Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Qatar Gas Transport Company (DSM:QGTS), known as Nakilat, has released its financial results for the first half of 2025, showcasing resilient performance and strategic positioning in the growing global LNG shipping market. The company reported a 3.7% year-over-year increase in net profit despite a slight decrease in total income, highlighting its operational efficiency and strong business model.

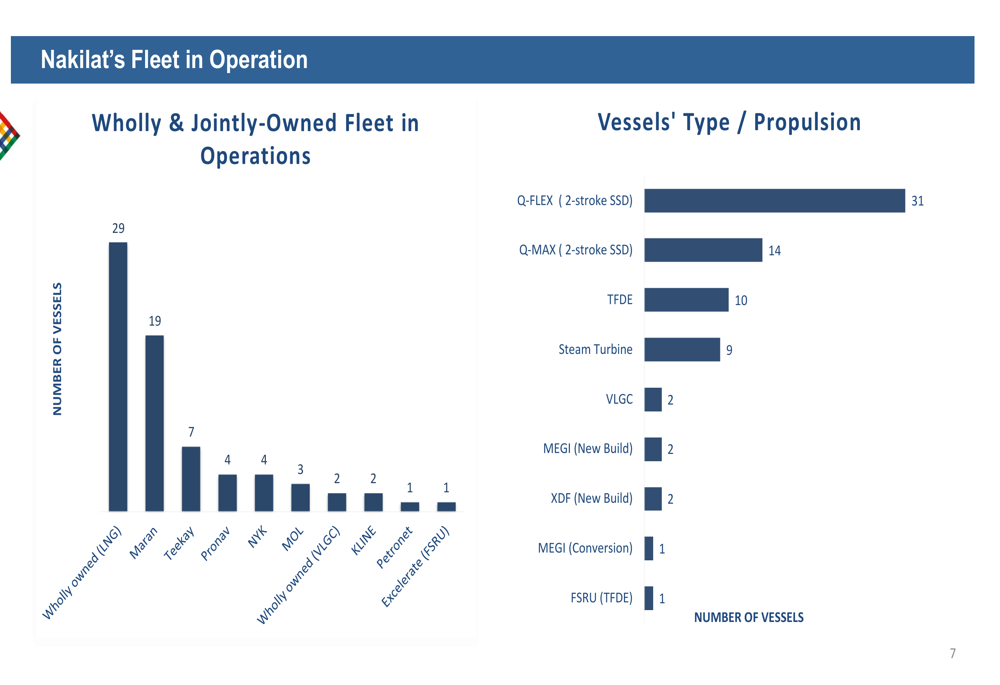

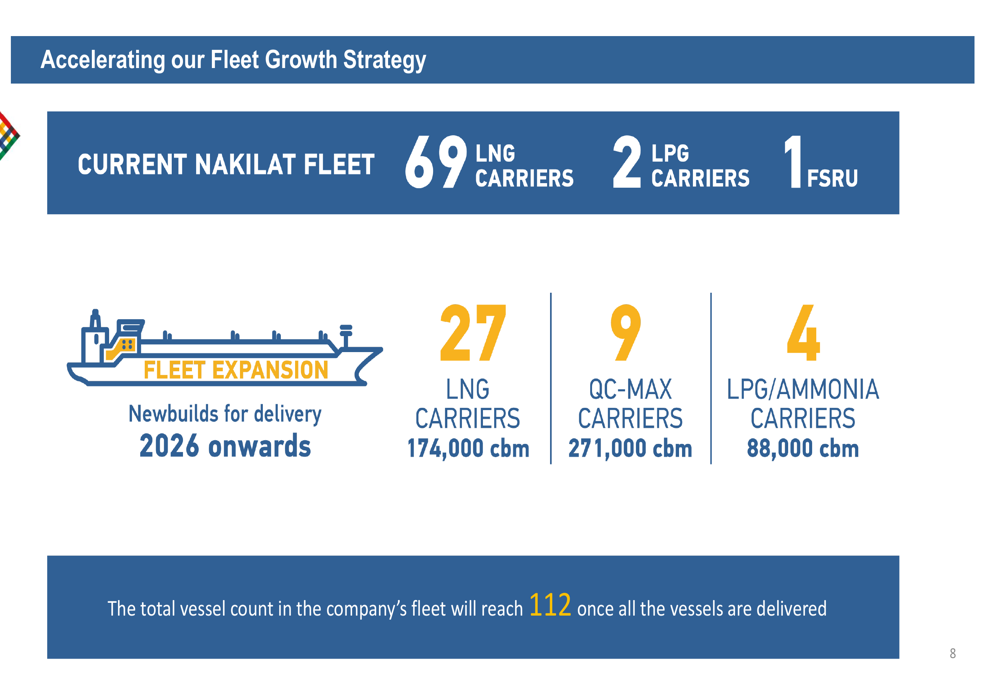

Nakilat continues to leverage its position as one of the world’s largest LNG shipping companies, with a current fleet of 69 LNG carriers, 2 LPG carriers, and 1 FSRU. The company is actively expanding its fleet to capitalize on projected growth in global LNG liquefaction capacity, which is expected to increase by 64% by 2030.

