10.50 on April 30, 2025, and was trading down 1.9% in premarket activity at $10.30, according to available market data. This follows a challenging period for the stock, which has traded between $9.06 and $23.05 over the past 52 weeks.

Segment Performance Analysis

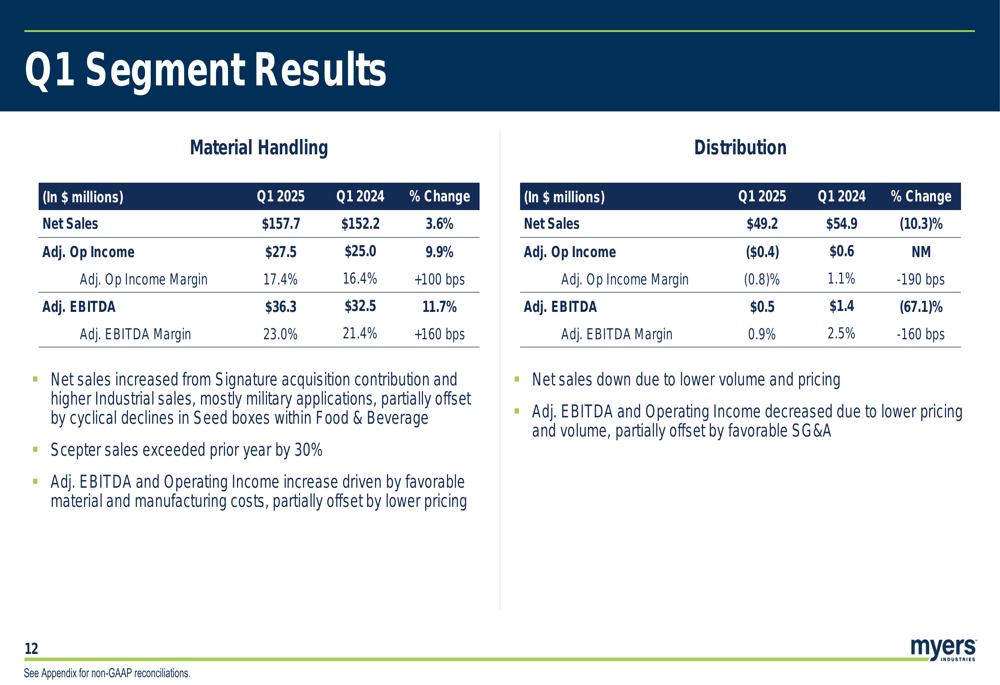

Myers’ performance showed a stark contrast between its two business segments. The Material Handling segment, which represents approximately 76% of total sales, delivered net sales of $157.7 million, an increase of 3.6% year-over-year. This segment’s adjusted operating income rose 9.9% to $27.5 million, with margin expansion of 100 basis points to 17.4%.

Conversely, the Distribution segment struggled with a 10.3% decline in net sales to $49.2 million and reported an adjusted operating loss of $0.4 million, compared to positive operating income in the prior year period.

The following segment breakdown illustrates these divergent performances:

The Material Handling segment benefited from the Signature Systems acquisition and higher Industrial sales, partially offset by declines in Seed boxes. Notably, Scepter sales exceeded the prior year by 30%, demonstrating strong momentum in this product line.

Strategic Initiatives & Transformation

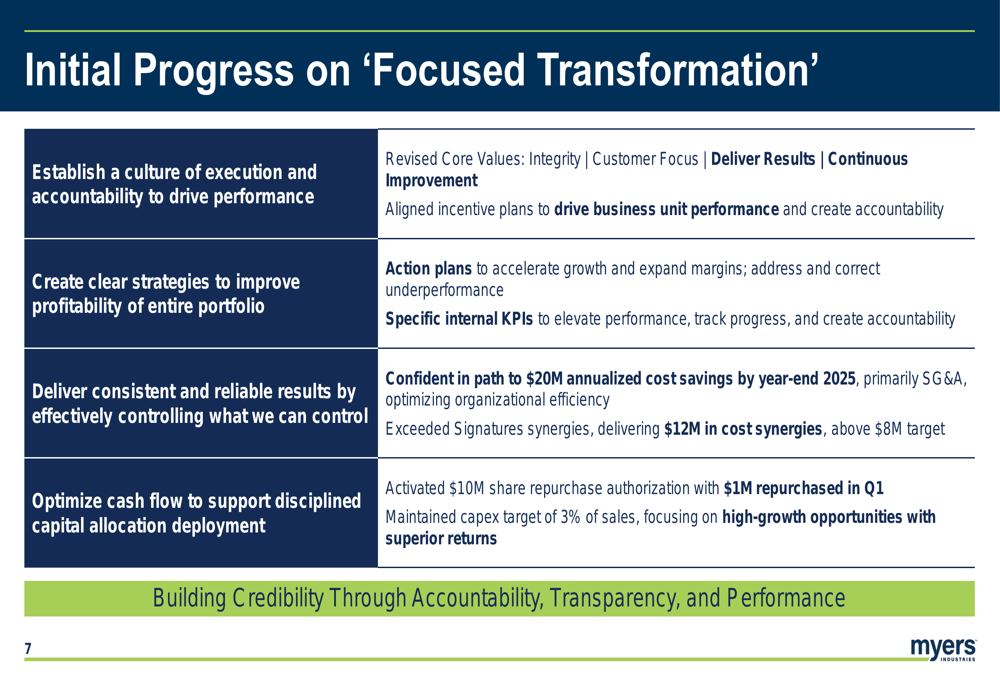

A central theme of Myers’ presentation was its "Focused Transformation" initiative, which aims to establish a culture of execution and accountability while optimizing cash flow for disciplined capital allocation. The company reported exceeding its Signature acquisition synergy targets, delivering $12 million in cost synergies compared to the original target of $8 million.

