Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

N-able Inc. (NYSE:NABL) released its Q2 2025 investor presentation on August 7, showcasing strong quarterly performance and an optimistic outlook for the remainder of the fiscal year. The cybersecurity and IT management solutions provider reported significant revenue growth and raised its full-year guidance, driving a 6.12% increase in premarket trading.

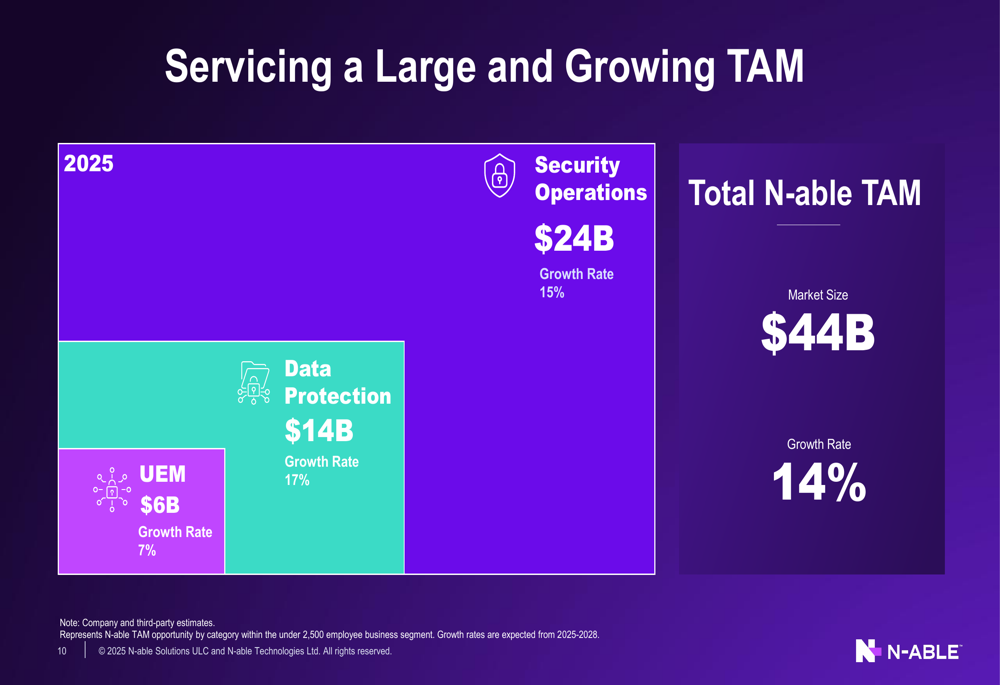

The company positions itself in a substantial addressable market, estimating the total SMB and mid-market IT spending at approximately $2.1 trillion in 2025. Within this broader landscape, N-able specifically targets a $44 billion total addressable market (TAM) growing at 14% annually, spread across security operations ($24B), data protection ($14B), and unified endpoint management ($6B).

As shown in the following chart of N-able’s target market segments and growth rates:

Quarterly Performance Highlights

N-able reported Q2 2025 revenue of $131 million, representing a 9% year-over-year increase. This performance exceeded analyst expectations and continues the company’s trend of consistent growth. The strong quarterly results follow a solid Q1 2025, where the company reported revenue of $118.2 million and earnings per share of $0.08, also surpassing Wall Street expectations.