Financial Performance Highlights

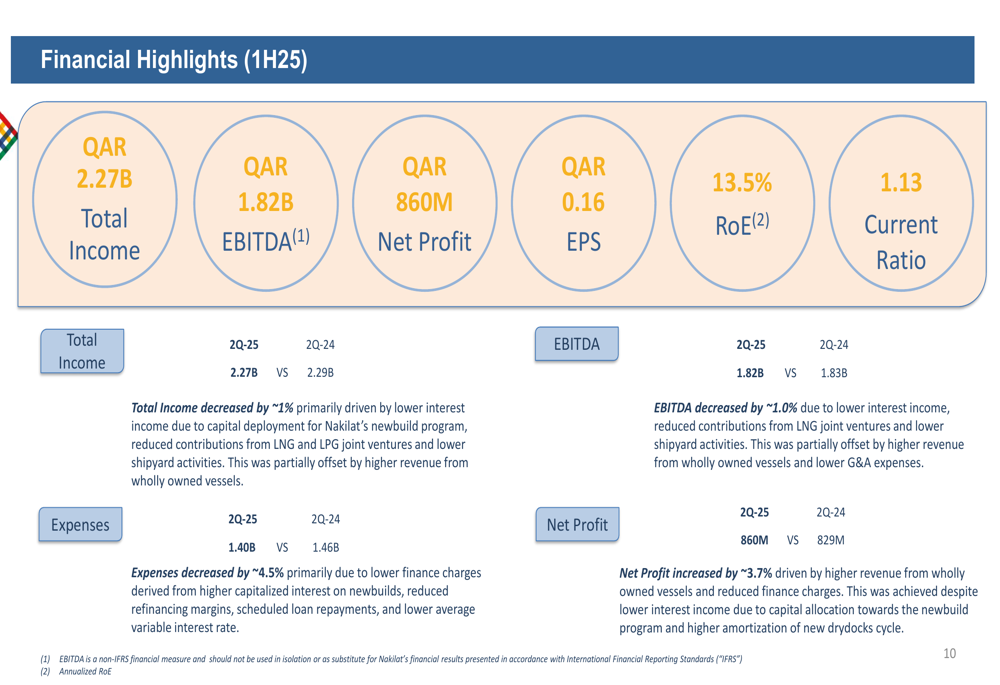

Nakilat reported a net profit of QAR 860 million for 1H25, representing a 3.7% increase compared to QAR 829 million in the same period last year. This growth was primarily driven by higher revenue from wholly owned vessels, despite a 1% decrease in total income to QAR 2.27 billion.

As shown in the following financial highlights:

The company’s EBITDA reached QAR 1.82 billion, showing a marginal decrease of approximately 1% compared to the previous year. Nakilat maintained strong profitability metrics with an earnings per share (EPS) of QAR 0.16 and return on equity (ROE) of 13.5%.