Myers has activated a $10 million share repurchase authorization, with $1 million repurchased in Q1. The company is targeting $20 million in annualized cost savings by year-end 2025, primarily through SG&A reductions.

The following slide details the progress on these transformation initiatives:

The company is also highlighting innovative products that align with its mission of protection. Its OmniDeck® flooring system protects athletic fields during non-sporting events, while its Scepter ammunition packaging solutions offer lightweight alternatives to traditional wood and steel containers for military applications.

The following image showcases the OmniDeck system being used at SoFi (NASDAQ:SOFI) Stadium:

Supply Chain Resilience

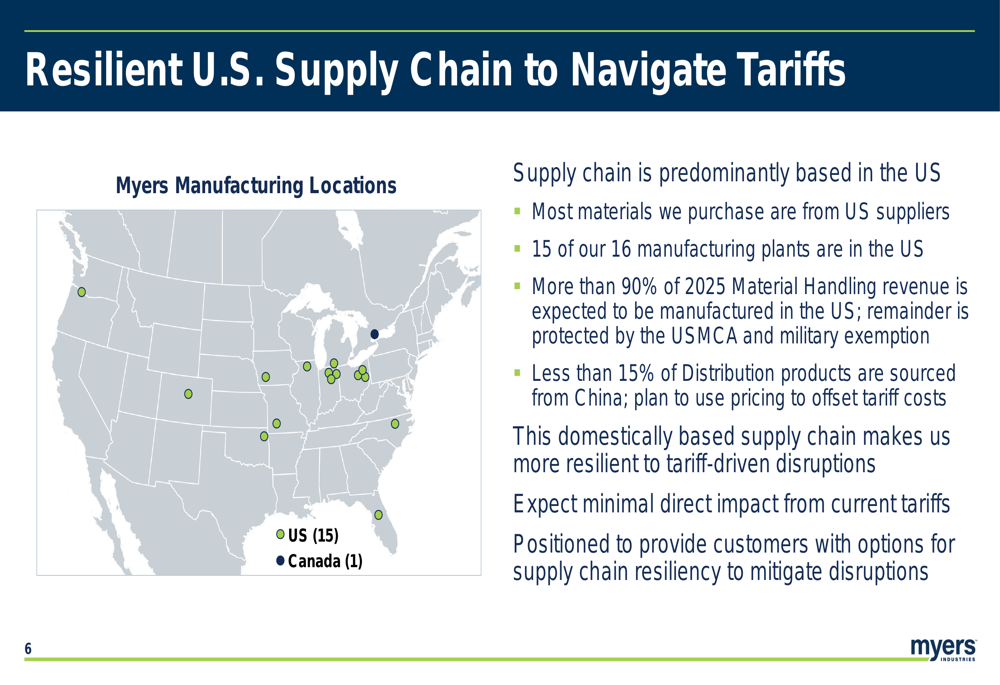

In the current environment of trade tensions and potential tariff impacts, Myers emphasized its predominantly U.S.-based supply chain as a competitive advantage. The company noted that 15 of its 16 manufacturing plants are located in the United States, with over 90% of 2025 Material Handling revenue expected to be manufactured domestically.

This manufacturing footprint is illustrated in the following map:

According to the presentation, less than 15% of Distribution products are sourced from China, leading management to expect minimal direct impact from current tariffs. This positioning could provide Myers with a competitive advantage if trade tensions escalate further.

