Trump meets Zelenskiy, says Putin wants war to end, mulls trilateral talks

Introduction & Market Context

Nature’s Sunshine Products Inc (NASDAQ:NATR) released its first quarter 2025 earnings presentation on May 6, showcasing significant profit growth despite modest revenue increases. The nutritional products company reported that net income more than doubled year-over-year, highlighting improved operational efficiency amid varying regional performance.

The company’s stock closed at $12.50 on the day of the announcement, down 0.72%, and continues to trade near the lower end of its 52-week range of $10.81 to $19.28. This performance follows a pattern seen after the company’s Q4 2024 results, when the stock declined despite exceeding revenue forecasts, suggesting continued investor caution despite improving fundamentals.

Quarterly Performance Highlights

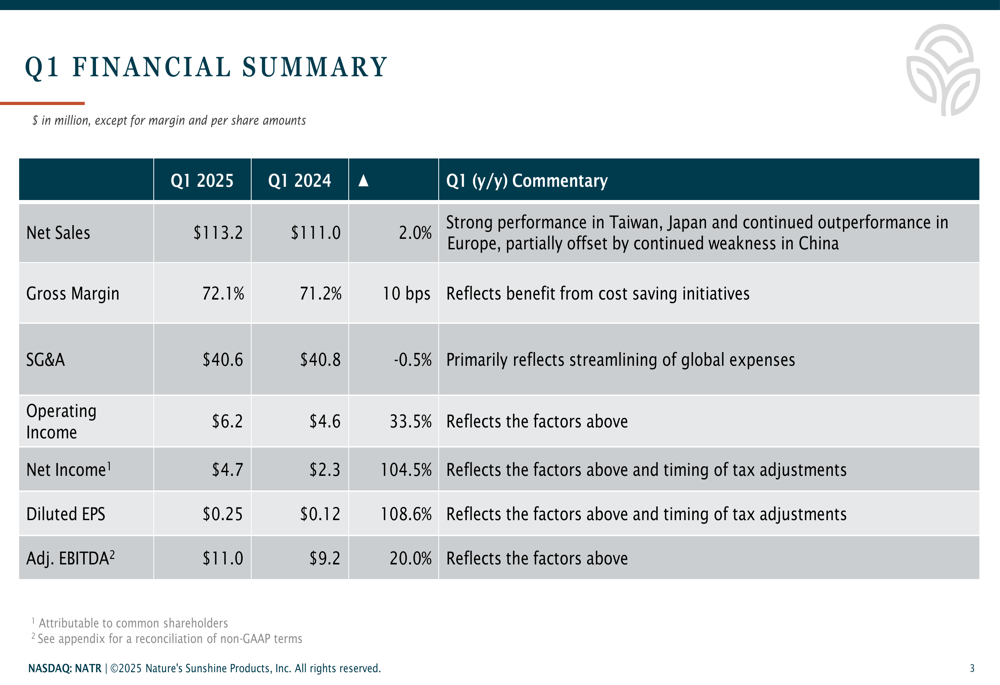

Nature’s Sunshine reported Q1 2025 net sales of $113.2 million, representing a 2.0% increase compared to the same period last year. When excluding currency impacts, the growth rate was more substantial at 4.5%. The modest top-line growth was accompanied by impressive bottom-line improvements, with net income surging 104.5% to $4.7 million and diluted earnings per share more than doubling to $0.25, up 108.6% year-over-year.

As shown in the following financial summary from the company’s presentation:

The company’s gross margin improved slightly to 72.1%, while operating income jumped 33.5% to $6.2 million. Adjusted EBITDA increased by 20.0% to $11.0 million, reflecting the company’s focus on operational efficiency and cost control. The presentation highlighted that these improvements were driven by cost-saving initiatives and the streamlining of global expenses.