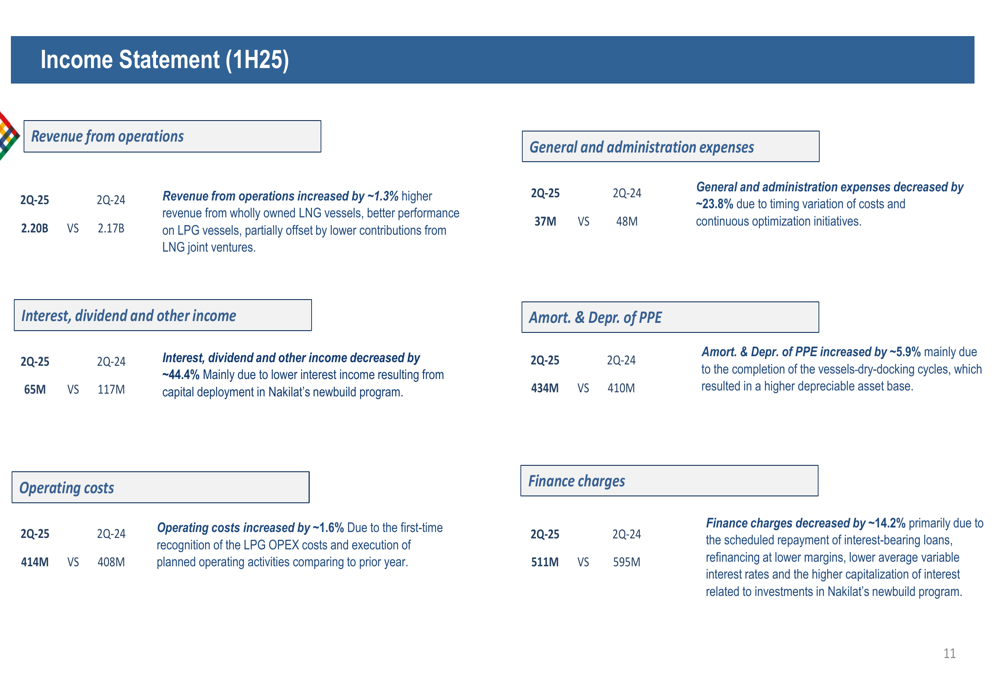

Operating expenses saw a modest increase of 1.6% to QAR 414 million, attributed to the first-time recognition of LPG operating expenses and planned operating activities. However, this was offset by significant reductions in other cost areas:

Finance charges decreased substantially by 14.2% to QAR 511 million, primarily due to scheduled repayment of interest-bearing loans, refinancing at lower margins, and lower average variable interest rates. General and administration expenses also decreased by 23.8% to QAR 37 million, reflecting timing variations of costs and continuous optimization initiatives.