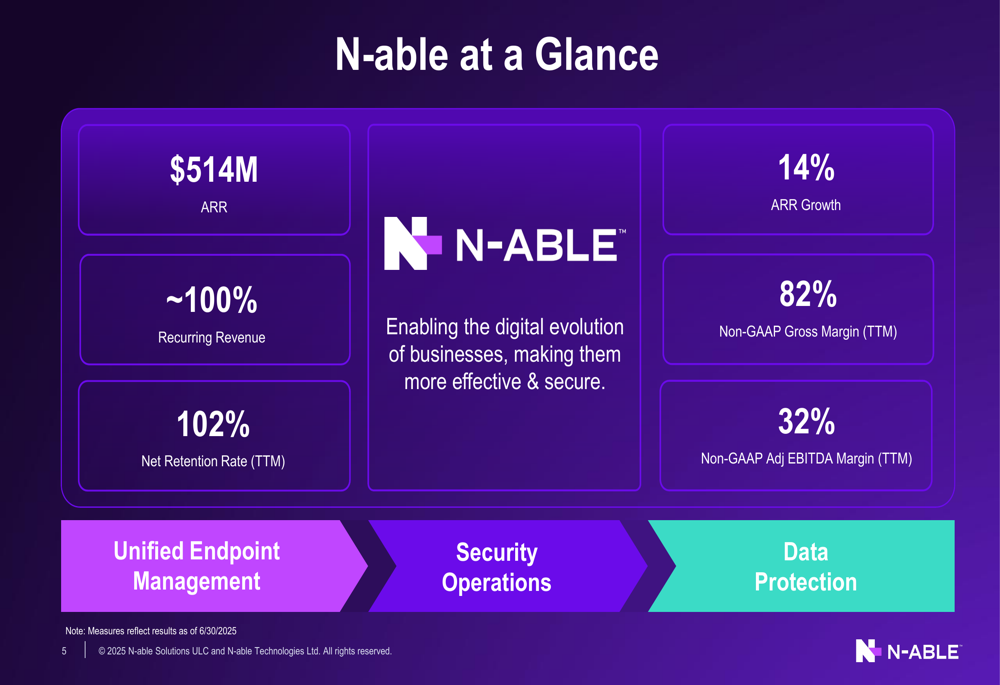

The company’s annual recurring revenue (ARR) reached $514 million as of June 30, 2025, showing 14% growth. Other key performance metrics include a net retention rate of 102% (trailing twelve months) and an impressive non-GAAP gross margin of 82%.

The following slide illustrates N-able’s key metrics and business segments:

N-able’s customer base continues to expand, with 2,540 customers now generating over $50,000 in ARR each, representing a 34% increase since 2022. Average revenue per customer has also grown substantially, reaching $19,400 in Q2 2025 compared to $15,000 in 2022.

Strategic Initiatives

N-able’s growth strategy centers on its unified cyber resilience platform, which integrates management, security, and recovery capabilities. The company’s approach addresses the expanding attack surfaces that SMBs and mid-market businesses face in today’s digital environment.

The comprehensive platform is illustrated in the following diagram:

A key component of N-able’s growth strategy is cross-selling across its product portfolio. The company identifies a substantial $2.5 billion cross-sell opportunity across its three main solution areas: Security Operations (~$1,400M), Data Protection (~$800M), and Unified Endpoint Management (~$300M).

N-able employs a channel-driven, one-to-many go-to-market model, leveraging distributors, value-added resellers (VARs), and managed service providers (MSPs) to reach SMB and mid-market customers. This approach allows the company to efficiently scale its reach while maintaining strong customer relationships.