Regional Performance Analysis

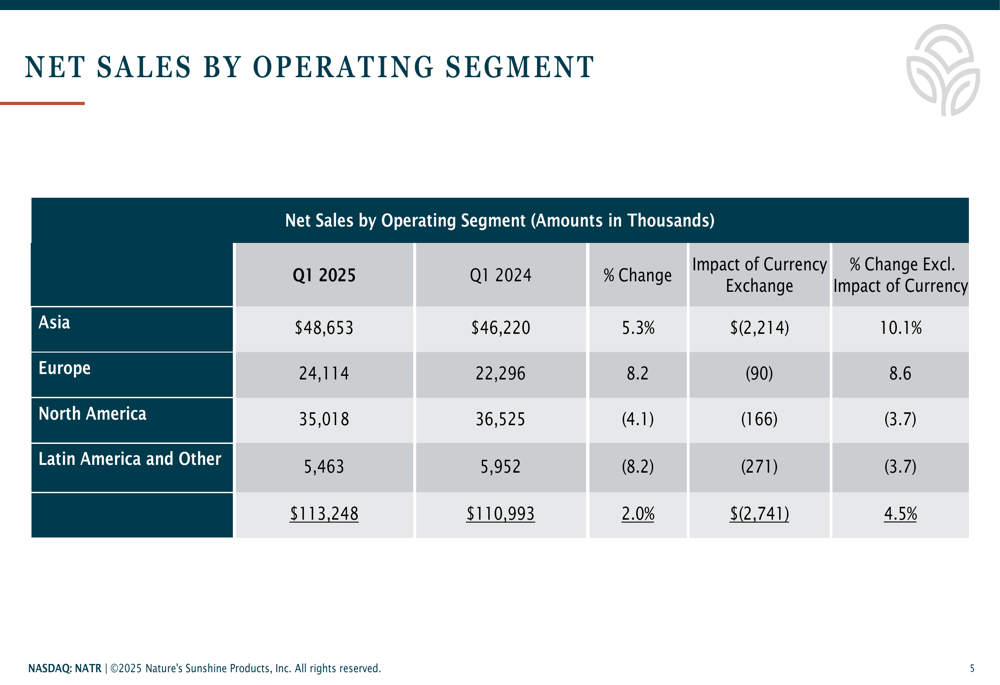

Nature’s Sunshine’s overall performance was marked by significant regional variations. Strong results in Asia and Europe were partially offset by continued challenges in North America and Latin America.

The following breakdown illustrates the regional performance disparities:

The Asia segment led growth with sales of $48.7 million, up 5.3% year-over-year, or 10.1% when excluding currency impacts. The company specifically highlighted strong performance in Taiwan and Japan, though noted continued weakness in China. Europe also performed well, with sales increasing 8.2% to $24.1 million.

In contrast, North America saw a 4.1% decline to $35.0 million, while Latin America and other markets decreased by 8.2% to $5.5 million. These regional challenges mirror trends observed in previous quarters, as the Q4 2024 earnings report had also noted North American sales declines despite overall company growth.

Balance Sheet Strength & Capital Allocation

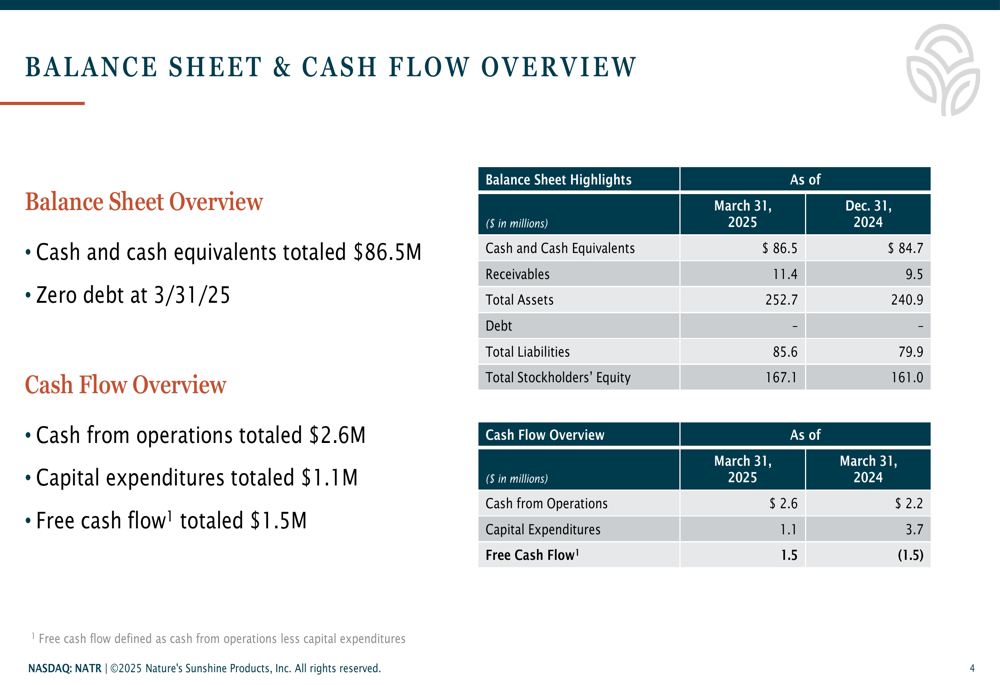

Nature’s Sunshine maintained a strong financial position with $86.5 million in cash and cash equivalents and zero debt as of March 31, 2025. The company generated $2.6 million in cash from operations during the quarter and reported free cash flow of $1.5 million after $1.1 million in capital expenditures.