Balance Sheet Strength and Debt Management

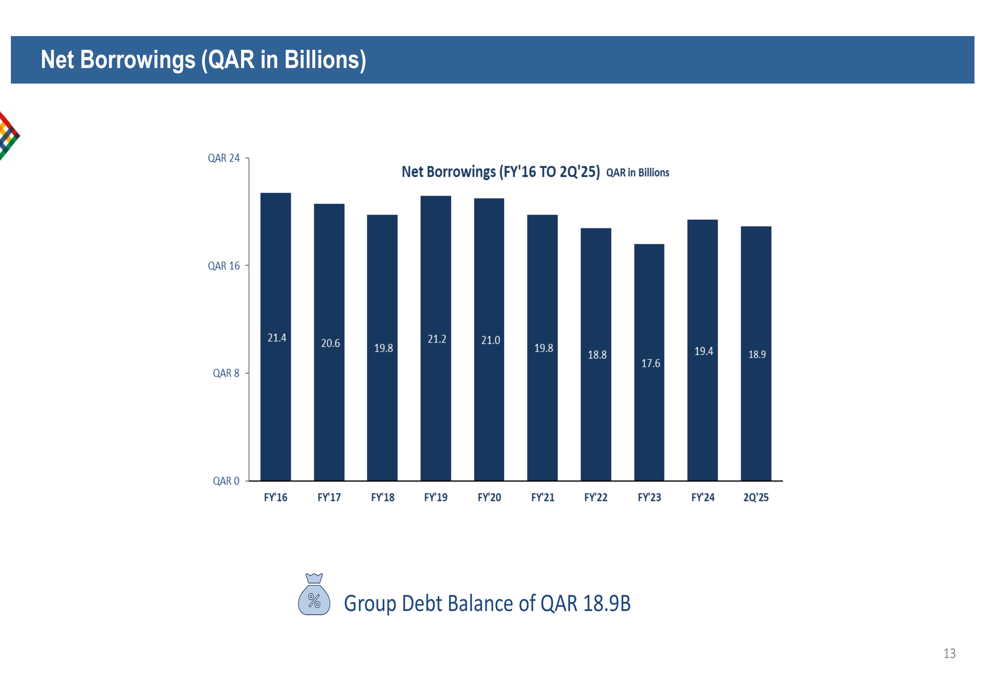

Nakilat has maintained a strong balance sheet with continued focus on debt reduction. As of June 30, 2025, the company’s borrowings decreased by 2.8% to QAR 18.90 billion, primarily due to scheduled loan repayments. The company’s cash and deposits balance stood at QAR 2.37 billion, down 9.5% from the previous period, reflecting capital deployment toward the newbuild program.

The following chart illustrates Nakilat’s consistent reduction in net borrowings over the years:

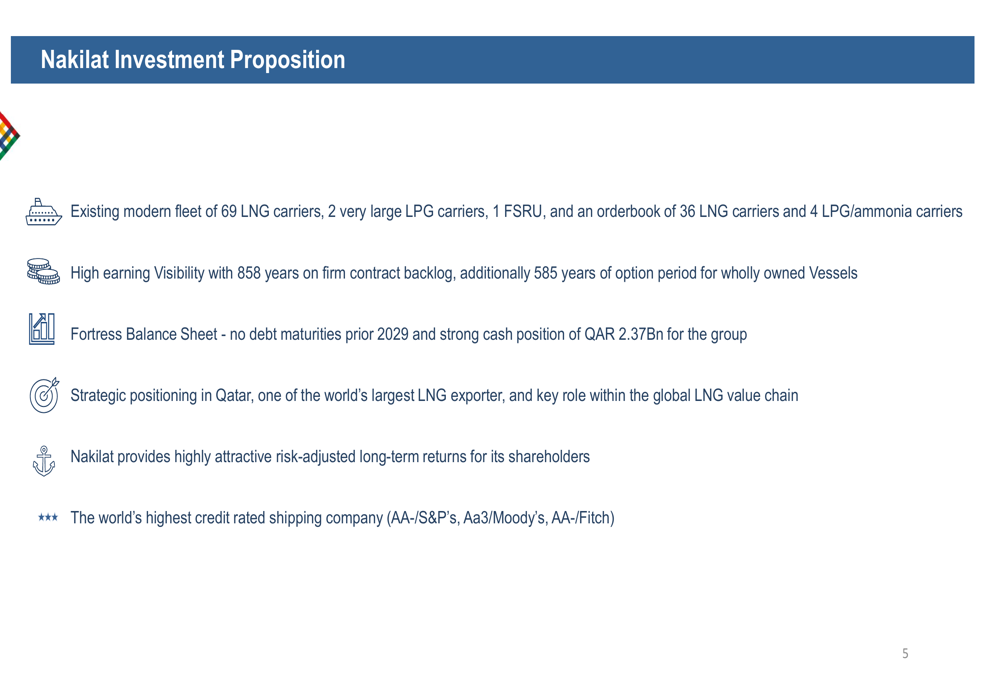

This disciplined approach to debt management has helped Nakilat maintain its status as the world’s highest credit-rated shipping company, with ratings of AA-/S&P’s, Aa3/Moody’s, and AA-/Fitch. The company’s strong financial position provides a solid foundation for its ambitious fleet expansion plans.

Fleet Composition and Expansion Strategy

Nakilat currently operates one of the world’s largest and most diverse LNG shipping fleets. The following chart provides a detailed breakdown of the company’s fleet composition:

Building on this strong foundation, Nakilat has embarked on an ambitious fleet expansion program that will significantly increase its capacity and market presence:

The expansion includes orders for 27 conventional LNG carriers (174,000 cbm), 9 QC-MAX carriers (271,000 cbm), and 4 LPG/AMMONIA carriers (88,000 cbm), bringing the total fleet to 112 vessels once all deliveries are completed. This strategic expansion positions Nakilat to capitalize on the growing global demand for LNG transportation.