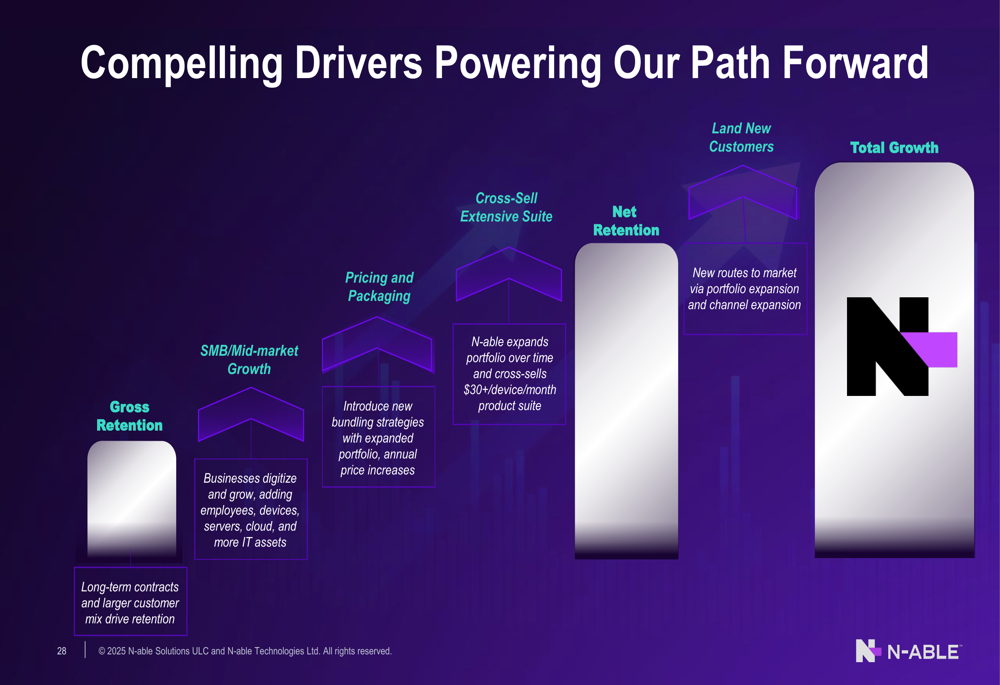

The company has identified multiple growth drivers, including improved gross retention through long-term contracts, enhanced pricing and packaging strategies, cross-selling additional products, and acquiring new customers. These strategies are designed to accelerate growth and improve financial performance.

As shown in the following growth strategy overview:

Detailed Financial Analysis

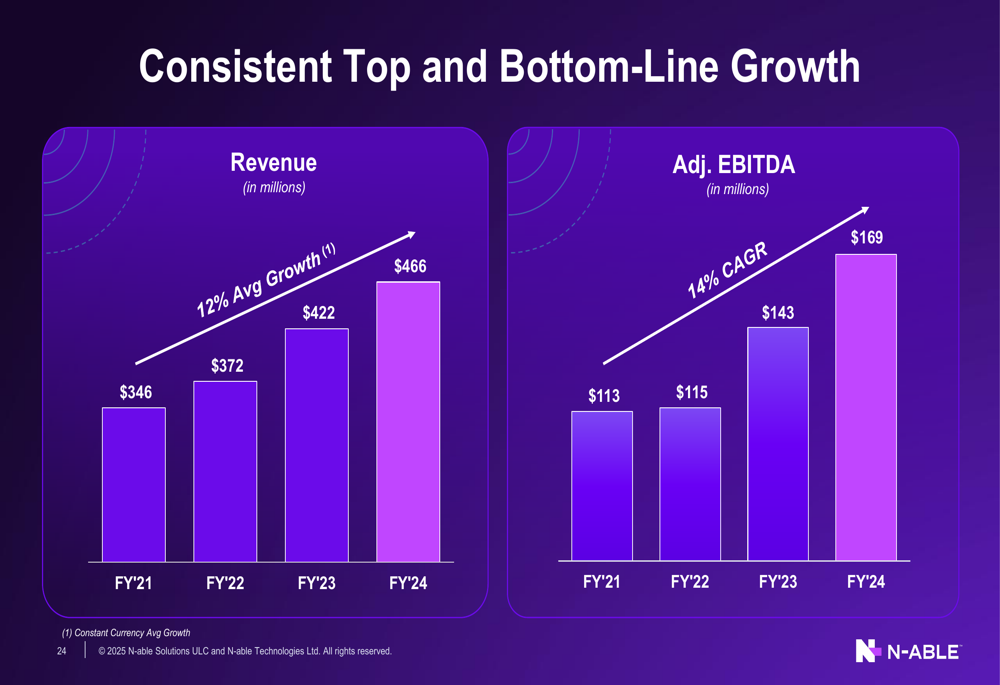

N-able has demonstrated consistent financial growth over recent years. Revenue increased from $346 million in FY’21 to $466 million in FY’24, representing a 12% average growth rate. Similarly, Adjusted EBITDA grew from $113 million to $169 million over the same period, reflecting a 14% compound annual growth rate (CAGR).