The company’s solid balance sheet is illustrated in the following slide:

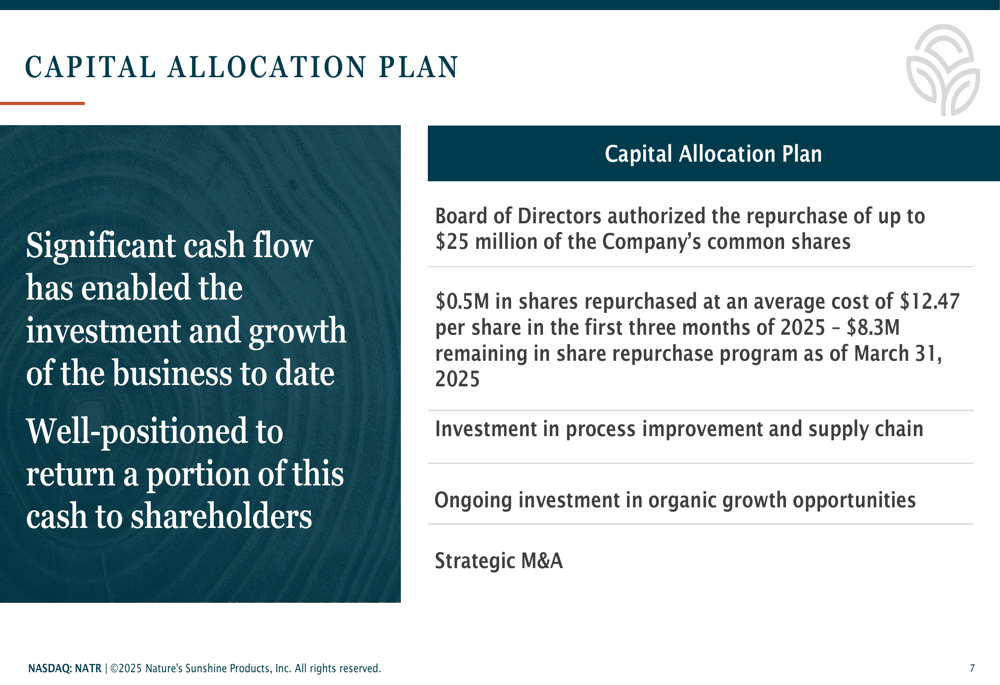

This financial strength has enabled Nature’s Sunshine to implement a shareholder-friendly capital allocation strategy. The Board of Directors has authorized a $25 million share repurchase program, with $0.5 million in shares already repurchased at an average cost of $12.47 per share during the first quarter of 2025.

The company’s capital allocation priorities are outlined below:

Beyond share repurchases, Nature’s Sunshine is focusing on process improvements, supply chain investments, organic growth opportunities, and potential strategic acquisitions, leveraging its debt-free balance sheet to fund these initiatives.