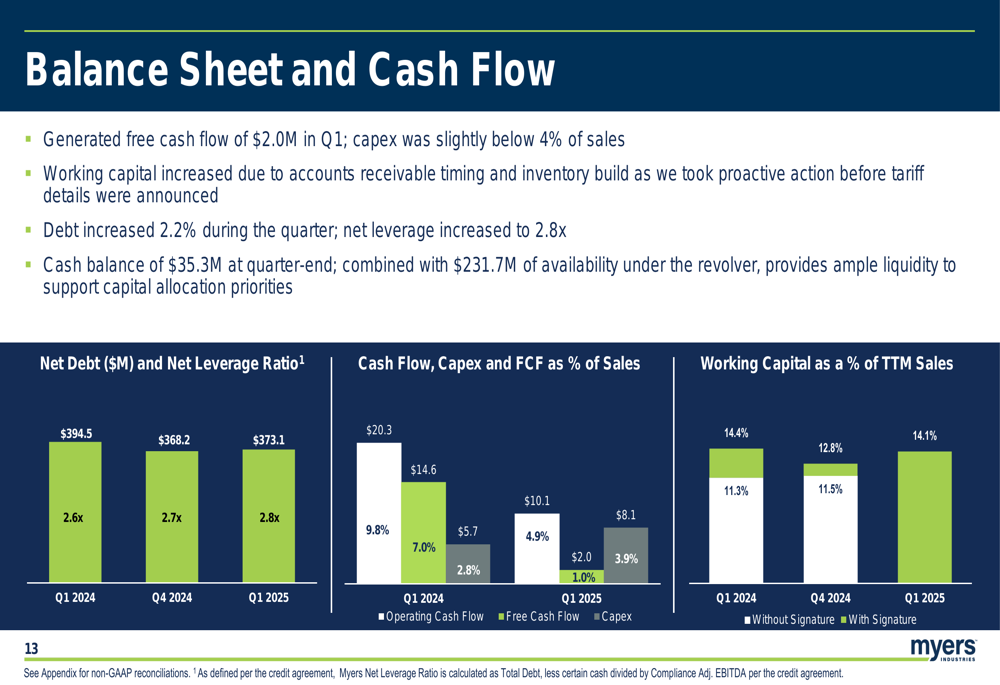

Financial Position & Capital Allocation

Myers generated $2.0 million in free cash flow during Q1, with capital expenditures slightly below 4% of sales. The company’s working capital increased due to accounts receivable timing and inventory build in anticipation of tariff details.

The balance sheet showed a debt increase of 2.2% during the quarter, resulting in a net leverage ratio of 2.8x, which is above the company’s target range of 1.5x to 2.5x. Myers maintained a cash balance of $35.3 million at quarter-end, with $231.7 million of availability under its revolving credit facility.

The following charts illustrate these financial metrics:

Management reiterated its commitment to a disciplined capital allocation approach, maintaining its dividend practice while targeting debt reduction to return to its leverage ratio goal.

Forward-Looking Statements

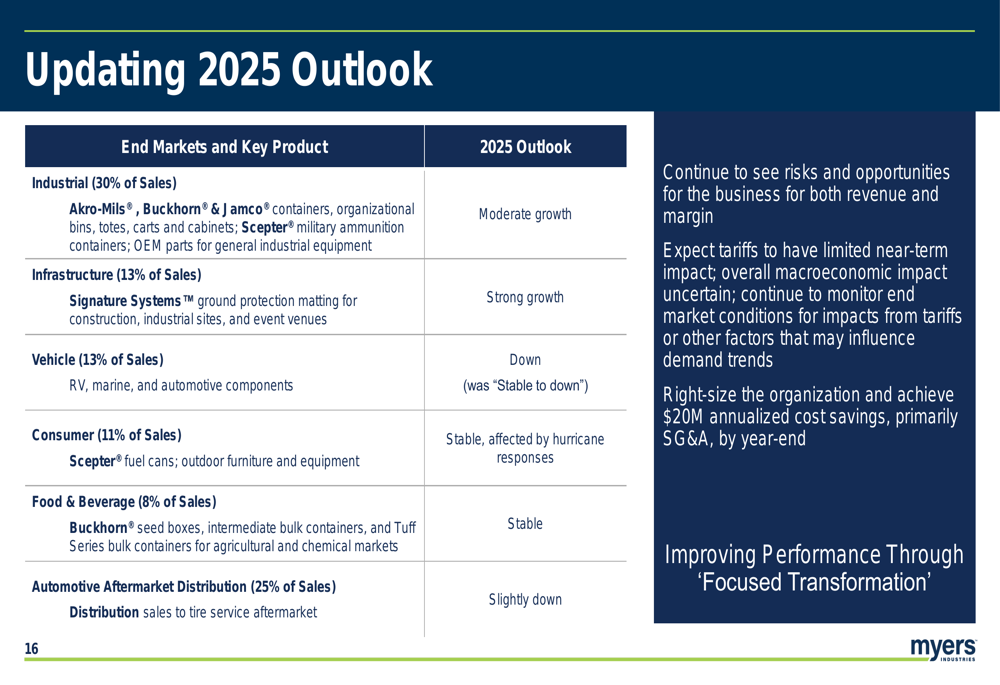

Looking ahead, Myers provided an updated outlook for 2025 by end market. The company expects moderate growth in Industrial (30% of sales) and strong growth in Infrastructure (13% of sales). However, it now forecasts the Vehicle market (13% of sales) to be down, a revision from its previous "stable to down" outlook.

Consumer (11% of sales) and Food & Beverage (8% of sales) markets are expected to remain stable, while the Automotive Aftermarket Distribution segment (25% of sales) is projected to be slightly down.

The following table details the company’s 2025 outlook by end market:

Management noted that it continues to see both risks and opportunities for the business regarding revenue and margin. The company expects tariffs to have limited near-term impact and remains focused on right-sizing the organization to achieve its targeted cost savings.

As Myers continues to navigate a mixed economic environment, its focus on operational efficiency, margin expansion, and strategic cost reductions appears to be yielding early positive results, despite the challenges in its Distribution segment and flat overall revenue growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.