The following chart illustrates this consistent top and bottom-line growth:

Quarterly performance has also shown steady improvement, with revenue increasing from $94 million in Q3’22 to $131 million in Q2’25. Adjusted EBITDA margins have fluctuated somewhat, with Q2’25 showing a strong recovery to $42 million (32% margin) after a dip to $27 million (23% margin) in Q1’25.

The company maintains a highly predictable business model with approximately 100% recurring revenue. While net retention rates have declined slightly from 110% in 2023 to 101% in Q2’25, dollar-based retention has remained relatively stable between 85-88% during this period.

Forward-Looking Statements

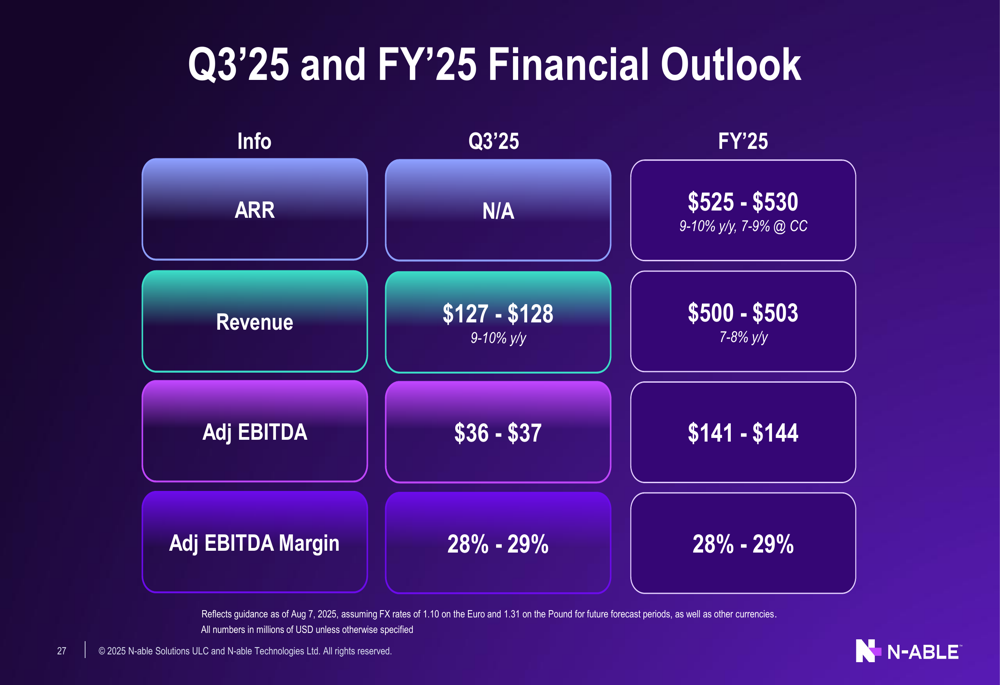

Based on its strong performance, N-able has raised its full-year 2025 guidance. The company now expects:

- ARR of $525-$530 million for FY’25, representing 9-10% year-over-year growth

- Revenue of $500-$503 million for FY’25, reflecting 7-8% year-over-year growth

- Q3’25 revenue of $127-$128 million, representing 9-10% year-over-year growth

- Adjusted EBITDA of $141-$144 million for FY’25, with margins of 28-29%

This revised guidance represents an increase from the previous outlook shared in Q1 2025, when the company projected full-year revenue of $492-$497 million.

The following slide details N-able’s financial outlook:

N-able’s investment thesis centers on four key points: servicing a large and growing market, offering differentiated products, employing an effective go-to-market strategy tailored for SMB/mid-market segments, and maintaining a disciplined and profitable business model that has achieved "Rule of 40+" performance (combined growth rate and profit margin exceeding 40%) every year since its spin-off from SolarWinds (NYSE:SWI).

As illustrated in the company’s investment thesis summary:

With its focus on cyber resilience solutions for SMB and mid-market customers, strong financial performance, and clear growth strategy, N-able appears well-positioned to capitalize on the expanding cybersecurity and IT management market. The positive market reaction to the Q2 results and raised guidance suggests investor confidence in the company’s strategic direction and execution capabilities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.