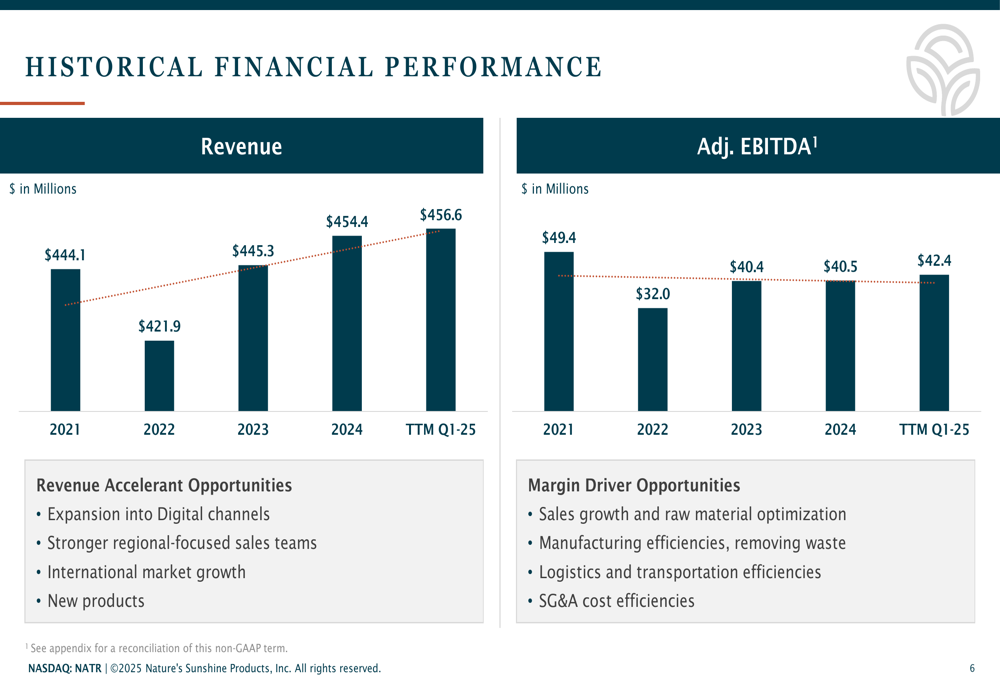

Historical Performance & Future Outlook

Nature’s Sunshine’s Q1 results continue a pattern of steady revenue growth and improving profitability over recent years. The company’s trailing twelve-month revenue reached $456.6 million, while adjusted EBITDA for the same period was $42.4 million, showing gradual improvement from previous years.

The following chart illustrates the company’s long-term performance trajectory:

Looking forward, Nature’s Sunshine has identified several growth opportunities, including expansion into digital channels, stronger regional-focused sales teams, international market growth, and new product development. The company also highlighted margin improvement opportunities through raw material optimization, manufacturing efficiencies, logistics improvements, and SG&A cost efficiencies.

These initiatives align with the guidance provided after Q4 2024, when the company projected 2025 net sales between $445 million and $470 million and adjusted EBITDA of $38 million to $44 million. The current trailing twelve-month figures suggest Nature’s Sunshine is on track to meet these targets, though management had previously noted a conservative outlook due to potential tariff impacts and macroeconomic uncertainties.

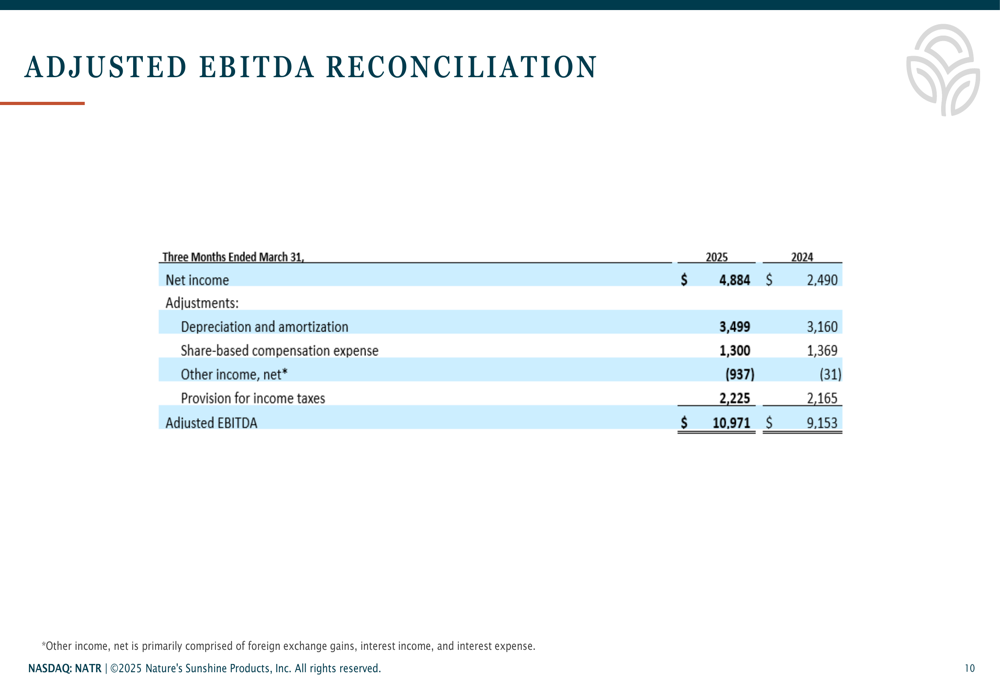

The detailed reconciliation of adjusted EBITDA, which provides insight into the company’s operational performance excluding non-recurring items, is presented in the following slide:

With its strong balance sheet, improving profitability metrics, and strategic focus on both regional growth and operational efficiency, Nature’s Sunshine appears positioned to continue its positive momentum despite the challenges in certain markets. However, investors remain cautious, as reflected in the stock’s current trading level relative to its 52-week high, suggesting concerns about sustained growth in an uncertain macroeconomic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.