Shareholder Returns and Dividend Policy

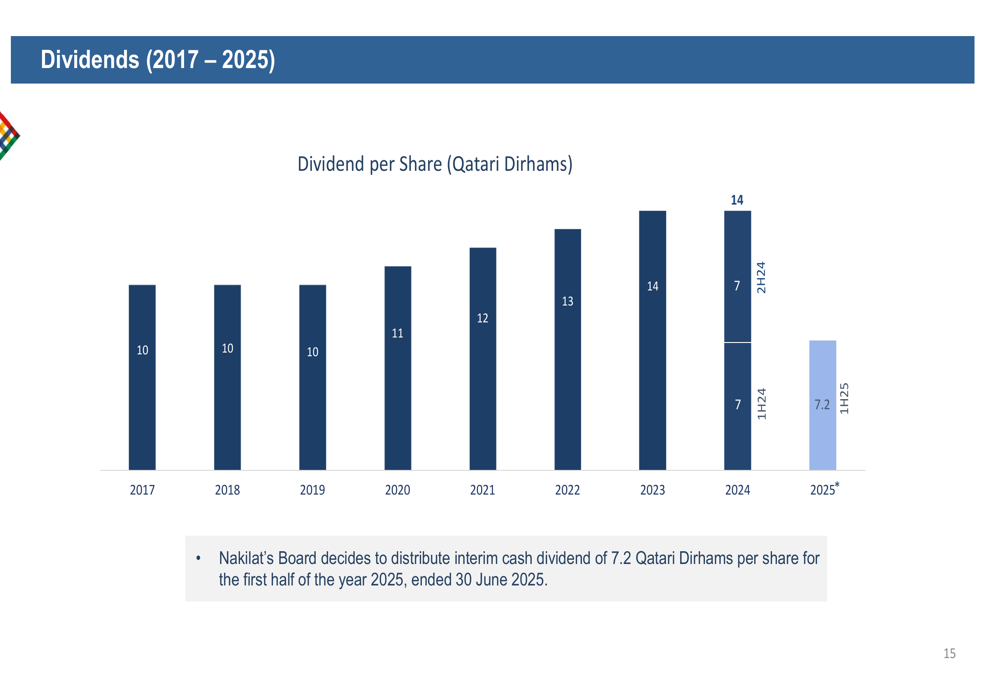

Nakilat continues to prioritize shareholder returns, announcing an interim cash dividend of 7.2 Qatari Dirhams per share for the first half of 2025. This reflects the company’s commitment to delivering value to shareholders while maintaining financial flexibility for future growth.

The following chart illustrates Nakilat’s consistent dividend distribution history:

LNG Market Outlook and Industry Positioning

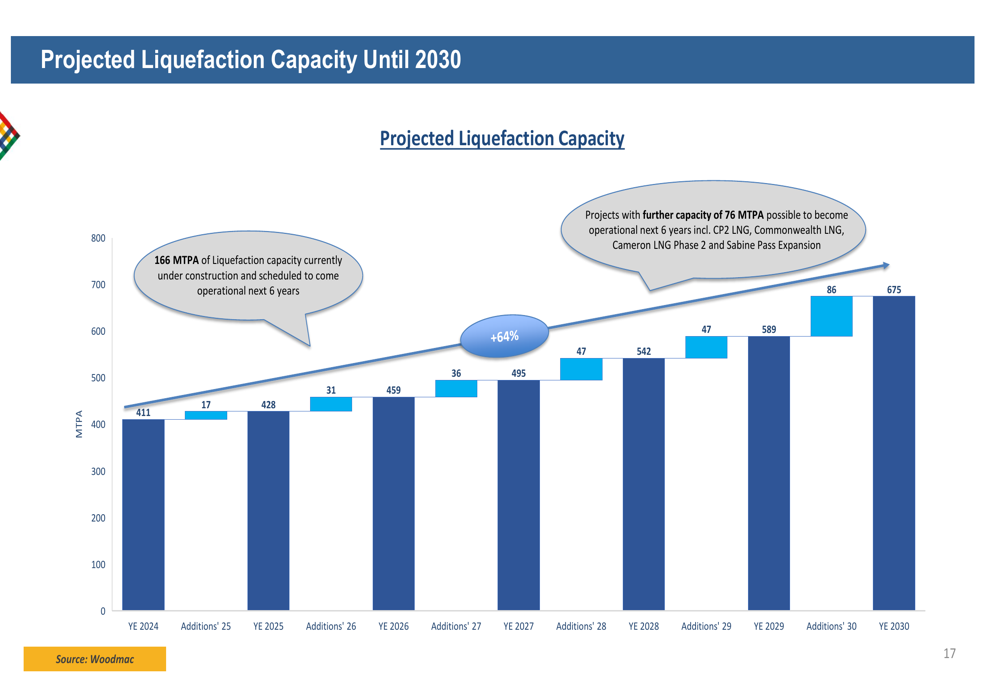

The global LNG market is projected to experience significant growth in the coming years, creating substantial opportunities for Nakilat. According to the presentation, global liquefaction capacity is expected to increase from 411 MTPA in 2024 to 675 MTPA by 2030, representing a 64% growth:

This projected growth in LNG production capacity will drive increased demand for LNG transportation services, aligning perfectly with Nakilat’s fleet expansion strategy. The company’s long-term contracts provide stable revenue streams, with 858 years on firm contract backlog and an additional 585 years of option periods for wholly owned vessels.

Strategic Initiatives and Forward-Looking Statements

Nakilat’s investment proposition remains compelling, built on several key strengths:

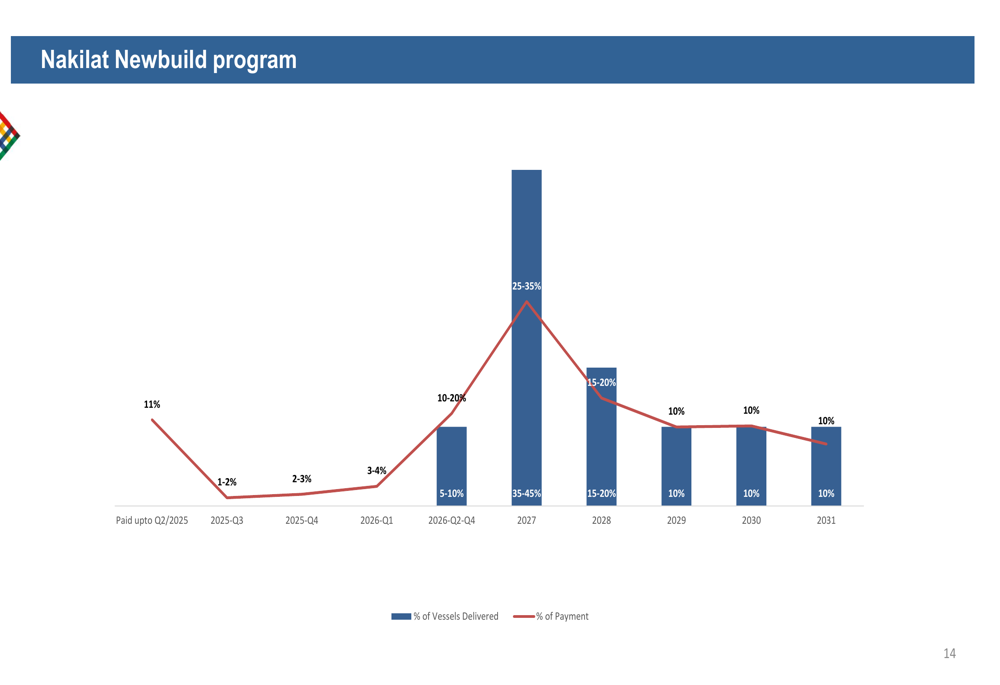

Looking ahead, Nakilat remains focused on maximizing shareholder returns while pursuing sustainable growth opportunities. The company’s newbuild program is structured with payments spread over several years, with the majority of payments scheduled for 2027-2031:

Conclusion

Nakilat’s 1H25 financial results demonstrate the company’s resilience and strategic positioning in the global LNG shipping market. Despite a slight decrease in total income, the company achieved profit growth of 3.7%, driven by higher revenue from wholly owned vessels and lower finance charges.

With a strong balance sheet, decreasing debt levels, and an ambitious fleet expansion program, Nakilat is well-positioned to capitalize on the projected 64% growth in global LNG liquefaction capacity by 2030. The company’s focus on operational efficiency, strategic fleet expansion, and shareholder returns underscores its commitment to long-term value creation in a growing market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.